The world of medicine is quickly moving from the pages of a science fiction novel to reality. Imagine a time when a person’s cells are “re-engineered” to recognize and attack cancer, so that conventional therapies are not needed.

Well, that time is upon us. Immunotherapy – therapies that use and strengthen the power of a patient’s immune system to attack cancers – has emerged in what many are calling the “fourth pillar” of cancer treatment joining surgery, radiation therapy and chemotherapy.

The immunotherapy that is closest to actually helping cancer patients is called Car T-cell therapy. After literally decades of painstaking research, the field has reached a tipping point, with several companies producing very promising results recently.

If you are unfamiliar with the term CAR-T, it stands for chimeric antigen receptor cell therapy. But before I reveal to you those companies that have had outstanding trial results, let me fill you in on what exactly CAR-T therapy is, which some doctors describe as a “living drug”.

What is CAR-T?

Here in general is how the Car-T process works:

Millions of a patient’s white blood cells are extracted through a process called apheresis. These cells are then sent on to a lab where scientists isolate T-cells from the white blood cells. T-cells are often called the ‘workhorses’ of the immune system because of their crucial role in orchestrating a response from our immune systems, killing cells infected by pathogens.

The next step, using a ‘disarmed’ virus, involves genetically modifying these T-cells to produce chimeric antigen receptors on their surface. This process once took a six-week period, but the times for cell modification have now been greatly reduced.

These chimeric antigen receptors allow the T-cells to recognize and attach to a specific protein, or antigen, found on cancer cells. Additionally, scientists believe modified T-cells have the ability to reactivate other immune system elements that have been suppressed by the cancer. They ‘talk’ to other cells of the immune system using chemicals known as cytokines.

Once these modified T-cells have been produced in the laboratory, they are ‘expanded’ by scientists to number in the hundreds of millions.

After receiving the chimeric antigen receptor CAR T-cells back from the lab, doctors infuse them back into the patient’s body. But not before one final round of chemotherapy, called lymphodepleting, which eradicates out the existing T-cells. This allows the re-engineered cells more room to multiply themselves and (hopefully) attack the cancer.

Now let me tell you about some of the companies that have had recent successful trials for Car-T therapies that were reported at the focus of the biotech world this week – the annual meeting of the American Society of Hematology in Atlanta.

Related: 3 Stocks for Double Digit Gains from Personalized Medicine

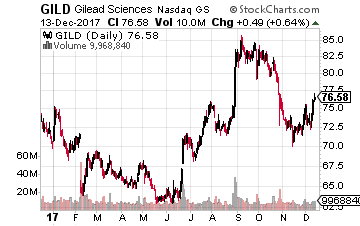

Car-T Therapy Company #1 – Gilead Sciences

The first company I want to tell you about is Gilead Sciences (Nasdaq: GILD), which revealed results of a trial that took place at the University of Texas on December 10. The trial was conducted by what is now a subsidiary of Gilead – Kite Pharma – that was acquired in August for $11.9 billion.

The first company I want to tell you about is Gilead Sciences (Nasdaq: GILD), which revealed results of a trial that took place at the University of Texas on December 10. The trial was conducted by what is now a subsidiary of Gilead – Kite Pharma – that was acquired in August for $11.9 billion.

Gilead’s product, Yescarta, was given an okay by the FDA in October. The trial results showed that after a median period of 15.4 months, 59% of patients with non-Hodgkin lymphoma were still alive, while 42% were in remission and 40% exhibited absolutely no trace of cancer. That is quite a contrast to existing therapies, where the median survival time for people at stage of this disease is only six months!

This is a key point because most of the doubters of Car-T therapies expressed reservations about the longevity of the effects of the treatment. But apparently, the modified T-cells do remain in a patient’s system, guarding against recurrence of the cancer.

Gilead sees the long-term promise of these types of therapies and bought a second Car-T company, Cell Design Labs, recently for $567 million. Going big into Car-T therapies should, over the long term, boost the company’s stock which is up only 6% year-to-date.

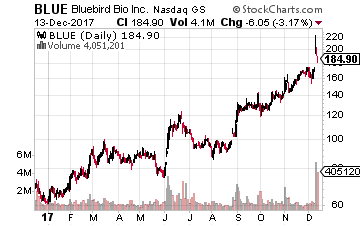

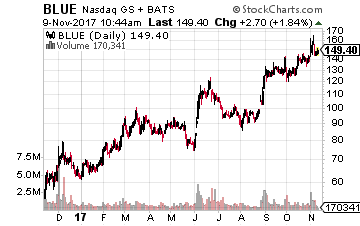

Car-T Therapy Company #2 – Bluebird Bio

The second company, which revealed spectacular trial results at the Atlanta conference, is Bluebird Bio (Nasdaq: BLUE). The stock soared about 30% on December 11 and is now up about 225% year-to-date!

