The last six weeks have shown that trying to guess the direction of share prices is a tough way to make money in the stock market. The previous two years made it look easy to generate great profits in the market. The reality is that the stock market is much more likely to be like the last two months. If you are a long-term investor with the goal of building wealth and income to support a comfortable future, you need a plan that is not based on guessing and chasing stock prices.

Income and total return focused investors have a powerful mathematical tool that few realize exists. The math is what happens between stock yield and dividend growth. Here is how it works. If a company increases its dividend, for the stock yield to stay the same, the share price must increase by the same percentage as the percentage increase of the dividend boost. Let me demonstrate with an example.

A stock yields 5% and the dividend is increased by 5%. The new yield is then 5.25%. For the stock to stay at a 5% yield, the share price must move up by the same 5%. The result is a 5% dividend income plus a 5% share price gain for a 10% total return. In the short to intermediate term, this share price to dividend growth relationship is not apparent. Too many short term “news” items pull share prices in this direction and that. Over the long term, history shows that the average annual total returns from quality dividend growth stocks end up very close to the average yield plus the average dividend growth rate.

The relationship works through market corrections and bear markets. The dividend paying stock prices will go down with the rest of the market, but the subsequent recovery will see stock price gains sufficient to bring the relationship back to expectations. An investor can boost the mathematical total return with dividend reinvestment.

The real estate investment trust (REIT) sector is a good place to find stocks with attractive yields and companies that increase dividends every year. I maintain a REIT sector database to track yields and annual dividend increases. I use the database to screen the REIT world for a range of income focused investment strategies.

Here are five stocks that score well on the total return potential of current yield plus dividend growth. The dividend growth rate is for the last 12 months, so as an investor your task is to review each company’s results and make your own analysis whether dividend growth will continue at the same pace, accelerate or slow down.

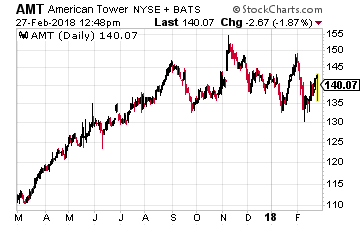

American Tower Corp (NYSE: AMT) is a large-cap REIT that develops and owns multi-tenant telecommunications real estate – cell phone towers. Over the last 12 months the company has increased its dividend by 20.7% with a dividend hike every quarter. Add the dividend growth rate to AMT’s 2.0% yield and you get 22.7% annual total return potential.

American Tower Corp (NYSE: AMT) is a large-cap REIT that develops and owns multi-tenant telecommunications real estate – cell phone towers. Over the last 12 months the company has increased its dividend by 20.7% with a dividend hike every quarter. Add the dividend growth rate to AMT’s 2.0% yield and you get 22.7% annual total return potential.

The recent dividend growth is not a fluke. Over the last five years, the company has grown the dividend by an average of 23% per year. The current yield is slightly above the average of 1.78%. The higher yield indicates that AMT may be slightly undervalued based on its market sector and dividend growth.

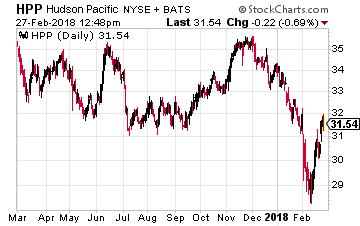

Hudson Pacific Properties Inc(NYSE:HPP) is focused on acquiring, repositioning, developing and operating office and media and entertainment properties throughout Northern and Southern California and the Pacific Northwest.

Hudson Pacific Properties Inc(NYSE:HPP) is focused on acquiring, repositioning, developing and operating office and media and entertainment properties throughout Northern and Southern California and the Pacific Northwest.

The company increased its dividend by 25% over the last 12 months. This continues the company’s record of low to mid-20% dividend growth for the last three years.

The current dividend is just 50% of FFO per share, which gives plenty of room for future dividend increases. HPP yields 3.15%, which is almost 1% above the company’s four-year average yield. This stock has strong potential for 20% plus total annual returns.

