Much of the income stock universe will report 2019 first quarter results starting on April 28 and running through May 8. Last week there was a 4% to 5% sell-off of many income stocks.

The drop was fueled by some negative Wall Street analyst comments that don’t seem to be well grounded in reality. For many stocks, the quarterly earnings reports are most of the real news upon which long term investors can hang their hats.

I expect that earnings from quality dividend paying companies will positively surprise the market and lead to a reverse of last week’s share price declines.

For long-term, income focused investors, earnings season is a mixed bag. The actual earnings and management comments provide an accurate snapshot of a company’s business and how well they are operating in relation to expectations.

For the stocks I follow, I have a good idea on where the important numbers such as cash flow and dividends should trend. Whether a company remains on or misses the forecast trend determines my recommendation concerning the stock.

The downside to earnings are the games played between Wall Street analyst estimates and the actual earnings result. An earnings “miss” can produce significant share price volatility.

Since the Wall Street crowd changes there expectations frequently, the estimates are of little use for real investment planning. The share price moves you see around the earnings dates are just a game between Wall Street and short term traders.

If you are a longer term investor, sharp share price drops in quality dividend stocks should be viewed as attractive times to buy.

Here are three stocks that have dropped in the weeks before they release earnings and have good potential to exceed market expectation when results are actually announced.

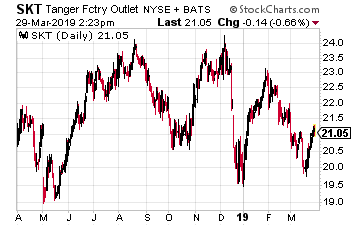

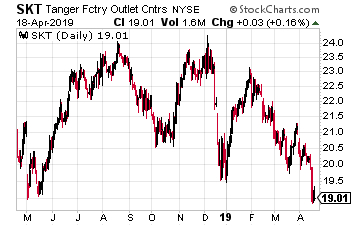

Tanger Factory Outlet Centers (SKT) is real estate investment trust –REIT—that is the only pure play outlet mall company in the larger shopping center REIT sector. The SKT share price has lost 10% of its value over the last few weeks.

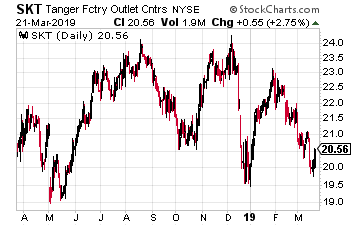

Over the last two years, Tanger has struggled with tenant retailers declaring bankruptcy, returning space in the REIT’s malls. Management has been able to keep occupancy high at the cost of not getting historical rental rate growth.

Cash flow per share has been flat and dividend increases in the 1.5% per year range. On the positive side, Tanger has a very conservative balance sheet and a 25 year history of successful business management and dividend growth.

A positive quarterly result could give this stock a solid share price increase. SKT currently yields 7.5%.

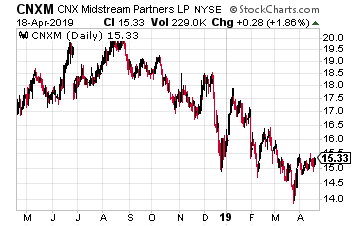

CNX Midstream Partners LP (CNXM) is a growth-oriented master limited partnership –MLP– that owns, operates, and develops gathering and other midstream energy assets to service natural gas production in the Marcellus Shale in Pennsylvania and West Virginia.

While much of the energy infrastructure sector has gone through a painful round of financial restructuring, CNXM has steadily grown its revenues and distributions to investors. The MLP’s small cap status has kept it off the radar of investors.

With a 9% yield and 15% distribution growth, this MLP has a good chance for a nice value pop when earnings come out.

New Residential Investment Corp (NRZ) is a finance REIT whose complicated investment portfolio leaves investors confused concerning the company’s prospects. Thus the 12% yield. Over the last six months New Residential has raised over $1 billion from common stock secondary offerings.

Management has not yet revealed how that capital will be invested. A big investment or merger announcement with earnings could boost the NRZ share price.

Source: Investors Alley