Have real estate investment trusts (REITs) finally “decoupled” from rising interest rates? In other words, has the popular (but untrue) “rates up, REITs down” reasoning been busted (again)?

For those of us who have been waiting for the stock market’s landlords to carve out a bottom before buying anything new, we may be back in business:

REITs Finally Rising with Rates?

Regular readers know that the best REITs do just fine as rates rise. That’s been the case historically, and they’ll rally again this time around.

Why? Because elite landlords simply keep raising their rents. These higher cash flows translate to higher dividends, and higher stock prices, regardless of what the Fed is up to.

Let’s consider the case of Ventas (VTR), which kept on hiking its payout as Uncle Sam’s 10-year IOU rallied from 2003 to 2006. Its investors were rewarded with total returns (including dividends) of 174% as the 10-year rate rose above 5%:

Ventas Outran the Long Bond

Also as you can see above, it didn’t take Ventas much time to start scaling the rate-induced wall of worry. We’re starting to see the same scenario unfold with the top REITs today.

But what exactly are “the best” REITs? Certainly not retail, where even reliable anchor tenants like grocers are seeing their business models threatened.

Heck, even Ventas is having a rough go of things today. Its dividend growth has slowed considerably in recent years.

We’re better off looking elsewhere. So let’s consider the early leaders – the sectors sparking this budding REIT rally. If it proves to have legs, these are the stocks likely to continue paving the way.

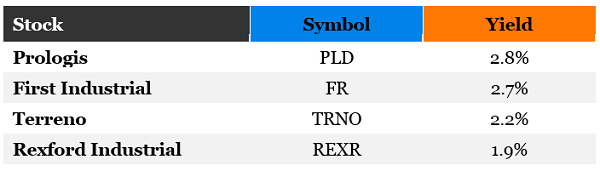

REIT Leader #1: Industrial Space

This asset class is growing just as fast as Amazon. Yet it’s much cheaper and – if you buy right – you can bank a soaring stream of dividends to boot.

“First-level investors” – the basic types who buy and sell of headlines without deeper thought – believe they must purchase Amazon.com (AMZN) itself to profit from the e-commerce boom.

We instead consider what Amazon CEO Jeff Bezos (and other e-commerce entrepreneurs) will need to gobble up themselves to keep their firms growing. By purchasing ahead of their curve, we can then “lease” our asset back to them (at higher and higher rates, of course).

Mark Twain presciently advised readers to invest in land because new supply would be limited. If Twain were advising us today, he’d probably buy warehouses – because they are quickly becoming the most valuable beachfront property in America.

Think about the number of deliveries you receive every week these days. Each package starts in a warehouse somewhere.

The Economist reports that online sellers (including Amazon) will need 2.3 billion square feet of new warehousing to fulfill their increasing order volume. And these firms want their warehouses to be close to big cities (where most of the online orders must be shipped to).

Which landlords is Wall Street buying aggressively? Here’s the rally leaderboard for stocks with momentum, dividends and payout growth:

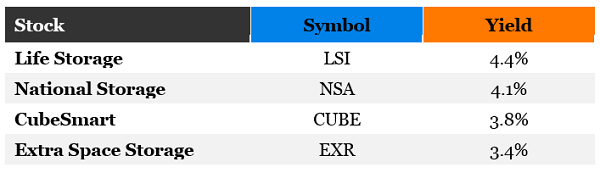

REIT Leader #2: Self-Storage

As Americans acquire more and more “stuff” while they downsize their homes and move into cities, they look for places to put everything. Enter self-storage units, which save you from having to actually purge any of your worldly possessions. For a modest monthly fee (when compared with rent or mortgage payments), you get a slab of space and unlimited visitation rights!

Self-storage is a difficult business to get into. “Not in my backyard” (NIMBY) sentiments often make it difficult to land permits for a new facility.

But once you’re in the business, it’s highly profitable. Operators simply need to divide up the space, hand out unit keys, and make sure the facility doesn’t get too dusty while they cash their monthly rent checks.

Occupancy levels in self-storage facilities are above 90%. Owners don’t have much of a problem renting their facilities, and they are usually able to raise the rent each year – by 3% or more.

It’s traditionally been a fragmented business, with storage facilities run by independent operators. More recently, real estate investment trusts (REITs) have begun to consolidate the space.

The REIT structure is well suited to self-storage. These firms are able to tap the public markets for capital, which they use to buy more facilities. More storage space generates more rent, the bulk of which gets sent to investors in the form of ever-increasing dividend checks.