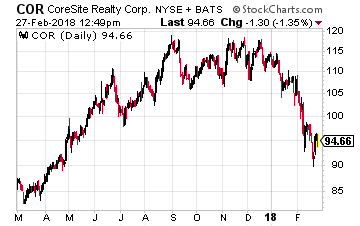

CoreSite Realty Corp (NYSE: COR) is one of the small number of data center REITs. The growth in data storage needs is truly on a parabolic trajectory. Data center REITs like CoreSite are experts at acquiring land, developing facilities appropriate for modern data storage server arrays, and providing high-speed Internet connections for companies leasing space in the data center facilities.

CoreSite Realty Corp (NYSE: COR) is one of the small number of data center REITs. The growth in data storage needs is truly on a parabolic trajectory. Data center REITs like CoreSite are experts at acquiring land, developing facilities appropriate for modern data storage server arrays, and providing high-speed Internet connections for companies leasing space in the data center facilities.

Over the last 12 months, CoreSite increased its dividend twice for a total increase of 22.5%. The tech sector needs for ever more data storage points to mid-teens or higher cash flow growth for the data center REITs for many years. COR currently yields 4.1%. Do the math on this stock’s return potential.

Related: 3 High-Yield and High Growth REITs for Value Investors

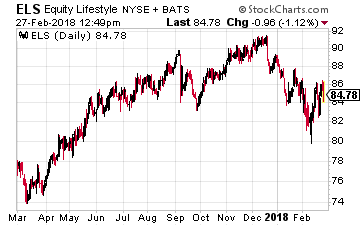

Equity Lifestyle Properties, Inc. (NYSE: ELS) is an owner and operator of lifestyle-oriented properties (properties) consisting primarily of manufactured home communities and recreational vehicle resorts and campgrounds. Equity Lifestyle owns high-end manufactured home communities located in popular retirement regions. This REIT has been a high dividend growth rate stock, growing the payout by 17% compounded per year over the last five years. The compounded growth results in dividends growing by 120% over the five-year period.

Equity Lifestyle Properties, Inc. (NYSE: ELS) is an owner and operator of lifestyle-oriented properties (properties) consisting primarily of manufactured home communities and recreational vehicle resorts and campgrounds. Equity Lifestyle owns high-end manufactured home communities located in popular retirement regions. This REIT has been a high dividend growth rate stock, growing the payout by 17% compounded per year over the last five years. The compounded growth results in dividends growing by 120% over the five-year period.

For the most recent 12 months, the ELS dividend has increased by 14.7%. The stock yields 2.27% compared to its four-year average of 2.33%. Remember for that yield to have stayed flat, the ELS share price appreciated by 15% per year.

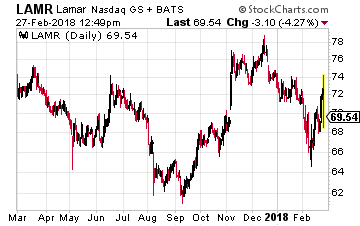

Lamar Advertising Company (Nasdaq: LAMR) owns billboard, airport, and transit advertising assets. The company converted to REIT status at the beginning of 2014. At that point Lamar started to pay regular dividends with annual dividend growth of about 10%, including a 9.6% boost last year.

Lamar Advertising Company (Nasdaq: LAMR) owns billboard, airport, and transit advertising assets. The company converted to REIT status at the beginning of 2014. At that point Lamar started to pay regular dividends with annual dividend growth of about 10%, including a 9.6% boost last year.

Compared to the stocks above, LAMR has a significantly higher yield at 5.0%. This REIT represents a different way to play the yield plus dividend growth equals total returns strategy. In the case of Lamar Advertising, the dividend growth rate is not as high, but the 5% yield is attractive cash return that can be used to compound share ownership.

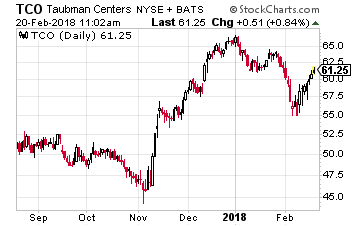

Taubman Centers, Inc. (NYSE: TCO) acquires, develops, owns and operates regional and super-regional shopping centers. The company has grown its dividend by a 6% annual compound growth rate for the last 10 years. The payout rate was boosted by 5.0% last year. Despite a challenging retail environment in 2017, the company was able to generate growth in all its key financial metrics.

