There’s one income-producing sector you probably hold in your portfolio—and you may be wondering why it’s crashing out this year.

I’m talking about utilities, which are famous for their rock-steady dividends (and predictable dividend hikes). These companies literally power the economy. But if utilities are so important, why are they in the toilet while the rest of the market is on fire?

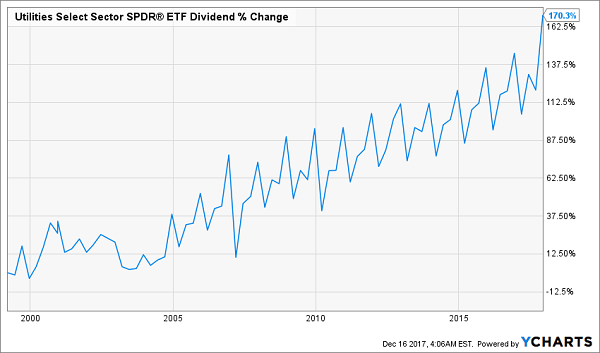

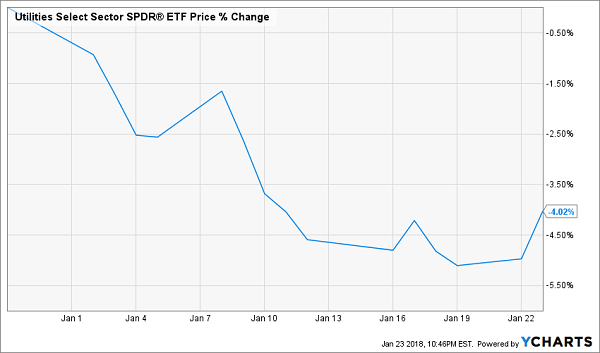

Investors Loathe Utilities

Before we go further, if you’ve noticed your portfolio’s utility sleeve taking a dive like the one above—or bigger—don’t worry. This dip is a buying opportunity! I’ll give you one option paying a fat 8.7% dividend below.

First, the big driver behind utilities’ plunge is the recovery in energy prices. Oil and natural gas are soaring after 2017’s bear market and the cold snap that kick-started this year’s commodity consumption. Higher energy costs hurt utilities’ profits, which, in turn, lowers their stock prices.

The Upside of Down

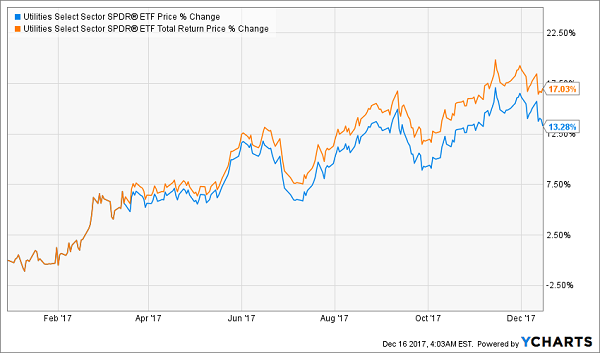

But if you’re an income seeker, this crash is an excellent opportunity to bulk up your income stream. Consider the Utilities Sector SPDR ETF (XLU), which is now yielding 3.5%, its highest level in over a year:

Utilities’ Income Rises

Let’s put some numbers behind this to understand what’s going on.

If you put $500,000 into XLU at the start of 2018, you would have gotten a $16,500 annual cash payout from the fund’s then-decent 3.3% dividend. But if you buy XLU today, you’ll get $17,350—a 5.2% raise! And that’s just because of a 0.2% increase in yield.

That is the power of dividends. And now I’m going to show you how we can kick that payout into overdrive.

Double Your Income in One Buy

There are a lot of funds out there paying a 6% dividend yield, or higher, while still investing in those same utilities XLU does. They’re called closed-end funds (if you’re not familiar with CEFs, click here for a quick and easy-to-follow primer), and they operate in an important way that supercharges their income stream.

The secret? Discounts.