The second company, which revealed spectacular trial results at the Atlanta conference, is Bluebird Bio (Nasdaq: BLUE). The stock soared about 30% on December 11 and is now up about 225% year-to-date!

A novel therapy from Bluebird Bio and Celgene (Nasdaq: CELG) was given to 18 multiple myeloma patients that were nearing death (four months expected left to live) from a very aggressive form of the cancer. A single infusion of bb2121 at the highest dose generated an 86% overall response rate and all but one of the patients saw a clinical benefit. After nine months, 56% of the patients were in remission – an improvement from May when only 27% of the patients were in remission (again those beneficial long-term effects).

The results are important because, despite advances in drug therapy improving survival from three years to 8-10 years, multiple myeloma is still largely incurable.

This apparently successful Bluebird therapy targeted the BCMA protein that is found on myeloma and plasma cells. Targeting that particular protein is a path also taken by other companies involved with Car-T therapies – Novartis AG (NYSE: NVS) and GlaxoSmithKline PLC (NYSE: GSK).

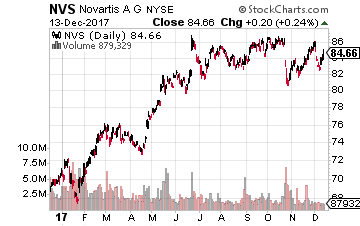

Car-T Therapy Company #3 – Novartis

That brings me to the third Car-T company with promising results presented in Atlanta, Novartis, and its Kymriah therapy, which was given the go-ahead by the FDA in August. The stock of this pharma giant is up over 15% year-to-date.

That brings me to the third Car-T company with promising results presented in Atlanta, Novartis, and its Kymriah therapy, which was given the go-ahead by the FDA in August. The stock of this pharma giant is up over 15% year-to-date.

New analysis of trial data for Kymriah presented at the conference showed that the drug sustained complete responses in adults with a difficult to treat form of blood cancer – diffuse large B-cell lymphoma (DLBCL).

The overall response rate among patients was 53%, with 40% achieving a complete response and 14% a partial response. At six months, 30% of patients were in complete response, with a 74% rate relapse-free rate after the onset of response. Again, very promising longer-term results.

The Good and the Bad

Will these life-saving therapies become commonplace, benefiting these companies and, most importantly, the patients?

There are two obstacles as I see it. The first one includes the side effects from these therapies.

In the attempt to kill cancer cells, the treatment effectively sends the immune system into overdrive. That jacked-up immune response can often cause something called cytokine-release syndrome. The cells that the engineered T-cells target release a group of proteins known as cytokines, triggering a massive inflammatory response. This can be too much for the body to handle, and can cause life-threatening side effects like severely high fevers, dangerously low blood pressure or even a temporary inflammation in the brain.

Luckily, both the drug companies and the doctors are making improvements along this line… the actual side effects are less severe than in the original trials and the doctors are getting better at managing the side effects in patients.

The bigger obstacle may be the cost, thanks to the still very complicated process to engineer a patient’s T-cells. The cost is possibly the highest ever seen in the drug industry. For example, Gilead charges $373,000 for Yescarta, while Novartis put a price tag of $475,000 on Kymriah, although it says it will offer refunds if the treatment does not work.

Prices though should drop as Car-T therapies become more common. That makes a company like Bluebird Bio worth a look by you on any pullback as a long-term investment.

Buffett just went all-in on THIS new asset. Will you?

Buffett could see this new asset run 2,524% in 2018. And he's not the only one... Mark Cuban says "it's the most exciting thing I've ever seen." Mark Zuckerberg threw down $19 billion to get a piece... Bill Gates wagered $26 billion trying to control it...

What is it?

It's not gold, crypto or any mainstream investment. But these mega-billionaires have bet the farm it's about to be the most valuable asset on Earth. Wall Street and the financial media have no clue what's about to happen...And if you act fast, you could earn as much as 2,524% before the year is up.

Click here to find out what it is.

Source: Investors Alley

One very conservative way is through an exchange traded fund – the Ark Innovation ETF (NYSE: ARKK). The goal of this fund is to provide investors like you with exposure to innovation and new technologies across a broad range of sectors. The ARKK ETF owns a position in the aforementioned Bitcoin Investment Trust. The Bitcoin Investment Trust is the number one position in its current 53 stock portfolio and it makes up 6.79% of the overall ARKK investment portfolio. In other words, any major selloff (noted short seller Andrew Left is short GBTC) won’t devastate the fund.