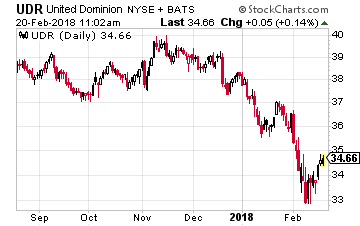

Taubman Centers, Inc. (NYSE: TCO) acquires, develops, owns and operates regional and super-regional shopping centers. The company has grown its dividend by a 6% annual compound growth rate for the last 10 years. The payout rate was boosted by 5.0% last year. Despite a challenging retail environment in 2017, the company was able to generate growth in all its key financial metrics. UDR, Inc. (NYSE: UDR) owns and operates multi-family apartment complexes. The company increased its dividend by 5.1% last year and has averaged annual dividend growth of 7.1% over the last five years. Adjusted FFO per share was up 5.5% for 2017.

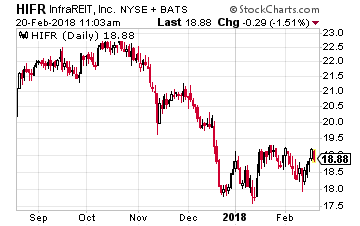

UDR, Inc. (NYSE: UDR) owns and operates multi-family apartment complexes. The company increased its dividend by 5.1% last year and has averaged annual dividend growth of 7.1% over the last five years. Adjusted FFO per share was up 5.5% for 2017. InfraREIT Inc. (NYSE: HIFR) is a REIT that owns electric power transmission and distribution assets in Texas. The company came to market with a January 2015 IPO. After its first year, the HIFR dividend was boosted by 11.1%. The dividend was not increased in 2017, even though revenues and cash flow were up in the high single digits.

InfraREIT Inc. (NYSE: HIFR) is a REIT that owns electric power transmission and distribution assets in Texas. The company came to market with a January 2015 IPO. After its first year, the HIFR dividend was boosted by 11.1%. The dividend was not increased in 2017, even though revenues and cash flow were up in the high single digits.

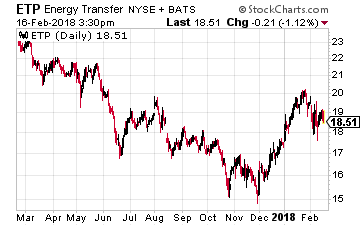

I asked Jay to discuss why he liked Energy Transfer Partners LP (NYSE: ETP) as the largest holding in the InfraCap MLP ETF (NYSE: AMZA). He discussed how ETP had become undervalued due to mechanical selling. When ETP merged with Sunoco Logistics, ETP was suddenly overweight in index tracking MLP funds. These index funds were forced to sell ETP to become balanced with the MLP indexes they are committed to mirror. Then Alerian put a 10% weighting cap on MLPs in the AMZI, and funds tracking that popular MLP index were again forced to sell ETP units to stay in line with the index weightings. The result is that Jay believes ETP with its 12% yield is very undervalued and has lots of upside potential from here.

I asked Jay to discuss why he liked Energy Transfer Partners LP (NYSE: ETP) as the largest holding in the InfraCap MLP ETF (NYSE: AMZA). He discussed how ETP had become undervalued due to mechanical selling. When ETP merged with Sunoco Logistics, ETP was suddenly overweight in index tracking MLP funds. These index funds were forced to sell ETP to become balanced with the MLP indexes they are committed to mirror. Then Alerian put a 10% weighting cap on MLPs in the AMZI, and funds tracking that popular MLP index were again forced to sell ETP units to stay in line with the index weightings. The result is that Jay believes ETP with its 12% yield is very undervalued and has lots of upside potential from here.

