For an investor trying to build wealth, the massive amount of news coming out of the financial media can be contradictory and confusing. Investors often don’t realize that there are two sides to every stock trade.

The seller doesn’t want to own the shares for a range of reasons, and the buyer does so with the belief that the share price will go up. One key to success is to understand which financial news is “real” and which is rumor or opinion, and thus “fake.”

Here are some tips that help you decide whether the stock market information you are hearing, or reading is actual, useful information, or is something we can drop into the “fake news” file.

• Real News: Information provided directly from the company behind the stock. The best of these are the quarterly and annual earnings reports. Income statements and balance sheets give accurate pictures of how a company is operating. Also useful are press releases on other topics and management comments during conference calls and Q and A sessions.

• Fake News: Short term market reactions and financial news comments about an earnings report. Wall Street analysts generate earnings forecasts that are just estimates, and the stock market treats it them as hit or miss targets. Also, in the fake news category are financial writer analysis articles. They can be useful to get an educated opinion, but they are not a substitute for doing your own analysis.

• Real News: Dividend payments. Dividends are a cash return on your investment that cannot be clawed back. Dividends are how a company shares profits with shareholders. If a company can grow profits, it will also grow the dividend payments. Looking at history and monitoring continued dividend payments are a great way to monitor a company’s financial success.

• Fake News: Counting on share price gains as sustainable and predictable profits. It can be surprising how quickly a stock that shows as a profit in your brokerage account can drop and wipe out your gains, and even go to a loss.

The challenge of expecting share appreciation to fuel your expected investment returns is that at some point you need to find another investor willing to buy your shares at a higher price. Trying to pick tops and bottoms in the stock market and share prices is a very difficult, if not impossible, way to build and sustain wealth.

• Real News: To build wealth or sustain a nest egg to last for decades, you need an investment strategy that will work through the stock market cycles. This means being ready to manage and invest during corrections and bear markets as well as when stocks are going up. In my newsletters I discuss strategies focused on building a dividend income stream. Whatever system and strategy selected, you should know how you are going to handle the periods when stock values are falling.

• Fake News: Hot tips and get rich quick offers are designed to separate investors from their money and not to help them actually succeed in reaching their investment goals. Think about this: If someone has a system that will turn a few thousand dollars into millions, why do they need to sell it?

The bottom line to this discussion is that successful investing for the long term will be based on fundamental analysis of the companies behind the shares. Dividend history and payments are a great way to track how well a company is doing, and an attractive yield is a great return in itself.

Here are three stocks currently out of favor with the market with great long term potential.

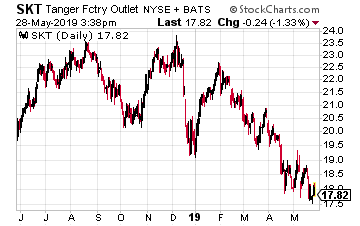

Tanger Factory Outlet Centers, Inc. (SKT) is a pure play owner of outlet style shopping centers. It is the only REIT focused on this type of retail space. Tanger has increased its dividend rate every year since the company’s 1996 IPO.

The recent “fake news” about the end of brick and mortar retail has driven the SKT share price down to around $18, compared to a high over $41 two years ago. The company is financially conservatively managed, and at some point, will resume a growth trajectory. Right now, value oriented investors can pick up shares with a 7.9% yield and annual dividend increases.

History shows that retail trends go through repeating cycles, and when retailers are again opening more stores than closing them, Tanger will be a great stock to own.

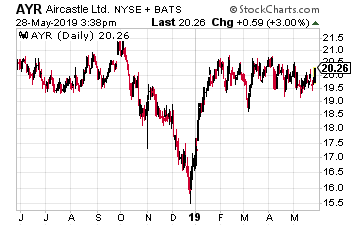

Aircastle Limited (AYR): is an aircraft leasing company that has almost 300 commercial planes leased to airlines around the world.

There are many factors that have “fake” news effects on the Aircastle share price. These include the global economic predictions, forecast travel plans, and the Boeing 737 Max problems. Good news is that Aircastle doesn’t own any 737’s.

Despite all the events that investors believe will affect the company’s results, Aircastle is a very profitable company with steady revenue and free cash flow growth. The dividend will be increased by 6% to 9% per year, generating attractive long term total returns, especially if you add shares on any dips.

Current yield is 6.0%.

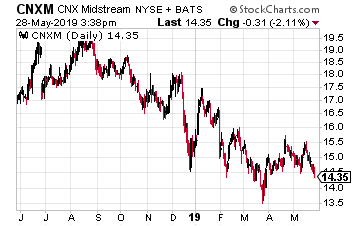

CNX Midstream Partners LP (CNXM) is a is a master limited partnership that owns, operates, develops and acquires gathering and other midstream energy assets to service natural gas production in the Appalachian Basin in Pennsylvania and West Virginia.

This MLP is managed and sponsored by CNX Resources Corporation. The share values of both CNX and CNXM are down on lower natural gas prices. However, as a midstream services provider, CNXM operates as a fee based business whose revenues are not dependent on natural gas prices.

The MLP’s management team has stated they are targeting 15% annual distribution growth. Combine that growth with a current 9.7% yield and you have tremendous total return potential.

Pay Your Bills for LIFE with These Dividend StocksGet your hands on my most comprehensive, step-by-step dividend plan yet. In just a few minutes, you will have a 36-month road map that could generate $4,804 (or more!) per month for life. It's the perfect supplement to Social Security and works even if the stock market tanks. Over 6,500 retirement investors have already followed the recommendations I've laid out.

Click here for complete details to start your plan today.