In the universe of higher yield stock investing, often no news is good news. Income stock investors want to own shares that pay steady dividends from companies that can be counted on to earn enough to cover the dividends quarter after quarter.

Stock market drama usually leads to share price volatility, which is something that makes dividend investors uncomfortable. As a result, often the best dividend stocks don’t make much news in the financial news, which makes it harder for investors to find them.

One group that gets little press but pays steady dividends and attractive yields are the small cadre group of commercial mortgage finance real estate investment trusts (REITs).

REITs are divided into two broad categories. Equity REITs own commercial properties. They earn revenue from rent or lease payments. Finance REITs originate or own portfolios of real estate secured loans. The residential focused REITs usually own highly leveraged portfolios of mortgage-backed securities (MBS).

Commercial finance REITs typically originate loans on commercial properties and hold them in their own portfolios. Commercial finance REITs contrast starkly compared to the more popular residential MBS owning REITs. They are less leveraged, financially more conservative, and have better dividend track records.

Commercial finance REITs are lower risk and historically have been more stable dividend payers. Commercial mortgages are typically done with variable interest rates, and commercial REITs match their loans with variable debt. They lock in the interest rate spreads, no matter which way interest rates move. These REITs also use a lot less leverage than their residential MBS owning cousins.

If you are looking for 7% to 8% yields where you can count on the dividends for years to come, consider commercial finance REITs. Here are three that I’ve been following for years to get you started.

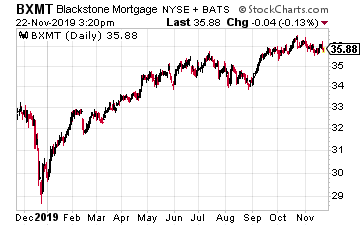

Blackstone Mortgage Trust, Inc. (BXMT) is a pure commercial mortgage lender. The REIT receives high-quality mortgage lending leads from its sponsor, The Blackstone Group L.P. (BX).

As of its 2019 third-quarter earnings, BXMT had a $16.4 billion portfolio of senior mortgage loans.

In the quarter, the company originated $3.7 billion of new senior loans and received about $3 billion of principal paybacks. 94% of the portfolio is floating rate.

The loans were at 62% loan to the value of the underlying properties. Leverage is 2.8 times debt to equity.

The stock currently yields 6.8%.

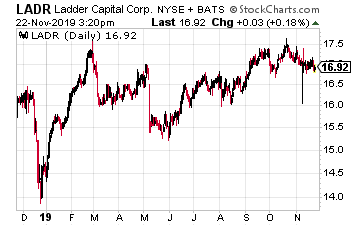

Ladder Capital Corp (LADR) uses a three-prong approach to its investment portfolio. The three legs are commercial mortgage loans, with a current $3.4 billion portfolio of floating and fixed-rate loans, commercial real estate equity investments, valued at $981 million, and commercial MBS bonds, worth $1.9 billion.

The business plan is that the three groups cycle to more or less attractive through the commercial real estate cycle, each being more attractive at different phases of the cycle.

Leverage is a comfortable 2.6 times.

Since it paid its first dividend for Q1 2015, Ladder has steadily increased the quarterly payout at an average 5% annual growth rate.

The shares currently yield 8.0%.

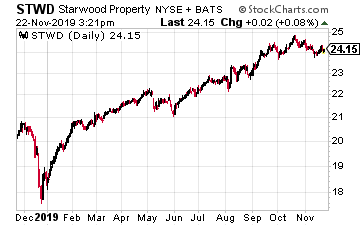

Starwood Property Trust, Inc. (STWD) is one of the largest commercial lenders of any business type – including banks. The company currently has an $8.0 billion loan portfolio with a 65% loan to value.

Since launching in 2009, the company has deployed over $40 billion in loans and investments with zero realized losses.

In recent years, Starwood has acquired the largest commercial mortgage special servicer. This acquisition has led to growth in CMBS origination and investments.

The company also owns a $2.7 billion equity commercial property portfolio that generates 9% to 12% cash on cash returns. Recently Starwood has invested in non-agency residential MBS.

The $1.2 billion RMBS portfolio has a 68% loan to value. Management constantly looks for investment opportunities both in and out of the commercial mortgage business.

Get your hands on my most comprehensive, step-by-step dividend plan yet. In just a few minutes, you will have a 36-month road map that could generate $4,804 (or more!) per month for life. It's the perfect supplement to Social Security and works even if the stock market tanks. Over 6,500 retirement investors have already followed the recommendations I've laid out.

I’m going to show you my favorite (perfectly legal) way to pay 0% tax on your dividend income.

To show you the big savings this could mean, let’s look at two fictional investors who are nearing retirement: Jane and Janet.

We’ll assume both are single, are earning $50,000 per year and live in a state with no income taxes. Now let’s assume Janet has taken the so-called “right” path, as suggested by her financial advisor, while Jane has steered her own course. A quick look at both will show how that “right” path can create a hefty tax problem.

Let’s say Janet put a million dollars in the Vanguard S&P 500 ETF (VOO) because she’s been told that a low-cost index fund is best for retirement. VOO is giving her $14,100 in annual dividends as a result, but because Janet is still working, she’ll have to give Uncle Sam $1,864 in taxes on her dividends for just one year—and that doesn’t include tax she’ll pay when she eventually sells her shares.

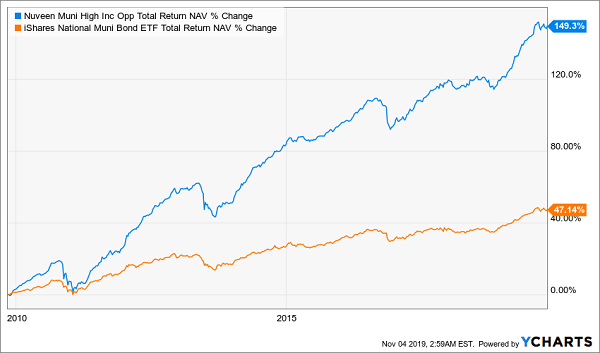

Over to Jane. Instead of following the herd and buying VOO, she’s put her million in a lesser-known fund called the Nuveen Municipal High Income Opportunity Fund (NMZ), which pays a 5% dividend yield, giving her an income stream of $50,000 from her investment. Not only is her nest egg now entirely replacing her work income, but she’s also getting all of it.

That’s right. Of that $50,000 a year NMZ is giving Jane, zero is going to Uncle Sam. And it doesn’t matter if she gets a promotion at work and makes more, or if NMZ starts paying her more (which it did for its shareholders at the start of the year; more on that later).

She will not have to pay any of her income from this fund to the tax man.

Of course, the more Janet gets paid, the more taxes she’ll have to pay out. If her work pay rises 20%, for instance, the tax on her dividends will climb to $2,115 per year, meaning her tax burden has gone up by almost as much as her raise!

Municipal Bonds: Your Tax-Free Income Option

Municipal bonds, the investments NMZ holds, are popular because they’re one of the few ways Americans can legally get paid without having to pay taxes. It’s all thanks to a 1913 law exempting municipal bonds from federal income tax. Since then, investors have been using “muni” bonds to generate a high income stream—and keep all of it.

Dispelling the Biggest Muni Myth

How popular are muni bonds? Right now, the market is worth nearly $4 trillion in the US, which is about 13% of the size of the total stock market. Considering municipalities aren’t in the business of making a profit, it’s surprising that muni bonds are as big as they are.

While many muni bonds are gobbled up by wealthy investors looking to cut out the tax man, the middle class often ignores them. One reason why is fear: headlines about municipalities going bankrupt and leaving investors in the cold result in paranoia—and many bad investment decisions.

Here are the facts: according to Moody’s, the total default rate of muni bonds since 1970 is 0.09%. In other words, for every 10,000 muni bonds issued, nine go into default. Put another way, you’re 1,442 times more likely to get in a car crash than to hold a muni bond that defaults.

The Power of Diversification

Here’s another crucial point: when a municipality defaults, it doesn’t mean investors get nothing. In reality, municipalities will restructure their debts on new terms, which could mean a small loss for bondholders. But one way to limit this risk even further is to hold a fund like NMZ.

With $1.5 billion in assets, NMZ can diversify across many bonds (it currently holds 598 of them) to slash the risk of being exposed to a default.

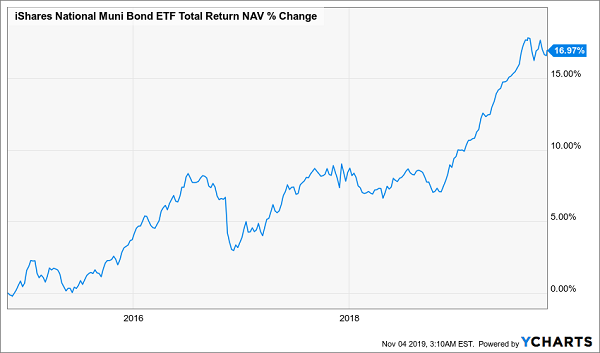

This doesn’t just make NMZ safer, it’s also made the fund’s returns impressive. Thanks to NMZ’s unique market access and expertise, it’s crushed a muni-bond index fund like the iShares National Muni Bond ETF (MUB), in orange below.

