With the U.S. stock market fresh off its first quarterly loss since 2015, many conservative investors are in need of dividend stock ideas that can provide safe income and preserve their capital over the long term.

Using Dividend Safety Scores, a system created by Simply Safe Dividends to help investors avoid dividend cuts in their portfolios, we identified 10 high-quality dividend stocks from traditionally defensive sectors like telecom, healthcare and consumer staples.

These stocks have an impeccable record of paying continuous dividends over the years given their durable business models, strong cash flows and disciplined approach to capital allocation.

Many of these companies are also in Simply Safe Dividends’ list of the best high dividend stocks here and trade at yields above their five-year averages, providing an attractive combination of current income and growth.

Let’s take a look at 10 of the best safe dividend stocks for the second quarter.

Safe Dividend Stocks: AT&T (T)

Sector: Telecom Services

Industry: Integrated Telecommunication Services

Dividend Yield: 5.6%

5-Year Average Yield: 5.2%

AT&T Inc. (NYSE:T) is a global leader in telecommunications, media and technology. The company provides wireless and wireline communications services, including data, broadband and voice, digital video services, telecommunications equipment and other services.

AT&T has a huge customer base consisting of 157 million wireless subscribers, over 12 million internet subscribers and around 25 million video customers.

Few companies can compete with AT&T’s massive scale, which allows it to invest heavily in the quality and coverage of its cable, wireless, and satellite networks. In fact, AT&T is planning to deploy the next generation 5G wireless technology in 12 U.S. markets by late 2018.

Should AT&T’s acquisition of Time Warner be completed, the deal has potential to create value for shareholders and customers by combining its strong distribution capabilities with Time Warner’s large content portfolio.

While this deal will increase AT&T’s debt burden, Simply Safe Dividends estimates that the combined company’s free cash flow payout ratio will sit around 70% to 80%, which is sustainable for a cash cow with recession-resistant services like AT&T. Investors can read the firm’s in-depth dividend stock analysis on AT&T here.

AT&T has recorded 34 consecutive years of quarterly dividend growth and last raised its payout by 2% in late 2017. An improving balance sheet and moderately growing demand for faster delivery of video and data services should enable the company to continue raising its dividend at a low single-digit pace.

Safe Dividend Stocks: Pfizer (PFE)

Source: Shutterstock

Sector: Healthcare

Industry: Pharmaceuticals

Dividend Yield: 3.8%

5-Year Average Yield: 3.5%

Pfizer Inc. (NYSE:PFE) is a global biopharmaceutical giant engaged in the development and manufacture of healthcare products. It is one of the largest global pharmaceuticals companies, with 2017 revenues exceeding $52 billion.

Founded in 1849, Pfizer has come a long way to become a leading healthcare company, with manufacturing sites in 63 locations and sales in 125 countries. The company has a wide portfolio of medicines, vaccines and consumer healthcare products and is known for popular drugs like Prevnar and Viagra, among others.

The company’s business can be divided into two distinct business segments — Pfizer Innovative Health (focusing on six therapeutic areas like oncology) which accounted for 60% of 2017 revenues and Pfizer Essential Health (legacy drugs that have lost patent protection) comprising the remaining 40%.

A relatively recession-proof business model, diversified portfolio of R&D intensive products, and global scale create a competitive moat around the company.

Pfizer is also benefiting from U.S. tax reform, which has driven the firm to repatriate most of its cash held overseas and aggressively return cash to shareholders.

The company last raised its dividend by 6.3% in December 2017, and mid-single-digit growth is likely to continue. In fact, management expects 11% earnings growth in 2018, and rising global demand for healthcare should continue to serve as a long-term tailwind.

Income investors can read Simply Safe Dividends’ comprehensive analysis on Pfizer’s business here.

Safe Dividend Stocks: Procter & Gamble (PG)

Sector: Consumer Staples

Industry: Household Products

Dividend Yield: 3.5%

5-Year Average Yield: 3.1%

Procter & Gamble Co (NYSE:PG) is a leading global consumer goods company. With more than 180 years of existence, the company is today an international household name, selling products in more than 175 countries.

Accounting for 32% of total sales in 2017, fabric and home care is Procter & Gamble’s biggest segment, followed by baby, feminine and family care (28%), beauty (18%), grooming (11%) and health (11%) segments.

By geography, North America is P&G’s largest market (45% of sales) while developing economies account for 35% of its total sales.

