I like to look for what are called contrarian investments. That is, trades where Wall Street is piled into one side of the ‘boat’. When this happens, the ‘boat’ has a tendency to ‘capsize’ turning into very large profits for taking the opposite side of the trade that Wall Street is on.

There are several of these trades going on right now including shorting U.S. Treasuries, being long the U.S. dollar, being short commodities, and also shorting overseas markets and using the proceeds to go even longer with even more leverage in the U.S. on favorites like the FANG stocks.

The reason for the latter trade is that Wall Street’s perception is that the tariffs imposed on foreign products will hurt those economies even though history says just the opposite – that the country imposing the tariffs is hurt the most. So what I have done in my personal account is scour the globe for companies that are actually benefiting or may gain from the tariffs imposed by the Administration.

Don’t Ignore ADRs

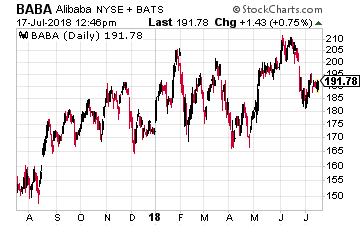

This really isn’t hard, with many of these type of companies trading right here in the U.S. in the form of American Depository Receipts or ADRs. Some of these are large, well-known companies such as Alibaba (NYSE: BABA). Here is a quick overview of ADRs.

ADRs can be sponsored or unsponsored and have three different levels, depending upon foreign companies’ access to US markets, as well as disclosure and compliance requirements. Level 1 ADRs cannot be used to raise capital and are only traded on the over-the-counter market. Level 2 and Level 3 ADRs are both listed on an established U.S. stock exchange, with Level 3 ADRs having the ability to be used to raise capital.

Most ADRs that trade over-the-counter as easy to spot since the last letter of the five letters in their symbol is always a Y. For instance, the food giant Nestle symbol is NSRGY and China’s internet and gaming powerhouse Tencent symbol is TCEHY.

However, the number of ADRs listed in the U.S. has shrunk drastically in recent years. The reason for that lies in the cost of compliance with among other regulations, Sarbanes-Oxley. It is just not cost-effective for companies to spend millions of dollars to comply and then see little daily trading in their ADR thanks to lack of interest in foreign firms by U.S. investors (home bias).

If you do stick with ADRs, the commissions charged you by brokerage firms, such as Charles Schwab, is the same as for U.S. companies – $4.95.

And if you’re worried about the accounting standards at foreign companies, don’t be. Listed foreign companies follow international accounting standards as set by the IFRS. There are differences between IFRS (International Financial Reporting Standards) and GAAP (Generally Accepted Accounting Principles) standards here in the U.S. But that would be a long, boring discussion we don’t have the time to get into.

Suffice it to say that IFRS standards are very good and better than the pro forma earnings numbers often reported here in the U.S., which I consider to be trash. As Warren Buffett has often pointed out, pro forma earnings often leave out real expenses, such as stock compensation.

Convergence between IFRS and GAAP standards have been a topic of discussion at the SEC and other governmental agencies for years. But interestingly, U.S. officials seems to dragging their feet. Maybe it’s because the U.S. doesn’t always have the highest standards for corporations.

Take AliBaba (NYSE: BABA), for example. It listed here in the U.S. and not in Hong Kong because the corporate governance rules were less strict here in the U.S. The Hong Kong Exchange frowned upon the company wanting to nominate the majority of the board itself. Although now there is talk Hong Kong will adopt the lower U.S. standards.

Now let me move on and bring you three ADRs I found that are either benefiting from the tariffs or are unaffected. Keep in mind that these are major companies in their home markets that trade millions of shares a day there.

Soybeans Anyone?

One of most prominent retaliations taken against the U.S. was China’s tariffs on U.S. farm products such as soybeans. That immediately make me think of another big agricultural economy that China already bought a lot of products from – Brazil.

One of the largest agricultural companies in Brazil is a company named SLC Agricola SA that does have an ADR with the symbol SLCJY. The ADR is liquid enough for individual investors (I do own it) with trading volume of about 15,000 a day.

The company, founded in 1977, has an English website slcagricola, so it’s easy to get information on it. The company has 16 production sites located in six Brazilian states totaling 404,479 hectares during the 2017/18 crop season. The acreage breakdown is: 230,164 of soybeans, 95,124 of cotton, 76,839 of corn and 2,352 of other crops, such as wheat, corn 1st crop, corn seed and sugarcane.

The ADR has taken off in recent months and is now up 100% year-to-date and 140% over the past year. I’m sure many Brazilian farmers, as well as Agricola shareholders, are thankful tariffs were imposed.

Germany’s Square

Another favorite target seems to be Germany, so I looked to see what I could find there. And I came up with a global leader in the payments space, a company named Wirecard AG that has an ADR with the symbol WCAGY. Its ADR also has decent liquidity with about 10,000 shares traded daily even though it only became available in late 2016.

Wirecard is one of the fastest growing financial commerce platform that services 36,000 large- and medium-sized merchants and 191,000 small-sized merchants. It had over $106 billion in processed transaction volume worldwide in fiscal year 2017.

The company works together with ApplePay in many European countries. And it bought Citibank’s prepaid card services in North America as well as its merchant acquiring business in the Asia-Pacific region.