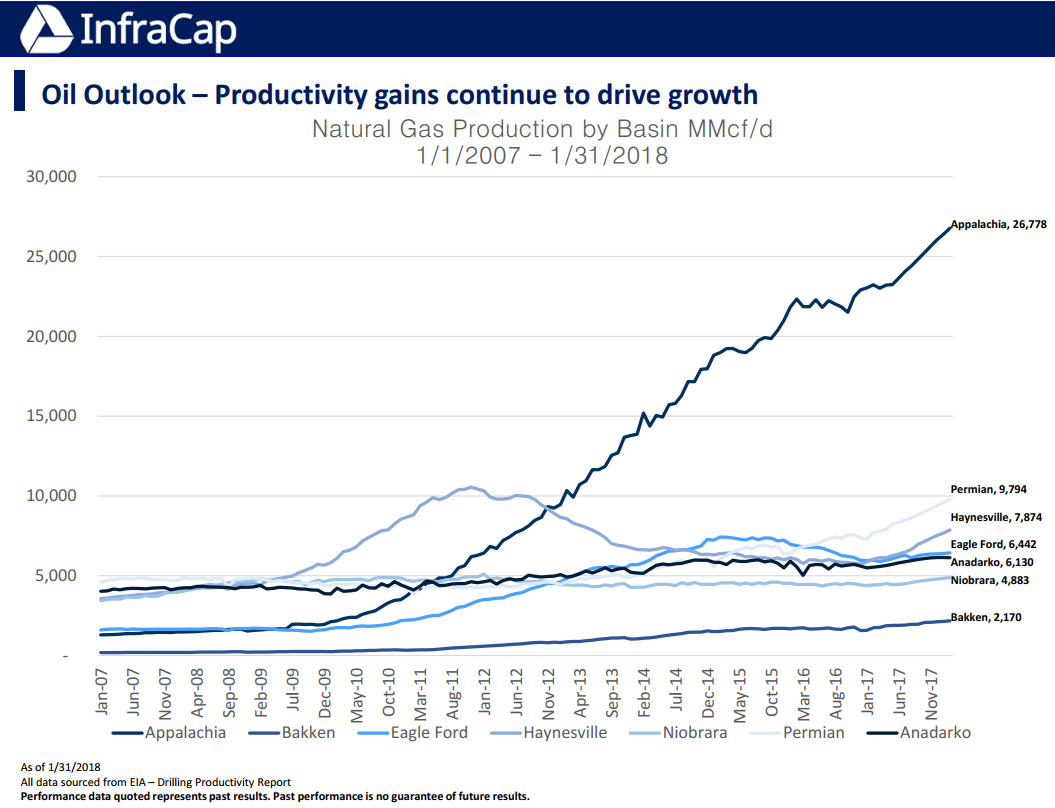

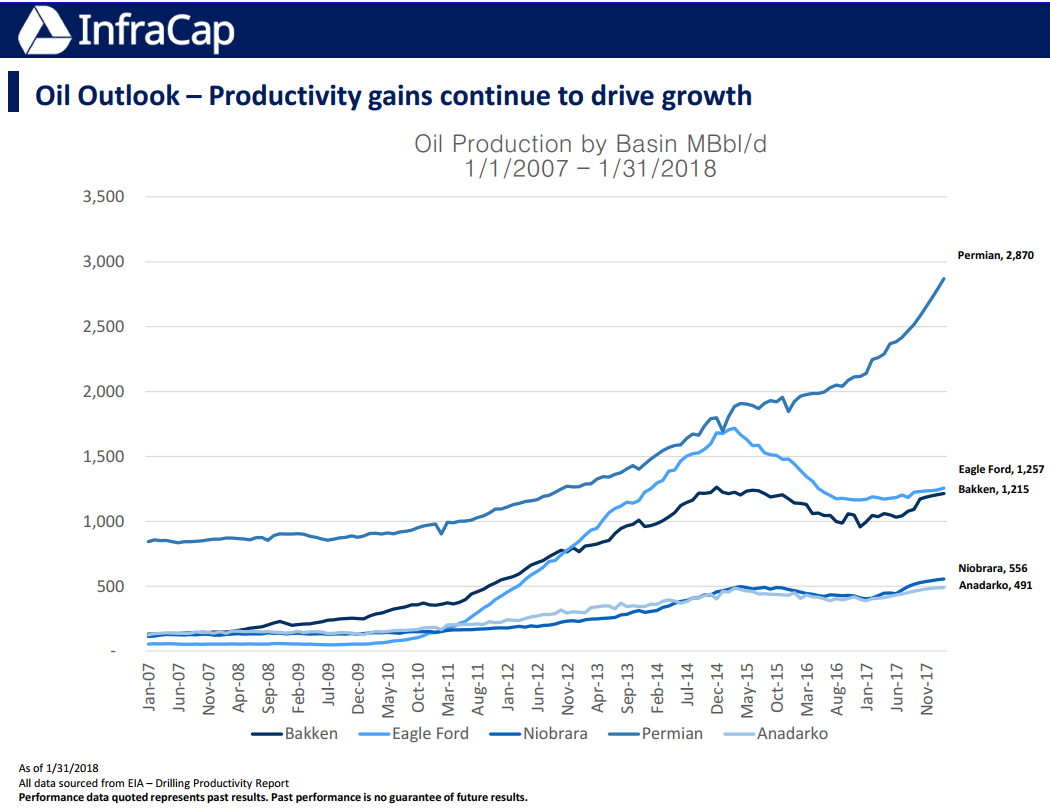

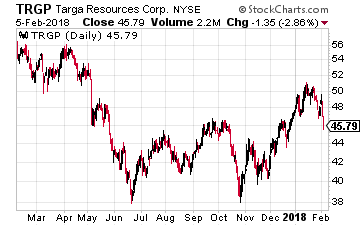

At the time of its 2010 IPO, Targa Resources Corp (NYSE: TRGP) owned the general partner interests in the midstream MLP, Targa Resources Partners LP (NYSE: NGLS). When energy prices crashed in 2015, the separate general partner and MLP business arrangement was an expense drag on the companies. In early 2016 TRGP completed the purchase of all NGLS units, which eliminated the general partner expenses. Currently Targa Resources operates four business units providing the following services:

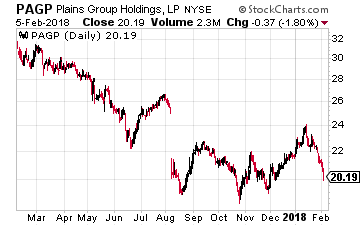

At the time of its 2010 IPO, Targa Resources Corp (NYSE: TRGP) owned the general partner interests in the midstream MLP, Targa Resources Partners LP (NYSE: NGLS). When energy prices crashed in 2015, the separate general partner and MLP business arrangement was an expense drag on the companies. In early 2016 TRGP completed the purchase of all NGLS units, which eliminated the general partner expenses. Currently Targa Resources operates four business units providing the following services: Plains GP Holdings LP (NYSE: PAGP) was also a general partner interests company, owning GP rights from large cap MLP Plains All American Pipeline, LP (NYSE: PAA). Last year, the companies restructured, eliminating the GP interests and expenses. Now each PAGP share is backed by one PAA unit. PAA is a K-1 reporting company and PAGP reports tax info on a Form 1099. In all other respects, they are shares of the same company with the same dividend rates.