One very conservative way is through an exchange traded fund – the Ark Innovation ETF (NYSE: ARKK). The goal of this fund is to provide investors like you with exposure to innovation and new technologies across a broad range of sectors. The ARKK ETF owns a position in the aforementioned Bitcoin Investment Trust. The Bitcoin Investment Trust is the number one position in its current 53 stock portfolio and it makes up 6.79% of the overall ARKK investment portfolio. In other words, any major selloff (noted short seller Andrew Left is short GBTC) won’t devastate the fund.

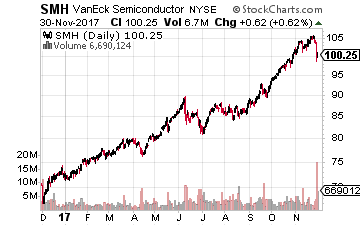

The first and the broadest way you can invest in semiconductors is the MarketVectors Semiconductor ETF (NYSE: SMH). It owns 26 of the world’s top semiconductor-related companies such as Intel. The only major stock not in this portfolio is Samsung. This ETF has, of course, done very well for its holders. It has soared over 50% over the past year and is up about 42% year-to-date.

The first and the broadest way you can invest in semiconductors is the MarketVectors Semiconductor ETF (NYSE: SMH). It owns 26 of the world’s top semiconductor-related companies such as Intel. The only major stock not in this portfolio is Samsung. This ETF has, of course, done very well for its holders. It has soared over 50% over the past year and is up about 42% year-to-date.

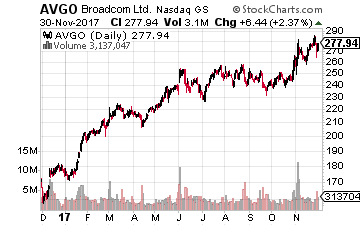

Next up is Broadcom (Nasdaq: AVGO), which is currently attempting to take over rival Qualcomm. Its stock is up 55% year-to-date and about the same amount over the past year.

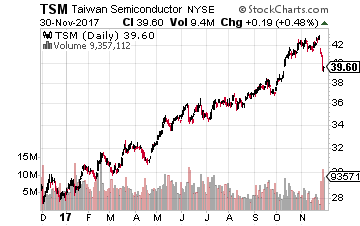

Next up is Broadcom (Nasdaq: AVGO), which is currently attempting to take over rival Qualcomm. Its stock is up 55% year-to-date and about the same amount over the past year. Finally, we come to Taiwan Semiconductor (NYSE: TSM), whose stock is up 37% year-to-date and about 33% over the last 12 months.

Finally, we come to Taiwan Semiconductor (NYSE: TSM), whose stock is up 37% year-to-date and about 33% over the last 12 months.

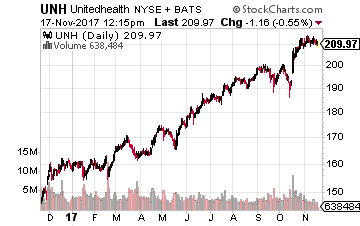

Among the companies in the prescription drug distribution sector, I believe the best of the lot is UnitedHealth Group. About 40% of its revenues come its Optum Rx PBM business, with the remaining 60% of revenues coming from its vast health insurance businesses.

Among the companies in the prescription drug distribution sector, I believe the best of the lot is UnitedHealth Group. About 40% of its revenues come its Optum Rx PBM business, with the remaining 60% of revenues coming from its vast health insurance businesses.

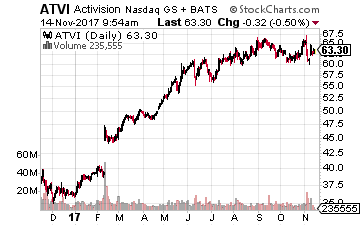

At the top of my buy list is the aforementioned Activision Blizzard, which also has a live streaming channel called Major League Gaming. It acquired the firm in 2016 for $46 million.

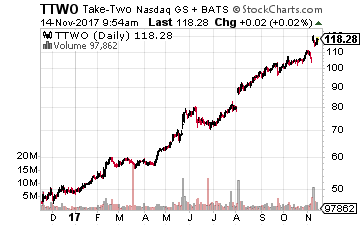

At the top of my buy list is the aforementioned Activision Blizzard, which also has a live streaming channel called Major League Gaming. It acquired the firm in 2016 for $46 million. Next on the list is a rival of Activision, Take Two Interactive Software (Nasdaq: TTWO), which is best known for its Grand Theft Auto franchise. Its stock soared nearly 10% after its recently-released earnings report.