Due to its strong organic growth in excess of 25%, management raised its guidance in April for the 2018 fiscal year from 510 million to 535 million euros up to 520 million to 545 million euros. This has not been lost on investors. . . . .

Its ADR is up 60% year-to-date and has soared more than 143% over the past year.

It’s Not Made Here

The final ADR is one that is thinly traded (only a few hundred shares daily). But I wanted to bring it your attention because it makes something that is NOT made in the U.S. meaning that barriers or not, it is an absolute necessity for some firms. Let me explain. . . . .

If you’re having trouble finding some electronic devices, such as a Sony Playstation 4, it is likely due to the ongoing global shortage of MLCCs, or multilayer ceramic capacitors. You may never see these capacitors, which are less than one millimeter on each side. But they are a crucial component of your smartphone as well as your car. They help control the flow of electricity and store power for semiconductors, without which no electronic device will function.

The market for MLCCs is dominated by Asian manufacturers with just three companies controlling 60% of the market – Korea’s Samsung Electro-Mechanics and two Japanese firms, Murata Manufacturing and Taiyo Yuden. Both Japanese companies have ADRs trading in the U.S. with the symbols MRAAY and TYOYY respectively.

Murata has more liquidity, with over 18,000 shares traded daily versus just a few hundred shares. But Taiyo Yuden is by far the better performer. Even before the shortage occurred, Taiyo Yuden saw its sales of capacitors increase by over 21% in its last fiscal year.

That helped send its stock skyward. Its ADR is up 87% over the past year, with most of the performance occurring this year – up 82.5% year-to-date – as the realities of a global shortage of MLCCs have set in.

There you have it – just three of the overseas companies that either are benefiting or will be unaffected by tariffs. There are plenty more too, so please do not be afraid to put a little bit of your portfolio into stocks outside the U.S.

Buffett just went all-in on THIS new asset. Will you? Buffett could see this new asset run 2,524% in 2018. And he's not the only one... Mark Cuban says "it's the most exciting thing I've ever seen." Mark Zuckerberg threw down $19 billion to get a piece... Bill Gates wagered $26 billion trying to control it... What is it? It's not gold, crypto or any mainstream investment. But these mega-billionaires have bet the farm it's about to be the most valuable asset on Earth. Wall Street and the financial media have no clue what's about to happen...And if you act fast, you could earn as much as 2,524% before the year is up. Click here to find out what it is.

The S&P 500 is an index containing the largest stocks in the country. Investors use it to gauge how stocks are doing overall, as it serves as a snapshot for the U.S. equities market. Generally speaking, the index is also used as a benchmark, as everyone from retail investors to hedge fund managers compare their performance to it.

With that being said, there are a lot of names in the S&P 500 that investors don’t want to own, simply because they are not performing well. Do you know how unlikely it is to consistently get 500 winners?

In that regard, let’s take a look at how investors can use key stocks held in the S&P 500 to build a winning portfolio over the long term.

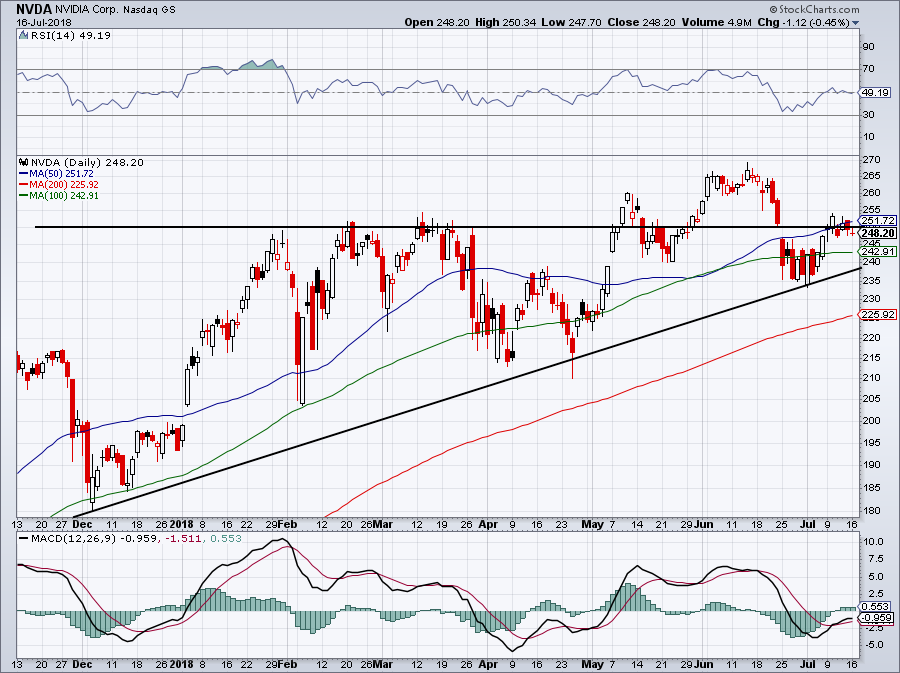

Top S&P 500 Stocks to Own: Nvidia (NVDA)

Perhaps Nvidia (NASDAQ:NVDA) is too obvious a stock to name here. But given its large rally over the past year, many investors feel like they’ve missed the boat.

Admittedly, Nvidia stock has rallied impressively over the past few years, up 53%, 379% and 1,157% over the past 12, 24 and 36 months, respectively. While another 1,000% rally in the next few years is likely out of the cards, there could still be substantial upside in Nvidia. For instance, the stock reaching over $300 in the next six to 12 months isn’t out of the question.