The Power of Diversification—and Expert Management

It’s rare to get superior returns and greater safety, but NMZ delivers both.

Finally, a Word on Rates

There’s one last reason why Jane would be smart to buy NMZ: the Federal Reserve.

In 2019, the Fed cut interest rates three times, which has had two effects on muni bonds. The first is that they’re more attractive to investors than before. From 2015 to the start of 2019, when the Fed was raising interest rates, muni bonds were struggling to make headway, as you can see in the chart below:

Rising Rates a Drag on Munis—Until 2019

There are two reasons why munis stalled in this period: first, many investors thought they could get higher income streams elsewhere as rates rose. Second, and more important, bonds fall in value as interest rates go up, which meant the resale value of these bonds dropped with the Fed’s aggressive rate-hike cycle.

Fortunately, the opposite is also true: lower rates mean muni bonds go up, which is why you see that huge hockey stick at the end of the chart above. It’s also why NMZ raised its dividend earlier in 2019, and why it may raise it again. The Fed’s aggressive rate cuts have been a blessing for munis this year, and with the central bank likely to continue lowering rates, that hockey stick will get bigger.

5 Huge 8.8% Dividends That Fit Perfectly With NMZ

NMZ is just the start: now, I want to give you 4 more funds that hand you a much bigger dividend payout—I’m talking a blockbuster 8.8% average yield.

PLUS, these funds are so cheap now, they’re “spring-loaded” for 20%+ price upside in 2020.

So if, say, you invested $400K in this diversified collection of income powerhouses, you’d be looking at $35,200 in dividend cash by November 2020—and $80,000 in price gains too!

But these 4 income plays won’t be cheap for long—especially with the Fed determined to keep cutting rates, which will drive more income-starved investors into the CEF market.

Dividend yields are so low today that dividend growth is actually becoming cool. Income investors are combing over “Dividend Aristocrats”–stocks that have raised their payouts for 25 straight years–in desperation to find any meaningful yield.

Problem is, these stocks are so popular and richly valued that they don’t pay much today. Nor will they yield much more tomorrow, even with yearly raises. Our princely picks pay less than 2% today, which is going to net you less than $20,000 on a million bucks.

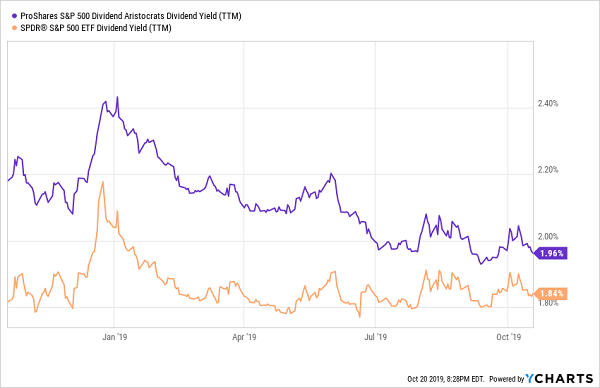

Dividend Aristocrat Yields Head Towards Zero

The Dividend Aristocrats are the well-worn, oft-recommended dividend growers of the S&P 500. All 57 Aristocrats have improved the amount of their total annual payouts every year for at least 25 years (and in many cases, they have done it for much longer.)

Yes, reliably increasing income matters. After all, the dividend-growth strategy in my Hidden Yields product is roughly doubling our money every four years with a 17%+ yearly return since inception.

But the Aristocrats are starting with too much of a handicap. As you can see above, the ProShares S&P 500 Dividend Aristocrats ETF’s (NOBL) yield is better than the market, but still below 2%.

The actual average among all 57 components isn’t much better, at 2.4%. In fact, only 13 components yield more than 3%. And just two—AT&T (T) and AbbVie (ABBV)—yield more than 5%.

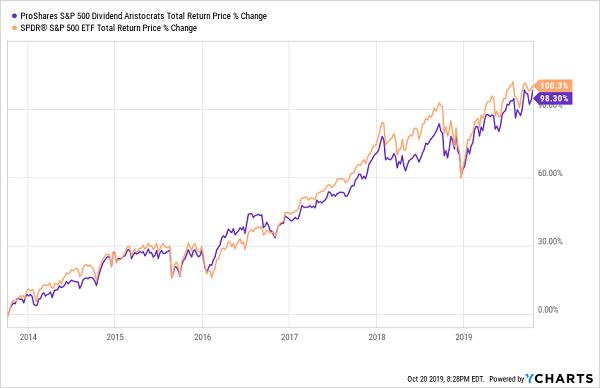

That’d be OK if we were sacrificing high nominal yields for great price performance, but we’re not. In fact, NOBL has actually underperformed the S&P 500 since 2013 inception.

My take? Cherry pick ‘em. A few Aristocrats are truly royalty among the entire world of publicly traded stocks. Others actually have promising growth prospects that you wouldn’t expect from supposedly stodgy dividend plays.

Let’s look at a six-pack of the best and worst Dividend Aristocrats together.

McCormick & Co. (MKC) Dividend Yield: 1.4%

Let’s start with McCormick & Co. (MKC), a frequent cupboarder in American kitchens. Whether it’s the namesake spices, Old Bay seasoning, Stubb’s barbecue sauce, Zatarain’s rice mixes, French’s mustard or Frank’s Red Hot, our food has often been flavored up by its products.

In fact, you probably enjoy McCormick more often than you realize, given that it also provides spices and condiments to restaurants. Overseas, too, as its international reach spans roughly 150 countries and territories.

All this makes McCormick & Co. a recession-resistant play hiding in your pantry corner. When times are tight, folks eat out less and prepare more food at home.

Check out our last mega-recession as an example. While the S&P 500 was trashed during the bear market of 2007-09, MKC managed to tread the boiling water for most of the downturn:

Bam!

Its dividend, which has improved for 33 consecutive years, has grown by a nice 43% since the start of 2015. But it yields less than a 10-year T-note today, which is not good enough for us income seekers.

Franklin Resources (BEN) Dividend Yield: 3.8%

Franklin Resources (BEN), the name behind the Franklin Templeton investment firm, has expanded its payout for 37 years. Recently shares have jumped 73% since the start of 2015 plus the firm dished a generous $3-per-share special dividend at the start of 2018 as a way of giving back after the passage of the Tax Cuts and Jobs Act. That translated into an additional 9 percentage points of yield for the year!

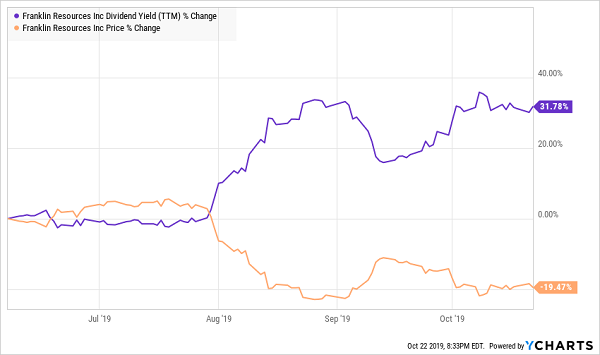

However, Franklin’s yield has recently rocketed higher for the wrong reasons. Its business is in the tank, and the dividend looks increasingly dicey as a result.

In June, I highlighted BEN as one of several “zombie dividends” to sell. The company has been suffering from dwindling assets under management for years, and it was way behind the curve with ETFs, finally launching its first suite of passive products in 2017. Since we called out this loser, it quickly dropped 20%:

The Wrong Way to Increase Yield

Walmart (WMT) Dividend Yield: 2.8%

Walmart (WMT) is one of the few retailers that can compete with (and potentially topple) Amazon.com. Sales through Walmart’s website and mobile app are booming. Its e-commerce revenue is growing at a brisk 43% clip year-over-year.

In my college days at Cornell we operations research and industrial engineers (ORIE) actually studied Walmart’s supply chain. It was one of the finest examples of ORIE applied to market domination. “Wally World” is one of the few retailers positioned to compete with Jeff Bezos and Amazon on same-day delivery, thanks to its logistics expertise and deep bench of brick and mortar locations. Really the firm is one partnership with Uber away from getting you anything you want within the hour.

Clorox (CLX) is a consumer staple that needs no introduction. But to get an idea of just how wide its reach is, understand that Clorox is far more than just Clorox. It’s also Pine-Sol, Brita water filters, Fresh Step cat litters, Glad trash bags, Liquid Plumr, Burt’s Bees lip balms and even Hidden Valley ranch sauces.

These are durable brands that have no-brainer recession appeal. But the company is taking a decided step back.

Earlier this month, Clorox presided over a dour analyst meeting in which it cut its full-year guidance from $6.50-$6.30 per share to $6.25-$6.05 per share. That led to several price-target downgrades, including by JPMorgan’s Andrea Teixeira (Underweight rating), who trimmed her outlook from $143 per share to $137. What’s particularly concerning is she sees additional downside earnings risk.

There’s little criticizing CLX’s dividend growth. Payouts have been on the rise for 42 consecutive years, and have improved 43% since the start of 2015.

