A New York Times (NYT) headline blared, “Too Little Too Late’: Bankruptcy Booms Among Older Americans”. They reference a Consumer Bankruptcy Project (CBP) study, “Graying of U.S. Bankruptcy: Fallout from Life in a Risk Society”:

“For a rapidly growing share of older Americans, traditional ideas about life in retirement are being upended by a dismal reality: bankruptcy.

…. Driving the surge …. is a three-decade shift of financial risk from government and employers to individuals, who are bearing an ever-greater responsibility for their own financial well-being as the social safety net shrinks.”

While the NYT is noted for wrapping selective facts inside an article pushing a political ideology, the study appears well-researched. Look at the source data and form your own conclusions.

How bad is the problem?

The study shows triple-digit gains in bankruptcy for those over 55:

“The number of senior households filing bankruptcy is not negligible. With 800,000 household filings annually, approximately 97,600 (12.2 percent) of those are households headed by seniors. The drivers of these bankruptcies were reported by our respondents. The most pressing was inadequate retirement and employment income.(Emphasis mine)”

In 2013, John Mauldin and Jonathan Tepper authored, “Code Red, How to protect your Savings from the Coming Crisis”. Central banks lowered interest rates to historically low levels (Zero Interest Rate Policy – ZIRP); forcing yield-starved savers into the stock market:Why inadequate income?

“(Fed Chairman) Bernanke openly acknowledges that his low interest-rate policy is designed to get savers and investors to take more chances with riskier investments. The fact that this is precisely the wrong thing for retirees and savers seems to be lost in their pursuit of market and economic gains.” (Emphasis mine)

The CBP weighs in:

“While many Americans confront these risk shifts, they profoundly affect older people….

…. With the 401(k)-style of savings, payout during retirement is not defined or predictable,employees bear all of the market risks, and returns depend on employees’ investment skills.” (Emphasis mine)

| Retirees saw their guaranteed, safe income projections fall woefully short. There was zero risk in FDIC insured CDs! |

This 2013 New Yorker magazine article, “Shut Up, Savers!” marginalizes the critics of Fed Chairman Ben Bernanke:

“…. to his detractors, Bernanke is guilty of waging a “war on savers”-fleecing people, especially retirees, of hundreds of billions of dollars that they could have earned in interest.

Certainly, it’s not the easiest time to live off interest income. The average rate on a savings account is less than 0.25 percent. Long-term certificates of deposit offer rates well below inflation, and even a ten-year government bond yields less than two percent.”

…. It’s easy to understand why savers feel like collateral damage (Emphasis mine) in the Fed’s fight against recession, but too much sympathy for their plight is dangerous.”

Dr. Ron Paul recently took another look at the economic fallout in, “The Dollar Dilemma: Where To From Here?”

“…. It is true that the rich are getting richer and the middle class is being wiped out. (Emphasis mine) …. The seriousness of the problem, …. explains the anger and frustration the people feel.”

Wiping out the middle class and almost 100,000 bankruptcies in a single year is a heck of a lot of collateral damage!

A second opinion

I reviewed the “Employee Benefit Research Institute 2018 Retirement Confidence Survey”. The EBRI is non-partisan. Retirement confidence is rapidly declining:

Their press release says:

“This year’s Retirement Confidence Survey (RCS) finds …. retiree confidence in having enough money to cover basic expenses and medical expenses has dropped: 80 percent say they are very/somewhat confident about covering basic expenses this year compared to 85 percent in 2017; and 70 percent say they are very/somewhat confident about covering medical expenses this year vs. 77 percent in 2017.

The EBRI discusses how important Defined Contribution (DC) plans, like a 401(k), are for retiree confidence.

“Those with a defined contribution (DC) plan like a 401(k) are far more likely to say they are confident in their ability to live comfortably in retirement: 76 percent of workers with a DC plan are at least somewhat confident in their ability to live comfortably in retirement versus 46 percent of those without a DC plan.

…. However, the data suggests many plan participants don’t know what to do with their DC plan assets at retirement.” (Emphasis Mine)

Here is what the New Yorker wants us to shut up about….

| Ten years ago the government bailed out the banks at the expense of seniors and savers. Social security benefits won’t keep up with inflation while medical costs rise by double digits.Americans are problem solvers and will deal with it, but I hope they never shut up. |

While Dr. Paul is correct, there is a lot of anger and frustration, it’s foolhardy to expect the government to fix anything.