The company has positioned itself as a market leader in a number of secular end markets. Nvidia’s work in artificial intelligence (along with its numerous subcategories like deep learning and machine learning), in gaming chips and in the datacenter is all very impressive. Finally, it would come as a shock if Nvidia wasn’t the biggest winner from the autonomous driving race. While automotive revenue isn’t clocking in with massive growth right now, the self-driving industry is still in the very early innings. As it gains tractions, Nvidia’s DRIVE platforms will play a massive role in the industry.

While Nvidia may trade at 14 times sales, keep in mind it has far better margins than Advanced Micro Devices (NASDAQ:AMD) or Intel Corporation (NASDAQ:INTC). On an earnings basis though, Nvidia’s valuation is much more reasonable. At just 34 times this year’s earnings, that’s not much of a premium for a big-time grower like NVDA.

Analysts expect 34% sales growth this year and 50% earnings growth. While those numbers slow significantly in 2019, my guess is that they’re too conservative. Nvidia hasn’t just topped earnings estimates over the last few years — it has crushed every quarter. Its story isn’t done yet.

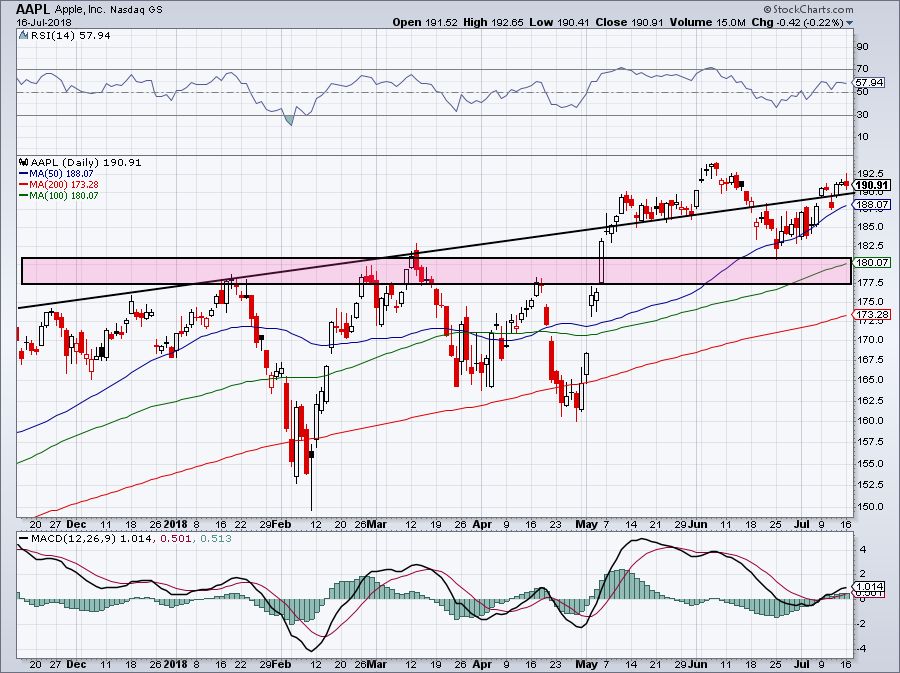

Top S&P 500 Stocks to Own: Apple (AAPL)

Apple (NASDAQ:AAPL) isn’t very controversial, but it needs to be included.

It’s the largest company in the S&P 500 and for good reason. Apple’s products and brand have made it so millions of customers around the world don’t even consider owning a competing brand. So long as it continues to make a sticky ecosystem, business should continue to do well.

Having a $100 billion buyback shows just how strong those cash flows are each quarter. Impressively, this follows previous buyback plans that ran into the tens of billions as well. More than likely, it comes ahead of many more billions being plowed into future share repurchases. Warren Buffett has made Apple the largest position in his Berkshire Hathaway (NYSE:BRK.A, NYSE:BRK.B) holdings as well.

Apple also pays out a decent dividend, yielding 1.5%.

While shares are near the highs and as its market cap gravitates toward $1 trillion, it’s still one investors should have on their radar. Perhaps use a market-wide correction to initiate a new position.

At 18.5 times this year’s earnings, Apple stock is reasonably priced given its size and status. It’s also reasonable given its growth, even though on its own historical averages, it’s not exactly cheap. Analysts expect sales to grow 14% this year and 4% in 2019. On the earnings front, estimates call for 25% growth this year and 15% growth next year.

Don’t forget about the company’s budding services revenue, which could be a standalone company at this point. Last quarter its $9.2 billion in sales grew 31% year-over-year and came in vastly ahead of analysts’ expectations of $8.4 billion. If that momentum continues, it will help drive AAPL stock higher.

