The 2019 rebound has done a lot to revive most people’s portfolios. But there’s a new trap you need to dodge as the market ticks up: the risk you’ll stumble into an overbought stock (or fund).

But don’t take that to mean stocks are pricey—far from it! The S&P 500 is barely up from the start of 2018 and still far from its all-time highs, which is ridiculous when you consider last year’s near-20% earnings growth.

So it’s pretty easy to see that stocks are still ripe for buying.

But there is one sector I am worried about—and it brings me to the first of 3 closed-end funds (CEFs) I want to warn you about today.

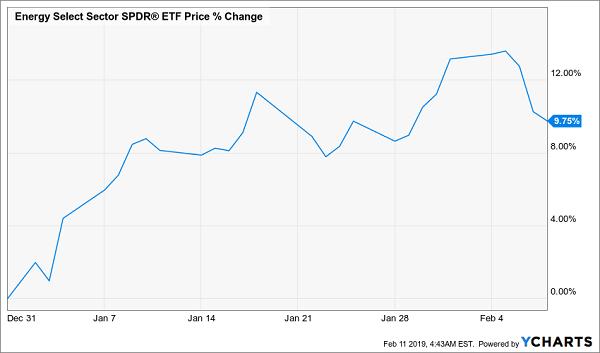

I’m talking about energy stocks, which have been on a tear so far this year, as you can see from the performance of the benchmark Energy Select Sector SPDR ETF (XLE):

Energy Gets Ahead of Itself

Trouble is, that growth isn’t supported by earnings! In fact, profits in the sector have actually fallen nearly 6%, according to FactSet. And the CEF I’m going to tell you about now has actually run up even more than XLE, despite massively underperforming the market.

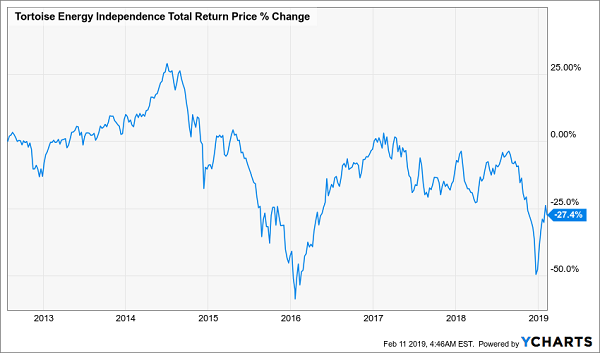

That would be the Tortoise Energy Independence Fund (NDP), which has soared a shocking 37% since the start of 2019. Investors holding this fund probably feel pretty smug about that gain, but they shouldn’t. While NDP’s market price is up big, its NAV (or the value of its underlying portfolio) is up just 7.1%, a fair amount behind XLE’s gain.

Snapshot of an Overbought Fund

The main reason for NDP’s meteoric rise is classic yield chasing: many are enticed by this fund’s astronomical 18.7% yield. But that is a mirage; not only has NDP cut its dividend massively throughout its history, but it is currently under-earning its dividend, which means yet another cut is coming soon.

The fund is also down on a total-return basis (so even when taking dividends into account!) since its inception, no thanks to the 2014 oil crash. But even before that, its returns were less than impressive:

A Perennial Money Loser

For this reason, NDP is my No. 1 must-sell CEF right now.

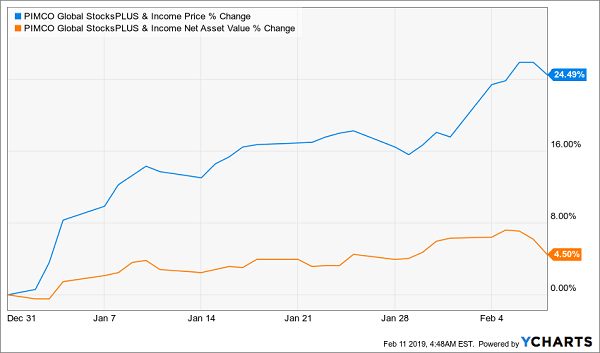

But it’s not the only one to run away from. The PIMCO Global StocksPLUS & Income Fund (PGP) is a complex bond-and-derivatives fund whose market price has also run far ahead of its NAV, and not by a little, either! PGP has soared 24.5% in 2019, while its NAV is only up 4.5%:

PGP Steps Onto the Precipice

As a result, PGP’s premium to NAV is now an absurd 56%, which means it’s positioned for a crash anytime now.

If this sounds familiar, it should. I’ve written about PGP’s huge premium many times before, noting how easy it is to swing trade this fund for 40% annualized gains if you buy it when its premium gets too low and sell when its premium is too high. Right now we’re at a clear sell point, just like the one I spotlighted in August after recommending investors play PGP for a short-term trade in June. Investors who followed that advice bagged a 39% annualized return in less than three months.

Now we’re at a crest in the wave, so if you have PGP in your portfolio, this is the time to ditch it.

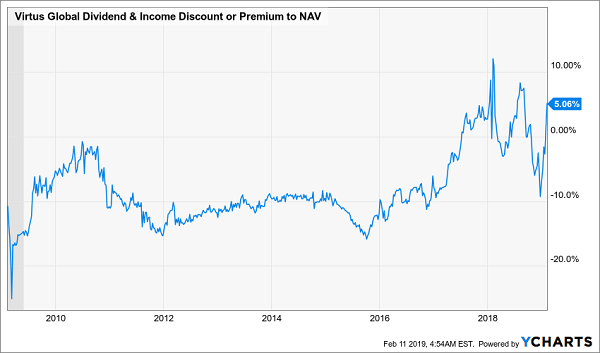

One more fund we need to be wary of: the Virtus Global Dividend & Income Fund (ZTR), which did something unusual just over a year ago: it traded at a premium for the first time ever.

A Suddenly Costly Fund

Although that premium disappeared during the recent market crashes, ZTR investors don’t care. They’re buying at a 5.1% premium for no good reason, since ZTR both underperforms its peers and the Vanguard Total World Stock Fund (VT) over the long haul.

Trailing the Market

Since ZTR’s NAV is up a measly 4.2% in 2019, while its market price is up a shocking 18.6%, it is clearly overbought—which means it’s time to walk away.

Here’s a SAFE 8.5% Cash Dividend for 2019

I don’t know why anyone would play around with looming disasters like ZTR, PGP and NDP when the CEF market continues to throw us bargain after bargain.

In fact, I’ve got 18 of the very best deals in the space waiting for you now! As a group, these 18 retirement lifesavers throw off an incredible 8.5% dividend!

Investors are increasingly hyped up when it comes to earnings season. At least that’s the hope and prayer for the folks over at CNBC that need all the excitement that they can get to lure viewers. And while some corporate chieftains, including JP Morgan’s (NYSE:JPM) Jamie Dimon and Berkshire Hathaway’s (NYSE:BRK.A, NYSE:BRK.B) Warren Buffett are campaigning to end quarterly reporting, earnings season is really just a normal update on how business is going for companies.

And earnings season comes, of course, every quarter — quarter after quarter — year after year. And for the last quarter of 2018, out of the 505 stocks that make up the S&P 500 Index, 358 have released their report cards for the quarter.

And the news is pretty good. Sales overall were up on average by 6.88% and earnings were up on average by 14.20%.

It’s no wonder that the S&P 500 is up by 10% year-to-date and we’re only in February. And that’s after last quarter’s selloff on fears that the earnings were as good as they were going to get and that growth was only going to be just good, and not spectacular.

But there are plenty of companies that aren’t on the list of over-hyped stocks that jump and fall on every little morsel of opinions from talking heads on CNBC, particularly during quarterly reporting times. They tend to be dependable businesses and are focused on longer-term shareholders and not day traders. And they pay nice dividends.

Each of the following dividend stocks I’m going to explore below has already filed its quarterlies with continued good results without fanfare.

Assets Pay

I’ll start with one of my favorite industries — fund management. Fund management is all about assets under management (AUM). The more AUM, the more fee income that a company will earn. The goal is to keep AUM stable to increasing and fee income will follow. You don’t have to be spectacular in managing the assets (although it helps), but you do have to be good at keeping and raising more AUM.

One of the best in this market is AllianceBernstein (NYSE:AB). It has ample AUM, which is up to $550 billion after AB gained $800 million in the last quarter. That is boosting fee income nicely and feeding an ample dividend.