But the sub-3% yield is nothing to fawn over, especially given Clorox’s growth issues. It’s also curiously priced at 23 times profits.

Clorox’s (CLX) Merely Market-Matching Performance Could Slow Even More

Dover (DOV) Dividend Yield: 1.9%

Near the end of 2018, I told Market Wrap host Moe Ansari that the key to finding potential doublers is to home in on boring stocks.

And Dover (DOV) is a publicly traded bottle of ZzzQuil.

Dover is a diversified industrial that makes everything from product-tracing technologies to bench tools to chemical dispensing systems and even commercial refrigeration units. That kind of revenue diversification always keeps Dover in the game, and more importantly, it has helped finance one of the longest-standing payout increases among the Aristocrats.

Indeed, I mentioned Dover in July 2018. Since then, it has announced two more annual dividend increases to extend its streak to 64 years. It has also quadrupled the broader market with 43% in total returns.

The Saucy Side of Fluids and Food Equipment

Dover is a little pricey at the moment, but it should keep slowly churning out growth of about 3% annually over the next few years. The bottom line is what’s more encouraging–analysts are looking for a 17% bump this year and a still-respectable 8% improvement on top of that in 2020.

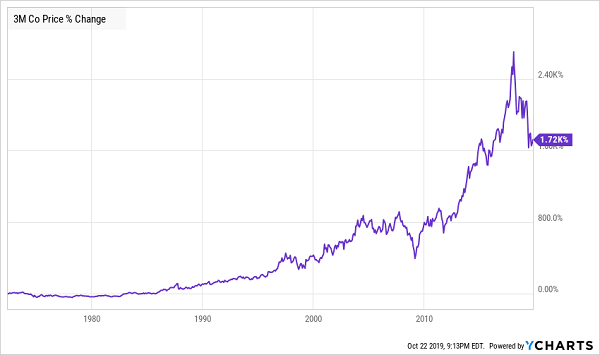

3M (MMM) Dividend Yield: 3.5%

“Broken.”

That’s the word JPMorgan analyst Stephen Tusa used to describe 3M’s (MMM) business model in an early August note.

“There is something that goes beyond the impact of cyclical volume pressure here. (A) structural issue, that there is generally a higher cost to serve than many appreciate, now seems clear.”

It’s yet another sign of just how much has turned for what once was one of the most consistent blue chips on Wall Street. It’s currently mired in its sharpest decline in decades, a 35% drop since early 2018.

The industrial conglomerate that’s responsible for Post-it Notes, Scotch Brite and Nexcare bandages has delivered a few dismal reports in that time. That includes a ghastly earnings miss in April that saw it also cut its full-year forecast, announcement of the layoffs of 2,000 workers, and informed investors it was undergoing some restructuring and other measures to try to cut costs and boost cash flow.

It’s also been bitten by the litigation bug. 3M could face as much as $6 billion in legal liabilities connected to accusations that the company’s chemicals have shown up in groundwater across the country.

3M is one of the longest-tenured Dividend Aristocrats at 61 consecutive years and counting. But even that seems like less of a guarantee than it used to. While the payout is well-covered at less than 70% of profits, Tusa warned that “Another leg down in fundamentals would mean they are on watch for a cut, after 37 straight years of increase.”

Will things degenerate that much? It’s difficult to say. But 3M appears set up to endure more pain before it establishes an enduring recovery.

Better Than Aristocrats: “2008-Proof” Income Plays With 7.5% Yields and Fast 10%+ Upside

It’s remarkable to think that even the most reputable blue chips sporting decades of dividend growth can be so suspect.

But that’s how I can help you separate yourself from “first-level” investors. While they lean on lazy recommendations based on past performance and reputations, I invest using methodical, forward-looking analysis, and sniff out the dangers in supposedly no-brainer plays.

And I want to start by showing you how to get real income. We’re talking safe, sustainable payouts of 3 to 4 times what most Dividend Aristocrats deliver.

This is no time to gamble in a desperate stretch for yield. We’re in the back half of a bull market that’s extra-long in the tooth, and numerous global risks are converging on this fragile market.

Big yields mean nothing if you’re not protecting your hard-earned nest egg, too.

These 5 income wonders deliver two things most “blue-chip pretenders” don’t:

Rock-solid (and growing) 7.5% average cash dividends (more than my portfolio’s average).

A share price that doesn’t crumble beneath your feet while you’re collecting these massive payouts. In fact, you can bank on 7% to 15% yearly price upside from these five “steady Eddie” picks.

With the Dow regularly lurching a stomach-churning 1,000 points (or more) in a single day during pullbacks, I’m sure a safe—and growing—7.5% every single year would have a lot of appeal.

And remember, 7.5% is just the average! One of these titans pays a ROCK-SOLID 8.5%.

Think about that for a second: You can buy this incredible stock right this second, and every single year from now on, nearly 9% of your original buy boomerangs straight back to you in CASH.

If that’s not the very definition of safety, I don’t know what is.

These five stout stocks have sailed through meltdown after meltdown with their share prices intact, doling out huge cash dividends the entire time. Owners of these amazing “2008-proof” plays might have wondered what all the fuss was about!

These five “2008-proof” wonders give you the best of both worlds: a 7.5% CASH dividend that jumps year in and year out, with your feet firmly planted on a share price that holds steady in a market inferno and floats higher when stocks go Zen.

Editor's Note: The stock market is way up – and that’s terrible news for us dividend investors. Yields haven’t been this low in decades! But there are still plenty of great opportunities to secure meaningful income if you know where to look. Brett Owens' latest report reveals how you can easily (and safely) rake in 8%+ dividends and never worry about drawing down your capital again. Click here for full details!

When I show people how closed-end funds (CEFs) can hand them safe 7% yields and let them retire on much less than a million bucks, they often say one thing:

“Why the heck hasn’t my financial advisor told me any of this?”

The reasons are both simple and surprising: 1) Many financial advisors don’t fully understand how CEFs work, and 2) Some CEFs involve a bit of research, so for a lot of advisors it’s easier to recommend low-cost index funds and call it a day.

Both of these (unacceptable) reasons are costing folks millions in profits!

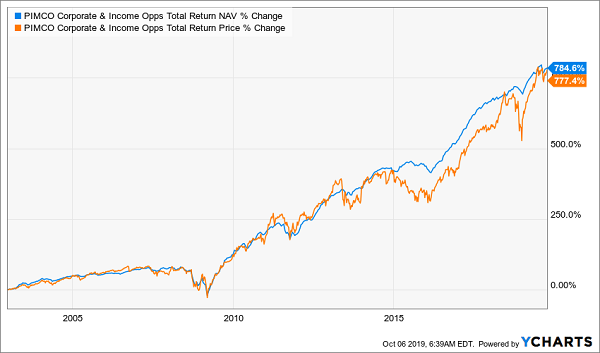

So today we’re going to demystify CEFs by zeroing in on a fund that’s crushed the market for nearly two decades. In fact, since its IPO in 2002, the PIMCO Corporate & Income Opportunities Fund (PTY) has given investors double the S&P 500’s return.

The Power of a Top-Notch CEF

A lot of advisors dismiss funds that beat the S&P 500 in a year or two as simply lucky—but that doesn’t explain PTY’s 777% return in 17 years. And a deeper look tells us a lot about CEFs and how we can harness them to retire earlier and lock in a massive income stream that too many pros say is unattainable.

How to Buy a 777% Winner (With an 8.6% Dividend) on the Cheap

Since its inception, PTY has returned 13.6% annualized on its market price, while the S&P 500 has returned 9.3%. This outperformance is due to one factor: the fund’s inherent return, despite the market’s lower valuation of PTY.

Let me explain the difference. If we look at the value of the portfolio of assets PTY holds, we see that this portfolio has risen 784.6% since its inception, a bit above the fund’s market-price return.

Portfolio Value Outraces Market Price—and Hands Us a Discount

In other words, PTY’s portfolio gains and the dividends the fund has paid out, if reinvested, are greater than the market price you’d pay for PTY if you bought it now.

This is in large part compounding magic: when you reinvest 8.6% dividends in such a high-performing fund, your total return is bound to grow. But the other part of the story is PTY’s portfolio itself—the real source of its massive outperformance—and PIMCO’s skill in managing it.

Let’s take a look at that now.

A Misunderstood Fund With an Undervalued Edge

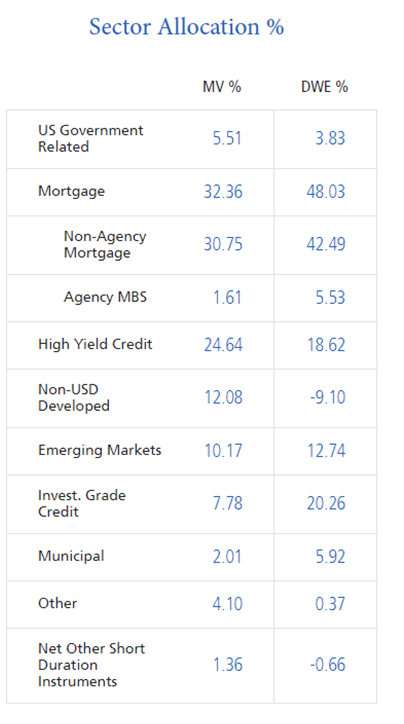

PTY’s portfolio consists of $2 billion worth of a variety of debt instruments:

Source: PIMCO

If we focus on the market value (MV) column, we see that the biggest allocation is to mortgage bonds (32.36%), separated into non-agency and agency mortgage-backed securities (MBS’s).

