So the Federal Reserve cut interest rates. This was their third rate cut in the last three months. The new target range for overnight interest rates is 1.5 to 1.75%. That’s below the rate of inflation.

There are three things you should do right now.

#1. Don’t panic.

#2. Seriously, don’t panic.

#3. Make sure you own a broad, well-diversified portfolio of high-quality growth stocks.

I can help you with #3, but for the first two, well…you’re on your own but hopefully #3 will help.

Before I go further, let’s look at what the Fed is doing and why.

The Federal Reserve’s Game Plan

Not that long ago, the Federal Reserve was on a path of increasing interest rates. After all, the economy was slowly getting over its long hangover, and interest rates had been cut to the bone. Things were gradually getting back to normal.

In a three-year stretch, the Fed hiked interest rates nine times. Not only that but going by their public statements, they seemed on track for several more hikes. For the most part, Wall Street was cool with that.

But then it stopped, and Wall Street got scared. In the fourth quarter of last year, stocks plunged. Not only that, but stocks in economically sensitive areas really plunged. President Trump wasn’t shy about expressing his displeasure with the Federal Reserve and all those higher rates.

The key metric to watch is the yield on the two-year Treasury note. It’s not perfect, but the two-year yield can often be a decent forerunner for Fed policy. Last November, the yield on the two-year got as high as 3%. As worries about the economy and trade war set in, that yield started to plunge. By May, the two-year was below 2%, and earlier this month, it fell below 1.4%. That’s a stunning fall for such a short amount of time.

The Fed had to keep up. That’s why in late July, the Fed cut rates. They cut again in mid-September and again today. Jay Powell, the top banana at the Fed, said that this is simply a “mid-cycle” adjustment and not the start of recessionary rate-cutting splurge.

Wall Street believes him. At least for now. After today, the Fed will probably chill out on any more rate cuts, and they’ll assess how the current cuts have worked. The Fed, I should add, does not exactly have a stellar track record when it comes to forecasting the economy.

What does this mean for us? Lower rates are good news for investors for two reasons. One is that it lowers the cost of borrowing, and that’s a major expense for companies. It will also lower the cost of many variable-rate mortgages. Importantly, lower rates tend to help equity valuations. The lower rates go, the higher price/earnings ratios can rise. (Not always, but in general.)

There’s an old saying on Wall Street, “don’t fight the Fed.” That’s very true. Don’t forget; they have a lot more money. This is why investors should be following the Fed’s path.

The key insight is that lower rates help particular sectors of the economy. Basically, anything that is bought with financing; housing is the obvious example. Another area is the industrial sector.

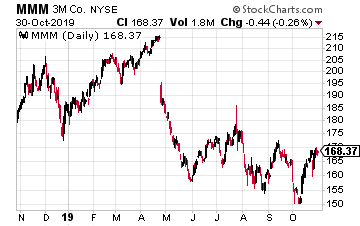

Consider a company like 3M (MMM), formerly known as Minnesota Mining and Manufacturing. This is a classic example of an economically sensitive industrial stock.

Blue chips don’t get much bluer than 3M, and the company is a lot more than Post-It Notes. Last year, 3M had revenues of more than $32 billion. The company is a Dow component, and it has 93,000 employees all over the world.

There’s something else it has—an amazing dividend streak. 3M has raised its dividend every year for 60 years in a row. That dates back to the Eisenhower administration.

This is a good time to give 3M a close look because the stock has disappointed Wall Street this year. Just last week, the company had to lower its business forecast again. This could be 3M’s worst year for sales growth since the recession.

But remember, most of those results happened when interest rates were higher. The lower rates will help 3M and its customers. You always want to pay attention when good companies go through rough patches. Over the last two years, the S&P 500 has gained 19%, while 3M has lost 19%.

Honestly, I’m not too worried about 3M. This is one of the largest and most innovative companies in the world. 3M currently pays out a quarterly dividend of $1.44 per share or $5.76 per share for the year. That currently works out to a dividend yield of 3.4%. That’s about twice what the Fed is charging.

3M will be back, and the Federal Reserve is helping.

Pay Your Bills for LIFE with These Dividend Stocks

Get your hands on my most comprehensive, step-by-step dividend plan yet. In just a few minutes, you will have a 36-month road map that could generate $4,804 (or more!) per month for life. It's the perfect supplement to Social Security and works even if the stock market tanks. Over 6,500 retirement investors have already followed the recommendations I've laid out.