AllianceBernstein (AB) Assets Under Management

Source: Bloomberg

The dividend distribution is currently 64 cents for a yield of 8.29%. And that distribution is rising over the past five years by an average annual gain of 12.62%.

Shares have generated a return of 101.02% over the past five years — amply outperforming the S&P 500 Index. It makes for one of the better dividend stocks to buy under $33.

Powered Up

Utilities make for one of the most reliable stock sectors for both longer-term growth and regular to rising income. They serve that function particularly well during times of market strife due to the reliability of demand for their core products and services.

If you think that they underperform the general stock market, you’d be wrong. Over the past 20 years, U.S. utility stocks, as tracked by the S&P Utilities Total Return Index, have outperformed the general stock market as tracked by the S&P 500 Index.

The market for utilities isn’t about sacrificing return for just dividend income, rather, it can be a potent rival for the returns you expect from more growth-oriented stocks.

What’s more, utilities can be a great defensive counterweight in your portfolio.

For example, during the market rout from October to year-end 2018, the S&P 500 was down, heavily, by 14.28%. But during that same time, utilities managed to outperform with a positive return of 1.66%

This is all thanks to the combination of reliable core business assets and higher dividend payments that utilities represent.

Of course, not all utilities are the same and neither are all dividend stocks. They can include a host of essential services including electricity, natural gas and water. And they are comprised of both regulated and unregulated businesses.

Regulated business means that the companies have contracts set with specific rates for gas, electricity and water that are set by local public utility commissions (PUCs).

This means that the companies with regulated markets must lobby local PUC officials for acceptable rates that take into consideration the cost of providing the services as well as the capital costs of the operations for the services.

In addition, PUCs, along with other regulatory bodies, must approve any expansion of regulated services, including new plants and transmission or other conveyance lines. And they also need to gain approvals for payments for upkeep and repairs. All of this takes a wide array of skillsets by management to make the most for shareholders while keeping customers and their PUCs content. This includes negotiating and lobbying as well as budgeting and market supply-and-demand forecasting.

Yet, at the same time, regulated business means that companies can conduct longer-term budgeting for capital expenditures as well as having better forecasting for revenues and profitability.

This means that utilities can provide smoother performance for shareholders, especially in challenging times. That adds stability for investors over the long term.

Then there is the unregulated part of the utility market. This can include wholesale provision of essential services for industries as well as for other local utility companies that will contract for gas, power or water.

This is where some companies can provide larger-scale services across local markets and even across the country. The companies in this space can provide the opportunity for investors to cash in on their success in markets with less regulatory oversight on rates.

One of the best utilities in the market is NextEra Energy (NYSE:NEE). The company is primarily comprised of two operating units that take advantage of both the regulated and unregulated power utility market.

Based in Florida, NextEra has its primarily regulated power company in Florida Power & Light. The operation provides power through a variety of generating sources, including natural gas, coal and oil, as well as nuclear power plants. Its customers number in the millions and are primarily residential customers, with some commercial customers.

In addition to its own power generation, it also contracts with external power generators that transmit power via the power grid to supplement its own power generation.

The other side of the company is Next Era Energy Resources. This division of NextEra provides unregulated wholesale power around the U.S. with some additional assets in Canada and Spain. Much of its power generation comes from traditional power plants, but increasingly wind and solar generation provide a large portion of its power. It has quickly become one of the largest renewable power generation companies.

In addition, NEE also has some petroleum and natural gas pipeline assets that take advantage of the company’s reach across the U.S. Revenues from the regulated FPL side of the company represent the larger sum of revenues, which continue to expand at a reliable three-year average of 1.58%. This makes for a steady cash flow for the company.

The company continues to focus more on the NEER division, which provides the namesake for the overall company. The idea is that the next era in power generation will be ever more focused on renewable energy sources. This is supported in that the revenues for the NEER unit have expanded to become 28.55% of overall revenue of the company.

The industry is benefiting from state and local legislation around the nation requiring that a portion of power be generated by renewable sources. In addition, NextEra’s renewable power expansion is also benefitting from Federal tax credits for renewable energy facilities. These come based on capacity and not just the amount of power generated. This means that the company can operate wind and solar facilities around the nation and not just in areas that are particularly sunny or windy.

NextEra Energy (NEE) Total Return

Source: Bloomberg

The company is a stronger performer for investors. The return on its capital is running at 9.90%, while the return on investor’s equity is a whopping 21.30%. And this is resulting in the market recognizing its performance now and for the future. The shares have delivered a total return over the past five years of 127.76%.

Yielding 2.42%, it makes for a good buy under $185.

Pumping Profits

Petroleum has been one of the better markets for companies last quarter with sales gains for companies reporting of 12.14% (so far within the S&P 500) and earnings growth of 102.19%.

One of the more reliable segments of the petroleum market is in the midstream segment of the toll-takers of the pipeline market. And one of my favorites dividend stocks in this space is Plains GP Holdings (NYSE:PAGP), which has a great network of pipes and related assets throughout North America including the vital Permian Basin in the U.S.

Revenue continues to flow with gains over the trailing year of 29.90%. And the shares are valued at a huge bargain as they are trading currently at a 90% discount to the trailing sales of the company.

As a passthrough, the distributions are shielded from current income tax liabilities making the dividends all the more valuable on a tax-equivalent basis. With the current distribution of 30 cents per year, it yields 5.03%.

Plains GP Holdings (PAGP) Total Return

Source: Bloomberg

And the overall shares have been dependable for income and for an overall total return over the trailing twelve months of 12.29%. It makes for a good dividend paying toll-taker under $26.65.

All My Best,

Neil George

Neil George is the editor of Profitable Investing and does not have any holdings in the securities mentioned above.

Just a few months ago, bond “experts” were all over the financial news networks predicting the yield curve would soon invert. An inverted curve, where short-term rates are higher than long-term rates, is a reliable indicator that the economy will go to negative growth – a recession. At that time the stock market was setting new records higher, even as the fears of a recession grew. Currently the rate curve is very flat, meaning short-term rates and long-term bond rates are not very different.

The interest rate news in late 2018 helped push the stock market into a steep decline. So, what is it to be? An economic recession with higher stock prices or a strong economy with lower stock prices? Or market and economic activity no one predicted? Will the yield curve flatten or steepen? What will they say next week?

The point is that an investor who invests based on the latest “expert” opinions is likely to get whipsawed into losing money in the stock market. In December, the stock market went into a deep correction. Many financial pundits took this as a prediction of an economic recession and continued stock price decline into a bear market. Stocks did just the opposite and so far, have gone up every week in 2019.

If you are an investor, and not a trader, and want to grow your portfolio value, you need an investment strategy that accounts for market corrections. Over the course of 2018, there were lots of predictions that a correction was coming. Now we have experienced the mental stress that comes with a steep market drop.

My plan, which I regularly share with my Dividend Hunter readers, is to focus on owning higher yield dividend stocks with potential for dividend growth. A dividend focused investment strategy provides three advantages when the stock market corrects.

Quality companies will continue to pay dividends. You will earn dividend income right through the correction and recovery.

Dividends are additional cash to put to work when share prices are down. Investors say they are waiting for a correction to invest. Reinvesting your dividends allows you to do that.

Buying income stock shares when prices are down boost your portfolio yield, which you will continue to earn for as long as you own the shares.

Now that the major market indexes have lost almost 20%, there are lots of dividend stocks at very attractive valuations. However, my editor likes for me to highlight some attractive stocks with each article. Here are three that have monthly dividends and will pay well through a correction and provide you with nice gains when the market recovers.

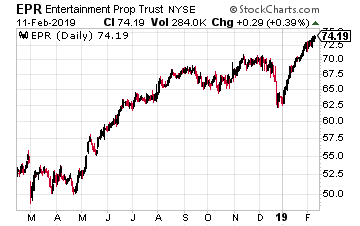

EPR Properties (NYSE: EPR) is a very well-run net lease REIT that has done a great job of growing the business and generating above average dividend growth for investors.

With the triple net-lease (NNN) model, the tenants that lease the properties owned by EPR are responsible for all the operating costs like taxes, utilities and maintenance. EPR’s job is to collect the rent checks.

Typically, NNN leases are long term, for 10 years or more, with built-in rent escalations. EPR Properties separates itself from the rest of the triple net REIT pack by the highly focused types of properties the company owns. The EPR assets can be divided into the three categories of Entertainment –movie megaplex theaters, Recreation – golf and ski facilities, and Education – including private and charter schools, and early childhood centers. EPR just increased its dividend for the ninth consecutive year, boosting the payout by 4%.