These are often depicted as complicated and exotic derivatives, but they’re pretty simple at their core: imagine taking a large number of mortgages, putting them together in a single portfolio, then selling portions of that portfolio to investors.

PTY would be one of these investors, because it can get less exposure to any one single mortgage, helping insulate its portfolio, even if housing crashes like in 2008. (It’s important to note that PTY survived 2008 and kept beating stocks during that crash).

The other large exposure, to high-yield credit, is to bonds from corporations with lower credit ratings. Think of this as a group of loans that companies take out and pay back at a higher interest rate. With defaults in these loans staying below 2% most of the time, it’s a lower-risk bet than many people think.

But it’s even less risky for PIMCO, because it’s the world’s second-largest bond buyer. It can access top-quality bonds and information about companies that most other investors can’t. This edge has helped PTY crush the market for decades. And since they still have that advantage, this outperformance will likely continue.

The Income Key to Financial Independence

A lot of investors hear things like “MBS’s” and “high-yield bonds” and get scared. Others cynically say that this kind of outperformance can’t last. But PTY not only survived the worst recession in living memory, its portfolio recovered faster than the S&P 500. And it paid out a high level of income throughout the crisis.

This is what really matters. Investors who held PTY during the crash saw unrealized losses in their portfolios—but they also lost no money if they didn’t sell. And PTY’s huge income stream makes it possible to hold during tough times.

Remember: PTY’s dividend yield is 8.6%. That means investors get $716.67 per month for every $100,000 they invest. If you wanted that same income stream from an S&P 500 income fund, you’d need to invest $450,000.

Yet financial advisors tell their clients to tolerate the pathetic yield they get from the stock market, because they don’t understand how funds like PTY have been crushing the market for years. But PTY’s record speaks for itself.

And PTY isn’t the only CEF that’s crushed the index. It isn’t even the best-performing CEF, or the highest yielding. There’s a whole universe of CEFs out there that you can harness for financial independence.

And now I want to introduce you to 5 of them with 8%+ dividends and 20% gains ahead in the next 12 months …

5 More 8%+ Dividends Wall Street Hides From You

Before I do that, I have to tell you that advisors aren’t the only ones trying to keep CEFs off your radar. The big fund companies are in on it, too!

I’m talking about massive providers of exchange-traded funds (ETFs), such as Vanguard and iShares. These firms throw big marketing dollars at ETFs, and because most of these funds are automated, their costs are next to nothing.

Translation: even the low management fees they collect are pure profit.

But CEFs are different: with average yields of 7% and up, they often beat ETFs on dividends alone! And that doesn’t account for the performance a top-flight human manager can add on, especially in areas like high-yield bonds, preferred stocks and real estate investment trusts (REITs).

I just showed you how PTY demolished its benchmarks while paying an 8.5% dividend—and bear in mind that its return is net of fees.

I don’t know about you, but I don’t mind paying a few hundred bucks more in fees if it will net me a market-crushing 777% return!

Which brings me to the 5 CEFs I want to show you now. They’ve delivered their shareholders life-changing gains, they yield 8% on average (with the highest yielder of the bunch paying an outsized 9.3%), and they’re all bargains now.

The upshot: they’re primed for 20%+ price upside in the next 12 months or less!

Michael Foster has just uncovered 4 funds that tick off ALL his boxes for the perfect investment: a 7.4% average payout, steady dividend growth and 20%+ price upside. — but that won’t last long! Grab a piece of the action now, before the market comes to its senses. CLICK HERE and he’ll tell you all about his top 4 high-yield picks.

New funds are rare in the closed-end fund (CEF) world. But there’s a new kid on the block throwing off a monthly 6% dividend. Today we’re going to run through this new fund to see if it might have a place in your portfolio.

6% Dividends and Netflix-Like Growth—in 1 Fund

I’m talking about the BlackRock Science and Technology Trust II (BSTZ), launched in mid-May of this year.

The unique thing about BSTZ is right in its name: it’s no stodgy income play: its portfolio is packed with some of the fastest-growing tech plays out there.

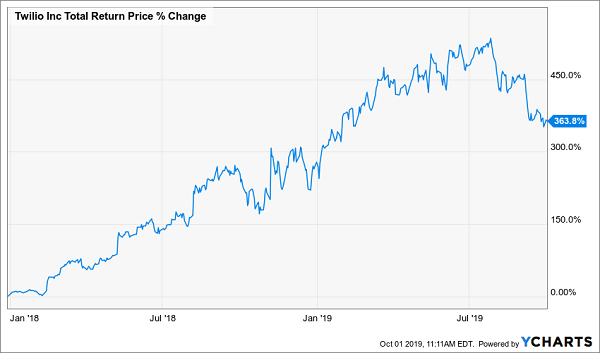

I’m not talking about Apple (AAPL),Netflix (NFLX) or Facebook (FB). Instead, BSTZ focuses on off-the radar companies whose biggest growth lies ahead, like payment processor Square (SQ) and Twilio (TWLO), a communication platform many big companies already depend on.

That’s in contrast to many tech funds, which start and stop with the well-trodden territory of FAANG—Facebook, Apple, Amazon (AMZN), Netflix and Google (Alphabet [GOOGL]).

The Next Apple? It’s Likely in Here.

Source: BlackRock

Twilio is a great example. Its stock price has more than tripled since the start of 2018, and management feels there’s plenty more to come:

A 6% Dividend Plus Gains Like This

The next question is obvious: as none of these companies pays a dividend, what’s BSTZ’s plan for maintaining—and growing—its 6% income stream? Simple: it will sell these stocks when management feels they’re overvalued and buy when it senses a bargain. The profits then roll out to us in the form of that 6% dividend.

The strategy works because these are the kind of firms that, despite their small size, rely on their own cash flow to drive growth. They’re also the kinds of stocks that can get overbought quickly, giving BSTZ’s tech-savvy analysts the chance to sell at a premium.

Can a Growth-Focused Dividend Strategy Work? Absolutely.

The concern here, from a dividend investor’s point of view, is also obvious: can BSTZ keep paying out dividends by rotating in and out of tech stocks?

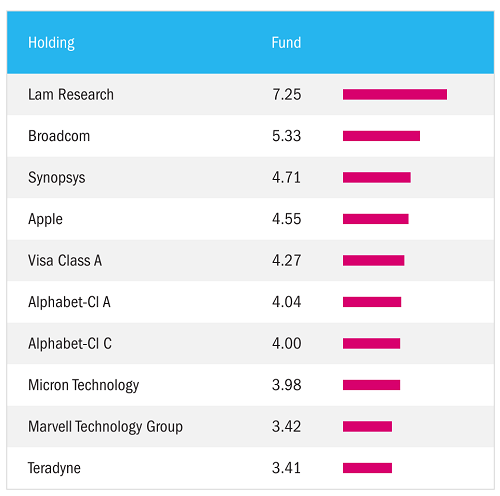

To answer this, let’s look at a competing fund: the Columbia Seligman Premium Tech Fund (STK). While the management team is different, the strategy is similar: find high-quality, fast-growing companies and buy them up.

A Tech Portfolio Focused on Quality

Source: Columbia Threadneedle Investments

As you can see, STK’s portfolio has gotten a little more conservative lately, with a shift from smaller growth companies toward big names like Alphabet and Apple. But don’t be fooled: most of the portfolio is still focused on fast-growing companies like Synopsys (SNPS) and Teradyne (TER). STK is an aggressive tech growth fund, just like BSTZ.

One difference? History. While BSTZ held its IPO a few months ago, STK has been around for a decade. Which is why its past is helpful in understanding BSTZ’s future.

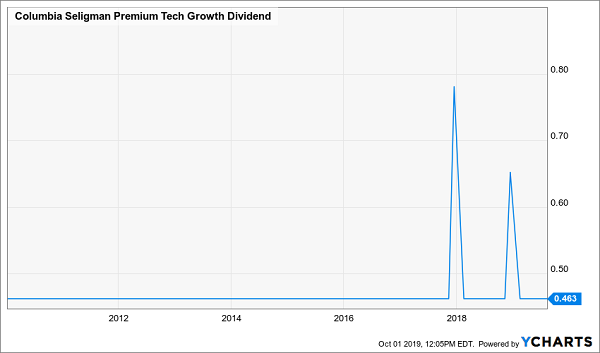

Namely: was STK able to maintain dividends throughout its history by buying and selling tech stocks? Yes.

Steady Payouts—and More

Not only has STK maintained its distributions, which yield a whopping 8.8%, but it’s even paid special dividends in recent years, meaning it has been an even bigger income producer.

I expect the same from BSTZ, but with even bigger gains, thanks to its more aggressive strategy of buying younger, faster-growing companies before the rest of the world is aware of their true potential.

8.8% Dividends and Fast 20% Upside—in Your Income Portfolio?