Click here for complete details to start your plan today.

Source: Investors Alley

NRG Yield Inc. (NYSE: NYLD) owns a nationally diverse portfolio of conventional, solar, thermal, wind, and natural gas electricity production assets. The company was spun out in 2012 by NRG Energy (NYSE: NRG), a regulated electric utility company. Renewable energy assets developed by NRG were sold to NYLD to support the growth of NYLD.

NRG Yield Inc. (NYSE: NYLD) owns a nationally diverse portfolio of conventional, solar, thermal, wind, and natural gas electricity production assets. The company was spun out in 2012 by NRG Energy (NYSE: NRG), a regulated electric utility company. Renewable energy assets developed by NRG were sold to NYLD to support the growth of NYLD. Enviva Partners, LP (NYSE: EVA) is a publicly traded master limited partnership (MLP) that takes a different type of natural resource, wood fiber, and processes it into a transportable form, wood pellets. The pellets are sold on long term contracts to companies in the UK and Europe where they are burned to produce electricity.

Enviva Partners, LP (NYSE: EVA) is a publicly traded master limited partnership (MLP) that takes a different type of natural resource, wood fiber, and processes it into a transportable form, wood pellets. The pellets are sold on long term contracts to companies in the UK and Europe where they are burned to produce electricity.

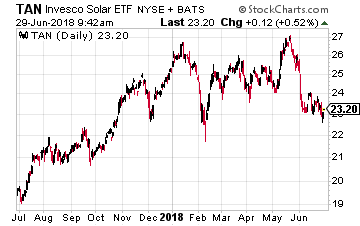

First of all, you must stay away from broad exposure to the industry through ETFs such as the Invesco Solar ETF (NYSE: TAN), which is down about 8.5% year-to-date. There are just too many of the lower-tier players in such a broad fund.

First of all, you must stay away from broad exposure to the industry through ETFs such as the Invesco Solar ETF (NYSE: TAN), which is down about 8.5% year-to-date. There are just too many of the lower-tier players in such a broad fund.

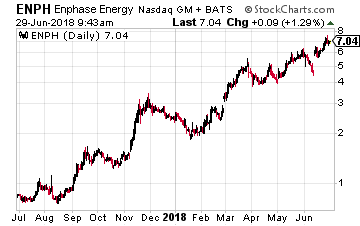

Another company to look at is one that was once considered ‘dead’ – Enphase Energy (Nasdaq: ENPH). Its semiconductor-based microinverter system converts energy at the individual solar module level and brings a system-based high-technology approach to solar energy generation, storage, control and management.

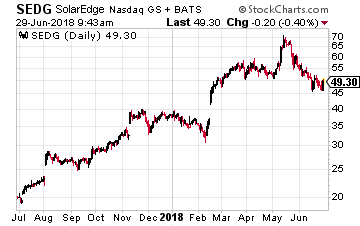

Another company to look at is one that was once considered ‘dead’ – Enphase Energy (Nasdaq: ENPH). Its semiconductor-based microinverter system converts energy at the individual solar module level and brings a system-based high-technology approach to solar energy generation, storage, control and management. Finally, there is my favorite and a member of the Growth Stock Advisor portfolio, SolarEdge Technologies (Nasdaq: SEDG).

Finally, there is my favorite and a member of the Growth Stock Advisor portfolio, SolarEdge Technologies (Nasdaq: SEDG).

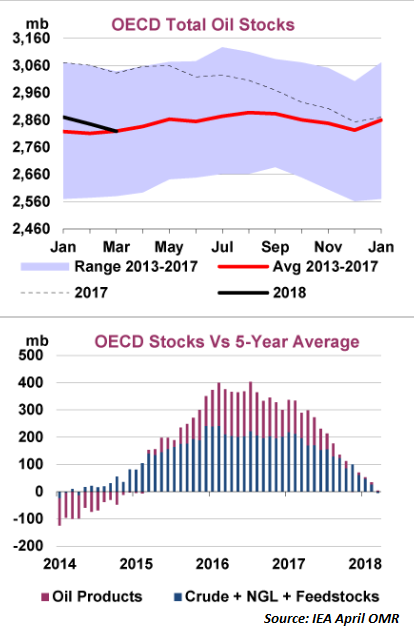

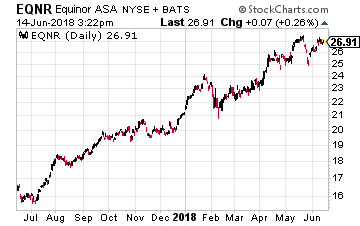

Of the larger oil companies, my favorite is Norway’s Equinor ASA (NYSE: EQNR), which recently changed its name from Statoil to emphasize its long-term move pivot away from oil and toward alternative energy.