What can WE do?

Two major factors affect us all. Even though they may not push us into bankruptcy, they should be understood and dealt with as best you can.

Debt is the enemy.

CBP weighs in:

…. 71.6 percent either “very much” or “somewhat” agreed that they filed because of the stress of dealing with debt collectors. Collectors called their homes, their workplace, their families, and knocked on their doors.

They quoted several respondents:

“All things went up in price. Retirement never went up. Had a part-time job that was helping to meet monthly payments.House payment kept going up.” ….

“Mismanaged my retirement savings…. Tried to restructure my debts but creditors refused. Unable to find suitable employment to pay my credit cards.” ….

“My wife developed medical problems and had to leave her job…. About two years later, I developed medical problems and was not able to continue working. We …. simply could not handle the debt load. The constant calls from bill collectors forced us to contact an attorney for help.”

The EBRI also discusses debt:

| It appears that the majority of workers and retirees are not concerned about debt impacting their ability to save or retire until they suffer an income loss while the debts remain. |

Dump the debt! Save your line of credit for real emergencies. Downsize and do what it takes to be debt free!

The debt rule is simple, “get out, stay out, and don’t ever come back!” I’ve never met anyone who lamented being debt free.

CBP weighs in heavily on medical costs:Medical Costs

“Despite the widespread belief that Medicare meets health needs of older Americans, …. it is utterly inadequate. Out-of-pocket spending among older Americans with Medicare comprises about 20 percent of their income, and the estimated total of all noncovered medical expenses for a 65-year-old retired couple during their retirement years is $200,000….

…. Respondents were asked to list the single most important thing that they or their family members were unable to afford in the year before their bankruptcies. Over half of older filers (52 percent) who responded indicated that the single most important thing they had to forego was related to medical care-surgeries, doctor visits, prescriptions, dental care, and health/supplemental insurance. These responses continue to suggest that their health care coverage is inadequate.”

EBRI shows the public has little confidence in the government providing medical care, social security – or doing the right thing:

What is the solution?

The NYT and CBP pushed for government-provided funded health care for all.

I prefer to avoid partisan politics; the entire political class governs against the will of the majority.

When I was with Casey Research I spent countless hours researching government health care. I interviewed doctors who practiced worldwide. I spoke with experts and a member of Congress who was on the committee that drafted Obamacare.

I’ve concluded:

- Government sponsored health care sounds good, but in practice it is terrible.

- While the motives of the health care workers may be pure, quality health care deteriorates. If the VA had to care for all Americans – do you think their quality would improve?

- Government health care is fiscally impossible. Health care costs in the UK are bankrupting the country.

- The underlying (unstated) motive of government health care is to ration care for seniors. A senior congressman told me the basis for care was the value of the citizen to society. Seniors could eventually expect end of life counseling as opposed to health care.

- Most countries have a two-tiered system; one for the masses and one for the elite who can afford to pay out of pocket. Many Canadians come to the US for treatment that they cannot get in Canada. I spent an hour with the president of a big-name hospital in central America. They were gearing up for hundreds of US patients once government medical is fully implemented.

- Expect social engineering. Politicos always pander for votes. I’m confident the majority of US citizens oppose paying for health care for those in the country illegally.

Buy good insurance! Medicare by itself will not provide quality coverage. The old adage, “you get what you pay for” applies to insurance premiums also. Many who bought inexpensive coverage did not realize it was inadequate until it was too late.

Those filing for bankruptcy are the tip of the iceberg. No one wants to live out their golden years constantly worrying about money. Get out of debt, save your money, learn how to invest wisely and buy good insurance.

And most of all – don’t ever be bullied into shutting up by anyone pushing a political agenda, whatever it may be.

Pay Your Bills for LIFE with These Dividend Stocks Get your hands on my most comprehensive, step-by-step dividend plan yet. In just a few minutes, you will have a 36-month road map that could generate $4,804 (or more!) per month for life. It's the perfect supplement to Social Security and works even if the stock market tanks. Over 6,500 retirement investors have already followed the recommendations I've laid out.

Click here for complete details to start your plan today.

Iron Mountain Inc. (NYSE: IRM) is a niche REIT that provides information and asset storage, records management, data centers, data management and secure shredding services. The company has facilities and provides services in Asia, Europe, Africa and South America as well as in North America.