A diverse portfolio of iconic brands (Ariel, Bounty, Braun, Olay, Pantene etc.), strong consumer loyalty, and a global sales network have made P&G one of strongest consumer goods companies in the world.

In recent years the company has restructured its brand portfolio (from 170 in 2013 to 65 today) to focus more on stronger product lines with faster growth and greater profitability. The company also has targeted to save $10 billion in operating costs between fiscal year 2017 and 2021.

Despite its modest growth profile, Procter & Gamble has an impeccable record of paying consecutive dividends over the last 127 years. It last raised its dividend by 3% in 2017, marking it the 61st consecutive dividend increase and reinforcing its status as a dividend king (see all the dividend kings here).

The company is targeting up to $70 billion in capital returns through fiscal 2019 and 5% to 7% in core earnings per share growth. This should enable the company to comfortably continue its dividend growth streak.

Safe Dividend Stocks: United Parcel Services (UPS)

Sector: Industrials

Industry: Air Freight and Logistics

Dividend Yield: 3.4%

5-Year Average Yield: 2.9%

United Parcel Service, Inc. (NYSE:UPS) is a holding in Warren Buffett’s dividend portfolio hereand is the world’s largest package delivery and logistics company. It is also a premier provider of global supply chain management solutions.

The company operates through three segments: U.S. Domestic Package (62% of 2017 revenue), International Package (20%) and Supply Chain & Freight (18%).

UPS has a balanced presence globally delivering 20 million packages and documents each day in more than 220 countries. The US is its largest market with 79% of sales while Europe is the largest among international markets (21%).

The company has an extensive global logistics and distribution system consisting of 2,500 worldwide operating facilities, 119,000 vehicles and over 500 aircraft. Upstarts and smaller rivals cannot afford to invest in such a transportation network, and they lack UPS’s package volumes which help the company achieve meaningful cost efficiencies.

Thanks to its advantages, UPS has been paying generous cash dividends for the last 50 years. The company’s recent payout boost in late 2017 represented a 10% increase over the prior year, and analysts expect 2018 adjusted diluted earnings per share to grow by 20% thanks largely to tax reform.

Given the continued surge in global online shopping trends and long-term growth in global trade, the company should be able to continue increasing its dividend comfortably in the high single to low double-digit range.

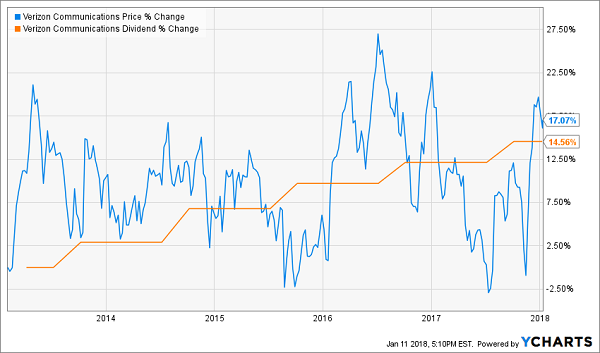

Safe Dividend Stocks: Verizon Communications (VZ)

Sector: Telecom Services

Industry: Integrated Telecommunication Services

Dividend Yield: 4.9%

5-Year Average Yield: 4.5%

Verizon Communications Inc (NYSE:VZ) is the biggest provider of wireless service in the U.S. with 116.3 million retail customers and enjoys a duopoly position with AT&T, Sprint Corp (NYSE:S) and T-Mobile US Inc (NASDAQ:TMUS).

The company has the largest 4G LTE network (with 97.9 million retail postpaid connections) and is available to over 98% of the U.S. population. Although wireless operations generate over 80% of the company’s cash flow, Verizon’s superior fiber-optic technology also enables high speed broadband internet and has been ranked No.1 for internet speed ten years in a row by PC Magazine.

Customers prefer Verizon for its highly reliable wireless services, which are made possible by substantial investments in its network each year. The company also owns highly valuable and scarce telecom spectrum licenses, which form a strong entry barrier for new entrants.

Verizon is also leading the 5G wireless technology development over the last few years to reinforce its strong position, and it has plans to launch 5G wireless residential broadband services in three to five U.S. markets this year.

With tax reform freeing up several billion dollars more of cash flow this year, and management’s plans to cut $10 billion in costs by 2022, Verizon’s dividend remains on solid ground.

Verizon recorded its 11th consecutive dividend increase in 2017 with a 2.2% raise, and low-single-digit growth is likely to continue in the years ahead as the company trims its cost base and benefits from growing demand for high speed data and internet.