The shares yield 6.1%.

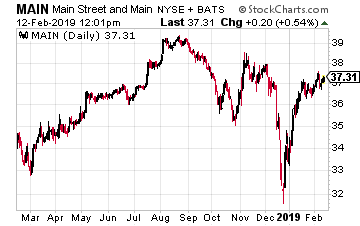

Main Street Capital Corporation (NYSE: MAIN) is a business development company has been a tremendous stock for income focused investors.

A BDC is a closed-end investment company, like closed-end mutual funds (CEF). The difference is that a CEF owns stock shares and bonds, while a BDC makes direct investments into its client companies. A BDC will have hundreds of outstanding investments to spread the risk across many small companies. MAIN uses a two-tier approach to its portfolio. This unique strategy allows Main Street to generate a high level of interest income and capital gains from equity investments.

This company is one of just a small number of BDCs that has grown its dividends and net asset value per share. The monthly dividend has been increased five times in the last three years. MAIN has also been paying semi-annual special dividends that boost the realized yield above the current yield.

The stock currently yields 6.3%.

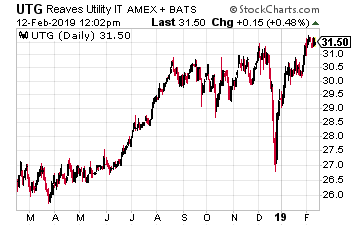

The Reaves Utility Income Fund (NYSE: UTG) is a closed end fund manage by Reaves Asset Management, an investment manager firm that solely focuses on the utility, telecom and infrastructure sectors.

I recommend UTG over individual utility stocks because it pays monthly dividends and has a higher yield than the typical utility stock. The UTG dividend has never been reduced. It has increased steadily and is now 75% higher than at the time of the fund’s IPO in 2004. No portion of the dividends paid have every been classified as return-of-capital.

Utilities are viewed as a safe haven stock sector, and UTG is a great way to invest in that sector.

Whether you watched the State of the Union address by President Trump last week or not, you, like me, probably have no illusions that the two parties will accomplish much together in the foreseeable future. One area where they reportedly have common ground is infrastructure repair and maintenance. The numbers certainly argue for a new spending bill, but the need for common sense spending, and what Washington actually does with our tax dollars, don’t necessarily line up these days.

The American Society of Civil Engineers (ASCE) compiles an extensive report on the state of the infrastructure in the U.S., looking at roads, bridges, waterways, schools, airports, and a variety of other key infrastructure indicators. The news is not good, and hasn’t been for years. The total amount of infrastructure is massive, and much of it has not gotten needed attention for repair and maintenance. ASCE issues a “report card” every four years for the overall infrastructure, and as of 2017 the grade was a D+. It was the same in 2013.

The report details crumbling roads and bridges, inadequate school facilities, and airports and air traffic control systems that have failed to keep pace with an increasing number of aircraft and air travellers across the U.S. Dams are ever closer to failing, and our ports, which handle approximately 26% of all goods flowing through the U.S. economy, need deeper channels to handle larger ships, and new equipment landside to load and offload these new larger vessels.

So, if I look at infrastructure companies, ones that provide the material and logistics to build new roads, bridges and airports, I might expect to find a graveyard of broken stocks. But that’s simply not the case. Why?

Three factors are driving infrastructure spend, which, according to the companies selling the cement and asphalt, is getting increasingly stronger. First, we actually do have an infrastructure bill in place in the U.S already. The Fixing America’s Surface Transportation (FAST) Act was signed into law by President Obama in December 2015, and provides for over $305 billion of dedicated funding for U.S. infrastructure. The five year budget, running through 2020, is still being spent and driving business for infrastructure companies.

Second, a strong economy the last few years, as measured by unemployment numbers and jobs created, has meant more money for state coffers. State Departments of Transportation across the U.S. are starting to pick up the slack from federal funding and fix their infrastructure themselves. It appears this funding is in the early stages, with many states recently engaging in large long term projects.

And third, the companies I look at below, are working in states where the population is growing. This means more building as residents move in, more tax revenue, and then more infrastructure building. According to the latest U.S. census numbers the highest growth states include the Carolinas at 9 and 10, Texas at 8, Colorado at 7, and Florida at 5. Not surprisingly, these states represent the backyard of the infrastructure companies doing well. Let’s not hold you in suspense any longer, and get to the companies.

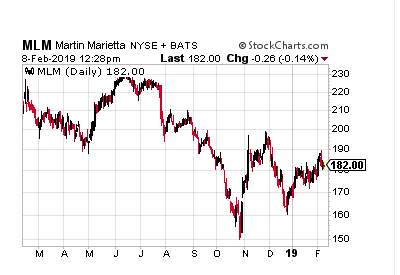

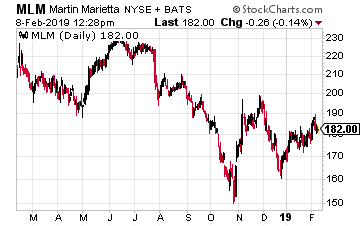

Martin Marietta Materials (NYSE: MLM)

Maybe my mention of Martin Marietta stirs your memory of the aerospace and electronics company it once was. When Martin Marietta merged with Lockheed in 1995, the companies formed Lockheed Martin (NYSE: LMT). But the new aerospace and defense company had no need for a provider of cement and concrete, and spun off Martin Marietta Materials the following year.

Today, Martin Marietta provides aggregates and heavy building materials. They sell the material necessary to build roads, sidewalks and the foundations of homes and commercial buildings. And they’re doing a good job of it. The company has taken advantage of a strong economy in the U.S. and grown earnings an average of 31% the past 5 years.

Operating in growing states such as Texas, North Carolina, Georgia and Florida, Martin Marietta is seeing an acceleration in public contracts let by the Departments of Transportation in these states. The company has made a focus on demographic trends a mainstay of their business strategy, and they are following the time tested tactic of going where the money is.

As CEO C. Howard Nye, who has been CEO since 2010 recently stated, “In fact, many of our most attractive areas, while growing, are still well below mid-cycle shipment levels. Further, it remains difficult to see an end to this recovery when the long-awaited arrival of increased infrastructure activity has only recently begun in earnest.” It doesn’t get much rosier than that.

Not only is the company seeing an uptick in business, they are raising prices at the same time. This is one of the reasons to get in the stock now. As Mr. Nye puts it, “Our optimism is further bolstered by favorable pricing trends, typically an indicator of underlying market strength.” Martin Marietta is projected to grow earnings per share next year 16.5%.

Finally, the company should benefit from unfavorable weather which adversely impacted the Carolinas last year in the form of Hurricane Florence. Causing an estimated $18 billion in damage to the Carolinas, the region will have to go through a long period of rebuilding damaged infrastructure. This rebuilding process generally takes several years, and results in an increased demand for the products Martin Marietta provides.

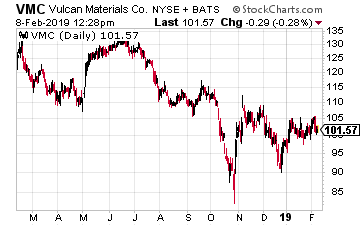

Vulcan Materials (NYSE: VMC)

A second supplier of building materials which should benefit from the same tailwinds as MLM, is Vulcan Materials. Echoing comments from Martin Marietta, Vulcan Materials CEO, J. Thomas Hill noted about their third quarter, which was marred by the inclement weather mentioned above, “Highway construction demand is strengthening across the country, but much more so in our markets. We’re now seeing the conversion of public funding in the shipments, and this showed up in 10% growth in our quarterly aggregates shipments and a 6% increase on a same-store basis.”

Supporting my thesis here, Mr. Hill added, “Prices continue to escalate. With improved flow-throughs, all of which is supported by growing demand.” And Vulcan isn’t content with just growing organically, they’re making acquisitions, something I like in an expanding market.

In 2018 the company bought Aggregates USA, a materials provider with operations in Georgia, South Carolina, and Florida. As Mr. Hill points out, the acquisition “adds to our product offering, expands our distribution network and service areas, and will help us better serve our customers.” Any merger kinks should be worked out by now, one year later.

