Money-Making Stocks to Buy: Baidu (BIDU)

baidu stockI highly recommend checking out Baidu Inc (ADR) (NASDAQ:BIDU), China’s No. 1 search engine. With a Q1 beat and very strong Q2 guidance, this is a top stock to track right now. “The beat was attributed to a series of AI-driven efforts including dynamic ads, which has been described as increasing click-through rates by double digits” explains top Wells Fargo analyst Ken Sena.

He is feeling so encouraged by the company’s outlook that he ramped up his already-bullish price target by $10 to $310. This suggests 22% upside potential. According to Sena, “Baidu’s share currently trades at 24x Adj. 2018E EPS of ¥67.20/$10.59, making it attractive among our Outperform-rated names, particularly when considering the industry leadership it is showing within AI, both as it applies to core (Search, Feed), video, and new initiatives (Apollo, DuerOS).”

Top Oppenheimer analyst Jason Helfstein agrees. He believes Baidu is still undervalued compared to Google, especially when you consider that BIDU is in prime position for the rapid growth of China’s online ad market. “We think key drivers include increasing number of paid clicks, higher conversion rates and higher cost-per-click (CPC). The penetration of smartphones in China, especially in lower tier cities, provides another strong revenue stream for BIDU as it starts to monetize mobile search separately” comments the analyst.

He has a $295 price target on BIDU. Bear in mind that Helfstein’s strong track record on BIDU stock specifically (87% success rate and 21.1% average return per rating) further reinforces the credibility of his latest recommendation.

Compare Brokers

Money-Making Stocks to Buy: Merck (MRK) Our second money-making stock, Merck & Co., Inc. (NYSE:MRK), is one of the world’s largest pharma companies. MRK delivered revenue in 2017 of over $40 billion. The pharma giant is seeing the dollars roll in from its best-selling cancer drug Keytruda. This isn’t surprising given that the drug currently costs a whopping $150,000 per patient per year.

The company has just announced positive Q1 earning results, revealing an unexpectedly robust performance of key franchises outside the U.S.

“Keytruda’s beat reflects Merck’s strong commercial execution. Januvia and Gardasil’s strong demand in ex-US (e.g., China) should also drive growth in the near term” comments top BMO Capital analyst Alex Arfaei. He calls the execution and R&D on Keytruda ‘excellent.’

Investors should keep a close eye on data presented at the upcoming ASCO annual meeting in June advises Arfaei. This will be ‘the next catalyst’ which “should further strengthen the drug’s lead in lung cancer, raise expectations in other tumors, and provide insights on the next set of Keytruda combo data (e.g., with Lenvima).” He has a $70 price target on “Strong Buy” rated MRK (22% upside potential). Indeed, in the last three months, MRK has received four consecutive buy ratings from top-ranked analysts.

Note that Merck is also a top dividend stock. The company pays an impressively high dividend yield of 3.36%. With six straight years of dividend growth under its belt, Merck’s latest quarterly payout came to $0.48 in April.

Money-Making Stocks to Buy: Alexion Pharma (ALXN)

Source: Alexion Pharmaceuticals

US pharma stock Alexion Pharmaceuticals, Inc. (NASDAQ:ALXN) is best known for rare blood disorder drug Soliris. So far this drug has proved extremely successful. Now the company is looking to expand Soliris into new treatment opportunities, including for Generalized Myasthenia Gravis (gMG). This is a chronic autoimmune neuromuscular disease that causes weakness in skeletal muscles.

Five-star Cowen & Co analyst Eric Schmidt calls Alexion a ‘top pick’. He is looking forward to the new possibilities for Soliris in gMG. “We think a favorable financial outlook, strong launch for Soliris in gMG, and increased confidence in ALXN1210’s profile could position ALXN shares for a potential re-rating as investors gain confidence in the growth and durability of the company’s complement franchise,” Schmidt told investors on April 26.

Indeed, the gMG launch is now on track to be the drug’s best-ever launch says Schmidt. He estimates that gMG sales might have reached between $20-25 million. Bearing in mind solid Q1 financials and strong underlying demand trends, Schmidt predicts upside potential of 40%. This would take shares all the way from $118 to $163.

Overall, ALXN demonstrates an overwhelmingly positive outlook from the Street. In the last three months, 14 out of 15 analysts have published ‘Buy’ ratings on ALXN. Their average price target of $157 is 33% above the current share price.