Recently the stocks in this sector have come under pressure as some markets creep towards saturation. But “storing stuff” is a local phenomenon, and investors are finally sorting and rewarding these stocks accordingly. Here are current REIT-rally leaders, which also boast current yield with yearly dividend growth to boot:

REIT Leader #3: Recession and Rate-Proof Landlords for 7.5%+ Yields with 25% Upside

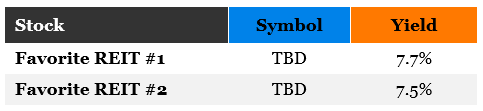

My two favorite REITs today are comfortably positioned in recession-proof industries. They’ll have no problem continuing to raise their rents – and reward their shareholders – no matter what the Fed decides at its next meeting, what Trump tweets or when the stock market finally takes a breather.

My favorite commercial real estate lender lets us play Monopoly from the convenience of our brokerage accounts. They do all the legwork, building a secure, diversified loan portfolio featuring offices, retail space, hotels and multifamily units.

Management then collects the monthly payments, deposits the checks – and then it sends most of the profits our way as dividends (a requirement of its REIT status).

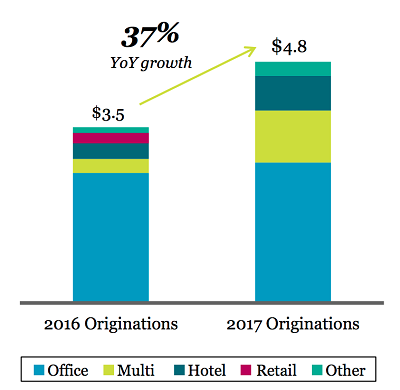

The stock’s current dividend (a 7.7% yield today) is covered by earnings-per-share (EPS) today. And don’t be fooled by the stagnant dividend (not that stability is bad). The firm continues to originate an increasing number of loans:

37% Loan Growth Today Tees Up Dividend Growth Tomorrow

This firm is a conservative lender with perfect loan performance (100%). Its growing portfolio will drive higher profits, which in turn will inspire the next dividend hike. The best time to buy the stock is right now, as it makes the investments which will drive its payout and share price higher from here.

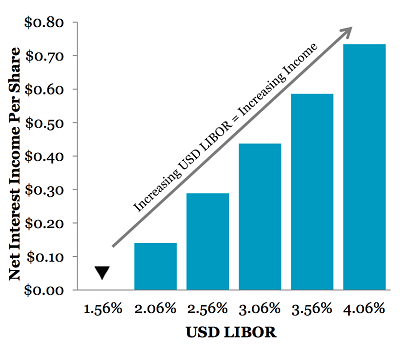

Plus this firm has also smartly eliminated interest rate risk because it uses floating rates. In fact, it’s actually set up to make more money as interest rates move higher:

More Income as Interest Rates Rise

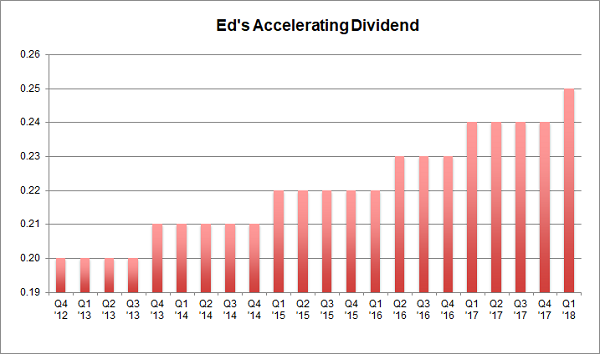

Same for another REIT favorite of mine, a 7.5% payer backed by an unstoppable demographic trend that will deliver growing dividends for the next 30 years. Interest rates are no problem for this landlord because it will simply continue raising the rents on its “must have” facilities.

Its founder Ed admitted that, fourteen years ago, he had “zero assets, a dream, and a business plan.”

Well his dream and plan were plenty – the visionary entrepreneur parlayed them into $6.7+ billion in assets!

And right now is the best time yet to “bet on Ed” because his growing base of assets is generating higher and higher cash flows, powering an accelerating dividend:

I love dividend increases because they are proof that management is actually making more money, so can afford to pay us shareholders more. And an accelerating payout is a flat out cry for help!

Any management team that raises its dividend faster and faster is clearly making more money than it knows what to do with. This usually happens when it achieves a tipping point where its machine no longer requires as much reinvestment to continue growing. So leadership says: “Please, take a bigger raise, shareholders.”

Meanwhile investors and money managers who spot dividend accelerators lose their minds because, in theory, there is no valuation too high for a company that is increasing its dividend at an accelerating rate. Their spreadsheets literally break, and they buy the stock in a frenzy.

Ed’s stock should be owned by any serious dividend investor for three simple reasons:

- It’s recession-proof.

- It yields a fat (and secure) 7.5%.

- Its dividend increases are actually accelerating.

These two REITs are both “best buys” in my 8% No Withdrawal Portfolio – an 8% dividend paying portfolio that lets retirees live on secure payouts alone.