Vulcan has grown earnings per share almost 49% per year on average the past 5 years, and is projected to grow earnings at a 24% clip next year. The company currently trades at a PE of 32, but that should drop to around 21 if earnings come in as projected.

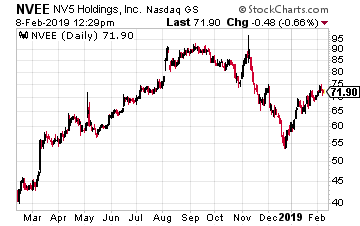

NV5 Holdings (Nasdaq: NVEE)

If you’re looking for a smaller company, that has exposure to U.S. infrastructure, but has exposure to growth from infrastructure projects globally, look no further than NV5 Holdings. The company provides a wide array of technical services related to building projects, including providing water and electricity to buildings, and providing logistics services for waste water management.

NV5 is an innovative company looking for new ways to provide value to its customers at lower cost. You know I like companies that not only develop technology, but apply new technology and develop business models using emerging tech. A great example of this is the drone survey business, a quickly growing sector for construction, as well as safety and inspections.

COO Alexander Hockman, describes the new way in which NV5 is using drones to attack business problems. “Our drone survey service is providing a differentiating technology and was used to collect survey data on over 300 acres of the Brooklyn Navy Yard. Using conventional techniques, the task would have taken several weeks but was completed in approximately four hours using our drone-based photogrammetry technology.”

NV5, like Vulcan, is also acquiring companies and adding additional services to its lineup. The company recently acquired CHI Engineering, which gives it access to a client base of over 80% of the 140 Liquified Natural Gas (LNG) facilities in the U.S.

NV5 has extensive business globally, and importantly operates over a range of sectors within the building industry. The company is currently working on projects in Abu Dhabi, Cypress, Macau, Hong Kong, China and Taiwan. And, customers range from municipalities, to transportation hubs, to multinational hospitality companies.

NV5 has grown earnings an average of 34% over the past 5 years, and is projected to grow earnings over 80% this year. The company has a very small amount of debt, and trades at a PE of just over 26.

New infrastructure bill in the U.S. or not, federal funds are flowing and states are ponying up to fix their crumbling infrastructure. And, even with growth slowing internationally, new building projects are still being captured by innovative companies. Take a look at Martin Marietta, Vulcan Materials, or NV5, they may be just the foundation your portfolio needs.

I’ve just returned from the Orlando MoneyShow and was very impressed at the amount of investors and traders looking to learn more about options strategies. I had the opportunity to deliver two different presentations to the options-oriented folks. One of the topics I spent quite a lot of time on was covered calls.

Of course, I’m a big fan of using covered calls whenever possible. But, it was nice to see that many in attendance also have tried the strategy or are interested in learnings more. I believe the more people know about the benefits of covered calls, the more popular the strategy becomes.

For instance, covered calls can often provide more steady returns from your portfolio. This consistency occurs because you are regularly receiving income from the calls you sell against the long shares you own. What’s more, the call premium can be used to offset some downside risk.

The combination of a regular income stream plus a built in hedge certainly has the effect of smoothing out the returns over time. Nobody likes inconsistent and choppy returns. It’s one of the reasons covered calls (aka buywrites) are so popular among institutions. The great things is, we can make the exact same buywrite trades as the institutions.

And don’t forget, using a covered call strategy does not preclude you from receiving a dividend. Since you are long the stock, you still get the dividend if you’re holding the shares when ex-divided comes around. Selling a call against long stock for income doesn’t impact the dividend at all – it just amplifies the yield.

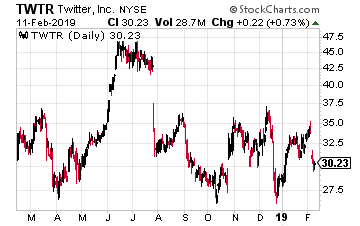

Let’s take a look at a very interesting covered call I just came across in Twitter(NYSE: TWTR). TWTR is an immensely popular microblogging site which just sold off fairly sharply after earnings. The stock dropped from around $35 to $30, as you can see in the chart.

Now, TWTR isn’t a dividend paying stock, but it’s a great example of another way you can use covered calls – to earn income while you wait for stock appreciation. In this case, the covered call buyer is probably hoping for a short-term rebound in the shares.

The actual trade was buying 2,288,000 shares of TWTR versus selling the March 15th 34 call. Remember, one call needs to be sold for every 100 shares, so the call was sold 22,880 times for $0.41 per option. This was done with the stock price at $30.29.

With the covered call in place, the trader can make money all the way up to $34 in the stock price before the gains are capped due to the short call. Meanwhile, $938,000 in premium is collected regardless of what the stock does. That means the shares are protected down to $29.88 before any money is lost.

The premium collected represents a 1.4% yield for just over a month holding period. However, if the stock moves up to $34, the trader can earn another $3.71 on the trade, or an additional 12%. In dollar terms, that’s about $8.5 million of additional upside.

If you think this is a good entry point for TWTR, I believe this is a great trade to make. You are getting paid to wait for a rebound and not significantly reducing the amount of upside you can attain if the stock rallies. Plus, this trade would be very easy to roll out if the stock doesn’t rebound by March 15th.

Trying to “beat the market” is a tough game on a day-to-day basis. Financial markets are volatile. They’ll swing higher one day and then fall the next day. Sometimes, we don’t even know why they move the way they do. They just move. And, because it’s nearly impossible to explain every day-to-day move on Wall Street, it’s equally impossible for even the sharpest minds to predict day-to-day moves in stocks with great accuracy.

Thus, trying to “beat the market” on a day-to-day basis is an uphill battle. But, if you zoom out and take a long-term approach to investing, you turn that uphill battle into an even playing field. Longer-term trends in stocks are often easier to predict because they almost always track fundamentals and narratives, and fundamentals and narratives are tangible enough that investors can — with practice and discipline — predict them with great accuracy.

As such, successful investors often tend to take the Warren Buffet approach and buy stocks of companies that have healthy long-term growth prospects, under the idea that healthy long-term growth will translate into a substantially higher stock price over time.

I have a special name for the cream-of-the-crop stocks in the long-term winners basket: forever stocks. Forever stocks are the classification of stocks that are not just long-term winners, but are also aligned with powerful and long-running secular growth trends, and have proven leadership within that trend. Thus, forever stocks project with high certainty to be long-term winners for a lot longer. Theoretically, they project to be winners “forever”.

These forever stocks are the best stocks to buy and hold for long-term investors. They will be highly volatile in the near term. But, such volatility will amount to nothing more than noise in the big picture. In that big picture, forever stocks will only head higher.

With that mind, let’s take a look at seven forever stocks to consider for the long haul.

Source: Shutterstock

Facebook (FB)

Secular Trend: Persistent internet addiction

Big Idea: The big idea behind the forever bull thesis in Facebook (NASDAQ:FB) starts with the fact that consumers are addicted to the internet. There have been multiple calls for this addiction to break over the past several years. It hasn’t. Instead, internet usage has gone up because the internet provides the easiest, most convenient and cheapest way to perform a great number of tasks.

Consumers spend most of their internet time on the digital properties that Facebook owns. That means that an addiction to the internet and an addiction to Facebook’s digital properties run parallel to one another. This will remain true for the foreseeable future. As such, the number of users on Facebook’s properties and the volume of ad dollars flowing through those properties will only go up over time. As they do, Facebook’s revenues and profits will steadily rise, and so will FB stock.

Secular Trend: Democratization of e-commerce in the coordinated economy

Big Idea: The big idea behind the forever bull thesis in Shopify (NYSE:SHOP) starts with the fact that the world is becoming increasingly democratized and decentralized. This concept is very simple. Companies far and wide are leveraging technology, which allows for unprecedented connectivity, to democratize supply and distribution processes globally. Think Uber, which democratized driving services so that anyone with a car could do it, or Airbnb, which democratized accommodation services so that anyone with an extra room could do it. I like to call this movement the coordinated economy since beyond democratizing services, these companies are also coordinating these services to create optimal outcomes on both the supply and demand side of the equation.

Shopify is doing this exact same thing in the commerce world. The company is democratizing selling services so that anyone with a product can sell it. They are also coordinating such services by creating a connected web of independent buyers and sellers. In so doing, Shopify is creating the building blocks for a new era of democratized commerce where we don’t buy everything from Amazon (NASDAQ:AMZN). As this democratization process plays out over the next several years (and it most certainly will, given that Amazon can’t control 50% of the U.S. e-commerce market forever), Shopify’s merchant volume, revenues and profits will rise by leaps and bounds. As they do, SHOP stock will rise, too.