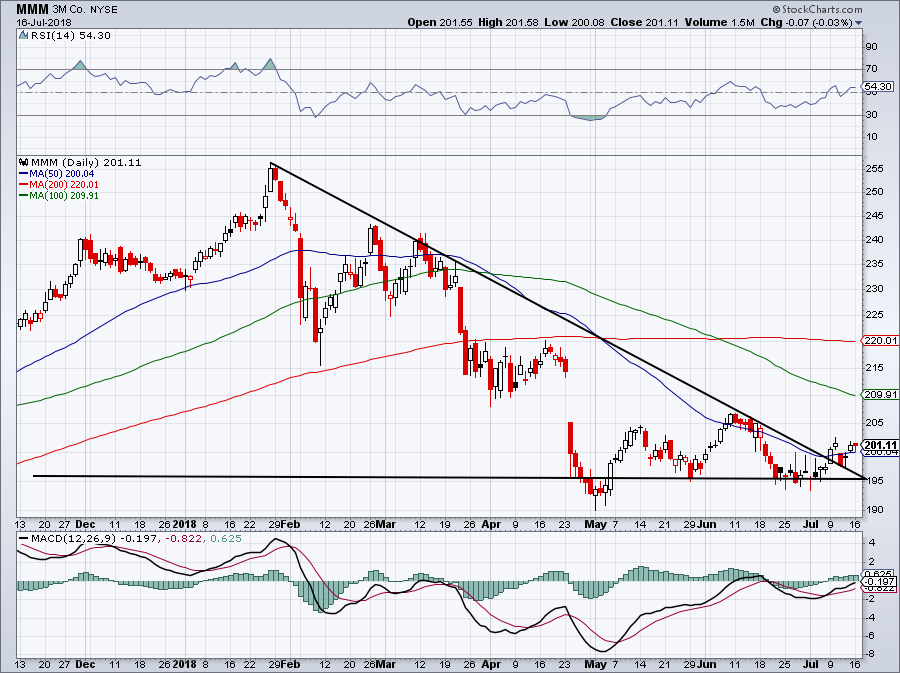

Top S&P 500 Stocks to Own: 3M (MMM)

3M (NYSE:MMM) hasn’t had the easiest time lately. But I think its business, chart and dividend make it one that certain investors should consider.

For starters, 3M made our list of best dividend stocks just this week. The company has not only paid out a dividend for a whopping 60 years, but it’s also raised its dividend every year for six decades. For income investors, there’s not much more you can ask for in terms of consistency. (The top dividend-payer only has three more years than 3M).

As for its business, estimates call for 5.7% sales growth this year and 3.5% next year. That goes along with 13% earnings growth in 2018 and 9% in 2019. For this, investors are paying about 18 times earnings.

Some will point out that they can buy Apple for a lower valuation with better growth and that’s true. 3M isn’t for all investors. But a look at the charts tells us we have a solid risk/reward opportunity here. Should MMM stay above downtrend resistance near $200, it could mean shares have finally bottomed.

This $190 to $195 area has clearly been support. If 3M can gain some upside traction, it could be attractive going into the second half of the year. Keep in mind, this stock topped out over $250 earlier this year.

Top S&P 500 Stocks to Own: General Motors (GM)

General Motors (NYSE:GM) may not be a name many would have expected, but the automaker doesn’t seem to get enough credit. With a dividend yield of nearly 4% and trading at 6.2 times next year’s earnings, GM stock is at least one to take a deeper look at.

Admittedly, the automaker does not boast great growth. Analysts expect revenue to grow just 40 basis points this year and 50 basis points next year. On the earnings front, they expect a 3% decline in 2018 and a 0.5% gain in 2019. I find that the expectations for a 3% decline may be a bit aggressive, but either way even if GM reports flat growth, it’s still rather unremarkable.

The stock recently ran from $37 to $45 in just a few days time. That was after SoftBank(OTCMKTS:SFTBY) took a near-20% stake in Cruise Automation, a company that GM bought for roughly $1 billion two years ago.

Based on the deal, that gave an $11.5 billion valuation to Cruise. In other words, GM owns a majority stake in what is now a highly valued asset. Buy low, right? However, despite GM rallying significantly after the SoftBank deal was announced, it’s now falling back down to $39.

That could give investors a great opportunity to get long the automaker at a low valuation and collect a big dividend while they wait. GM can be a big player in the autonomous driving movement, with RBS analysts predicting that it could become a $43 billion enterprise for GM by 2030.

It’s also worth noting is that GM currently has a market cap of $56 billion.