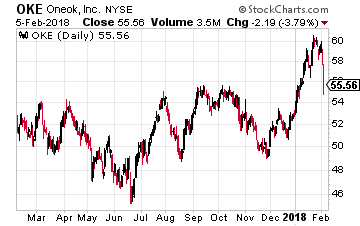

Plains GP Holdings LP (NYSE: PAGP) was also a general partner interests company, owning GP rights from large cap MLP Plains All American Pipeline, LP (NYSE: PAA). Last year, the companies restructured, eliminating the GP interests and expenses. Now each PAGP share is backed by one PAA unit. PAA is a K-1 reporting company and PAGP reports tax info on a Form 1099. In all other respects, they are shares of the same company with the same dividend rates. ONEOK, Inc. (NYSE: OKE) is another former general partner company that bought in its controlled MLP, ONEOK Partners LP. ONEOK completed the roll-up transaction in June 2017. This midstream company focuses on providing natural gas infrastructure services. Operations include a 38,000-mile integrated network of NGL and natural gas pipelines, processing plants, fractionators and storage facilities in the Mid-Continent, Williston, Permian and Rocky Mountain regions.

ONEOK, Inc. (NYSE: OKE) is another former general partner company that bought in its controlled MLP, ONEOK Partners LP. ONEOK completed the roll-up transaction in June 2017. This midstream company focuses on providing natural gas infrastructure services. Operations include a 38,000-mile integrated network of NGL and natural gas pipelines, processing plants, fractionators and storage facilities in the Mid-Continent, Williston, Permian and Rocky Mountain regions.