Secular Trend: Growing demand for cloud communication services

Big Idea: The big idea behind the forever bull thesis in Twilio (NASDAQ:TWLO) is that the world is becomingly increasingly connected, and as it does, the desire for cloud-based communication services will go from “want” to “need”. This market that involves these services is broadly defined as the Communication Platforms-as-a-Service (CPaaS) market, and it consists of companies integrating real-time communication services into their operations. Perhaps the most tangible example of this is when Uber or Lyft sends you messages to communicate that your ride has arrived.

Nuanced communication services like this will be increasingly integrated at greater scale over the next several years across various industries because, no matter the industry, one theme is constant: consumers and companies alike are becoming more connected than ever. Twilio has emerged as the unchallenged leader in this space. The customer base is growing by over 30%. Revenues are growing by nearly 70%. The retention rate is 95% and up. In other words, everything is going right for this company, and it will continue to go right as the CPaaS market goes from niche to mainstream over the next several years.

Big Idea: The big idea behind the forever bull thesis in The Trade Desk (NASDAQ:TTD) starts with the fact that technology is rapidly automating multiple jobs and processes across the enterprise ecosystem. This includes the process of buying and selling ads. Before, the ad transaction process was laborious, lengthy and included several human parties. Today, though, enterprises can now buy ads instantaneously and without friction or the high costs using computers.

This new method of using AI and machines to buy and sell ads is called programmatic advertising. It’s the future of advertising. Eventually, given the low-friction and low-cost advantages of programmatic advertising, all $1 trillion worth of ad spend globally will be transacted programmatically. At the forefront of this market is Trade Desk, a company which has distinguished itself as the programmatic advertising leader. As such, as the programmatic advertising method goes global over the next several years, Trade Desk will remain a huge grower and TTD stock will head higher.

Source: Shutterstock

Amazon (AMZN)

Secular Trend: Nearly everything

Big Idea: The big idea behind the forever bull thesis in Amazon is that this company is at the forefront of nearly every one of tomorrow’s most important markets. E-commerce? Amazon already dominates there. Cloud? Amazon already dominates there, too. Offline retail? Amazon is rapidly expanding its presence. Automation? Amazon is already automating its warehouses, and just made a big investment into self-driving car company Aurora. AI? Amazon dominates the voice assistant market. Pharma? Amazon has all the licenses it needs to launch a nation-wide e-pharmacy business. Digital advertising? Amazon’s digital ad business is the fastest growing among major players in the space. Streaming? Amazon is No. 2 in this market behind Netflix(NASDAQ:NFLX)

In other words, Amazon has its fingertips everywhere it matters. Inevitably, one or many of these growth initiatives will turn into a multi-billion dollar business (if they aren’t already). A few big breakthroughs in automation, pharma or AI will help offset slowing growth in e-commerce and keep Amazon a big growth business for a lot longer. That will push AMZN stock way higher in the long run.

Source: Shutterstock

Forever Stocks to Buy: Adobe (ADBE)

Secular Trend: Shift towards a visual and experience economy

Big Idea: The big idea behind the forever bull thesis in Adobe (NASDAQ:ADBE) starts with the idea that the world is becoming increasingly visual-centric. You can thank Instagram, Snapchat and YouTube for bringing this out recently, but the desire has always been there. The saying “a picture paints a thousand words” has been around for a long time. Now, that saying is turning into action as consumers globally are becoming increasingly obsessed with visual everything.

When it comes to visual everything, there’s one company in the world that stands out above the rest in terms of creating visual everything content: Adobe. Adobe has developed a reputation as being a second-to-none provider of visual everything solutions for creative professionals. Now, the company is leveraging that experience to create visual everything cloud solutions. These cloud solutions will be met with increasing demand as enterprises increasingly seek visual everything solutions to connect with consumers. As such, Adobe will benefit from a continued visual cloud demand surge over the next several years, and that will help keep ADBE stock on a winning trajectory.

Big Idea: The big idea behind the forever bull thesis in Square (NYSE:SQ) starts with the fact that cash is history. A few years ago, your average consumer almost always carried a wallet or purse that had at least some cash. Today, that’s no longer true. A majority of young, 30-and-under consumers I come across don’t carry cash. Instead, they have their phone and their payment card(s), and intend to pay for things exclusively through one of those items.

Retail shops have had to adjust to this cashless revolution, and Square has helped them. Square provides machines that facilitate cashless transactions. First, they simply helped facilitate brick-and-mortar cashless transactions. Now, they are helping facilitate e-commerce transactions, too. In other words, everywhere the consumer is, Square is there, too, helping them facilitate a cashless transaction. This is an extremely valuable position to be in for the foreseeable future, as cash truly becomes a relic in the modern economy. As it does, Square’s payment volume will surge higher, and SQ stock will stay on an uptrend.

As of this writing, Luke Lango was long FB, SHOP, TWLO, TTD, AMZN, NFLX, ADBE and SQ.

If you’re like most people, you’re wondering one thing right now: can stocks keep soaring following December’s nosedive—even after spiking 8% in January?

The answer? Absolutely.

To get at why I’m so sure, we’ll first go a couple steps further than headline-driven “first-level” investors do. Then I’ll give you a way you could double (or more) your rebound gains thanks to a terrific closed-end fund (CEF) yielding 7.2%—and “spring loaded” for 35% returns this year.

The Ignored Connection Between Jobs and Stocks

To get at what’s in store for the markets in 2019, we have to go back to 2009 and zero in on one thing: jobs. Because the crisis back then triggered a lost decade that only ended in 2017, when the unemployment rate finally got back to pre-crisis levels.

Then something strange happened—unemployment kept falling. In January, payroll data rose to one of the highest levels ever, blowing away even the rosiest estimates.

In such a job market, inflation seems like a sure thing. After all, when everyone who wants a job can get one and more jobs are created every day, employers will need to pay higher wages to keep the workers they have. And consumers will open their wallets, confident they’ll be earning more. But we’re not seeing that:

Inflation Defies Expectations

This has stumped many economists, because it’s normally a given that lower unemployment stokes inflation. But there’s a simple explanation for what’s happening today, and it comes back to folks who are unwillingly out of the workforce.

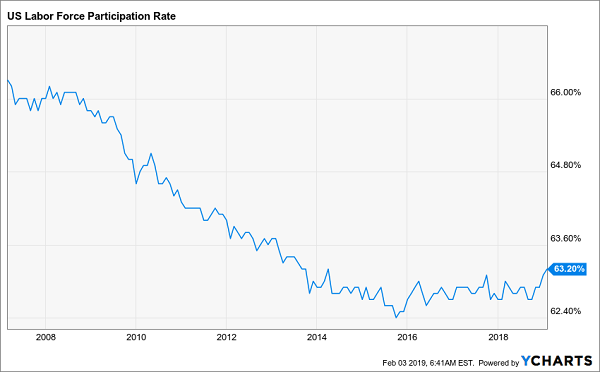

Here’s what I mean: the government measures unemployment by looking at what percentage of people are in the labor force, then looking at what percentage of those people don’t have jobs. But people can choose to be in or out of the labor force at any given time—and plenty of people have made an exit in the last decade:

US Workforce Shrinks—Till Now

For much of the 2010s, the unemployment rate wasn’t falling because more people were getting jobs—it was falling because more people gave up on getting jobs. But workforce numbers flat-lined since 2015 and began rising in late 2018. In short, Americans who’d thrown up their hands are getting back in the game.

That means inflation could be a risk in the future, when all those who left the labor force have come back, but we’re a long way from that.

In sheer numbers, think of it this way: 66% of 306 million people were in the labor force in 2007. That’s 202 million men and women. We’re now down to 63.2% of 327.16 million, or 206.8 million people. Another way to think about it: in the last 12 years, our labor force is up just 1.6% while our population is up 6.9%.

This is unsustainable: America needs more workers to keep up with its bigger population.

“A Rare Time When You Can Buy Stocks at a Discount”

This all means the market recovery will likely continue, because there’s too much demand for workers—and workers have too much money to spend—to cause a market hiccup. Better still, we’re at a rare time when you can buy stocks at a discount—and an even bigger discount is on the table for us, thanks to closed-end funds (CEFs).