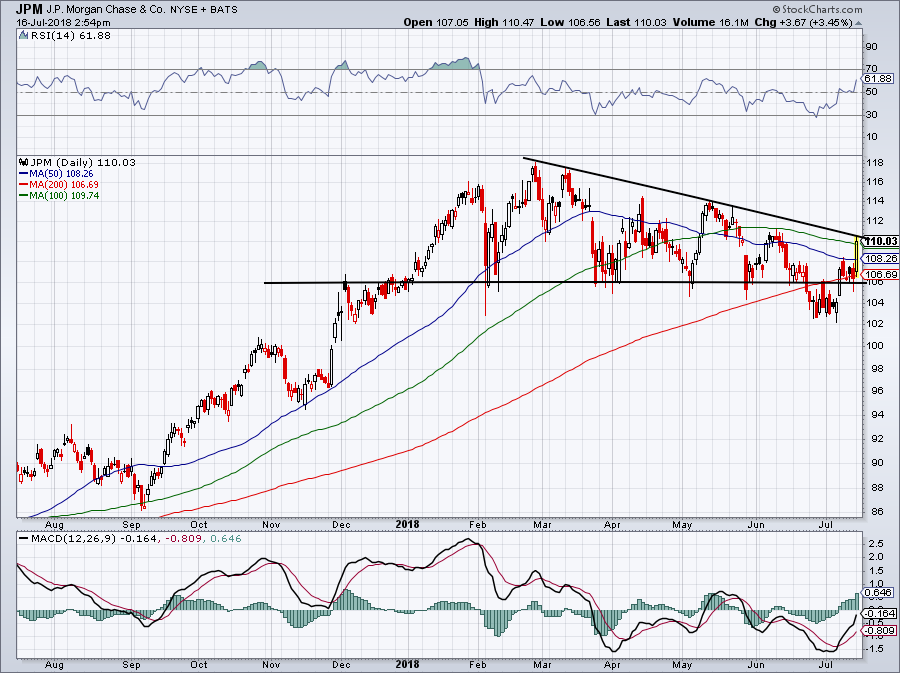

Top S&P 500 Stocks to Own: JPMorgan (JPM)

JPMorgan Chase (NYSE:JPM) beat on earnings and revenue estimates last Friday. Before that, the bank passed its Fed stress tests and gave a big boost to its capital return plans.

The bank is boosting its quarterly payout to 80 cents a share, up from 56 cents per share before the stress test results. In other words, JPM gave a 43% boost to its dividend and now yields about 2.9% annually. The bank can also buy back almost $21 billion over the next 12 months.

Even better, JPM’s valuation and growth profiles are attractive.

Analysts expect revenue to grow 7% this year and another 4% next year. On the earnings front though, estimates call for around 30% growth this year and another 8% growth in 2019. Given that JPM trades at just 16 times this year’s earnings, it makes it mighty attractive.

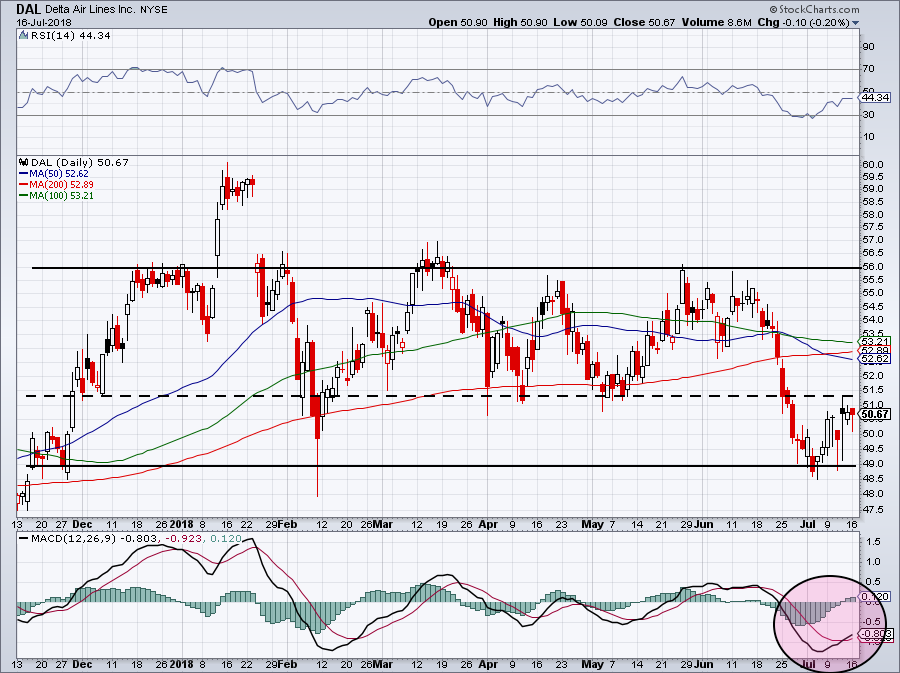

Top S&P 500 Stocks to Own: Delta (DAL)

We recently took a closer look at four airline stocks investors might want to buy. Like Apple, the four largest U.S. airline stocks are all owned by investing legend Warren Buffett. Their low valuation, strong cash flow generation and capital return make them attractive. Plus, air travel is becoming more popular than ever.

One to consider from the group is Delta Air Lines (NYSE:DAL). Check out this piece to see our simple table comparing all four names.

While Delta didn’t lead any specific category other than dividend yield, it scored high enough in each measure to be considered one of the best. The company boasts respectable revenue growth and double-digit earnings growth this year and next year.

Paying out a 2.7% dividend yield now, buying back plenty of stock and trading at less than 16 times this year’s earnings makes it too attractive to keep off the list. Unlike some other airline stocks, DAL stock is holding support too.

Now, it just needs to get through $51 and then a 10% rally is in the cards.

