The U.S. home building industry faces a Jekyll and Hyde situation. The good news is that the home construction industry has built much fewer houses over the last decade than are needed by a growing population and new household formations. At the same time builders face headwinds from rising material costs, labor costs, and higher mortgage rates. The opposing forces may make it tough for home builders to grow profits, but material supplies—lumber producers—should continue to see growing profits from higher prices.

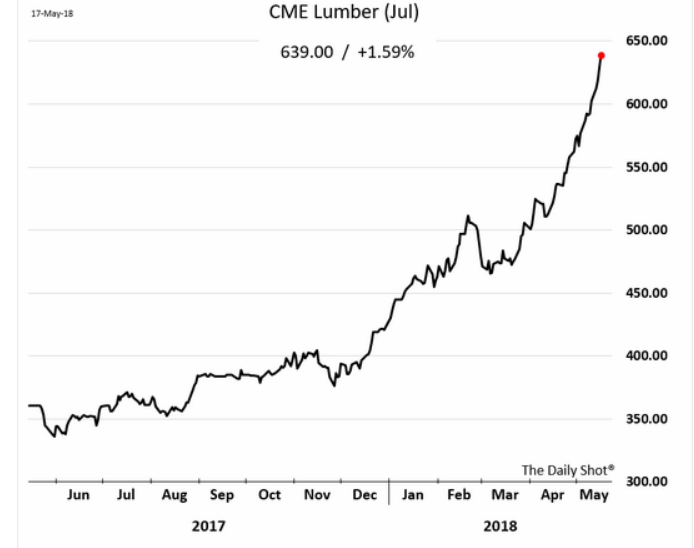

A recent news article noted that the National Association of Homebuilders says rising lumber prices have already increased the average price of a single-family home by $6,400 since January of last year. Here is a chart published by the Wall Street Journal showing the lumber futures price.

My expectation is that home builders will be able to build and sell enough homes to stay profitable. There is enough demand from the population needing additional housing to prevent enough of a slowdown to make building new homes completely unprofitable. If homes continue to be built, one of the winners will be the lumber producers.

There are three real estate investment trusts (REITs) that own timberland and sell lumber and other wood products. With the REIT structure these companies will likely pass along higher profits as rising dividends for share owners.

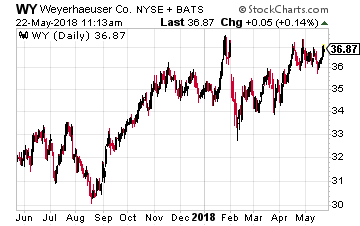

Weyerhaeuser Company (NYSE: WY) with a $27.6 billion market cap is one of the largest companies in the REIT sector. The company converted to a REIT in 2010. Over the last six years, Weyerhaeuser has doubled its timber holdings to 12.6 million acres. These holdings make the company the largest private timberland owner in the U.S.

Weyerhaeuser Company (NYSE: WY) with a $27.6 billion market cap is one of the largest companies in the REIT sector. The company converted to a REIT in 2010. Over the last six years, Weyerhaeuser has doubled its timber holdings to 12.6 million acres. These holdings make the company the largest private timberland owner in the U.S.

To process and sell the timber, Weyerhaeuser owns 35 mills and 18 distribution facilities. In 2017 adjusted EBITDA grew by 30%. For the 2018 first quarter, EBITDA was up 20% year over year and net income per share was up 63%.

In December the company increased the quarterly dividend by 3.2%. This year, I expect a high single digit to low double digit increase. WY currently yields 3.5%.

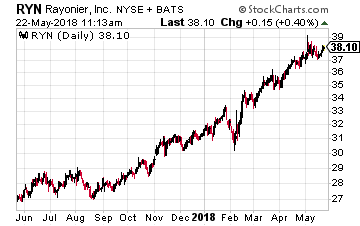

Rayonier Inc. (NYSE: RYN) owns 2.6 million acres of timberland in the U.S. and New Zealand. The company divides its operations into forest product sales and real estate sales. Rayonier will sell land that was once best suited for growing timber but is now more valuable for residential, industrial, commercial or conservation use.