BSTZ offers something all of us want but few people think is possible: a healthy dividend and fast upside from your income investments.

It’s the investment holy grail! Because with your income stream secure, any growth you can squeeze from this corner of your portfolio is gravy.

Free money. Pure and simple.

Too bad most people’s advisers tell them this dream is impossible. But not only is it possible, it’s easy with CEFs.

But BSTZ, promising as it is, isn’t our best play now.

For one, its dividend is lower than I’d like. With CEFs, it’s easy to bag safe 7%+ payouts, often paid out monthly. And second, because it’s a new fund, the hype has yet to die down: BSTZ trades at a 10% premium to its NAV (or the value of the stocks in its portfolio).

I don’t know about you, but I’m not fussy about paying $1.10 for every dollar of a fund’s assets. I don’t care how skilled its management team is!

28% Total Returns Waiting for You Here

That’s why I’m pounding the table on 4 other CEFs now: they yield an average 8.8% today, and they all trade at huge discounts to NAV.

The bottom line?

I fully expect 20%+ price upside from all 4 of these new picks, in addition to their huge dividend yields. Add it up and you’re looking at 28%+ total returns by this time next year, including their massive payouts and upside potential.

Michael Foster has just uncovered 4 funds that tick off ALL his boxes for the perfect investment: a 7.4% average payout, steady dividend growth and 20%+ price upside. — but that won’t last long! Grab a piece of the action now, before the market comes to its senses. CLICK HERE and he’ll tell you all about his top 4 high-yield picks.

On Saturday, September 14, Saudi Arabia’s largest crude oil processing facility at Abqaiq, was attacked by at least 30 drones and cruise missiles. The attack shut down about one-half of the country’s oil production capacity, which is 5% of the world’s daily production and consumption. When trading markets opened on Monday, crude oil prices jumped by 14%.

However, within a couple of days, crude was back trading at just a couple of dollars per barrel above the pre-attack price. I am shocked that the markets are that unconcerned about an attack that shut down 5% of the world’s oil supply.

The reason that crude oil, which saw WTI peak at almost $63 on Monday, is back trading in the high $50s is that Saudi Aramco management has promised to get the lost production quickly back online. From what I have read, this may not be feasible.

It is my opinion that Saudi Arabia will sell oil from its reserves and try to get Abqaiq back up to full capacity in a few weeks. This may be very, as in too, optimistic and the country could quickly exhaust its reserves and leave the world supply with a continuing shortage with a much smaller safety net.

Another concern is that oil traders seem to be completely ignoring the potential for another attack. I am a former Air Force pilot, and my thoughts are that when the attackers see that 30 drones and cruise missiles didn’t get the job finished, I would start to ready the next one with 60 drones and missiles.

The powers behind the first attack want to shut down the capitalist world. The capitalists trading oil seem to have blinders on that their way of life has been attacked.

I think the world of oil traders is insulated from the dangers of the world and are underpricing the risks to crude oil. There is a strong possibility of another event that will drive the price of a barrel of crude much higher, and the next time it will stay higher. Here are three dividend-paying stocks that would benefit from higher oil prices.

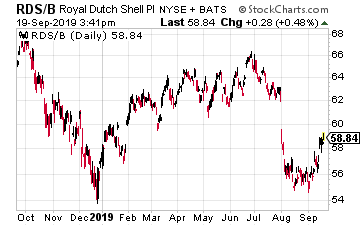

Royal Dutch Shell (RDS.A) (RDS.B) is a global energy producer that would be a significant beneficiary of another or continued production reductions out of Saudi Arabia.

The company is truly a global producer with production areas in the Gulf of Mexico, Canada, Norway, Malaysia, Nigeria, Brazil, and Russia.

Royal Dutch Shell appears to be a prime player to provide oil to end-users that find they are not getting what they need from Saudi Arabia.

RDS shares currently yield 6.4%.

Occidental Petroleum Corp. (OXY) is a crude oil and natural gas production company whose share price is down 40% since it announced earlier this year that the company would acquire Anadarko Petroleum Corp. The merger is now complete. OXY is a global energy producer with a large footprint in the U.S. Permian, Rockies and Gulf of Mexico production areas.

The U.S., especially the Permian, is where most of the world’s crude oil production growth is being fueled.

Higher oil prices will allow the Permian and other U.S. production areas to ramp up their growth further.

OXY shares currently yield 7.0%.

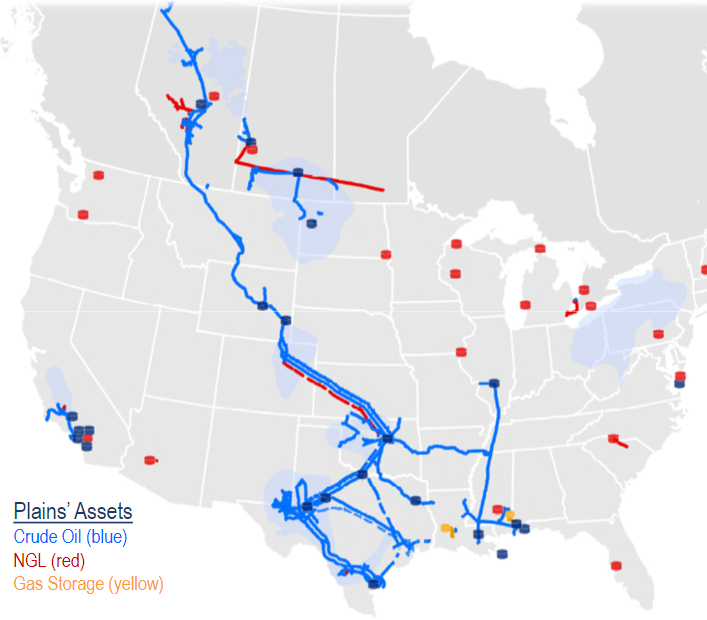

Plains All American Pipeline LP (PAA) is a master limited partnership (MLP) that owns the largest independent crude oil pipeline and storage network in the U.S.

The company is a major mover of crude oil out of the Permian.

The company has additional pipelines under development and typically partners with crude oil end users as partners in any new projects.

While the company doesn’t count on the results of its Logistics Division to support the dividend, this trading business can generate huge profits when energy prices get disrupted.

Get your hands on my most comprehensive, step-by-step dividend plan yet. In just a few minutes, you will have a 36-month road map that could generate $4,804 (or more!) per month for life. It's the perfect supplement to Social Security and works even if the stock market tanks. Over 6,500 retirement investors have already followed the recommendations I've laid out.

Let’s brush aside some financial noise today, as I’d like to show you the best retirement investment you can make.

I’m talking about secure dividends that’ll grow every year, fund your regular expenses today, plus grow your capital so you don’t have to ever worry about running out of money.

You won’t have to worry about what the Fed says, either, because this worry-free strategy is ahead of Jay Powell and his crew. In fact, this “1-click” indicator not only tells you what to buy, but it nails the “when” better than any armchair (or professional) Fed watcher.

Why REITs? For starters, they’re pullback-proof. For most of the late 2018 downturn, REITs actually rose. And even when they did get caught in the downdraft, they only fell half as much as the rest of the market:

REITs Show Their “Pullback-Proof” Chops

What’s more, by simply watching REITs, you can tell where the Fed will go next. Consider last January: as the Fed chief stubbornly stuck to his rate-hike plans throughout the month, investors in REITs—which are an ideal play on falling rates, as we’ll dive into in a moment—saw right through him.

They piled in!

Before poor Powell could find his way to a microphone to swear off his rate hikes, savvy REIT buyers had pounded these trusts a lot higher than the market—even though REITs were starting from a higher base, thanks to their resilience in the pullback:

REITs Call Powell’s Bluff

Fast-forward to today and we’ve got ideal conditions for REIT investing. First off, interest rates are low, and traders betting through the futures market expect them to go lower:

Source: CME Group

Second, the yield on the 10-year Treasury has collapsed, sitting at 1.75% after hitting highs above 3.2% late last year.

And some Wall Street vets, like Bob Michele, CIO and head of global fixed income at JPMorgan Asset Management, say they see the yield on the 10-year going to zero. Others see negative interest rates as a real possibility here in the US.

I think you’ll agree that REITs’ big dividends (roughly double, on average, what your typical S&P 500 stock pays) will be irresistible to a lot of investors if the other option is to pay the bank to hold onto their money!

You can set yourself up for bigger gains—and greater safety—if you look for REITs whose dividends are not only growing but accelerating. That’s because an accelerating dividend acts like a magnet on a company’s share price—pulling its payout higher with every single increase.

You can see this pattern in stock after stock—and not just REITs. Check out how shares of Coca-Cola (KO) rolled higher with each payout hike:

Coke’s “Dividend Magnet” in Action

It’s uncanny! And it shows that you just can’t keep a good dividend-payer down.

But we’re not going to buy shares of Coke today, because, as you can see above, its dividend growth is slowing. To lock in our upside (and hedge our downside), we need stocks whose payouts are, as I mentioned earlier, delivering bigger and bigger hikes every year.

When you buy “dividend accelerators,” gains can come fast—I’m talking 32% in just 10 months fast!