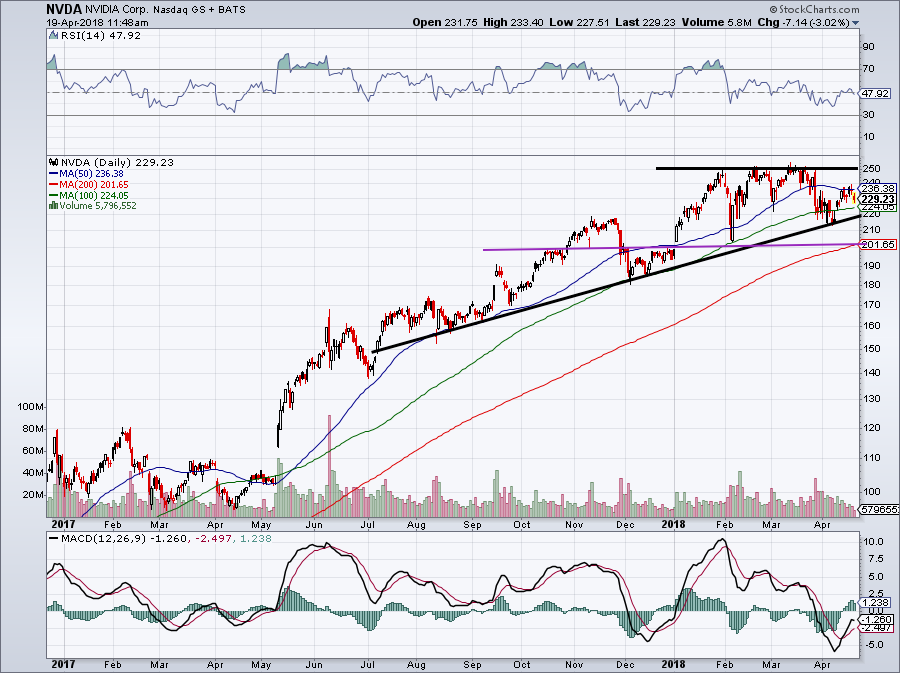

Money-Making Stocks to Buy: Nvidia (NVDA)

NVIDIA Corporation (NVDA) Stock Is at a Serious Tipping Point

Source: via Nvidia

Nvidia Corporation (NASDAQ:NVDA) has received a slew of bullish calls from the Street in the last month. All eyes are on the chip giant right now ahead of its first quarter earnings results on May 10. “Expect beat/raise … We remain positive on NVDA ahead of Q1 results,” five-star Bank of America analyst Vivek Arya told clients on May 7.

“In our view, FQ2 sales outlook can be at-least inline or better than consensus from continued data center strength, start of Nintendo Switch sales, workstation demand, and shift of GPU sales to gamers from miners” this five-star analyst added. He is predicting that prices can soar to $300 from $248 currently.

And the longer-term outlook for NVDA is even more impressive given its ‘unparalleled strength’ in both auto and AI. Top Goldman Sachs analyst Toshiya Hari advises investors not to be alarmed by any short-term choppiness: “Despite the potential near-term volatility, our long-term thesis on the stock is intact — we continue to see Nvidia as one of the best-positioned companies in the Semiconductor space with exposure/leadership in AI, PC gaming, and further down the road in L4/5 autonomous cars.”

SunTrust Robinson’s William Stein agrees. He believes shares have 23% upside right now (which would take shares to $305) and sees huge potential for NVDA in the self-driving space. Meaningful revenue from autonomous driving should hit in the next 2-3 years advises Stein. As a result, he urges investors to buy any weakness.

Money-Making Stocks to Buy: McDonalds (MCD) I recommend taking a closer look at “Strong Buy” stock McDonald’s Corporation (NYSE:MCD) . The fast food chain has a top rating from the Street in general, with a $187 average price target (13.6% upside potential). Following a Q1 earnings beat, the Street swooped in with bullish moves: Goldman Sachs added the stock to its Conviction Buy list; BMO Capital ramped up its price target $5 to $195; as did RBC Capital (from $170 to $175).

RBC Capital’s David Palmer explains that “a better business is worth a consumer staple multiple.” Looking around the corner, Palmer anticipates rapid free cash flow (FCF) growth with FCF conversion of 105%+ by 2020. He explains: “Over the next few quarters, we believe digital and delivery initiatives, more effective value marketing, product renovation, improving operational focus, and asset improvements can re-accelerate sales growth.”