Rayonier Inc. (NYSE: RYN) owns 2.6 million acres of timberland in the U.S. and New Zealand. The company divides its operations into forest product sales and real estate sales. Rayonier will sell land that was once best suited for growing timber but is now more valuable for residential, industrial, commercial or conservation use.

For the 2018 first quarter, adjusted EBITDA of $94.3 million was up 65% compared to a year earlier. Net income climbed by 15.8%. On Monday—May 21—the company announced an 8% increase in the quarterly dividend. Prior to this increase the dividend had not changed for over three years.

If timber prices remain strong there is potential for another increase or a year-end special dividend. RYN currently yields 2.8%.

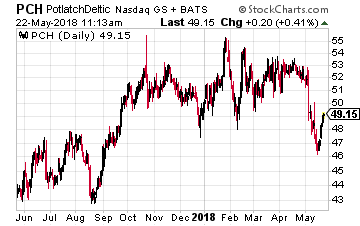

In February 2018 Potlatch and Deltic Timber Combined to form PotlatchDeltic Corporation (Nasdaq: PCH). The result of the merger is a leading timberland REIT and lumber manufacturer. The company owns two million acres of timberland in the U.S.

In February 2018 Potlatch and Deltic Timber Combined to form PotlatchDeltic Corporation (Nasdaq: PCH). The result of the merger is a leading timberland REIT and lumber manufacturer. The company owns two million acres of timberland in the U.S.

The merger converted the Deltic assets to REIT status. As a result, management has already stated a special cash plus shares dividend will be paid at the end of 2018. The regular quarterly dividend was increased by 7% in anticipation of the improved results due to combining the two companies.

PCH currently yields 3.3%.

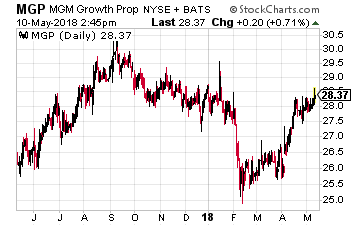

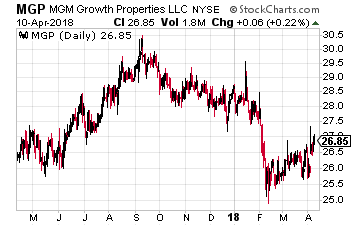

In April 2016, hotel and gaming company MGM Resorts International (NYSE: MGM) spun off about two-thirds of its hotel properties into a new real estate investment trust (REIT) IPO. MGM structured the new company, called MGM Growth Properties LLC (NYSE: MGP), to have a high level of cash flow safety to pay the planned dividend and with the potential for future growth.

In April 2016, hotel and gaming company MGM Resorts International (NYSE: MGM) spun off about two-thirds of its hotel properties into a new real estate investment trust (REIT) IPO. MGM structured the new company, called MGM Growth Properties LLC (NYSE: MGP), to have a high level of cash flow safety to pay the planned dividend and with the potential for future growth. At the end of 2017 I forecast that the energy midstream/infrastructure sector would return to valuation growth in 2018 providing lots of upside potential in the group. Through 2017 MLP sector market values declined sharply even as business fundamentals continued to improve. 2018 should be the year when investors realize very attractive returns from the quality companies in the sector.

At the end of 2017 I forecast that the energy midstream/infrastructure sector would return to valuation growth in 2018 providing lots of upside potential in the group. Through 2017 MLP sector market values declined sharply even as business fundamentals continued to improve. 2018 should be the year when investors realize very attractive returns from the quality companies in the sector.