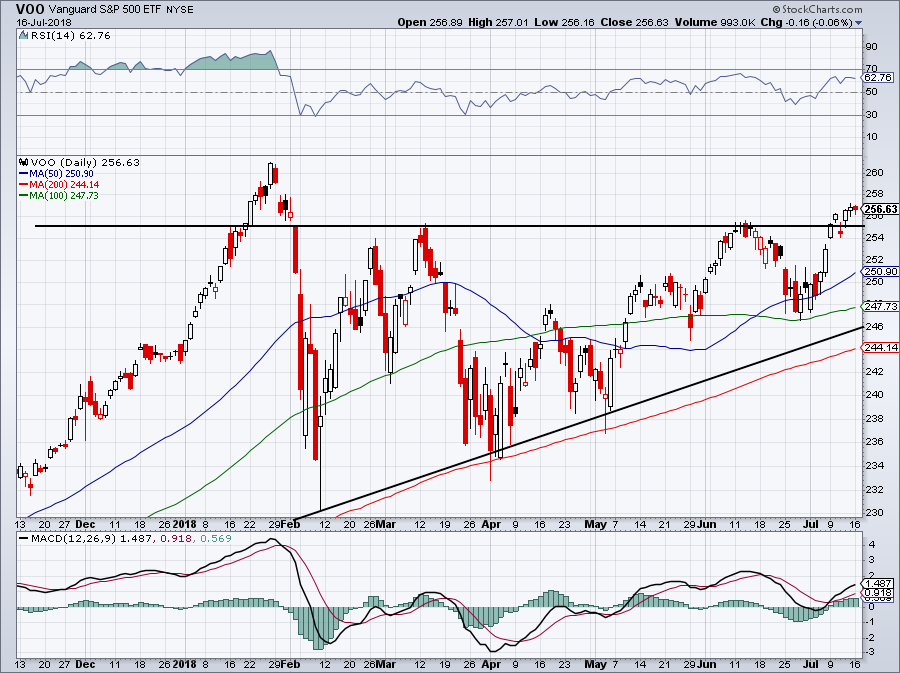

Top S&P 500 Stocks to Own: Vanguard S&P 500 (VOO)

I don’t want investors to mistake this article for a Warren Buffett rah-rah piece. But despite his humble approach, it’d be insulting to consider him anything less than an investing king at this point. Whether it has been his investments from three decades ago or how he stepped into the banks during the Great Recession, he will be remembered for eternity. (Well, probably).

In any regard, his top advice for individual investors is to invest in low-cost index funds for the S&P 500. When held over very long stretches, these investments have worked out wonderfully for investors. Throw in the low fees and the returns are better than most individual investors can muster on their own. For instance, the Vanguard S&P 500 ETF (NYSEARCA:VOO) is up 14% over the past year and 32% over the past three years.

While there’s a lot of stocks that have outperformed that and many on this list have done so, there are also plenty of duds that haven’t.

It doesn’t have to be an “either-or” situation though. Investors can use something like the VOO for a core position and, say, a few names on this list to build around it. That way they have the best of both worlds.

Get up to 14 dividend paychecks per month from safe, reliable stocks with The Monthly Dividend Paycheck Calendar, an easy-to-use system that shows you which dividend stocks to pick, when to buy them, when you get paid your dividends, and how much. All you have to do is buy the stocks you like and tell them where to send your dividend payments. For more information Click Here.

There has been no company like Amazon.com (Nasdaq: AMZN) ever with the ability to affect entire industries just by announcing its entry.

The most recent example of this was in late June when Amazon announced a roughly $1 billion acquisition of PillPack, a mail-order pharmacy that packages pills into daily portions before shipping them to patients in 49 states.

PillPack was backed by several well-known investors including Silicon Valley venture capital firms Accel and Menlo Ventures. Its target market is people with chronic illnesses or multiple conditions who take several different tablets every day, rather than people who take a single medication or use prescription drugs only occasionally.

Amazon already captures more than $4 out of every $10 spent online in the U.S. So in response to its PillPack announcement, about $14 billion magically disappeared from the stock market valuations of the biggest players in the U.S. drug distribution and retailing. Shares in those six companies – WalgreensBootsAlliance (Nasdaq: WBA), CVSHealth (NYSE:CVS), ExpressScripts Holding (Nasdaq: ESRX), CardinalHealth (NYSE: CAH), McKesson (NYSE: MCK) and AmerisourceBergen (NYSE: ABC) had already been depressed last year when Amazon hinted that it was coming into their territory. Proof positive trimmed their values by as much as 10%.

Already the fear of Amazon’s entry into the sector had started a frenzy of consolidation in the sector including CVS agreeing to acquire health insurer Aetna for $69 billion in December, and in March Cigna, a rival health insurer, agreed to pay $67 billion for the aforementioned Express Scripts, a pharmacy benefits manager that also delivers medication by mail.

Amazon’s Long Game

There is one characteristic I’ve always liked about Jeff Bezos and Amazon – its planning for the long-term. This is so unlike most U.S. companies that are focused on the very short-term.

The PillPack purchase looks like a crucial part of a strategy that Amazon has been slowly building brick by brick, and likely just one step of many in the sector it has long eyed.

Its interest goes back to 1999 when it bought a minority stake in Drugstore.com, but never fully integrated it into its core retail offering. Walgreens later bought the website and eventually shut it down in 2016. More recently, Amazon has pursued pharmacy licenses in several US states, held meetings with healthcare industry executives and made several senior hires from insurers and pharmacy benefits managers. And of course, it also recently joined with JPMorgan Chase and Berkshire Hathaway to create a not-for-profit healthcare company that aims to reduce bills for their employees and “potentially all Americans”.

In buying PillPack, Amazon is sticking with the same game plan it is following in the grocery business and its Whole Foods purchase. That is, acquire a company with an existing footprint in a market rather than trying to build a brand new business within its existing retail network. With this purchase, Amazon buys regulatory permits and contracts with health insurers.

While mail order deliveries represent a small proportion of the overall prescription market, it is seen as a source of growth due to demographics – an aging U.S. population will require higher levels of medical care in coming years.