Let me explain.

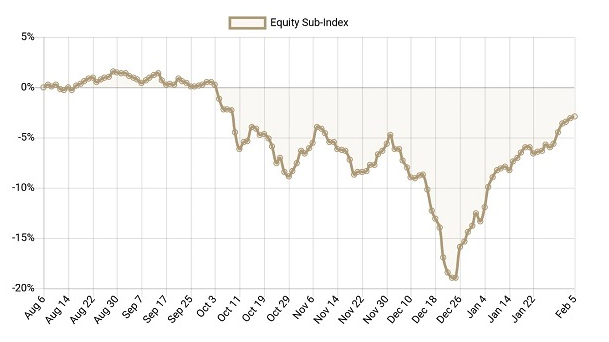

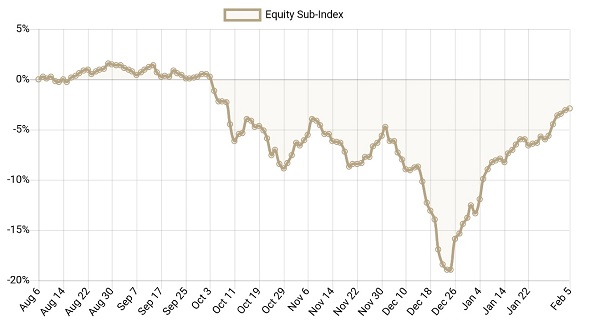

CEFs slipped in 2018, only to start recovering in early 2019:

CEFs Tumble … Then Bounce Back

But as you can see, CEFs still haven’t fully recovered—and there’s still a big gap between their 2018 peak and where they are now, even though CEFs’ year-to-date recovery has beaten the S&P 500’s 9.1% bounce, with the CEF InsiderEquity Sub-Index up 11.1% in 2019.

That tells me that this could be another year where CEFs outperform, as they did in 2017. And they’re likely to do so for the same reason: they were oversold in the prior year.

The One Fund to Buy for 35% Gains (and 7.2% Dividends) in 2019

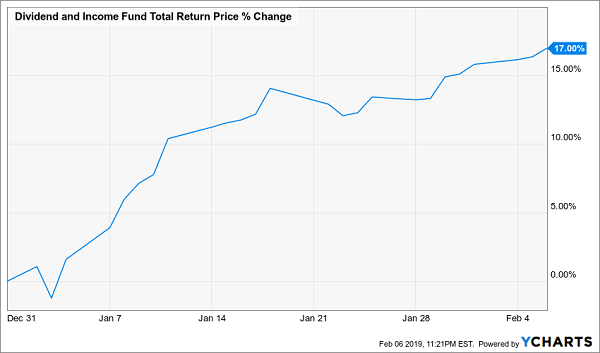

Which brings me to the Dividend and Income Fund (DNI), which focuses on bargain-priced US stocks like Apple (AAPL), Intel (INTC) and the Walt Disney Company (DIS). DNI is now signaling that it’s in the early stages of a huge recovery. Look at its outsized return in 2019 so far:

The Rally Is On!

But DNI still falls short of where it was in early 2018, so it has plenty of runway ahead:

DNI’s Ride Is Just Beginning

How high can DNI go? If we track its 2017 performance from when it got absurdly oversold at the end of 2016 (as it was absurdly oversold at the end of 2018), we see that a 35% return was in the cards:

History Looks Set to Repeat

And since DNI’s decline in ’16 wasn’t as severe as in ’18, there’s a good chance this year’s return will be even bigger than 35%.

One reason why I’m confident is that the fund’s unusually large 23% discount to net asset value (NAV, or the market price of its underlying portfolio) means that, just to sustain that discount, for every 1% its NAV gains, DNI’s price will have to go up 1.3%. If the market wants to make that discount disappear (as it did in 2017), its price will obviously have to go up much more than 1.3% for every 1% of NAV gains.

The kicker? DNI yields an outsized 7.2% now, so you’re getting around 20% of your potential 35% return in cash here.

Better still, DNI is far from your only choice: there are many other CEFs yielding as much or more than this fund and also look set to clobber the S&P 500. And these income wonders invest in similar top-notch (and cheap) US companies.

Cloud stocks are back. During the late 2018 market selloff, cloud stocks were thrown out — along with every other growth stock in the market. But as financial markets have improved in early 2019 due to stabilizing economic fundamentals, cloud stocks have come roaring back.

The First Trust Cloud Computing ETF (NASDAQ:SKYY) dropped more than 20% in late 2018. Since bottoming on Christmas Eve, the SKYY ETF has soared nearly 20%, and is now just 5% off of all-time highs.

The big rebound in cloud stocks can be chalked up to improving fundamentals and sentiment. As it turns out, the global economy isn’t spiraling downward at a rapid rate. Instead, it is simply slowing at a reasonable rate to a more steady 2-3% growth rate. Amid this slowdown, cloud services demand has remained robust, since cloud services are seen both as the future and a way to cut costs amid slowing growth.

Consequently, the fundamentals and sentiment underlying cloud stocks have dramatically improved over the past month. As they have, cloud stocks have soared higher.

This rally is far from over. Considering only 20% of enterprise workloads have shifted to the cloud, it’s fair to say that the rally in cloud stocks is still in its early stages. With that in mind, let’s take a look a 7 cloud stocks to buy now.

Source: Shutterstock

Adobe (ADBE)

Perhaps the best-in-class cloud stock to buy now for healthy upside and limited risk is Adobe(NASDAQ:ADBE).

The core growth narrative here is quite promising. Adobe is one part stable-growth business with a huge moat, and one part hyper-growth business with a rapidly expanding addressable market. Those two parts put together are worth far more than what the market is saying today.

On the stable growth side, Adobe is a one-stop shop digital solution for creative professionals with relatively muted competition. This has always been the case. If you can’t think of any true competitors to Adobe in the creative solutions space, you aren’t alone. Just check out this list or this list of Adobe Photoshop alternatives. None of them are household names. Nor do any of them offer products even close in quality to Adobe’s offerings. As such, this creative solutions business is a stable growth business with a huge moat and no competition, implying healthy revenue and profit growth for the foreseeable future.

On the hyper growth side, Adobe is morphing into a cloud business with a unique value prop. Other cloud solutions focus on various factors. Adobe’s cloud solutions focuses on experiences and visuals, and the company is leveraging its experience in visual-oriented solutions to create cloud solutions for companies looking to enhance their consumer’s experience. As it does, Adobe’s revenue and profits will move considerably higher.

Overall, there’s a lot to like about ADBE stock. This is a big growth company that will keep growing at a big rate for a lot longer. That level of robust growth will power ADBE stock significantly higher in a long term window.

Another best-in-class cloud stock is cloud communications app maker Twilio (NYSE:TWLO)

Over the past several quarters, Twilio has emerged as the unchallenged leader in the rapidly growing Communication Platforms-as-a-Service (CPaaS) market. The CPaaS market essentially consists of companies integrating real-time communication into their services. Think of Uber or Lyft using messages to communicate with riders when their rides are approaching.

This market will be huge due to continuous shifts towards cloud-based communication, personalized customer experience and digital engagement. Quite simply, as consumers, we enjoy digital, real-time, and personalized communication about the services and products we are paying for. Twilio enables this communication. That positions this company for huge growth as the CPaaS market expands over the next several years. For what it’s worth, research firm IDC expects this market to grow five fold over the next five years.

Thanks to its huge customer and revenue growth and 95%-plus retention rate, Twilio has emerged as the clear leader in this space. As this space matures over the next several years, companies will increasingly turn towards Twilio to enable CPaaS solutions thanks to the company’s leadership position (in new industries, you always tend to trust the leader).

As such, over the next several years, Twilio will continue to grow at a rather robust rate. This big growth will ultimately power TWLO stock higher, especially against a favorable equity backdrop.

ServiceNow (NOW)

In the digitization and automation fields, the cloud stock to buy is ServiceNow (NYSE:NOW).

ServiceNow is currently in the business of digitizing corporate operations. This includes automating corporate workflows and IT tasks. But, this is just the tip of the iceberg for ServiceNow. Automation is a big, big market. Automating IT tasks represents just a fraction of what the automation market will look like at scale.