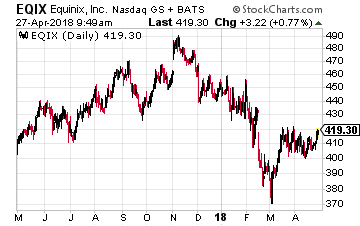

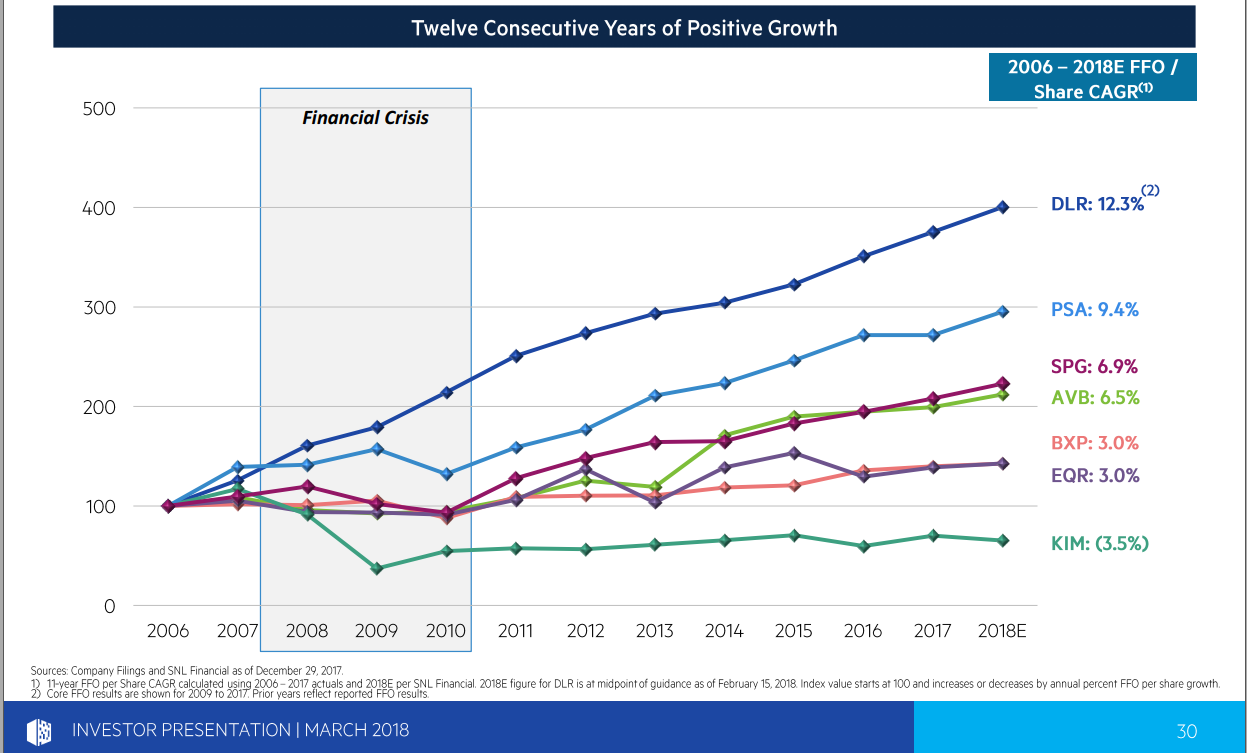

Equinix, Inc. (Nasdaq: EQIX) is the $32 billion market cap, 800 lb. gorilla of the data center industry. The company converted from corporate tax payer to REIT status at the start of 2015. The company is a colocation and interconnection service provider. Colocation is a data center facility in which a business can rent space for servers and other computing hardware. Typically, a colocation facility provides the building, cooling, power, bandwidth and physical security while the customer provides servers and storage.