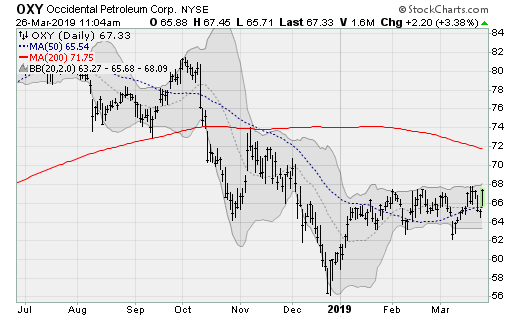

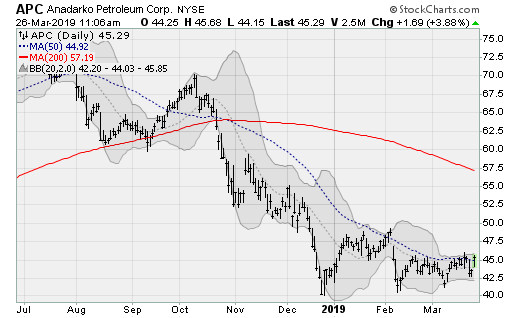

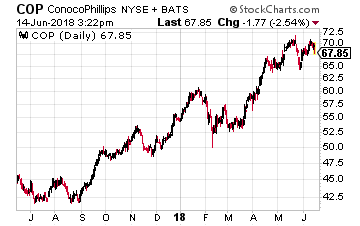

Of the larger oil companies, my favorite is Norway’s Equinor ASA (NYSE: EQNR), which recently changed its name from Statoil to emphasize its long-term move pivot away from oil and toward alternative energy. Here in the U.S. I like ConocoPhillips (NYSE: COP), which is also up 26% year-to-date. This should continue as the company expects compound annual growth rate (CAGR) of production through 2022 of 22%. Not surprising when you consider that the bulk of the acreage it holds in the Eagle Ford shake and Bakken shale are rich in oil. Another plus is that on February 1, ConocoPhillips entered into a deal with AnadarkoPetroleum to buy a 22% stake in the Western North Slope of Alaska. The company will also acquire the stake of Anadarko in the Alpine pipeline. Once the deal concludes, ConocoPhillips’ cash flow will rise from incremental production increases.

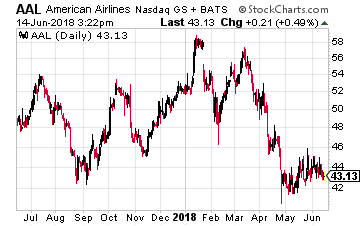

Here in the U.S. I like ConocoPhillips (NYSE: COP), which is also up 26% year-to-date. This should continue as the company expects compound annual growth rate (CAGR) of production through 2022 of 22%. Not surprising when you consider that the bulk of the acreage it holds in the Eagle Ford shake and Bakken shale are rich in oil. Another plus is that on February 1, ConocoPhillips entered into a deal with AnadarkoPetroleum to buy a 22% stake in the Western North Slope of Alaska. The company will also acquire the stake of Anadarko in the Alpine pipeline. Once the deal concludes, ConocoPhillips’ cash flow will rise from incremental production increases. Jet fuel represents a third of airlines’ expenses and industry executives predict costs will be passed on to consumers via higher fares. If I had to pick one loser among the airlines, it would be American Airlines (Nasdaq: AAL), which has added fuel costs to its other problems (overcapacity, etc.)

Jet fuel represents a third of airlines’ expenses and industry executives predict costs will be passed on to consumers via higher fares. If I had to pick one loser among the airlines, it would be American Airlines (Nasdaq: AAL), which has added fuel costs to its other problems (overcapacity, etc.)