At scale, jobs across the entire corporate ecosystem will be replaced by more efficient digitized and automated solutions. ServiceNow will provide the lion’s share of these solutions. As such, as the automation revolution plays out over the next several years, ServiceNow’s revenues and profits will explode higher. As they do, NOW stock will explode higher, too, considering the valuation today remains reasonable.

Overall, NOW stock is a great way to play the automation revolution. This revolution is still in the first inning, and the next eight innings promise to have broad and immense financial implications. For ServiceNow, those implications are hugely positive. As such, NOW stock should trend consistently higher over the next several years.

Okta (OKTA)

One of the more exciting cloud stocks to consider here is Okta (NASDAQ:OKTA).

Okta is pioneering what the company calls the identity cloud. Essentially, this is a cloud solution centered on individual identity that allows millions of people across a corporate ecosystem to seamlessly, securely, and uniformly connect to the technological tools that the corporation is adopting. This may sound like a complex idea. The underlying technology is complex. But, the idea isn’t. The idea is that companies everywhere are rapidly adopting new technologies, and that the implementation of these technologies is often difficult, chunky, and risky to identities and data. Okta solves this problem, and allows companies to adopt new technologies seamlessly and within the same secure cloud solution.

This is a big idea. Big ideas have big markets. Indeed, the addressable market for Okta’s identity cloud is the whole IT space. Okta recorded revenues of just over $100 million last quarter from growth of nearly 60%. This is nothing new. Over the past several quarters, the average revenue growth rate has hovered around 60% and the average customer growth rate has hovered around 40%.

Thus, this is a small company that is consistently and rapidly growing in a huge market. Gross margins are high, and marching higher, leaving room for big profits at scale. Overall, this is a big growth company with a ton of potential. The valuation is big, but the amount of growth firepower underneath this business implies a tremendous opportunity to grow into the valuation, and then some, making OKTA stock an attractive long term investment here.

Source: Shutterstock

Salesforce (CRM)

The king of all cloud stocks is Salesforce (NYSE:CRM), and there’s good reason for that.

Salesforce is at the heart of the cloud and data revolutions. The company leverages data and analytics to deliver robust cloud solutions to enterprises that want data-driven insights. Demand for this type of service will grow by leaps and bounds over the next several years as data-driven strategies and cloud solutions become the enterprise norm. Salesforce has developed a long-standing reputation for being the best in class for delivering these services.

That won’t change any time soon. As such, Salesforce’s revenues and profits will soar higher over the next several years as the cloud and data revolutions gain mainstream traction.

This will naturally push CRM stock higher. Valuation is somewhat of a concern at nearly 60x forward earnings. But, the company has enough growth firepower through cloud and data tailwinds to grow into its valuation. Plus, valuation has been a long-running concern for this stock, and the stock has done nothing but defy those concerns and head higher over the past several years.

The same will be true over the next several years, too. Cloud and data tailwinds will propel CRM stock higher, and this stock will ultimately grow into its valuation. Indeed, numbers indicate the stock could double in the long run.

Source: Shutterstock

Amazon (AMZN)

Amazon (NASDAQ:AMZN) is better known for its giant e-commerce business. But, the true profit growth driver behind Amazon is the company’s cloud business — Amazon Web Services.

AWS is the world’s largest cloud infrastructure services business, and it’s not even close. Amazon Web Services is bigger than its four closest competitors … combined. And the company has consistently controlled more than 30% of the cloud services market.

This dominance speaks volumes about just how good AWS is. Indeed, AWS is so good that even Amazon’s commerce competitors are giving money to the company through AWS. Notably, Amazon’s e-commerce competitor Zulily migrated its infrastructure to AWS recently. Also, AWS is so good that Amazon it is the clear front-runner to win a $10 billion Joint Enterprise Defense Infrastructure (JEDI) commercial cloud contract with the U.S. government. If Amazon were to win that contract, that would be the second government contract this decade (AWS won a $600 million CIA contract in 2013).

Overall, AWS is the clear leader in the cloud infrastructure services. As this market grows over the next several years, AWS will grow, too, and that will provide a big boost to Amazon’s profits. A big boost to Amazon’s profits will give AMZN stock firepower to head higher.

Source: Shutterstock

Alphabet (GOOGL)

Much like Amazon, Alphabet (NASDAQ:GOOGL,NASDAQ:GOOG) is better known for its non-cloud businesses.

But, a significantly underappreciated and underrated aspect of Alphabet is Google Cloud. Google Cloud is a big growth, big margin business for Alphabet. To be sure, the business has lost some steam over the past several quarters as Microsoft (NASDAQ:MSFT) has gained cloud market share at a more robust pace than Alphabet recently. But, there have been some C-suite changes at Google Cloud which could give the business new direction and new firepower to regain some lost momentum.

Regardless, Google Cloud will remain a 20%-plus growth business for a lot longer. Overall, Google Cloud is the key to unlocking the next leg of value in GOOGL stock. Fortunately, this business is progressing as expected, and will continue to do so over the next several years. As it does, GOOG stock will move higher.

As of this writing, Luke Lango was long ADBE, TWLO, CRM, AMZN and GOOG.

Do you remember the “browser wars” in the 1990s? It started when young upstart Netscape took the world by storm with its web browser.

At the time, Microsoft – with its Windows operating system – dominated the computing industry. It was a behemoth feared by all. Apple, IBM and HP were mere flecks in Microsoft’s rearview mirror.

Yet Microsoft knew that the web (and Netscape) represented an existential threat. It could be the only thing to drive Microsoft out of business.

So Microsoft pivoted. It embraced the internet and the web. And it created Internet Explorer. It was Microsoft’s bid to own access to the web.

Microsoft bundled Internet Explorer for free with its Windows operating system in an effort to crush Netscape and any other company that might have the temerity to launch its own browser.

The company’s efforts didn’t work. But they did define the competitive landscape for the better part of a decade.

Just like Microsoft more than 20 years ago, Facebook and Google have been hard at work trying to determine how they want to approach crypto – and the blockchain.

And this week, we learned more about their efforts.

Last May, David Marcus left Facebook’s Messenger product to lead Facebook’s blockchain initiatives. In December, media reports suggested Facebook was developing a cryptocurrency to be used on its WhatsApp messaging platform. And this week, Facebook hired away Chainspace’s top talent (Mashable).

The move, first reported by Cheddar, gives Facebook a talented crypto team that had been working on building smart contracts and a payment ecosystem (Cheddar).

Facebook didn’t get Chainspace’s technology. But Facebook doesn’t need the tech. It now has the talent and resources to build its own crypto ecosystem. And Facebook’s existing user base (2.32 billion monthly active users) could drive mainstream adoption. That makes Facebook a crypto force to be reckoned with.

Google, meanwhile, is entering crypto in typical Google fashion – by making it searchable. Google has uploaded the entire bitcoin and ethereum blockchains to its BigQuery cloud database and provided open-source tools to search it. It’s in the process of uploading litecoin, zcash, dash, bitcoin cash, ethereum classic and dogecoin to BigQuery. And independent programmers are uploading their own crypto datasets to BigQuery so they can search them (Forbes).

This is a remarkable development. One of the biggest regulatory issues facing crypto is market surveillance. But with the right programming or AI (artificial intelligence) in place, that problem can be solved. In fact, a Google developer has already spotted bitcoin cash being hoarded and autonomous agents moving ethereum around.

An independent developer used Google’s tools to find a specific smart contract flaw. Another created a heat map of XRP flow.

Google’s new foray into crypto has the potential to be transformational. And the entire crypto community should be on notice. Google and Facebook are playing for keeps. Everyone else needs to raise their game.

Speaking of MedMen, it’s been an interesting few months for James Parker. In the beginning of November, he was MedMen’s chief financial officer. In mid-November, MedMen announced his resignation. And by the end of January, Parker was suing MedMen for breaching its fiduciary responsibility to shareholders (Seeking Alpha).

A Florida judge has struck down a law that limits the number of medical marijuana facilities an operator can have (Orlando Sentinel).

And in Arizona, medical marijuana is legal – except when a county prosecutor says it isn’t (ABC15).

Okay, let’s follow the bouncing ball here. Arizona voters legalized medical marijuana in 2010. In 2017, a cancer patient was told by his oncologist that he should try medical marijuana. He obtained a medical marijuana card from the state and visited a legal medical marijuana dispensary where he bought some wax to help with his nausea.