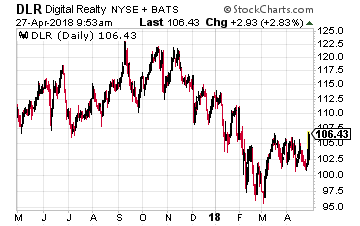

Equinix, Inc. (Nasdaq: EQIX) is the $32 billion market cap, 800 lb. gorilla of the data center industry. The company converted from corporate tax payer to REIT status at the start of 2015. The company is a colocation and interconnection service provider. Colocation is a data center facility in which a business can rent space for servers and other computing hardware. Typically, a colocation facility provides the building, cooling, power, bandwidth and physical security while the customer provides servers and storage. Digital Realty Trust, Inc. (NYSE: DLR) is a $20 billion market cap REIT that owns 205 data centers in 12 countries. Digital Realty has 2,300 customers. Digital Realty is also a colocation and interconnection services provider.

Digital Realty Trust, Inc. (NYSE: DLR) is a $20 billion market cap REIT that owns 205 data centers in 12 countries. Digital Realty has 2,300 customers. Digital Realty is also a colocation and interconnection services provider.

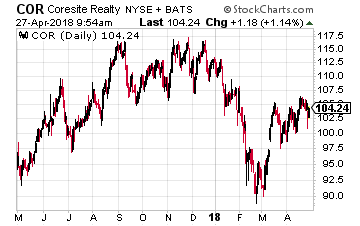

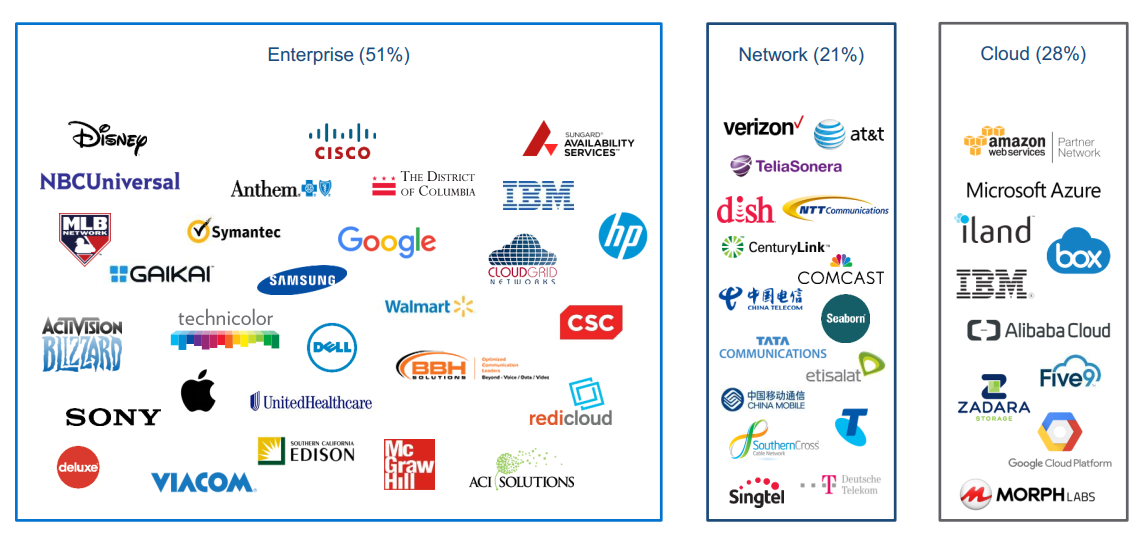

CoreSite Realty Corp (NYSE: COR) is a $3.6 billion market cap REIT that owns 20 data centers in eight strategic U.S. cities. The company’s focus is to provide colocation services to enterprise, network, and cloud services companies. Here is a graphic of the larger (out of 1200) customers:

CoreSite Realty Corp (NYSE: COR) is a $3.6 billion market cap REIT that owns 20 data centers in eight strategic U.S. cities. The company’s focus is to provide colocation services to enterprise, network, and cloud services companies. Here is a graphic of the larger (out of 1200) customers:

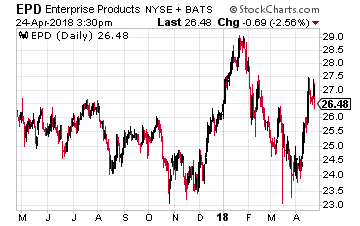

Enterprise Products Partners LP (NYSE: EPD) with a $57 billion market cap is the largest midstream MLP. The company provides the full range of energy infrastructure services. EPD is one of the biggest pipeline service providers to transport crude oil from the Permian to the Texas Gulf Coast. It recently announced that its 416-mile Midland-to-Sealy pipeline is now in full service with an expanded capacity of 540,000 barrels per day (BPD) and capable of transporting batched grades of crude oil.

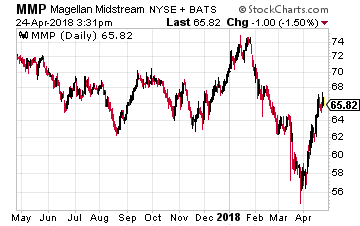

Enterprise Products Partners LP (NYSE: EPD) with a $57 billion market cap is the largest midstream MLP. The company provides the full range of energy infrastructure services. EPD is one of the biggest pipeline service providers to transport crude oil from the Permian to the Texas Gulf Coast. It recently announced that its 416-mile Midland-to-Sealy pipeline is now in full service with an expanded capacity of 540,000 barrels per day (BPD) and capable of transporting batched grades of crude oil. Magellan Midstream Partners LP (NYSE: MMP) primarily owns and operates refined products (gasoline, diesel fuel, jet fuel, etc.) pipelines and storage terminals. The company also owns 2,200 miles of interstate crude oil pipelines. The company provides service to almost 50% of the U.S. refining capacity.

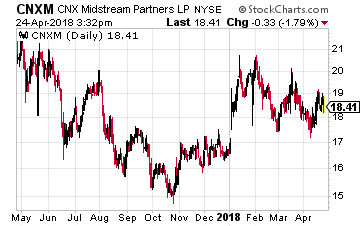

Magellan Midstream Partners LP (NYSE: MMP) primarily owns and operates refined products (gasoline, diesel fuel, jet fuel, etc.) pipelines and storage terminals. The company also owns 2,200 miles of interstate crude oil pipelines. The company provides service to almost 50% of the U.S. refining capacity. CNX Midstream Partners LP (NYSE: CNXM) owns, operates, develops and acquires gathering and other midstream energy assets to service natural gas production in the Appalachian Basin in Pennsylvania and West Virginia. This MLP primarily provides gathering and processing services to CNX Resources Corp (NYSE: CNX), which is also the sponsor and holds the MLP’s general partner interests.

CNX Midstream Partners LP (NYSE: CNXM) owns, operates, develops and acquires gathering and other midstream energy assets to service natural gas production in the Appalachian Basin in Pennsylvania and West Virginia. This MLP primarily provides gathering and processing services to CNX Resources Corp (NYSE: CNX), which is also the sponsor and holds the MLP’s general partner interests.

MGM Growth Properties LLC (NYSE: MGP) is a real estate investment trust that came to market in April 2016. As the name indicates, the new REIT was spun-off by hotel and gaming company MGM Resorts International (NYSE: MGM). At the IPO, MGM Growth Properties received title to seven properties on the Las Vegas Strip:

MGM Growth Properties LLC (NYSE: MGP) is a real estate investment trust that came to market in April 2016. As the name indicates, the new REIT was spun-off by hotel and gaming company MGM Resorts International (NYSE: MGM). At the IPO, MGM Growth Properties received title to seven properties on the Las Vegas Strip:

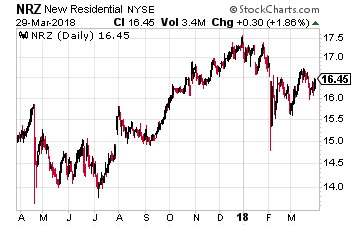

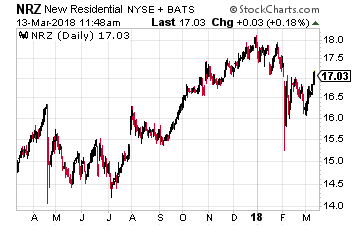

New Residential Investment Corp. (NYSE: NRZ) is a finance REIT that invests in products that are on the financial fringe of the residential mortgage industry. The largest investment is in mortgage servicing rights –MSRs. These are the contractual fees the mortgage servicing company receives out of the interest paid on a home mortgage. MSRs are typically 25 basis points (0.25%) per year. The cost to service a mortgage is typically less than 10 bp. The rest is profit to the company that owns the MSRs. New Residential owns full or excess MSRs on over half a trillion dollars of unpaid mortgage balances. 25 basis points of that much loan balance is a lot of cash flow!

New Residential Investment Corp. (NYSE: NRZ) is a finance REIT that invests in products that are on the financial fringe of the residential mortgage industry. The largest investment is in mortgage servicing rights –MSRs. These are the contractual fees the mortgage servicing company receives out of the interest paid on a home mortgage. MSRs are typically 25 basis points (0.25%) per year. The cost to service a mortgage is typically less than 10 bp. The rest is profit to the company that owns the MSRs. New Residential owns full or excess MSRs on over half a trillion dollars of unpaid mortgage balances. 25 basis points of that much loan balance is a lot of cash flow!

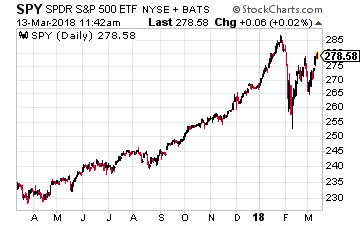

An ETF owns shares of stock to match the components of a specific stock index. For example, the SPDR S&P 500 ETF (NYSE: SPY) owns the 500 stocks in the same proportion as tracked by the Standard & Poor’s 500 stock index. The financial products industry has gone nuts with the development of new indexes to carve up the market into sectors and ETFs to track them. Currently there are over 2,000 ETFs listed in the U.S. The majority —78% of assets—of ETFs are based on stock market indexes. Those assets total over $2.4 trillion. ETF trading has become a very big part of what goes on in the stock markets.

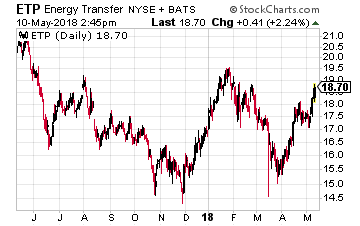

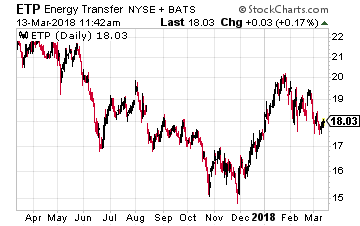

An ETF owns shares of stock to match the components of a specific stock index. For example, the SPDR S&P 500 ETF (NYSE: SPY) owns the 500 stocks in the same proportion as tracked by the Standard & Poor’s 500 stock index. The financial products industry has gone nuts with the development of new indexes to carve up the market into sectors and ETFs to track them. Currently there are over 2,000 ETFs listed in the U.S. The majority —78% of assets—of ETFs are based on stock market indexes. Those assets total over $2.4 trillion. ETF trading has become a very big part of what goes on in the stock markets. There are two ways ETF action can affect the share values of individual stocks. The most obvious and easy to discern is when the weighting of a stock in an index is changed. One high yield example is Energy Transfer Partners LP (NYSE: ETP), a large cap master limited partnership, commonly abbreviated as MLP. In April 2017 ETP completed a merger with Sunoco Logistics Partners LP, another MLP that was a large component of MLP indexes. Because of the merger, ETFs and index funds tracking MLP indexes were forced to sell significant portions of their ETP holdings to bring the size of the positions down to match the index weightings. This merger was the start of a year long decline in the ETP unit value. Later in 2017, Alerian, the provider of the most popular MLP tracking indexes, changed its methodology to cap Alerian MLP Index constituents to a 10% weight. At that time, ETP’s weight was much higher than 10% in the index, so index tracking funds were again forced to sell ETP units, regardless of investment merit. These forced sales of ETP are the source of much of the 25% value decline over the past year. The company’s fundamentals have been steadily improving, but you could not tell by the market price. ETP currently yields 12.5%.