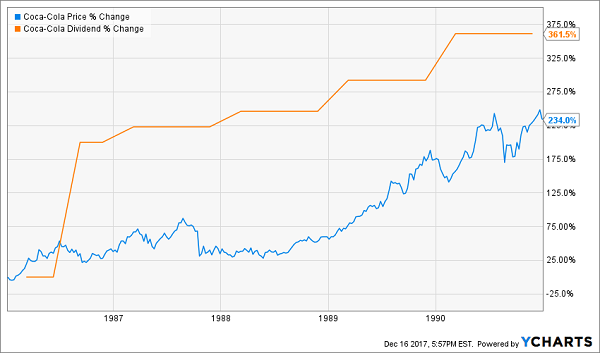

Safe Dividend Stocks: Coca-Cola (KO)

Sector: Consumer Staples

Industry: Soft Drinks

Dividend Yield: 3.5%

5-Year Average Yield: 3.2%

The Coca-Cola Co (NYSE:KO) is one of the largest beverage companies in the world, manufacturing and distributing more than 500 non-alcoholic drink brands. It owns four of the world’s top five sparkling soft drink brands — Coca-Cola, Diet Coke, Fanta and Sprite.

Coca-Cola’s activities can be grouped into five operating segments — Europe, Middle East and Africa (21% of 2017 revenues); Latin America (11%); North America (24%); Asia Pacific (14%); and Bottling Investments (30%).

Coca-Cola owns the world’s largest distribution system that enables seamless sales to 27 million customer outlets in more than 200 international markets. This distribution network serves as a major advantage as the company evolves its product mix.

As a result of increased customer health awareness, the company is focusing on constructing a healthier portfolio by introducing products like Coca-Cola zero sugar.

The Coca-Cola Company is a dividend aristocrat (see all the aristocrats here) that has increased dividends in each of the last 56 years and last raised its payout by 5%. The company has a target of a 75% payout ratio and 7% to 9% earnings growth over the long term.

Given its industry leading position, strong brands, and huge international presence, Coca-Cola should be able to continue delivering mid-single-digit dividend growth in future.

Safe Dividend Stocks: Merck (MRK)

Source: Shutterstock

Sector: Healthcare

Industry: Pharmaceuticals

Dividend Yield: 3.6%

5-Year Average Yield: 3.1%

Merck & Co., Inc. (NYSE:MRK) is a global healthcare company with a rich operating history exceeding 120 years. The company provides a host of prescription medicines, vaccines, biologic therapies and animal health products.

Geographically, the U.S. is its largest market with 43% of 2017 revenues, followed by EMEA, Asia Pacific, Japan, Latin America and others.

Merck’s core product categories include drugs for diabetes and cancer as well as vaccines and hospital acute care. A few of Merck’s best-selling products are Januvia (industry leading diabetic drug), Keytruda (cancer drug), Zetia and Remicade. The company’s 12 main drugs accounted for 53% of total sales in 2017.

The company spends heavily on R&D (18% of sales in 2017) to continuously rebuild its drug pipeline and deliver innovative health solutions. As a result, Merck is in a solid position to benefit from the growing demand for oncology treatments. The company has also been restructuring its business to cut long-term costs.

Merck has a rich history of paying uninterrupted dividends for nearly three decades and has increased dividends for seven years in a row. Its last dividend was raised by 2%, which is in line with its 10-year annual dividend growth rate.

Given the company’s disciplined capital allocation and reasonable payout ratio below 50%, Merck is poised to continue growing its payout in the future.

Safe Dividend Stocks: Altria (MO)

Sector: Consumer Staples

Industry: Tobacco

Dividend Yield: 4.4%

5-Year Average Yield: 4.0%

Altria Group Inc (NYSE:MO) is the undisputed market leader in the U.S. tobacco industry. The company has exclusive rights to sell cigarettes under a handful of leading brands including Marlboro, Virginia Slims, Parliament and Benson & Hedges. Altria also sells cigars, chewing tobacco and wine.

Marlboro has been the leading U.S. cigarette brand for over 40 years, and Copenhagen and Skoal account for more than 50% of the smokeless products category. Cigarette brands tend to have a high degree of stickiness, with customers having a very low preference to switch to other brands and a greater tolerance to pay higher prices given the addictive nature of tobacco.

With a long history of manufacturing cigarettes dating back 180 years, Altria has built a dominant market position over the years, resulting in a steady and growing stream of cash flow that has funded solid dividend growth.