Please don't make this huge dividend mistake... If you are currently investing in dividend stocks – or even if you think you MIGHT invest in any dividend stocks over the next several months – then please take a few minutes to read this urgent new report. Not only could it prevent you from making a huge mistake related to income investing, it could also help you earn 12% a year from here on out! Click here to get the full story right away.

Source: Contrarian Outlook

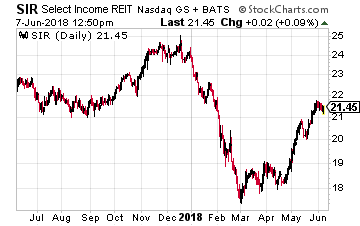

Select Income REIT (Nasdaq: SIR) owns 100 buildings, containing 17 million square feet that are 88.7% leased. In January the company spun off its 266 industrial properties into a new REIT, Industrial Logistics Properties Trust (NYSE: ILPT). SIR retained 69% ownership in the new REIT and consolidates the industrial company results to its income statement. Revenue growth is generated by built in rent escalators and the development of raw land industrial properties at ILPT.

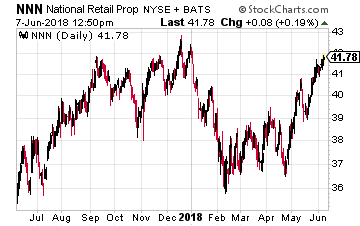

Select Income REIT (Nasdaq: SIR) owns 100 buildings, containing 17 million square feet that are 88.7% leased. In January the company spun off its 266 industrial properties into a new REIT, Industrial Logistics Properties Trust (NYSE: ILPT). SIR retained 69% ownership in the new REIT and consolidates the industrial company results to its income statement. Revenue growth is generated by built in rent escalators and the development of raw land industrial properties at ILPT. National Retail Properties, Inc. (NYSE: NNN) is a traditional triple-net lease REIT. The company owns over 2,800 (up by 300 in the last year) free-standing, single tenant retail properties. most of the REIT’s tenants are in business that cannot be hurt or replaced by online sellers. The top types of businesses are convenience stores, casual and fast food restaurants, auto service shops, fitness outlets, movie theaters and auto parts stores. When acquiring new properties NNN focuses on buying stores with great locations over high quality tenants. The good locations mean that the tenants will be successful and be able to pay the rents. Also, if a tenant does leave, it will be easier to re-lease a property in a great location.

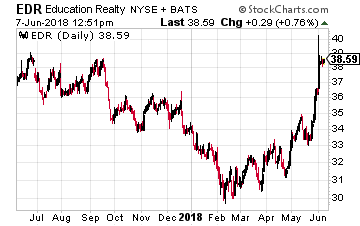

National Retail Properties, Inc. (NYSE: NNN) is a traditional triple-net lease REIT. The company owns over 2,800 (up by 300 in the last year) free-standing, single tenant retail properties. most of the REIT’s tenants are in business that cannot be hurt or replaced by online sellers. The top types of businesses are convenience stores, casual and fast food restaurants, auto service shops, fitness outlets, movie theaters and auto parts stores. When acquiring new properties NNN focuses on buying stores with great locations over high quality tenants. The good locations mean that the tenants will be successful and be able to pay the rents. Also, if a tenant does leave, it will be easier to re-lease a property in a great location. EdR, Inc. (NYSE: EDR) develops, acquires, owns and manages collegiate housing communities located near university campuses. Currently the company owns 79 (up 13 in the last year) communities in 50 different university communities. These communities are located 1/10th to 1/3rd of a mile from the campuses. The college housing business model has produced stable revenue growth, averaging 3.7% per year same store gains. Development and acquisitions boost that core growth rate.

EdR, Inc. (NYSE: EDR) develops, acquires, owns and manages collegiate housing communities located near university campuses. Currently the company owns 79 (up 13 in the last year) communities in 50 different university communities. These communities are located 1/10th to 1/3rd of a mile from the campuses. The college housing business model has produced stable revenue growth, averaging 3.7% per year same store gains. Development and acquisitions boost that core growth rate.

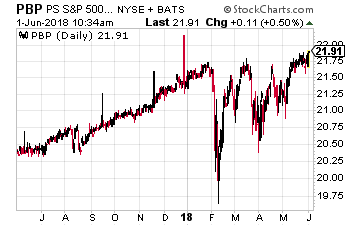

PowerShares S&P 500 BuyWrite ETF (NYSE: PBP) is the largest buy-write ETF by assets under management. As an ETF, the fund tracks a specific index, in this case the CBOE S&P 500 BuyWrite Index.