How “Dividend Magnets” Propelled Us to a Quick 32% Gain

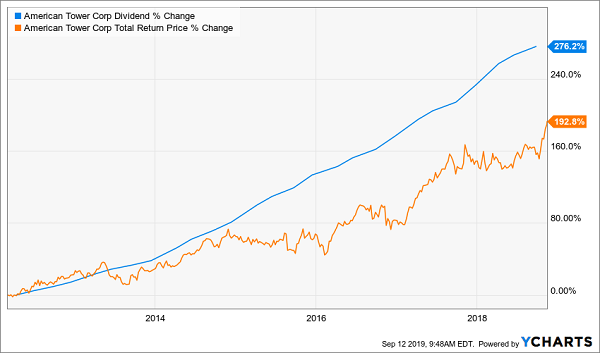

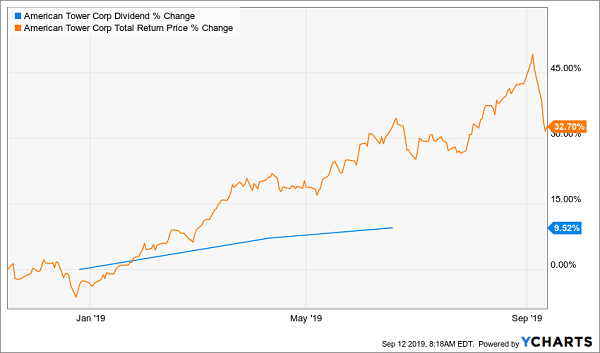

To see this dead-simple dividend-growth strategy in action, look at American Tower (AMT), a REIT I recommended in my Hidden Yields advisory in November 2018.

The REIT is a lynchpin of the world’s data networks, with 150,000+ cellphone towers scattered around the planet.

AMT is one of four major cell-tower REITs—the others being SBA Communications (SBAC), Crown Castle International (CCI) and Uniti Group (UNIT).

The REIT yields 1.6% today. But that low current yield masks the fact that management hikes the payout every quarter, and by no small amount: the dividend has soared 338% since American Tower declared its first payout in March 2012.

But a funny thing happened: after tracking the dividend closely, AMT’s share price fell off the pace. And when that gap got particularly wide late last year, we pounced:

AMT’s Dividend Magnet (Temporarily) Loses Its Grip …

The result? In the following 10 months, we bagged three dividend hikes (a nearly 10% raise in all) and 32% in total returns as AMT’s price raced to catch up to its dividend! That’s nearly three times the S&P 500’s 11.7% gain in that time.

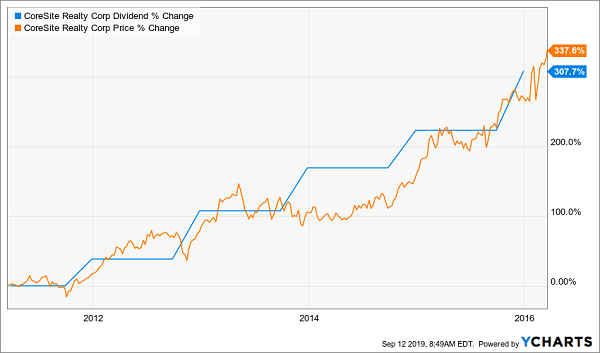

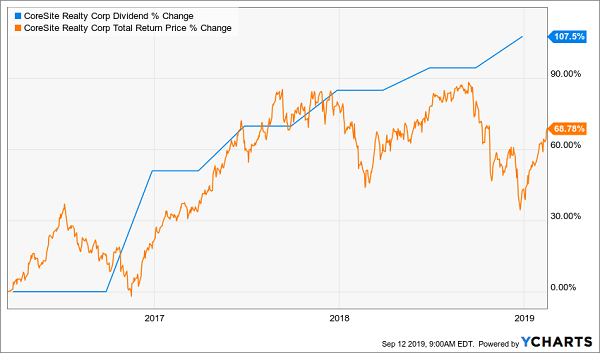

If you’re still not sold on the power of a surging payout, let me show you what happened to another data-center REIT: CoreSite Realty (COR). Before I recommended CoreSite in March 2016, it was showing the very same dividends-up, share-price-up pattern:

CoreSite Auditions for Our Hidden Yields Portfolio

It is true that, unlike with AMT, CoreSite’s dividend hadn’t fallen behind its payout. But that didn’t matter because management was flush with cash!

Driven by top-quality tenants like Microsoft (MSFT) and Verizon (VZ), CoreSite had seen its revenue grow 17% annually and funds from operations (FFO, the REIT equivalent of earnings per share) surge 24% over the preceding three years, so management had plenty of runway to grow the dividend.

I’d seen enough—I issued a buy call on the stock in Hidden Yields on March 18, 2016.

What happened? By February 2019, when we closed our position, management had hiked the payout five times—more than doubling it in size—and driving us to a 69% total return in just under three years!

CoreSite Rolls to a Fast Dividend Double

That’s the punch a soaring dividend packs. When you combine it with plunging (and possibly even negative) interest rates, you get a setup for even bigger upside.

This is the perfect time to mention my 7 top dividend-growth picks now. They’re set to hand out for life-changing gains and surging yields, thanks to their powerful “dividend magnets.”

In fact, I fully expect these 7 dividend stars to …

DOUBLE Your Money Every 5 Years (or less!)

I can’t wait to tell you about these 7 off-the-radar buys, whose payouts are growing so fast that I fully expect them double an investment made today by 2024—and likely a lot sooner.

And because these gains will be driven by these 7 stocks’ surging payouts, you can expect a huge slice of that win to come your way in cash!

Imagine turning a retirement “pot” of $250,000 into $500,000, or $500,000 into $1 million. That’s the kind of upside I’m talking about here.

These 7 dividend wonders are ridiculously cheap NOW—and they’re growing payouts at an accelerating pace.

Even if the market does take a tumble, these stocks’ soaring dividends give you protection as more yield-seekers spot their surging income streams and buy in, eager to hedge their downside with a reliable wave of dividend cash.

Editor's Note: The stock market is way up – and that’s terrible news for us dividend investors. Yields haven’t been this low in decades! But there are still plenty of great opportunities to secure meaningful income if you know where to look. Brett Owens' latest report reveals how you can easily (and safely) rake in 8%+ dividends and never worry about drawing down your capital again. Click here for full details!

Today I’m going to show you the one market indicator you can use to grab gains as high as 70% in nine months (or less!), plus dividends growing double-digits, too.

It’s a measure of market panic you’ve probably heard about, but here’s the funny thing: everyone is looking at this indicator backwards.

Let me explain.

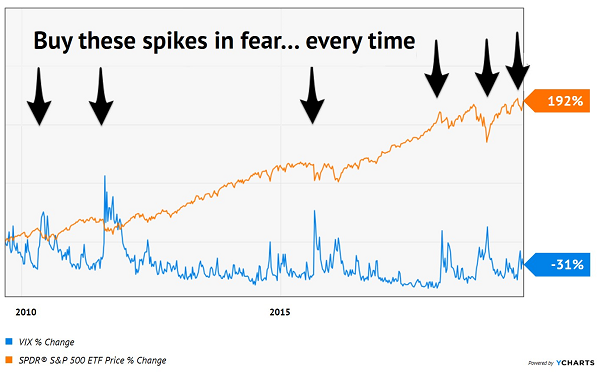

First, I’m talking about the CBOE S&P 500 Volatility Index, or VIX for short. You’ve probably heard of the VIX: dubbed the market’s “fear gauge,” it’s a measure of how volatile traders see stocks in the next 30 days.

In other words, when investors are twitchy, the VIX rises—and when they’re confident, it trends down. But to reallyprofit off this measure of terror, you have to be a gutsy contrarian and buy when fear shoots up.

It’s one of the most reliable buy indicators there is! Take a look:

VIX Up, Stocks Up

As you can see, every time the VIX spikes, the market takes off soon after. Take a look at the end of that chart: you can see that the VIX is a bit higher than it’s been for most of 2019.

That means our buy window is easing open once again.

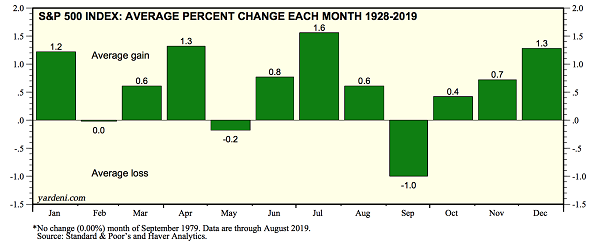

And if history is any guide, our opportunity will soon get better. That’s because September is one of the more volatile months, according to Yardeni Research, and typically turns in the worst performance.

And with profits and sales still strong, unemployment low and wages rising, any pullback (and spike in the VIX) this month would be a great buying opportunity.

But we’re not going to settle for ho-hum dividends from darlings like McDonald’s (MCD) or Coca-Cola (KO). To ride our “fear gauge” to market-beating gains, we need stocks whose dividends are not only growing but accelerating.

To show you how potent buying a rising dividend against a spiking VIX can be, let me take you back to December 21, 2018, when the “fear gauge” hit 30—the highest level in nearly five years.