The acquisition should create another competitive advantage for Amazon over others in the space thanks to its extensive logistics network and loyal customer base to its Prime subscription (with 100 million subscribers) delivery service. Amazon may bundle its prescriptions with other products where people make regular, frequent purchases, such as groceries. That could help attract even more Prime subscribers, who spend more and order more frequently from Amazon than non-Prime customers.

But it will not be an easy road for Amazon. That’s because the trend in the pharmacy business is going in the opposite direction of other retail businesses. Last year, about 88% of prescriptions filled were collected at brick-and-mortar pharmacies. That compares to 82% in 2009, according to Goldman Sachs.

As to why this is happening, it’s simple. . .existing mail-order pharmacies stink. For example, with Express Scripts it can take eight days to have a prescription filled and up to two weeks for a new prescription to be filled. Obviously, Amazon is hoping its strength in logistics will shorten those times greatly.

But its logistics won’t help with another problem – about 30% of prescriptions result in a “pharmacy callback”. That is when the medicine prescribed to a patient is not covered by their insurance and the pharmacy then has to contact the doctor’s office to see if a cheaper alternative is acceptable. Perhaps that is why Amazon is pursuing the insurance angle with JPMorgan and Berkshire Hathaway.

Investment Implications

This move into the drugstore space looks to be another win for Amazon. And a loss for the drug distributors and especially the retail drugstores. After all, Amazon is already undercutting them on the prices for non-prescription medicines.

According to Jeffries Group, median prices for over-the-counter, private-brand medicine sold by Walgreens Boots Alliance and CVS Health were about 20% higher than Basic Care, the over-the-counter drug line sold exclusively by Amazon. Amazon began selling the Basic Care line last August with roughly 35 products and has since expanded its range to 65 medicines including mild painkillers, cold and flu medication, sleeping aids and other medication commonly found in the pharmacy aisle. Many of these meds are available through Amazon Prime.

Take all of these moves by Amazon into the distribution of medicines and you have one more reason to sell the drug retailers or, if you’re an aggressive trader, short them.

Buffett just went all-in on THIS new asset. Will you? Buffett could see this new asset run 2,524% in 2018. And he's not the only one... Mark Cuban says "it's the most exciting thing I've ever seen." Mark Zuckerberg threw down $19 billion to get a piece... Bill Gates wagered $26 billion trying to control it... What is it? It's not gold, crypto or any mainstream investment. But these mega-billionaires have bet the farm it's about to be the most valuable asset on Earth. Wall Street and the financial media have no clue what's about to happen...And if you act fast, you could earn as much as 2,524% before the year is up. Click here to find out what it is.

M&A activity has been big part of the global market for the past few years now, and that’s likely to continue. Tax reform has freed up more cash and made potential targets more accretive. The economy is humming along. And in a few key sectors — consumer goods and media come to mind — there’s an obvious logic behind consolidation.

The old rules still apply as well. Older companies are looking to drive scale and cut costs. Newer companies are looking to expand their reach — or cash out by selling to one of those older companies looking to spark growth of their own.

With U.S. mergers actually down in 2017 — perhaps due to tax uncertainty — there’s some pent-up demand as well. And so this might be exactly the type of market to look for takeover stocks. These 18 stocks all have been rumored or reported targets. And in many (though not necessarily all) cases, the possibility of an acquisition doesn’t necessarily look priced in.

Takeover Stocks: BlackBerry (BB)

Source: Shutterstock

On this site late last year, Larry Ramer argued that BlackBerry (NYSE:BB) was a prime takeover target. Ramer isn’t alone in that argument. Noted short-seller Citron Research made a similar claim last year in arguing that BB stock had the potential to double.

Rumors of potential acquirers have swirled for some time. BlackBerry of course almost went private back in 2013 at $9-per-share. Two years later, the company reportedly was in talks with Samsung about an acquisition.

There’s still a logical takeover case for BlackBerry at the moment. The phone business is gone, leaving an attractive software business. The QNX operating system has a real role to play in ensuring security for autonomous driving. BlackBerry’s patents have real value, with potential upside from a filed suit against Facebook (NASDAQ:FB). And with over $2 billion in cash on the books, another go-private transaction could work as well.

BB stock, meanwhile, has pulled back below $10 despite a Q1 earnings beat. Investors are worried that the company’s turnaround simply isn’t progressing fast enough (indeed, I’ve made that argument myself). But with real value in the software and the nameplate, it simply may be that the turnaround could be better executed under different ownership.

Takeover Stocks: Lions Gate Entertainment (LGF.A, LGF.B)

Source: Shutterstock

The acquisition of Time Warner by AT&T (NYSE:T) has led to an belief that consolidation is coming in the media space. As James Brumley wrote last month:

“…the previous lines between media distribution, media creation, and content licensing have been completely wiped away. This is just the beginning of a heated M&A race, with all players knowing once-unthinkable partnerships are now going to be permitted.”

And so the owners of content look like attractive targets, and Lions Gate Entertainment (NYSE:LGF.A, NYSE:LGF.B) is high on the list. As Will Healy argued last month, its ownership of Starz, films such as The Hunger Games and TV programs, including Mad Menand Will & Graceall make Lions Gate an intriguing target for larger distributors.