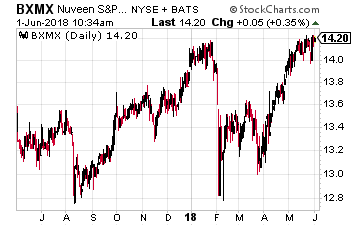

PowerShares S&P 500 BuyWrite ETF (NYSE: PBP) is the largest buy-write ETF by assets under management. As an ETF, the fund tracks a specific index, in this case the CBOE S&P 500 BuyWrite Index. Nuveen S&P 500 Buy-Write Income Fund (NYSE: BXMX) is a closed-end fund that seeks to substantially replicate the price movements of the S&P 500 Index and by selling index call options covering approximately 100% of the Fund’s equity portfolio value with a goal of enhancing the portfolio’s risk-adjusted returns.

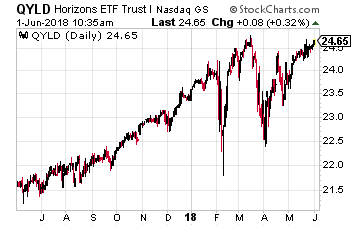

Nuveen S&P 500 Buy-Write Income Fund (NYSE: BXMX) is a closed-end fund that seeks to substantially replicate the price movements of the S&P 500 Index and by selling index call options covering approximately 100% of the Fund’s equity portfolio value with a goal of enhancing the portfolio’s risk-adjusted returns. Horizons NASDAQ 100 Covered Call ETF (Nasdaq: QYLD) is an ETF that tracks the CBOE NASDAQ-100® BuyWrite Index. As a result, this ETF will be more focused on the large technology stocks that make up a large part of the Nasdaq 100 stock index.

Horizons NASDAQ 100 Covered Call ETF (Nasdaq: QYLD) is an ETF that tracks the CBOE NASDAQ-100® BuyWrite Index. As a result, this ETF will be more focused on the large technology stocks that make up a large part of the Nasdaq 100 stock index. Nuveen Nasdaq 100 Dynamic Overwrite Fund (Nasdaq: QQQX) is a closed-end fund using the Nasdaq 100 Stock Index as its basis for covered call writing.

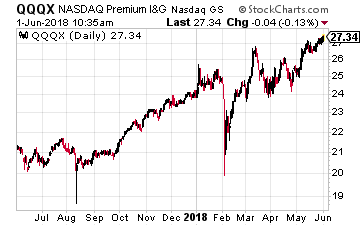

Nuveen Nasdaq 100 Dynamic Overwrite Fund (Nasdaq: QQQX) is a closed-end fund using the Nasdaq 100 Stock Index as its basis for covered call writing. First Trust Enhanced Equity Income Fund (NYSE: FFA) is a closed-end fund where the managers actively manage the stock portfolio and enhance income by selling call options.

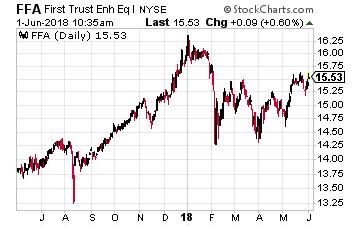

First Trust Enhanced Equity Income Fund (NYSE: FFA) is a closed-end fund where the managers actively manage the stock portfolio and enhance income by selling call options.

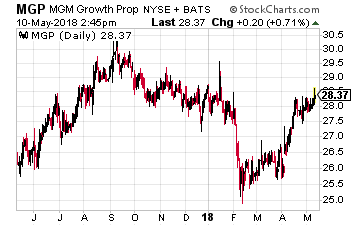

In April 2016, hotel and gaming company MGM Resorts International (NYSE: MGM) spun off about two-thirds of its hotel properties into a new real estate investment trust (REIT) IPO. MGM structured the new company, called MGM Growth Properties LLC (NYSE: MGP), to have a high level of cash flow safety to pay the planned dividend and with the potential for future growth.

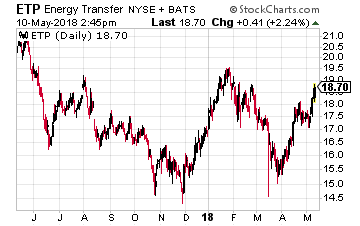

In April 2016, hotel and gaming company MGM Resorts International (NYSE: MGM) spun off about two-thirds of its hotel properties into a new real estate investment trust (REIT) IPO. MGM structured the new company, called MGM Growth Properties LLC (NYSE: MGP), to have a high level of cash flow safety to pay the planned dividend and with the potential for future growth. At the end of 2017 I forecast that the energy midstream/infrastructure sector would return to valuation growth in 2018 providing lots of upside potential in the group. Through 2017 MLP sector market values declined sharply even as business fundamentals continued to improve. 2018 should be the year when investors realize very attractive returns from the quality companies in the sector.

At the end of 2017 I forecast that the energy midstream/infrastructure sector would return to valuation growth in 2018 providing lots of upside potential in the group. Through 2017 MLP sector market values declined sharply even as business fundamentals continued to improve. 2018 should be the year when investors realize very attractive returns from the quality companies in the sector.