In fact, Altria’s latest dividend raise earlier this year was 6%, representing its 52nd dividend increase in the past 49 years. Altria has a target dividend payout ratio of 80% with annual earnings growth of 7% to 9% expected over the long term. This should allow the company to keep growing dividends at a mid to high single-digit clip going forward.

Safe Dividend Stocks: AbbVie (ABBV)

AbbVie Inc (NYSE:ABBV) is a research-driven global healthcare company, focusing on developing and delivering drugs in therapeutic areas like immunology, oncology, neuroscience, virology and general medicine. The company generates over 60% of its revenue (and an even greater share of profits) from its arthritis drug Humira.Sector: Healthcare

Industry: Biotechnology

Dividend Yield: 4.2%

5-Year Average Yield: 3.5%

Humira’s revenue stream in the U.S. is expected to be largely protected from competition through 2022 thanks to a number of patents owned by AbbVie. Meanwhile, AbbVie’s R&D expertise has helped the company develop a strong late-stage pipeline of promising medicines across several therapeutic areas which could potentially be converted into successful products in the near future.

The company recently experienced a setback as Rova-T, a lung cancer drug that was a key part of AbbVie’s plans to diversify its future profits, experienced achieved disappointing trial results, suggesting its overall impact on the company’s future results would be somewhat muted.

However, the company remains a cash cow with a handful of growth drivers and a reasonable payout ratio near 50%. Management continues cranking up the dividend, most recently announcing a 35% boost earlier this year.

New product launches and increasing demand for medicines both from developed and developing economies should help AbbVie grow its dividends at a solid rate going forward, but investors considering the stock do need to have a stomach for volatility given AbbVie’s drug concentration.

Safe Dividend Stocks: Cisco (CSCO)

Sector: Information Technology

Industry: Communications Equipment

Dividend Yield: 3.2%

5-Year Average Yield: 3.2%

Cisco Systems, Inc. (NASDAQ:CSCO) is a leading global technology company inventing new technologies and products that have been powering the internet for more than three decades.

Product sales account for approximately 75% of total sales while services comprise the remainder of the business. Switching and routing are the most prominent product categories followed by collaboration, data center, wireless, security and service provider video.

The company’s service revenue is composed of software, subscriptions, and technical support offered across its different segments. Cisco’s customers are highly diversified and include businesses of all sizes, public institutions, governments and service providers.

Cisco has a large worldwide sales and marketing network with field offices in 95 countries, strong R&D capabilities, and a massive patent portfolio. Market leadership, breadth of portfolio, global scale and customer loyalty are its key competitive advantages. Investors can read in-depth analysis of Cisco’s business here.

Cisco is also shifting its business towards a software and subscriptions model which will lead to a higher visibility of its cash flows. Currently, recurring revenue accounts for 33% of total sales, and more than half of software revenue is subscription based revenue.

Cisco recently increased its dividend by 14% and has targeted to return at least half of its free cash flow to shareholders annually. The company’s solid cash flow and sub-50% payout ratio should allow for continued dividend growth in the years ahead.

Get up to 14 dividend paychecks per month from safe, reliable stocks with The Monthly Dividend Paycheck Calendar, an easy-to-use system that shows you which dividend stocks to pick, when to buy them, when you get paid your dividends, and how much. All you have to do is buy the stocks you like and tell them where to send your dividend payments.

For more information Click Here.Source:

Investors Alley

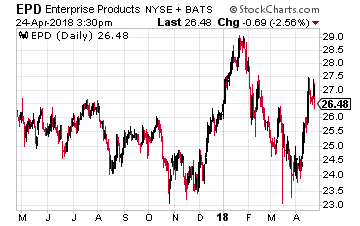

Enterprise Products Partners LP (NYSE: EPD) with a $57 billion market cap is the largest midstream MLP. The company provides the full range of energy infrastructure services. EPD is one of the biggest pipeline service providers to transport crude oil from the Permian to the Texas Gulf Coast. It recently announced that its 416-mile Midland-to-Sealy pipeline is now in full service with an expanded capacity of 540,000 barrels per day (BPD) and capable of transporting batched grades of crude oil.