You see, Hidden Yields comes out monthly, and every issue brings you one new dividend-growth pick. But in December, with my favorite contrarian indicator going wild, I decided the time was right to pound the table on not one but two dividend-growth picks.

How Fear Drove a 70% Gain

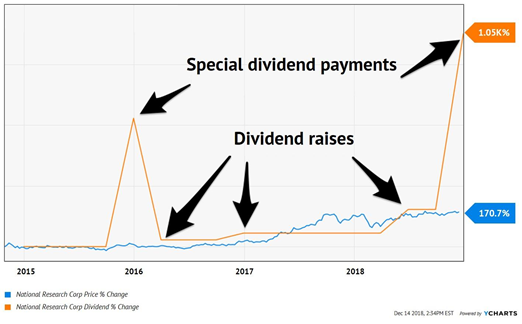

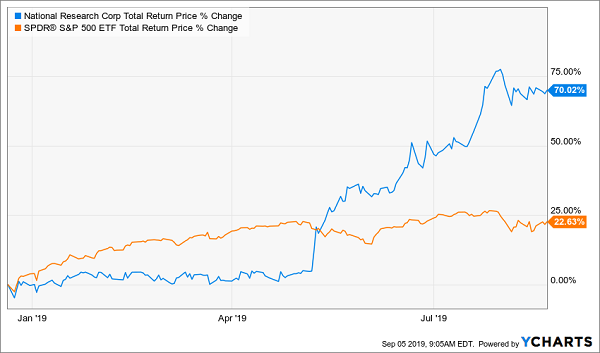

The first was NRC Health (NRC), a low-key maker of “back-end” systems for the healthcare industry, specifically surveys that solicit patient feedback on doctors, nurses and staff.

It’s a low-key firm with a smart business model: it’s free for patients to use but charges thousands of dollars a year to cash-rich healthcare providers! That gave it:

Recurring annual payments from customers with

Recession-proof businesses.

I also liked the fact that NRC had plenty of room to grow by building customized systems for clients and cross-selling its other products. It nearly tripled its “regular” dividend since 2014 and was kicking out regular special dividends, too:

NRC’s Dividend Grows 2 Ways

How did that buy turn out? Fast-forward nine months, and NRC had soared 70%!

NRC Triples the Market’s Gain

We weren’t done.

Because with my “fear gauge” still redlining back in December, I added a second dividend grower I’d been watching to our Hidden Yields stable.

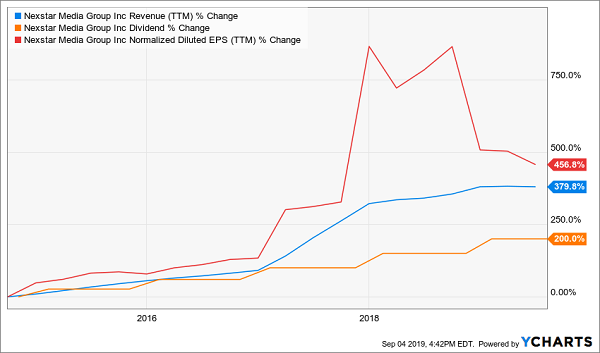

That would be NexStar (NXST), a midcap stock that had been dragged down by a misunderstanding of its business: NexStar is one of the biggest local-TV operators in the country, reaching an impressive 38% of US households.

This was a classic “disrespected dividend,” trading at 6.5-times earnings when I recommended it. But here’s what most folks missed:

NexStar’s retransmission revenue—the money it collects from broadcasters for the local content it provides—was growing quickly. Plus,

Its digital-media revenue (from its 114 local websites, 202 local mobile apps and online videos) was growing even faster.

Add these channels together and you had a company growing profits, sales and dividends at an amazing clip:

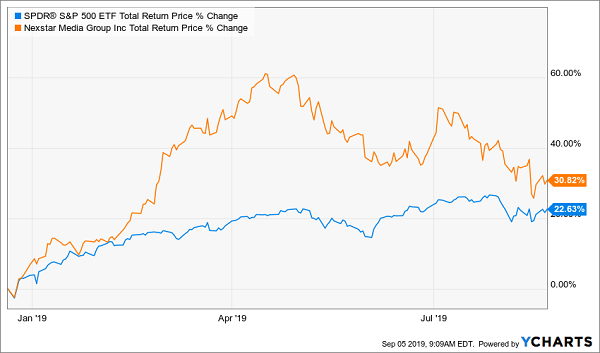

We Bought This for Just 6.5X Earnings

Over the following nine months, NXST handed us a fast 31% return, easily eclipsing the market!

“Fear Gauge” Ignites Another Market-Beating Return

Now let’s turn our attention to 7 of my very best dividend-growth picks. They’re perfect for the markets we’re in right now.

7 Buys to DOUBLE Your Money Every 5 Years (High VIX or Low)

I can’t wait to tell you about these off-the-radar buys, which are poised to throw off strong double-digit gains—year in and year out—with much of that return coming your way in cash dividends!

So what kind of upside am I talking about?

Enough to DOUBLE your money every 5 years—and likely less time than that!

Imagine turning a retirement “pot” of $250,000 into $500,000, or $500,000 into $1 million. That’s the kind of upside I’m talking about here.

And you don’t have to wait for the VIX to spike to buy them. These 7 dividend wonders are cheap NOW—and like NexStar and NRC, they’re growing payouts at an accelerating pace.

Editor's Note: The stock market is way up – and that’s terrible news for us dividend investors. Yields haven’t been this low in decades! But there are still plenty of great opportunities to secure meaningful income if you know where to look. Brett Owens' latest report reveals how you can easily (and safely) rake in 8%+ dividends and never worry about drawing down your capital again. Click here for full details!

Today I’m going to show you nothing less than a “dividend unicorn”: a closed-end fund (CEF) yielding 8.8% that’s raised its payout 24% in just the last six months. (And yes, it’s primed for many more hikes, too.)

Get this: because of the weirdness of the CEF market, this cash machine is still cheap today—trading at 13% off its “retail” price!

Let’s dive in.

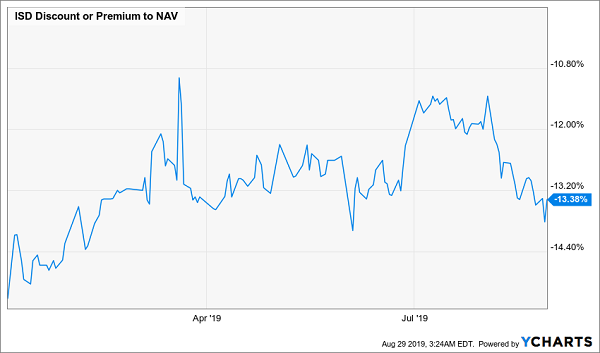

I’m talking about the PGIM High Yield Bond Fund (ISD). It’s a smaller CEF (with just $552 million in assets). That small size helps set up our chance to buy cheap—and I’ll say more about why this deal exists in just a moment.

First, though, if you’ve been reading my columns on Contrarian Outlook, ISD’s name might sound familiar: two weeks ago, I highlighted a buying opportunity in the fund, writing that its huge discount is “going to disappear soon.” The reason? Its “improving dividend-growth potential.”

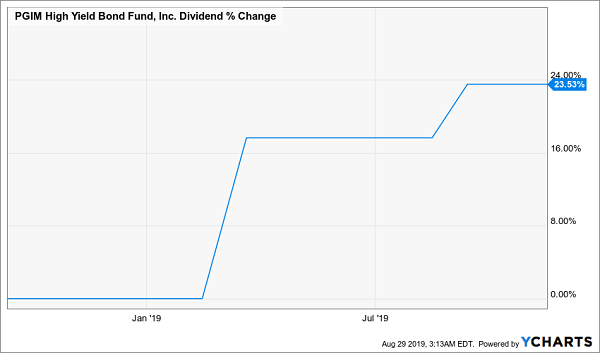

As if on cue, Prudential, the fund’s managers, announced less than a week later that ISD would hike its dividend—part of a recent trend that’s seen the fund raise its payout 24% this year alone:

8.8% Dividends and 24% Payout Growth—in 1 Buy

Heck, we’d be happy if ISD kept its 8.8% dividend where it is. But an 8.8% yielder with a payout growing this fast is unheard of.

And those hikes will likely keep on coming, for one reason: the Federal Reserve.

Management Reads the Fed Like a Book

Let’s quickly go back a few years. In 2015, when the Federal Reserve started raising interest rates, ISD had a strategy specifically designed to profit from the Fed’s hikes. At the time, ISD specialized in buying short-term corporate bonds, which are less sensitive to rate hikes than longer-term bonds.

That strategy helped ISD’s net asset value (NAV, or the value of its underlying portfolio) top the high-yield bond index, shown below by the SPDR Bloomberg Barclays High Yield Bond ETF (JNK):

ISD Taps the Fed for Benchmark-Beating Returns

Not only did ISD investors get corporate-bond exposure, they also snagged bigger gains and bigger dividends than they would have with JNK, which only yields 5.6%. The result was a larger total return and a bigger income stream.