Right now McDonald’s is in the process of bringing fresh cooked-to-order beef patties to all of its U.S. restaurants. “They wanted a hotter and juicier Quarter Pounder, and we wanted to deliver it to them,” says MCD’s manager for Michigan and Oregon. Just switching to fresh beef and delivery alone could each bolster same-store-sales growth by as much as 3-4% when fully rolled out.

And what could be juicier than a fresh Quarter Pounder? A top-rated Dividend Aristocrat. MCD boasts a lucrative quarterly dividend payout of $1.01 on a 2.45% yield. Back in September, the board of directors approved a sizable payout increase of 7% — it’s 41st straight dividend increase.

Money-Making Stocks to Buy: AutoZone (AZO)

Auto parts retailer AutoZone, Inc. (NYSE:AZO) is known as one of the ‘steadiest performers’ in the auto parts retail space. And now the stock has received a big thumbs up from Goldman Sachs’ Matthew Fassler. On May 7 Fassler added AZO to its ‘Conviction Buy’ list. This is a group of elite stocks that the firm expects will outperform the market.

Following a ‘more normative’ winter of 2017-2018, Fassler expects a ‘solid’ summer season as auto parts de-thaw. This can create parts failure — boosting AZO sales. At the same time, sales of auto parts correlate with cars over 10 years old. In 2019 this segment will become more evident as the “last stages of the hangover” from the 2009 financial crisis hit predicts Fassler.

The best part is that AutoZone boasts a “rich” free cash flow yield of 8.5% on 2018 estimates and 8.3% on 2019 estimates. Plus AZO is trading near the low end of its recent historical relative P/E range right now. Note that AutoZone is also a top pick at Fenimore Capital Asset Management.

Interestingly, our data shows AZO as a ‘Moderate Buy’ stock. However, if we limit recent ratings to only those from the best-performing analysts, this consensus shifts to ‘Strong Buy’. Meanwhile, the average price target from these analysts of $819 indicates big upside potential 26% from current levels.

Money-Making Stocks to Buy: MasterCard (MA)

Mastercard Stock

Last, but by no means least, we have online payments giant MasterCard Inc (NYSE:MA). Can this company do no wrong?! Our data shows that MasterCard has 100% support from the Street right now. In the last three months, this breaks down into 11 back-to-back buy ratings. These analysts have an average MasterCard price target of $204 (8% upside potential). Mastercard is the “most innovative and competitively advantaged payments ecosystem participant” with an “impressive” core business trend, writes SunTrust’s Andrew Jeffrey.

Right now analysts are digesting the latest set of positive earnings results. “We like Mastercard’s ability to grow faster than peers and its potential to expand margins. Results for 1Q18 were above expectations, with solid growth across all segments,” cheers Cantor Fitzgerald’s Joseph Foresi. MA reported solid growth across all segments with gross dollar volume growth of 19% year-over-year. For comparison, rival Visa reported 15% y-o-y dollar growth. On the back of these results, MA increased its 2018 revenue guidance range to high-teens from the mid-teens.

This isn’t some kind flash-in-the-pan success either. Foresi states that: “We remain attracted to Mastercard’s card network and strong products and solutions, which should continue to drive solid performance.” Accordingly he boosts his price target from $198 to $213 (13% upside potential).

Source: Investor Place

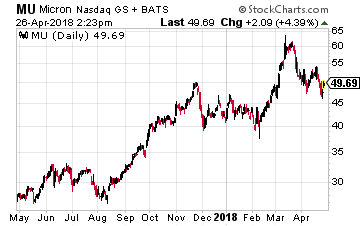

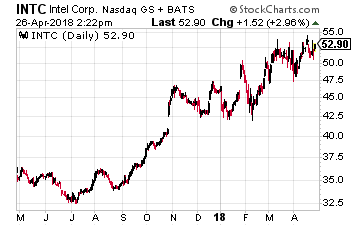

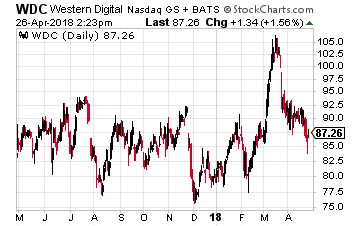

The company that is set to become China’s national champion in semiconductors is Tsinghua Unigroup. That name should be familiar to anyone that follows the chip industry. It made a $23 billion bid for Micron Technology (Nasdaq: MU) and tried to become a major shareholder in Western Digital (Nasdaq: WDC). But those moves were blocked by the U.S. government on national security grounds. So now it is going a different route.