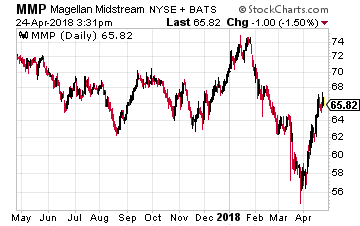

Enterprise Products Partners LP (NYSE: EPD) with a $57 billion market cap is the largest midstream MLP. The company provides the full range of energy infrastructure services. EPD is one of the biggest pipeline service providers to transport crude oil from the Permian to the Texas Gulf Coast. It recently announced that its 416-mile Midland-to-Sealy pipeline is now in full service with an expanded capacity of 540,000 barrels per day (BPD) and capable of transporting batched grades of crude oil. Magellan Midstream Partners LP (NYSE: MMP) primarily owns and operates refined products (gasoline, diesel fuel, jet fuel, etc.) pipelines and storage terminals. The company also owns 2,200 miles of interstate crude oil pipelines. The company provides service to almost 50% of the U.S. refining capacity.

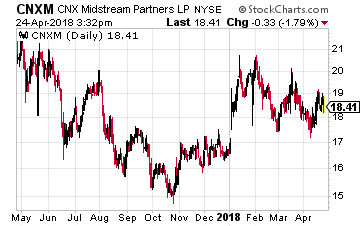

Magellan Midstream Partners LP (NYSE: MMP) primarily owns and operates refined products (gasoline, diesel fuel, jet fuel, etc.) pipelines and storage terminals. The company also owns 2,200 miles of interstate crude oil pipelines. The company provides service to almost 50% of the U.S. refining capacity. CNX Midstream Partners LP (NYSE: CNXM) owns, operates, develops and acquires gathering and other midstream energy assets to service natural gas production in the Appalachian Basin in Pennsylvania and West Virginia. This MLP primarily provides gathering and processing services to CNX Resources Corp (NYSE: CNX), which is also the sponsor and holds the MLP’s general partner interests.

CNX Midstream Partners LP (NYSE: CNXM) owns, operates, develops and acquires gathering and other midstream energy assets to service natural gas production in the Appalachian Basin in Pennsylvania and West Virginia. This MLP primarily provides gathering and processing services to CNX Resources Corp (NYSE: CNX), which is also the sponsor and holds the MLP’s general partner interests.

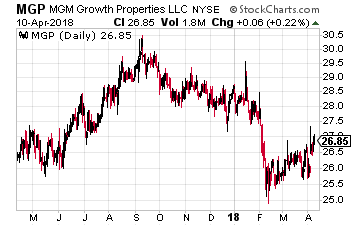

MGM Growth Properties LLC (NYSE: MGP) is a real estate investment trust that came to market in April 2016. As the name indicates, the new REIT was spun-off by hotel and gaming company MGM Resorts International (NYSE: MGM). At the IPO, MGM Growth Properties received title to seven properties on the Las Vegas Strip:

MGM Growth Properties LLC (NYSE: MGP) is a real estate investment trust that came to market in April 2016. As the name indicates, the new REIT was spun-off by hotel and gaming company MGM Resorts International (NYSE: MGM). At the IPO, MGM Growth Properties received title to seven properties on the Las Vegas Strip:

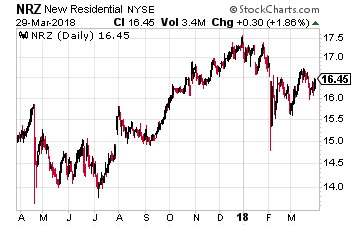

New Residential Investment Corp. (NYSE: NRZ) is a finance REIT that invests in products that are on the financial fringe of the residential mortgage industry. The largest investment is in mortgage servicing rights –MSRs. These are the contractual fees the mortgage servicing company receives out of the interest paid on a home mortgage. MSRs are typically 25 basis points (0.25%) per year. The cost to service a mortgage is typically less than 10 bp. The rest is profit to the company that owns the MSRs. New Residential owns full or excess MSRs on over half a trillion dollars of unpaid mortgage balances. 25 basis points of that much loan balance is a lot of cash flow!

New Residential Investment Corp. (NYSE: NRZ) is a finance REIT that invests in products that are on the financial fringe of the residential mortgage industry. The largest investment is in mortgage servicing rights –MSRs. These are the contractual fees the mortgage servicing company receives out of the interest paid on a home mortgage. MSRs are typically 25 basis points (0.25%) per year. The cost to service a mortgage is typically less than 10 bp. The rest is profit to the company that owns the MSRs. New Residential owns full or excess MSRs on over half a trillion dollars of unpaid mortgage balances. 25 basis points of that much loan balance is a lot of cash flow!