Simon Property Group Inc. (NYSE: SPG) is an owner of Class A and outlet center type of malls. With a $51 billion market cap, SPG is the largest publicly traded REIT. When evaluating a REIT, funds from operations (FFO) is the metric the shows dividend paying ability. For 2017, Simon reported FFO of $11.21 per share. This was up 6.4% over 2016. Management provides 2018 FFO guidance of $11.96 per share at the midpoint. If guidance is met, the cash flow per share will grow by 6.7% this year. With the 2017 fourth quarter earnings, the quarterly dividend was increased by 11.4% to $1.95 per share. The annual dividend rate of $7.80 per share is handily covered by almost $12 of FFO cash flow. This is a stock that is growing free cash flow and growing the dividend. An investor just needs to check in once a quarter to make sure the numbers are on track.

Simon Property Group Inc. (NYSE: SPG) is an owner of Class A and outlet center type of malls. With a $51 billion market cap, SPG is the largest publicly traded REIT. When evaluating a REIT, funds from operations (FFO) is the metric the shows dividend paying ability. For 2017, Simon reported FFO of $11.21 per share. This was up 6.4% over 2016. Management provides 2018 FFO guidance of $11.96 per share at the midpoint. If guidance is met, the cash flow per share will grow by 6.7% this year. With the 2017 fourth quarter earnings, the quarterly dividend was increased by 11.4% to $1.95 per share. The annual dividend rate of $7.80 per share is handily covered by almost $12 of FFO cash flow. This is a stock that is growing free cash flow and growing the dividend. An investor just needs to check in once a quarter to make sure the numbers are on track. Eastgroup Properties (NYSE: EGP) is a $3 billion market cap industrial properties REIT. For 2017 this company saw FFO increase by 6% to $4.26 per share. Industrial properties are the commercial property segment most benefitting from the shift to e-commerce retail sales. It takes three times as much warehouse space to fulfil e-commerce orders compared to traditional brick and mortar retail warehouse needs. Eastgroup increased its dividend by 3.2% in 2017 and the current dividend rate is just 59% of FFO. The company has paid dividends for 25 consecutive years, increasing the dividend in 22 of those years. This is an income stock you can count on to pay and grow the dividends. Current yield is 2.9%.

Eastgroup Properties (NYSE: EGP) is a $3 billion market cap industrial properties REIT. For 2017 this company saw FFO increase by 6% to $4.26 per share. Industrial properties are the commercial property segment most benefitting from the shift to e-commerce retail sales. It takes three times as much warehouse space to fulfil e-commerce orders compared to traditional brick and mortar retail warehouse needs. Eastgroup increased its dividend by 3.2% in 2017 and the current dividend rate is just 59% of FFO. The company has paid dividends for 25 consecutive years, increasing the dividend in 22 of those years. This is an income stock you can count on to pay and grow the dividends. Current yield is 2.9%.

Hercules Capital Inc (NYSE: HTGC) is a business development company (BDC) that makes loans in in the venture capital space. Hercules client companies are growth businesses backed by venture capital investors that need additional capital to fulfil their growth and investment goals.

Hercules Capital Inc (NYSE: HTGC) is a business development company (BDC) that makes loans in in the venture capital space. Hercules client companies are growth businesses backed by venture capital investors that need additional capital to fulfil their growth and investment goals. EPR Properties (NYSE: EPR) is a very well-run net lease REIT that has done a great job of growing the business and generating above average dividend growth for investors. With the net-lease (NNN) model, the tenants that lease the properties owned by EPR are responsible for all the operating costs like taxes, utilities and maintenance. EPR’s job is to collect the rent checks. Typically, NNN leases are long term, for 10 years or more, with built-in rent escalations.

EPR Properties (NYSE: EPR) is a very well-run net lease REIT that has done a great job of growing the business and generating above average dividend growth for investors. With the net-lease (NNN) model, the tenants that lease the properties owned by EPR are responsible for all the operating costs like taxes, utilities and maintenance. EPR’s job is to collect the rent checks. Typically, NNN leases are long term, for 10 years or more, with built-in rent escalations.