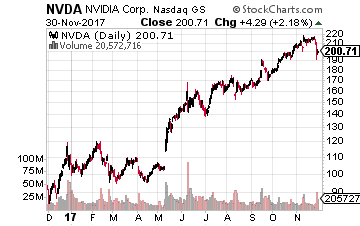

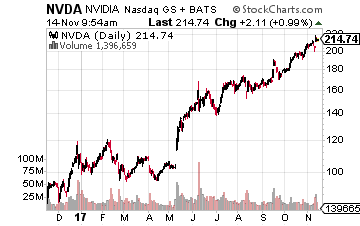

Next on the list is a rival of Activision, Take Two Interactive Software (Nasdaq: TTWO), which is best known for its Grand Theft Auto franchise. Its stock soared nearly 10% after its recently-released earnings report. Finally, an alternative way to play the e-sports trend is through the semiconductor company, Nvidia (Nasdaq: NVDA). Its stock has soared 101% year-to-date and 144% over the past 52 weeks. As I’m sure you may know, Nvidia is a worldwide leader in visual computing technologies and the inventor of the graphic processing unit, or GPU.

Finally, an alternative way to play the e-sports trend is through the semiconductor company, Nvidia (Nasdaq: NVDA). Its stock has soared 101% year-to-date and 144% over the past 52 weeks. As I’m sure you may know, Nvidia is a worldwide leader in visual computing technologies and the inventor of the graphic processing unit, or GPU.

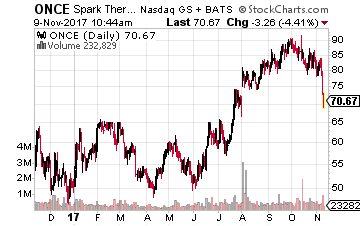

Let’s start with Spark Therapeutics. Most of the company’s $2.8 billion market capitalization is not due to Luxurna. The real excitement for the company comes from several early-stage gene therapy projects that are aimed at hemophilia.

Let’s start with Spark Therapeutics. Most of the company’s $2.8 billion market capitalization is not due to Luxurna. The real excitement for the company comes from several early-stage gene therapy projects that are aimed at hemophilia. Gene Therapy Stock #2 – Bluebird Bio

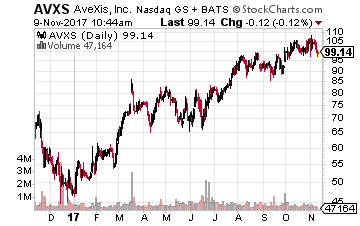

Gene Therapy Stock #2 – Bluebird Bio The third clinical-stage company worth a look is AveXis (Nasdaq: AVXS). The company’s primary focus is on gene therapies to develop a cure for Spinal Muscular Atrophy (SMA), Rett Syndrome and a genetic basis for ALS (Lou Gehrig’s disease).

The third clinical-stage company worth a look is AveXis (Nasdaq: AVXS). The company’s primary focus is on gene therapies to develop a cure for Spinal Muscular Atrophy (SMA), Rett Syndrome and a genetic basis for ALS (Lou Gehrig’s disease).

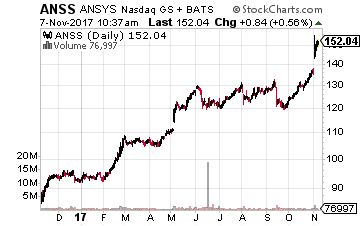

Living in western Pennsylvania, the company at the top of my list is from the area – ANSYS (Nasdaq: ANSS). It is a dominant player in the high-end design simulation software market and is used by most of the well-known manufacturing companies.

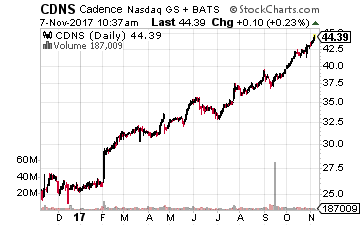

Living in western Pennsylvania, the company at the top of my list is from the area – ANSYS (Nasdaq: ANSS). It is a dominant player in the high-end design simulation software market and is used by most of the well-known manufacturing companies. The second company is Cadence Design Systems (Nasdaq: CDNS). Over 90% of its revenue is recurring, which is outstanding.

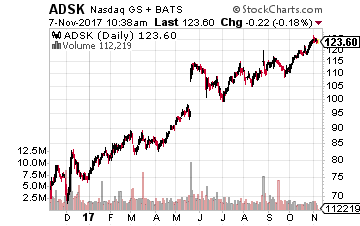

The second company is Cadence Design Systems (Nasdaq: CDNS). Over 90% of its revenue is recurring, which is outstanding. The final company is Autodesk (Nasdaq: ADSK), which generated over $2 billion in revenues in fiscal 2017. It serves customers in architecture, engineering and construction, manufacturing, and digital media and entertainment.

The final company is Autodesk (Nasdaq: ADSK), which generated over $2 billion in revenues in fiscal 2017. It serves customers in architecture, engineering and construction, manufacturing, and digital media and entertainment.