When you buy $1 in XLU shares, you get $1 of XLU’s portfolio. That’s pretty straightforward. But CEFs are different: they often trade at a discount to their portfolio’s net asset value (NAV, or the market value of their holdings). And that makes their dividend yield even higher.

For instance, the Duff & Phelps Global Utility Trust (DPG) trades at an 11.5% discount to NAV—or its “true” value—which helps it cover a nice 8.7% dividend to shareholders.

Now let’s put some numbers behind this to see what we’re talking about. That $500,000 investment in XLU that paid $16,500 in annual cash dividends? Put it in DPG and suddenly you’re getting $43,450 a year. That’s a 163% raise!

Think there’s a catch? Let me put your mind at ease.

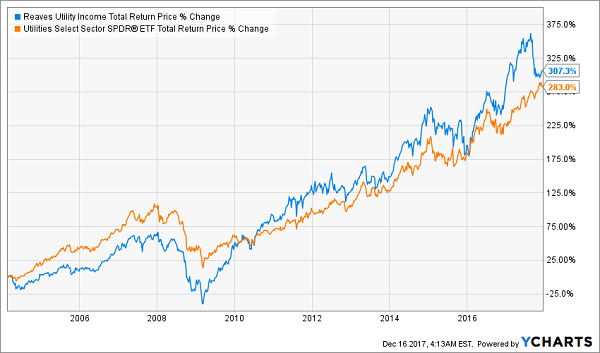

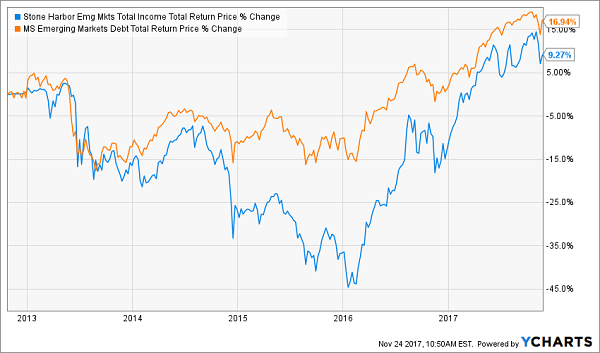

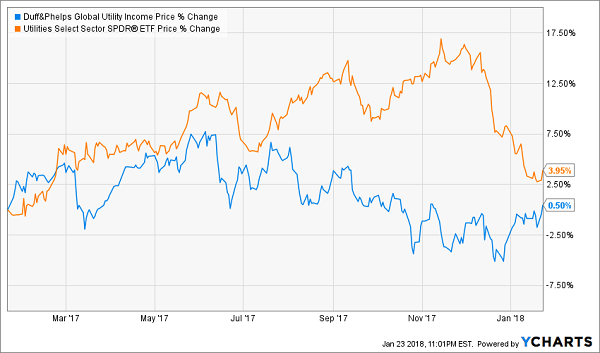

One of the first things investors do when they hear about a CEF is track its performance history. Do this with DPG, and things look bad. Let’s compare the price charts of DPG and XLU over the last year:

The Seeming Laggard

XLU is up nearly 4% while DPG is flat—a sucker’s bet, right?

Wrong.

The mistake most folks make is to look just at the price return of a fund and not the total return, including dividends. That’s because the media has trained us to obsess over the S&P 500, the Dow Jones Industrial Average and the Nasdaq 100—indexes that pay paltry dividends (you’ll get 2% on the S&P if you’re lucky). Paltry dividends don’t add much to total returns, which are the value of the dividend payouts and the price changes.