The company that is set to become China’s national champion in semiconductors is Tsinghua Unigroup. That name should be familiar to anyone that follows the chip industry. It made a $23 billion bid for Micron Technology (Nasdaq: MU) and tried to become a major shareholder in Western Digital (Nasdaq: WDC). But those moves were blocked by the U.S. government on national security grounds. So now it is going a different route.

While China’s move is not good news for Samsung, it is so well diversified it will survive. Other companies will be much more affected including Sk Hynix, Toshiba, Western Digital (Nasdaq: WDC) and Micron Technology (Nasdaq: MU).

While China’s move is not good news for Samsung, it is so well diversified it will survive. Other companies will be much more affected including Sk Hynix, Toshiba, Western Digital (Nasdaq: WDC) and Micron Technology (Nasdaq: MU).

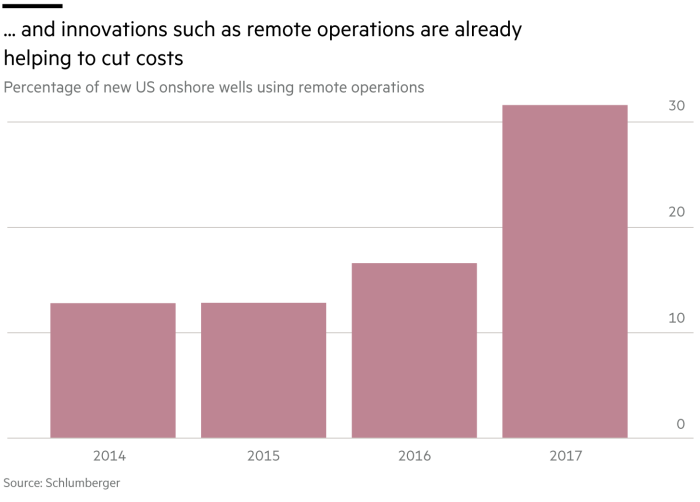

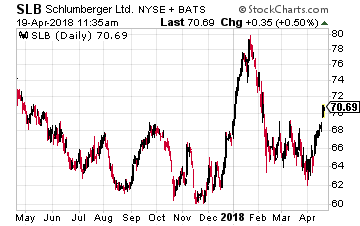

The number one company here is the world’s largest oil field services firm, Schlumberger (NYSE: SLB), which was founded in 1926. A sign of the change in its business since then is the fact that today it has a software technology innovation center that sits at the heart of Silicon Valley.

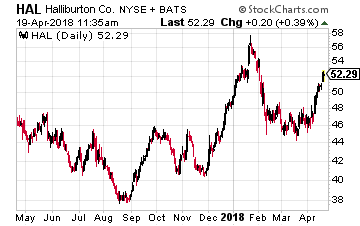

The number one company here is the world’s largest oil field services firm, Schlumberger (NYSE: SLB), which was founded in 1926. A sign of the change in its business since then is the fact that today it has a software technology innovation center that sits at the heart of Silicon Valley. The next company is Halliburton (NYSE: HAL), which is the world’s number two oil field services provider. Like Schlumberger, it is also working with Nvidia on adapting technology for viewing and analyzing seismic data.

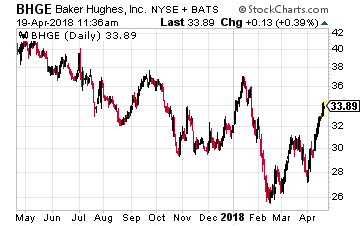

The next company is Halliburton (NYSE: HAL), which is the world’s number two oil field services provider. Like Schlumberger, it is also working with Nvidia on adapting technology for viewing and analyzing seismic data. Finally, there is Baker Hughes (NYSE: BHGE), which is currently 62.5% owned by General Electric. I expect GE to spin this off in the not-too-distant future.

Finally, there is Baker Hughes (NYSE: BHGE), which is currently 62.5% owned by General Electric. I expect GE to spin this off in the not-too-distant future.

But this new tax intended to tax overseas income earned by U.S. technology and pharmaceutical firms and their trademarks and patents has hit closer to home with the railroad company Kansas City Southern (NYSE: KSU), which has a substantial business in Mexico.

But this new tax intended to tax overseas income earned by U.S. technology and pharmaceutical firms and their trademarks and patents has hit closer to home with the railroad company Kansas City Southern (NYSE: KSU), which has a substantial business in Mexico.