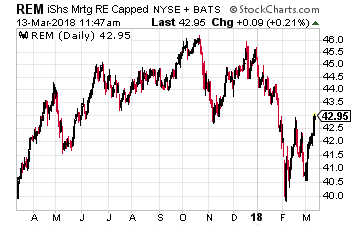

There are two ways ETF action can affect the share values of individual stocks. The most obvious and easy to discern is when the weighting of a stock in an index is changed. One high yield example is Energy Transfer Partners LP (NYSE: ETP), a large cap master limited partnership, commonly abbreviated as MLP. In April 2017 ETP completed a merger with Sunoco Logistics Partners LP, another MLP that was a large component of MLP indexes. Because of the merger, ETFs and index funds tracking MLP indexes were forced to sell significant portions of their ETP holdings to bring the size of the positions down to match the index weightings. This merger was the start of a year long decline in the ETP unit value. Later in 2017, Alerian, the provider of the most popular MLP tracking indexes, changed its methodology to cap Alerian MLP Index constituents to a 10% weight. At that time, ETP’s weight was much higher than 10% in the index, so index tracking funds were again forced to sell ETP units, regardless of investment merit. These forced sales of ETP are the source of much of the 25% value decline over the past year. The company’s fundamentals have been steadily improving, but you could not tell by the market price. ETP currently yields 12.5%. A subtler effect of the ETF boom is that trading of these funds leads to lack of discrimination between the financial results and business prospects. Stocks get lumped together into the ETFs that track specific market sectors. It is tough to figure out whether stock share prices and ETF trading are a chicken and egg dilemma, but it is becoming clearer that increases in ETF trading are tightening correlations, or the tendency for individual stocks and sectors to move up or down in lock step, regardless of a company’s fundamentals. While ETFs account for about 8% of the U.S. stock market value, ETFs are the source of more than 25% of the trading volume. Market observation clearly shows that share prices are greatly affected by short term sector switching by traders. The iShares Mortgage Real Estate ETF (NYSE: REM) provides a couple of examples. Most of the 30 or so stocks in this ETF own leveraged portfolios of residential mortgage backed securities, MBS in industry parlance. This business model is a dangerous game of lending long and borrowing short. This is a group of companies whose finances can be destroyed by a quick change in the yield curve. I recommend against owning any residential MBS focused REITs.

A subtler effect of the ETF boom is that trading of these funds leads to lack of discrimination between the financial results and business prospects. Stocks get lumped together into the ETFs that track specific market sectors. It is tough to figure out whether stock share prices and ETF trading are a chicken and egg dilemma, but it is becoming clearer that increases in ETF trading are tightening correlations, or the tendency for individual stocks and sectors to move up or down in lock step, regardless of a company’s fundamentals. While ETFs account for about 8% of the U.S. stock market value, ETFs are the source of more than 25% of the trading volume. Market observation clearly shows that share prices are greatly affected by short term sector switching by traders. The iShares Mortgage Real Estate ETF (NYSE: REM) provides a couple of examples. Most of the 30 or so stocks in this ETF own leveraged portfolios of residential mortgage backed securities, MBS in industry parlance. This business model is a dangerous game of lending long and borrowing short. This is a group of companies whose finances can be destroyed by a quick change in the yield curve. I recommend against owning any residential MBS focused REITs. In contrast, the third and fourth heavily weighted stocks in REM are solid companies with business operations that are sustainable through market cycles. In contrast to the rest of the REM portfolio stocks, these two will do even better when short term rates rise. Starwood Property Trust, Inc. (NYSE: STWD) and New Residential Investment Corp (NYSE: NRZ) are very attractive stocks with share prices that have trouble escaping from the trading in REM. STWD currently yields 9% and NRZ is over 11%.