A few days later, he was stopped by police for a traffic violation. And when they discovered the wax in his car, they arrested him and charged him with possession of a narcotic. He faces a 10-year prison term if convicted.

Whether this Arizona man gets convicted depends on the Arizona Supreme Court. The court is hearing a similar case about an Arizona man currently serving time for the same “crime.”

The legal “argument” at play is that the medical marijuana law says only the plant form of marijuana can be used for medical purposes. All other forms are illegal.

It’s a technicality – one that ignores the fact that he purchased the wax legally. And even the state’s attorney general doesn’t want anything to do with this case.

But the conviction has already been upheld once. Here’s hoping the Arizona Supreme Court does the right thing and frees these men from this legal nightmare.

Startups

Spotify is betting big on podcasts. It just bought podcast startups Gimlet and Anchor to fortify its strategy. The two startups had raised about $43 million combined from venture capital funds (Fortune). Spotify spent about $230 million on Gimlet and wants to spend about $500 million this year on acquisitions (Recode).

And Jetty, a startup that sells rental insurance, just raised $25 million in a Series B funding round. The round was led by Keith Rabois from Khosla Ventures (The Real Deal).

Crypto

Twitter CEO Jack Dorsey recently revealed that the only cryptocurrency he owns is bitcoin. Why bitcoin?

“Bitcoin is resilient,” Dorsey said on Twitter. “Bitcoin is principled. Bitcoin is native to internet ideals. And it’s a great brand” (Daily Hodl).

And in Argentina, 37 cities now accept bitcoin as payment for buying bus and metro (train/subway) passes (Bitcoinist).

And that’s your News Fix.

Have a great weekend!

Vin Narayanan Senior Managing Editor, Early Investing

It happened so quietly, you may not have even noticed. But the script has flipped on interest rates—and today I’m going to give you my favorite way to profit. (hint: this buy pays an 8.8% dividend—enough to hand you $8,800 a year in cash on every $100k invested—and is poised for quick 10% price upside, too!).

Let’s start at the beginning.

A Low-Key 180

I’m sure I don’t have to tell you that the big story of the last three years has been the Fed’s aggressive rate hikes. But the big story of the next three years will likely be a lack of aggressive rate hikes.

The change happened fast—at just one Fed meeting in January—and the market now expects zero hikes in 2019. Funny thing is, our best buy for this new world is a group of investments that, if you relied solely on the headlines, you’d think are some of the worst things you could own now.

I’m talking about floating-rate loans, which should rise in value as rates go up. But the Fed’s move to no hikes this year has actually created a great contrarian buying opportunity here.

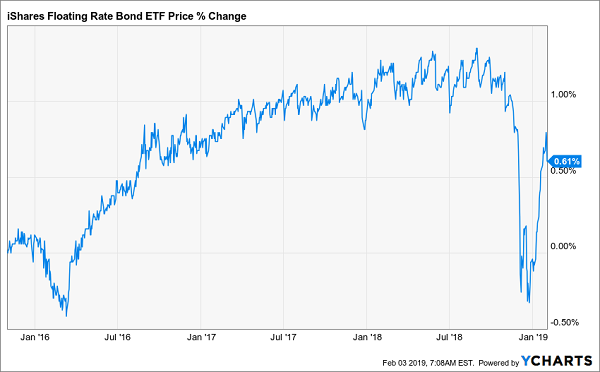

Floating-Rate Loans Have Been a Wildcard

Floating-rate loans were touted as a way to profit from higher rates since the Fed started hiking in late 2015, but there’s been a problem: reality kept butting against this theory.

Floating-Rate Loans Freeze Up

Despite the rising-rate cycle kicking off in December 2015, the benchmark iShares Floating Rate Bond ETF (FLOT) went nowhere following a brief, small bump in early 2016. And investors were no doubt frustrated with the 1% gain they got in the years they held FLOT, before kissing most of that gain goodbye in the late-2018 market panic.

In short: floating-rate loans, for much of this period, didn’t work as planned.

But now is a great time for floating-rate loans, even though the Fed rate is likely to flat-line. Because just as theory didn’t translate to reality by using these loans to profit from higher rates, the theory that their value will go down in value as rates fail to rise is equally unrealistic.

That’s because the recent fall in floating-rate-loan values has nothing to do with interest rates.

The floating-rate loan market saw a huge drop in late 2018 for two reasons: 1) There was a record number of loans in the market, due to lenders choosing floating-rates over corporate bonds (thus increasing supply and limiting price growth); and 2) There was a panic as investors feared lenders would default on their loans due to bankruptcies caused by an economic crash.

The second fear is already proving to be nonsense: not only is there no crash, but employment and corporate earnings seem likely to keep improving in 2019, even after a strong 2018. The first issue, however, is also disappearing—but many people don’t know about it.

Instead of using floating-rate loans, as they did in 2018, more US companies are going back to raising cash by issuing corporate debt in the form of bonds. They are even doing this in unusual and unexpected situations. The Financial Times tells the story of TransDigm (TDG), an aircraft-component manufacturer that used corporate bonds instead of floating-rate loans to fund its $3.8-billion acquisition of aerospace-component maker Esterline.

Commenting on the deal, TwentyFour Asset Management Head of Credit David Norris told the Financial Times: “I would typically have expected a company like this, doing an acquisition, to go to the loan market. But they didn’t do that. There are opportunities right now in the high-yield bond market.”

With the decline in the number of floating-rate loans, demand for those still in existence (and the few new ones coming to market) will likely drive up prices, especially since overblown default fears have kept floating-rate loans below their pre-crash levels.

That means there’s a huge buying opportunity for savvy buyers—especially if we get our floating-rate-loan exposure through closed-end funds (CEFs).

Floating-Rate Confusion Hands Us an 8.8% Cash Payout

Since CEFs often pay huge dividends, your chance to grab 7%+ yields from floating-rate funds is now. But which funds to pick?

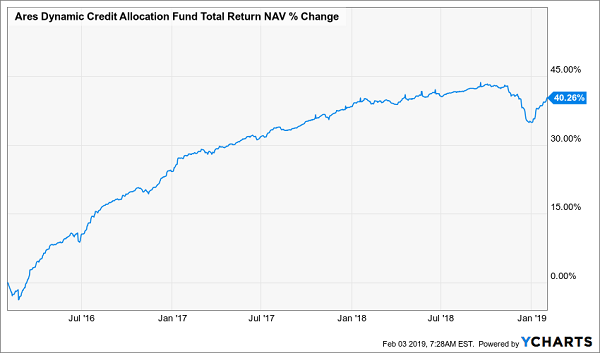

One of the most discounted floating-rate funds also has one of the biggest yields: the Ares Dynamic Credit Allocation Fund (ARDC) pays a massive 8.8%. It also gets “bounce-back” upside from its 13.1% discount to net asset value (NAV, or the what its underlying loan portfolio is worth). That’s well below the 7.2% discount it achieved in the past year.

As you might suspect, the fund’s name comes from its management team: Ares Management, which runs a number of funds and companies that provide credit to medium-sized businesses, including its business-development company, Ares Capital Corporation (ARCC). Ares Capital is the biggest BDC, with $12.3 billion in assets under management.

That size is important, because it means Ares has deep connections with many borrowers and knows which can pay their bills and which can’t. That has meant an impressive run-up for ARDC since interest rates started rising:

“In the Know” Management Delivers

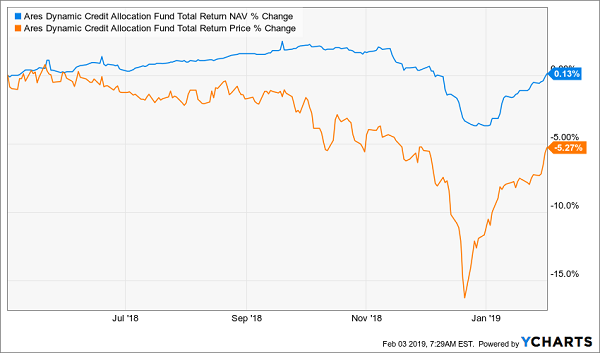

While investors typically reward ARDC with a steadily rising market price to match its portfolio’s fundamental strength, the fund’s price return is still lagging:

A Rare Buying Opportunity

The takeaway? Now is a great time to tap ARDC for its 8.8% income stream and hold while my expected 10% capital gain from both a strengthening floating-rate-loan market and the fund’s shrinking discount start to appear.