Iron Mountain Inc. (NYSE: IRM) is a niche REIT that provides information and asset storage, records management, data centers, data management and secure shredding services. The company has facilities and provides services in Asia, Europe, Africa and South America as well as in North America. Brixmor Property Group (NYSE: BRX) is an owner and operator of high-quality, open-air shopping centers. The Company’s more than 500 retail centers located primarily located in the eastern one-third of the continental U.S.

Brixmor Property Group (NYSE: BRX) is an owner and operator of high-quality, open-air shopping centers. The Company’s more than 500 retail centers located primarily located in the eastern one-third of the continental U.S. Crown Castle International Corp (NYSE: CCI) owns cell phone towers, which are leased by the various wireless services providers. The company is the nation’s largest provider of shared wireless infrastructure.

Crown Castle International Corp (NYSE: CCI) owns cell phone towers, which are leased by the various wireless services providers. The company is the nation’s largest provider of shared wireless infrastructure. Macerich Co (NYSE: MAC) focuses on the acquisition, leasing, management, development and redevelopment of regional malls throughout the United States. Currently the company owns 48 “market dominant” Class A malls located across the U.S. Macerich has paid a growing dividend for over 20 years.

Macerich Co (NYSE: MAC) focuses on the acquisition, leasing, management, development and redevelopment of regional malls throughout the United States. Currently the company owns 48 “market dominant” Class A malls located across the U.S. Macerich has paid a growing dividend for over 20 years.

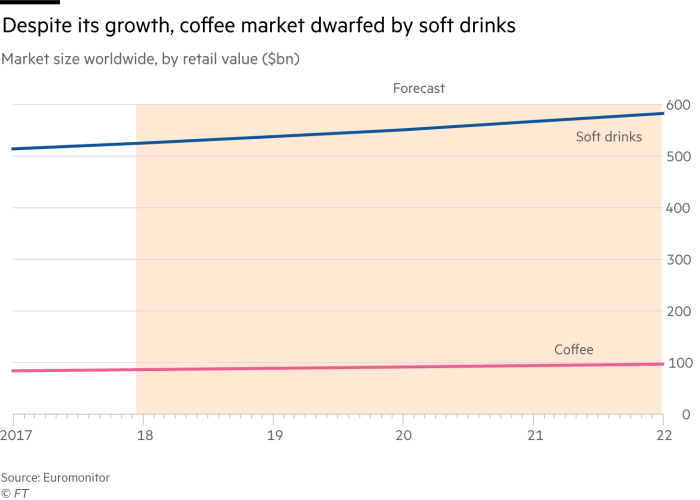

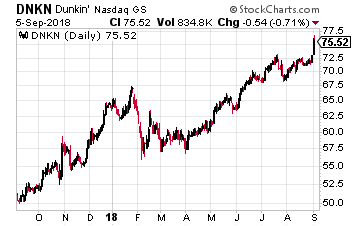

This data is also why Dunkin Brands (Nasdaq: DNKN) is Wall Street’s hottest takeover target, sending its stock to all-time highs. Dunkin is a lot more than a donut shop today and has pushed into more upmarket coffee offerings such as cold brew and espresso drinks. It will likely be added to the $250 billion in deals in the coffee business over the past six years.

This data is also why Dunkin Brands (Nasdaq: DNKN) is Wall Street’s hottest takeover target, sending its stock to all-time highs. Dunkin is a lot more than a donut shop today and has pushed into more upmarket coffee offerings such as cold brew and espresso drinks. It will likely be added to the $250 billion in deals in the coffee business over the past six years.

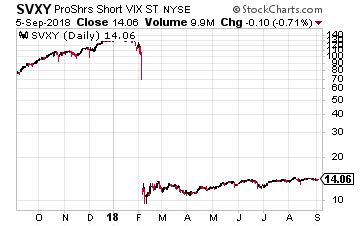

That’s not to say selling volatility is a bad idea. Quite the contrary, intelligently shorting of volatility (adhering to a strict risk management plan for one) can be a great way to generate income. Even after the death of XIV (a short volatility ETP) and the declawing of Proshares Short VIX Short-Term Futures ETF (NYSE: SVXY), going from -1 inverse short-term VIX to -0.5 inverse, shorting volatility has persisted.