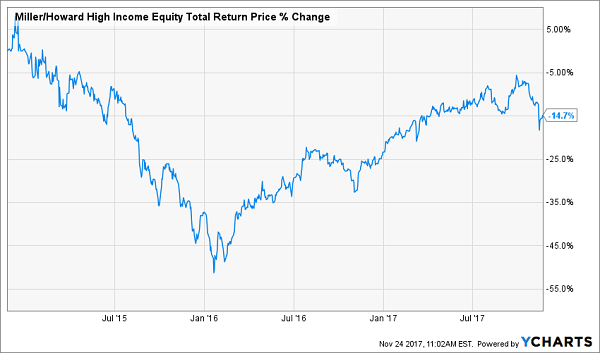

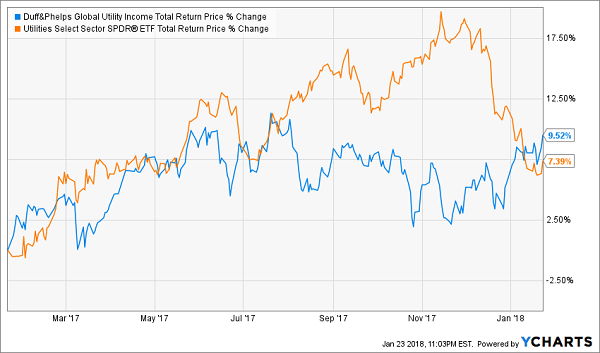

But CEFs typically yield 6% or more, so their dividends are a much more important component of their total returns. So now let’s look at a total return chart of DPG and XLU, including the dividends both funds paid out:

Laggard No More!

All of a sudden, DPG doesn’t look like a sucker’s bet anymore.

It’s a chronic problem with markets—a lot of investors do the most basic amount of research and give up. What exactly are they giving up? In this case, a 163% higher dividend, along with superior returns. If that isn’t a good enough reason to do deeper research, I don’t know what is.

So should you buy DPG now?

If you’re looking for a big income stream and you’re in it for the long haul, DPG is a good option. There are others, though. Some utility CEFs have bigger yields, and some have much better long-term returns than DPG. A basket of these funds, bought when their discounts are most attractive and their portfolios best positioned to guarantee their dividends, is ideal for most investors.

But, of course, as you’re shopping around for the right CEF, do make sure you look at total returns.

4 Better Buys Than DPG (Incredible Cash Payouts Up to 10.4%)

And I haven’t gotten to your best option yet: let me do the legwork for you.

In fact, I’ve already done it! And today I’m pounding the table on 4 bargain CEFs that hand you an average yield of 8.1% and even bigger upside (I’m talking gains of 20%+ here) than you’ll get from DPG in 2018.

One of these little-known picks hands you an astounding 10.0% payout and I expect it to be one of my biggest gainers in 2018, thanks to its massive discount to NAV. Just imagine banking an income stream like that while you watch your nest egg streak higher.

Editor's Note: The stock market is way up – and that’s terrible news for us dividend investors. Yields haven’t been this low in decades! But there are still plenty of great opportunities to secure meaningful income if you know where to look. Brett Owens' latest report reveals how you can easily (and safely) rake in 8%+ dividends and never worry about drawing down your capital again. Click here for full details!

Source: Contrarian Outlook

Hercules Capital Inc (NYSE: HTGC) is a business development company (BDC) that makes loans in in the venture capital space. Hercules client companies are growth businesses backed by venture capital investors that need additional capital to fulfil their growth and investment goals.

Hercules Capital Inc (NYSE: HTGC) is a business development company (BDC) that makes loans in in the venture capital space. Hercules client companies are growth businesses backed by venture capital investors that need additional capital to fulfil their growth and investment goals. EPR Properties (NYSE: EPR) is a very well-run net lease REIT that has done a great job of growing the business and generating above average dividend growth for investors. With the net-lease (NNN) model, the tenants that lease the properties owned by EPR are responsible for all the operating costs like taxes, utilities and maintenance. EPR’s job is to collect the rent checks. Typically, NNN leases are long term, for 10 years or more, with built-in rent escalations.

EPR Properties (NYSE: EPR) is a very well-run net lease REIT that has done a great job of growing the business and generating above average dividend growth for investors. With the net-lease (NNN) model, the tenants that lease the properties owned by EPR are responsible for all the operating costs like taxes, utilities and maintenance. EPR’s job is to collect the rent checks. Typically, NNN leases are long term, for 10 years or more, with built-in rent escalations.