In contrast, the third and fourth heavily weighted stocks in REM are solid companies with business operations that are sustainable through market cycles. In contrast to the rest of the REM portfolio stocks, these two will do even better when short term rates rise. Starwood Property Trust, Inc. (NYSE: STWD) and New Residential Investment Corp (NYSE: NRZ) are very attractive stocks with share prices that have trouble escaping from the trading in REM. STWD currently yields 9% and NRZ is over 11%.

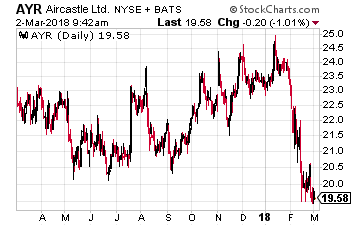

Aircastle Limited (NYSE: AYR) owns approximately 220 commercial aircraft that are leased to 81 airlines around the world. Aircastle must be nimble to adjust for changing needs for aircraft type and client airlines financial conditions. For example, in 2017, Aircastle purchased 68 aircraft and sold 37. The business is very profitable. The company generated a 15% return on equity last year and reported adjusted net income of $2.15 per share.

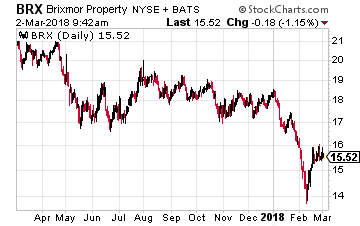

Aircastle Limited (NYSE: AYR) owns approximately 220 commercial aircraft that are leased to 81 airlines around the world. Aircastle must be nimble to adjust for changing needs for aircraft type and client airlines financial conditions. For example, in 2017, Aircastle purchased 68 aircraft and sold 37. The business is very profitable. The company generated a 15% return on equity last year and reported adjusted net income of $2.15 per share. Brixmor Property Group Inc (NYSE: BRX) is a real estate investment trust (REIT) that owns community and neighborhood strip malls. These malls are typically anchored by a grocery store and the tenants are often in businesses that are largely immune from ecommerce sales competition, or in recent terminology, “being Amazoned”.

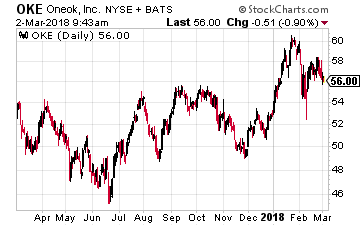

Brixmor Property Group Inc (NYSE: BRX) is a real estate investment trust (REIT) that owns community and neighborhood strip malls. These malls are typically anchored by a grocery store and the tenants are often in businesses that are largely immune from ecommerce sales competition, or in recent terminology, “being Amazoned”. ONEOK, Inc. (NYSE: OKE) is an energy sector infrastructure services company. ONEOK (pronounced “one-oak”) focuses on natural gas and natural gas liquids, also called NGLs. The company provides gas gathering services in the energy plays, facilities to process NGLs into the different components like ethane and propane, and interstate pipelines to transport natural gas and NGLs to their demand centers.

ONEOK, Inc. (NYSE: OKE) is an energy sector infrastructure services company. ONEOK (pronounced “one-oak”) focuses on natural gas and natural gas liquids, also called NGLs. The company provides gas gathering services in the energy plays, facilities to process NGLs into the different components like ethane and propane, and interstate pipelines to transport natural gas and NGLs to their demand centers.