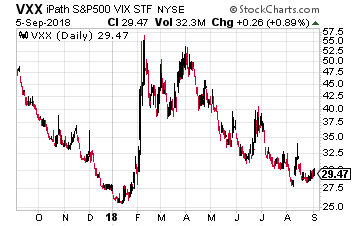

That’s not to say selling volatility is a bad idea. Quite the contrary, intelligently shorting of volatility (adhering to a strict risk management plan for one) can be a great way to generate income. Even after the death of XIV (a short volatility ETP) and the declawing of Proshares Short VIX Short-Term Futures ETF (NYSE: SVXY), going from -1 inverse short-term VIX to -0.5 inverse, shorting volatility has persisted. For instance, a huge block trade that caught my eye this week was a trader selling nearly 13,000 of the iPath S&P 500 VIX Short-Term Futures ETN (NYSE: VXX) 47 calls expiring on October 5th with the stock at $29.61. The trader collected $0.58 per contract or around $740,000 for the trade.

For instance, a huge block trade that caught my eye this week was a trader selling nearly 13,000 of the iPath S&P 500 VIX Short-Term Futures ETN (NYSE: VXX) 47 calls expiring on October 5th with the stock at $29.61. The trader collected $0.58 per contract or around $740,000 for the trade.

And you can’t get any bigger in the U.S. financial industry than JPMorgan (NYSE: JPM). It is launching its own low-cost digital trading platform, throwing down the gauntlet to online brokerages such as my former employer, CharlesSchwab.

And you can’t get any bigger in the U.S. financial industry than JPMorgan (NYSE: JPM). It is launching its own low-cost digital trading platform, throwing down the gauntlet to online brokerages such as my former employer, CharlesSchwab. One such blue chip you can buy now for no commission at Robinhood is the world’s number two sportswear maker, Adidas (OTC: ADDYY), which is catching up to Nike.

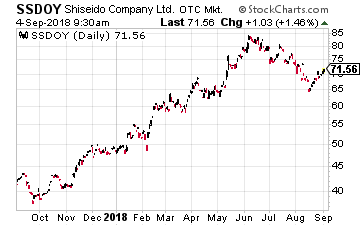

One such blue chip you can buy now for no commission at Robinhood is the world’s number two sportswear maker, Adidas (OTC: ADDYY), which is catching up to Nike. Another very high quality company that is doing very well is Asia’s largest cosmetics company, Japan’s Shiseido (OTC: SSDOY).

Another very high quality company that is doing very well is Asia’s largest cosmetics company, Japan’s Shiseido (OTC: SSDOY).

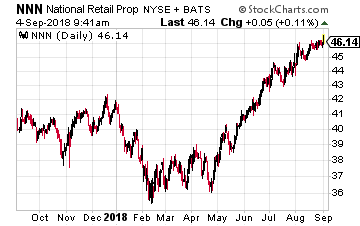

National Retail Properties, Inc. (NYSE: NNN) is a traditional triple-net lease REIT. The company owns over 2,800 (up by 300 in the last year) free-standing, single tenant retail properties. most of the REIT’s tenants are in business that cannot be hurt or replaced by online sellers.

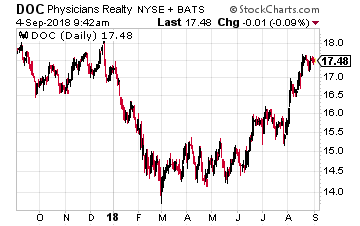

National Retail Properties, Inc. (NYSE: NNN) is a traditional triple-net lease REIT. The company owns over 2,800 (up by 300 in the last year) free-standing, single tenant retail properties. most of the REIT’s tenants are in business that cannot be hurt or replaced by online sellers. Physicians Realty Trust (NYSE: DOC) is a healthcare REIT that focuses its portfolio on medical office, physician group practice clinics, outpatient care, ambulatory surgery centers, specialized hospitals, rehabilitation facilities and small specialized long-term acute care hospitals. The company owns 249 properties located in 30 states. Ninety-two percent of the holdings are medical office buildings. Even through tough economic times, the healthcare sector will still need its offices and care facilities.

Physicians Realty Trust (NYSE: DOC) is a healthcare REIT that focuses its portfolio on medical office, physician group practice clinics, outpatient care, ambulatory surgery centers, specialized hospitals, rehabilitation facilities and small specialized long-term acute care hospitals. The company owns 249 properties located in 30 states. Ninety-two percent of the holdings are medical office buildings. Even through tough economic times, the healthcare sector will still need its offices and care facilities.