“Powell Pivot” Leads to a Strategy Shift—and More Gains

Then, in early 2019, ISD changed its name and its mandate. As the Fed made clear at the start of the year, the central bank would pivot from raising rates to cutting them. The first cut came in July, and the market is expecting another later this year, with the possibility of two or more over the next 12 months.

In response, ISD pulled a 180. In March of this year, Prudential announced that the fund would abandon its focus on short-term corporate bonds and become a broader high-yield bond fund. The reason is simple: in a market where interest rates are going down, long-term high-yield bonds tend to go up in value.

And ISD is taking advantage, riding its new strategy to market-beating returns, with much less volatility than stocks:

New Strategy Ignites ISD

About That 13% Discount …

By now you might be wondering about that 13% discount I mentioned earlier, and how it can exist on a fund that yields 8.8%, has hiked its payout twice in six months and is whipping the index.

Part of the reason is the market jitters of the past few months, which have helped push ISD’s discount about as wide as it’s been since the fund’s new investment policy began:

A Buying Opportunity Appears

But that’s not the only reason. Another one is the fund’s small size.

As I said earlier, ISD only has $552 million in assets. That makes it too small for most big investors—the multi-billion-dollar hedge funds and investment banks—to take advantage of. The fund is just too tiny for them to make noticeable profits, and that’s led to a lack of coverage of ISD. And that means plenty of folks have missed the big shift in the fund’s mandate.

That inefficiency is an opportunity for CEF investors, because it won’t last forever. While some CEFs can have their discounts last for years, well-performing and high-yielding funds like ISD will more often than not see investors rush in. That means grabbing a position now will likely pay off handsomely in gains, dividends and payout hikes in short order.

4 More Safe 8.7%+ Dividends (with 20% Upside) Waiting for You Here

Here’s the best news: there are dozens more smaller CEFs that, like ISD, offer fast-growing dividends and smooth, steady gains.

But because small CEFs get so little coverage, hardly anyone knows! (Though in today’s world, where Treasuries yield less than 1.6%, more folks are starting to catch on.)

That makes now a great time to buy ISD, but there’s no reason to stop there when there are so many more high—and growing—dividends available. Like the 4 CEFs I’ll share with you right here. They pay 8.7% dividends as I write, their payouts are growing and, yes, these “stealth” funds are terrific bargains!

So much so that I’m calling for 20%+ price upside from each of them in the next 12 months.

The 4th fund on my list is a great example: it yields an incredible 10.7% and, like ISD, its payout is growing—up 150% in the past decade!

A Rare 10.7% Dividend That Soars

More folks are starting to catch on—which is why this fund has clobbered the market so far in 2019:

Income-Starved Hordes Pile In

The funny thing is, even though this fund should be trading at a big premium, you can still grab it at a discount! And with interest rates headed lower (making its huge payout even more appealing), its gains are just getting started.

But even if I’m wrong and it just trades flat from here, you’re still beating the market’s average yearly return in dividends alone, thanks to this fund’s outsized 10.7% dividend yield!

If that’s not the definition of a win-win, I don’t know what is.

Full details on all 4 of these income (and growth) powerhouses are waiting for you now, and, as with ISD, this is the very best time to buy them.

Michael Foster has just uncovered 4 funds that tick off ALL his boxes for the perfect investment: a 7.4% average payout, steady dividend growth and 20%+ price upside. — but that won’t last long! Grab a piece of the action now, before the market comes to its senses. CLICK HERE and he’ll tell you all about his top 4 high-yield picks.

I feel like we have moved into a Dr. Strangelove type of financial world. The economic data shows that the U.S. economy is doing fine. We have growth in the economy, low unemployment, and rising wages.

Home prices continue to increase. In contrast, on the financial markets side of the universe, traders are pushing bond prices, making yields and stock prices act like the next Great Recession starts on Friday.

One effect of this schizoid financial world is the new existence of dividend stocks, with solid cash flow coverage and actual dividend growth trading with yields of 12%, 15%, even 18%.

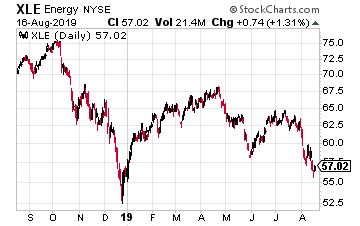

Energy is one economic and stock market sector that has been hit hard by the fears of an economic slowdown or possible recession. The Energy Select Sector SPDR (XLE) is down 18% from its 2019 high.

The sector is trading like the world is going to stop driving vehicles, turning on the lights, or running their air conditioners. Fundamental analysis and logic have no place in the current fear-driven energy stocks investor strategy.

One of the effects of this sell-off is that you now have energy midstream companies trading to pay tremendous dividend yields. The midstream sector provides the transport, storage, and other services to get oil and natural gas from the production plays to the refineries and power companies that consume the energy commodities.

Midstream companies deliver their services on long-term fixed-fee contracts. Interstate pipelines have rates set by the Federal Energy Regulatory Commission, with built-in annual rate increases.

Shippers on pipelines and users of energy storage commit to minimum volumes, so the midstream revenues are very predictable and growing. With stable, predictable cash flows, most energy midstream companies pay out most of their free cash flow as dividends. This is a business sector where income-focused investors can earn attractive returns.

The 2019 energy sector crash has not exempted these solid dividend-paying companies. Many have fallen harder and farther than the stocks of energy companies whose profits are dependent on the prices of energy commodities. Go figure.

As a result, there are midstream companies with solid revenue and cash flow stream, long term records of growth and even growing dividends that currently sport yields from the low teens up into the high teens. Maybe the market is right, and the next recession starts tomorrow. Or perhaps it’s wrong, and this is a once in a decade opportunity for income-focused investors.

Here are three midstream stocks with very high yields. Do your research and decide if these companies will be able to continue to pay dividends. I did mine and I think, yes.

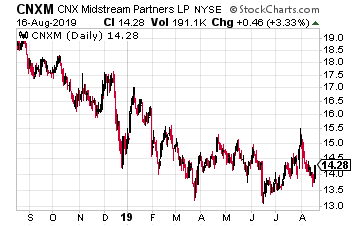

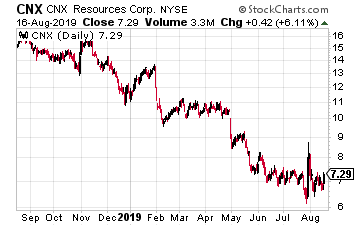

CNX Midstream Partners LP (CNXM) is a master limited partnership (MLP) that owns, operates, develops and acquires gathering and other midstream energy assets to service natural gas production in the Appalachian Basin in Pennsylvania and West Virginia. The midstream company is sponsored and controlled by upstream energy producer CNX Resources Corp (CNX).

At least a portion of CNXM revenues are dependent on production growth by CNX. In its second-quarter earnings notes, CNX increased their 2019 production guidance, with 12% annual growth predicted. CNXM has been growing distributions paid to investors by 15% per year.

Distributable cash flow (DCF) coverage is a strong 1.6 times the distribution. This MLP will increase its payout every quarter and currently yields 11%.

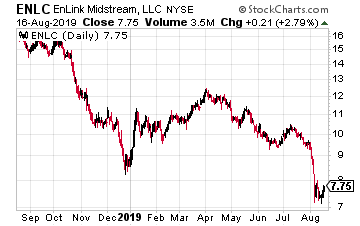

EnLink Midstream LLC (ENLC) provides midstream services for natural gas, crude oil, condensate, and NGL commodities. The company has its assets in premier production basins and core demand centers, including the Permian Basin, Oklahoma, North Texas, Ohio River Valley, and the Gulf Coast.

EnLink Midstream was created by Devon Energy Corp. (DVN).

A year ago, Devon sold its interest in ENLC to privately held Global Infrastructure Partners (GIP). This has produced investor uncertainty about the future of EnLink.

Company management has given guidance of 6% annual dividend growth with 1.3 times DCF coverage. That is very solid in the midstream world.

ENLC shares yield 15%.

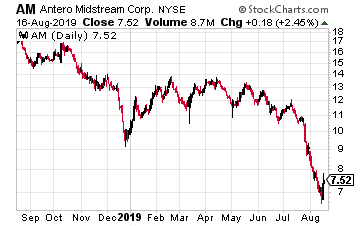

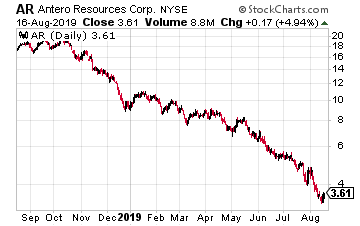

Antero Midstream Corp. (AM) is another midstream services provider focused on natural gas gathering and other midstream services in the Appalachian Basin. AM primarily provides its services to upstream producer Antero Resources (AR).

Early in the year, the current version of Antero Midstream was formed with the merger of an MLP and its publicly traded general partner. A good move for investors.

Recently Antero Resources had a Board of Directors take over by the former heads of Rice Energy, which was acquired by Antero in 2017.

Despite solid growth plans for this year and future years from both companies, the corporate turmoil has investors dumping shares driving down prices.

AM has been growing its dividend every quarter yet is priced to yield an astounding 18%.