Source: Shutterstock

The pace of technology is breathtaking. Just some of the trends include cloud computing, AI (Artificial Intelligence), machine learning and the IoT (Internet of Things). So for investors, there are many opportunities.

But then again, breakout stocks are usually volatile — and expensive. It can be tough to make a purchase decision when the returns have already been over triple digits for the past year! And because the expectations are at lofty levels, it does not take much to deflate the stock when there is some bad news.

This is why investors need to be cautious with breakout stocks. Basically, they really should only be a small portion of your portfolio.

So then, what are some companies to consider that could spice up your portfolio? Here’s a look at three:

Breakout Stocks to Buy: Okta (OKTA)

Okta (NASDAQ:OKTA) is a next-generation cloud operator that develops identity services for enterprises. For the most part, the focus is on helping to secure access to critical information. The platform has more than 5,500 pre-built integrations and over 5,100 customers.

Okta has also been seeing a strong acceleration in its growth. Just look at the latest quarter, as the company pummeled Wall Street expectations. Revenues soared by 57% to $94.6 million, compared to the consensus forecasts of $84.8 million. The company also raised its full-year guidance to $372 million to $375, up from the prior forecast of $353 million to $357 million.

A key is that the company has been getting much more traction with large customers. During the past year, there was a 55% increase in the number of customers that generate subscriptions of $100,000 or more. This is all part of the so-called “land and expand” strategy.

But it does look like the opportunity for Okta is still in the early phases. According to CEO Todd McKinnon, during the latest earnings call: “It starts with the significant market tailwind in our favor. Every organization is moving to the cloud. Every company has to become a technology company and everyone is worried about security. We are seeing identity become mainstream as organizations recognize the critical role that identity plays in their environment.”

Breakout Stocks to Buy: Advanced Micro Devices (AMD)

Despite a rough ride today, the turnaround of Advanced Micro Devices (NASDADQ:AMD) is starting to show big-time results. CEO Lisa Su has done an amazing job of focusing on the major opportunities while also being disciplined with the bottom line.

Even though AMD has been around since the late 1960’s, the company now looks more like a scrappy startup. In the most recent quarter, revenues jumped by 53% to $1.76 billion.

As for the main driver, it is the enormous datacenter market. Keep in mind that AMD’s EPYC server processor has gotten adoption from companies like Cisco (NASDAQ:CSCO) and HP Enterprise (NYSE:HPE). It also helps that rival Intel (NASDAQ:INTC) has stumbled, as it has been slow to introduce new chipsets. The company currently has about 99% of the market for datacenters.

In other words, it is a very juicy target for AMD.

Wall Street is definitely getting excited, with multiple upgrades. For example, FBN Securities analyst Shebly Seyrafi notes that the server-chip market is about $16 billion and that the EPYC chip is poised for strong gains.

Breakout Stocks to Buy: Cloudera (CLDR)

Back in early April, big data company Cloudera (NYSE:CLDR) stock got crushed, plunging by more than 40%. The company whiffed on its earnings as the growth engine stalled.

Yet management at CLDR took swift action, especially with the restructuring the sales team. And it looks like things are getting back on track. In the second quarter, revenues rose by 23% to $110.3 million, while the Street was looking for $107.7 million. The 8-cent loss was also much better than the consensus forecast of 15 cents. What’s more, CLDR increased its full-year guidance to $440 million to $450 million, up from $435 million to $445 million.

The company certainly faces tough competition from companies like Amazon (NASDAQ:AMZN), Microsoft (NASDAQ:MSFT) and Alphabet (NASDAQ:GOOG, NASDAQ:GOOGL). But the market size is large enough for multiple players. Besides, CLDR’s strategy of disrupting the traditional data warehousing market appears to be spot-on, as functions like machine learning, AI (Artificial Intelligence) and analytics move towards cloud platforms.

Get your hands on my most comprehensive, step-by-step dividend plan yet. In just a few minutes, you will have a 36-month road map that could generate $4,804 (or more!) per month for life. It's the perfect supplement to Social Security and works even if the stock market tanks. Over 6,500 retirement investors have already followed the recommendations I've laid out.

Click here for complete details to start your plan today.

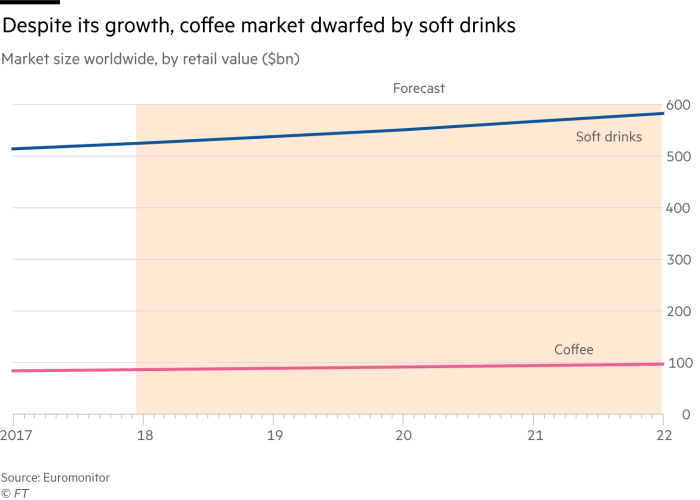

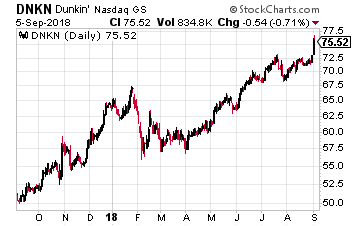

This data is also why Dunkin Brands (Nasdaq: DNKN) is Wall Street’s hottest takeover target, sending its stock to all-time highs. Dunkin is a lot more than a donut shop today and has pushed into more upmarket coffee offerings such as cold brew and espresso drinks. It will likely be added to the $250 billion in deals in the coffee business over the past six years.

This data is also why Dunkin Brands (Nasdaq: DNKN) is Wall Street’s hottest takeover target, sending its stock to all-time highs. Dunkin is a lot more than a donut shop today and has pushed into more upmarket coffee offerings such as cold brew and espresso drinks. It will likely be added to the $250 billion in deals in the coffee business over the past six years.

By now, everyone knows the dangers of investing in

By now, everyone knows the dangers of investing in

So get ready everyone… it looks like Amazon (Nasdaq: AMZN)is getting ready to dominate in another sector of the economy. But this time it is not going after traditional industries such as retailing or logistics or even healthcare.

So get ready everyone… it looks like Amazon (Nasdaq: AMZN)is getting ready to dominate in another sector of the economy. But this time it is not going after traditional industries such as retailing or logistics or even healthcare. One needs only to look at Amazon’s last earnings report to see that its advertising business is just starting to grow. The company’s CFO, Brian Olsavsky, called Amazon’s ad sales business “a multibillion-dollar program and growing very quickly.” Advertising sales made up the majority of sales in Amazon’s “other” section of their earnings.

One needs only to look at Amazon’s last earnings report to see that its advertising business is just starting to grow. The company’s CFO, Brian Olsavsky, called Amazon’s ad sales business “a multibillion-dollar program and growing very quickly.” Advertising sales made up the majority of sales in Amazon’s “other” section of their earnings.