LGF earnings have struggled a bit, and so has LGF stock. Analysts have abandoned the story of late. And investors likely will need a bit of patience. It seems likely that consolidation, if it comes, won’t kick into full gear until the drama between Comcast (NASDAQ:CMCSA), Disney (NYSE:DIS) and Twenty-First Century Fo (NASDAQ:FOX, NASDAQ:FOXA) has completed. But for investors who believe that consolidation is inevitable, LGF’s lower valuation and content portfolio make it among the most attractive takeover stocks to buy at the moment.

Takeover Stocks: AMC Networks (AMCX)

Source: Shutterstock

Lions Gate isn’t the only potential target, however. AMC (NASDAQ:AMCX) is another mid-sized content provider that could provide an attractive consolation prize for acquirers who miss out on the big fish. It also provides a nice ‘tuck-in’ acquisition for companies looking to expand their reach.

AMC owns five networks, including the flagship AMC, along with WE tv, Sundance, BBC America and IFC. Ratings for The Walking Dead have declined of late, but it’s still the most-watched program on cable and it has a huge long tail of content licensing revenue ahead. (AMCX owns Dead in full, unlike Mad Men and Breaking Bad.)

Meanwhile, AMCX is controlled by the Dolan family, who has already sold off Cablevision and reportedly would like to do the same with MSG Networks (NYSE:MSGN). And of late, the company has aggressively repurchased shares instead of paying down debt, which suggests at least a possibility that management believes that debt could become someone else’s problem.

The only concern here is valuation. I sold AMCX on a recent runup near $70, while the stock looks cheap on a price-to-earnings basis, further declines from The Walking Dead can lead earnings south, and even 2018 growth looks relatively muted. With a recent pullback after a big run following the AT&T/Time Warner deal, however, AMCX is starting to drift back to an attractive valuation.

Takeover Stocks: BioMarin Pharmaceutical (BMRN)

Source: Shutterstock

Acquisition rumors have swirled around specialty biotech BioMarin Pharmaceutical (NASDAQ:BMRN) for years now. In fact, Genetic Engineering & Biotechnology News has had it on its takeover target list for six years now.

Analysts have become part of the act off and on as well, with speculated acquirers including Sanofi (NYSE:SNY) and Roche Holdings (OTCMKTS:RHHBY).

The M&A case here makes some sense. BioMarin has developed an attractive portfolio, including several “orphan drugs”, as well as potentially valuable gene therapy treatments for hemophilia. 2018 revenue should be in the range of $1.5 billion, but BioMarin continues to post losses, which is one reason why the stock has flat-lined the past few years.

A larger acquirer could add growth from BioMarin’s drugs and cut costs to turn the company profitable. The big concern is valuation, particularly after a 30% run off of April lows. Still, at some point, the long-awaited sale of BioMarin appears likely. And even just below $100, there’s still more upside to come in that scenario.

Takeover Stocks: Arconic (ARNC)

Source: Shutterstock

Aircraft parts manufacturer Arconic (NYSE:ARNC) has been a subject of takeover speculation ever since it split from Alcoa (NYSE:AA). An activist stake owned by Elliott Management, whose strategies generally center on a near-term sale, only added to the frenzy. CNBC’s Jim Cramer argued last year that Honeywell International (NYSE:HON) was the obvious buyer, after United Technologies (NYSE:UTX) agreed to acquireRockwell Collins (NYSE:COL).

That speculation has been paused, however, as Arconic’s performance has hit the skids. The stock plunged in late April after cutting its full-year outlook. Higher aluminum costs are hitting margins (and somewhat ironically benefiting the Alcoa unit that supposedly was hiding Arconic’s true potential). Production missteps under Elliott’s new, hand-picked CEO have only added to the pressure.

Still, at some point, Arconic seems likely to return to being one of the most talked-about takeover stocks. It will take some time for the company to work through near-term issues. But with end demand from Boeing (NYSE:BA) strong and likely to stay the way, and consolidation in the space inevitable, Arconic very well may be acquired sooner than many investors currently believe.

Takeover Stocks: Xilinx (XLNX)

Source: Shutterstock

There are three key reasons why chipmaker Xilinx (NASDAQ:XLNX) is a likely acquisition target. The first is that the chip space in general is performing well and optimism toward the future is rising. With trends like IoT (Internet of Things) providing tailwinds, there’s an increasing belief that the old, more cyclical, nature of the space is starting to fade.

And, third, there’s a logical acquirer here in Broadcom (NASDAQ:AVGO). Even before Broadcom’s bid to buy Qualcomm (NASDAQ:QCOM) fell through, XLNX was touted as an attractive target for that always-acquisitive company. With Broadcom now U.S.-based, and with plenty of dry powder, such a deal makes even more sense at the moment. With XLNX lagging the chip space — it has gained less than 5% over the past year — despite strong earnings, the valuation looks workable as well.

Takeover Stocks: Maxim Integrated (MXIM)

Source: Shutterstock

Maxim Integrated (NASDAQ:MXIM) is another target for Broadcom or another large semiconductor company. Indeed, speculation has swirled for some time. Rumors of interest from Japan’s Renesas Electronics (OTCMKTS:RNECY) spiked MXIM stock in January, but the rumor was quickly shot down. Back in 2015, sources said Maxim held talks with Analog Devices (NASDAQ:ADI) and Texas Instruments (NASDAQ:TXN).

In both cases, price was a reported issue, and that still may be the case. At 21x forward earnings, MXIM stock isn’t exactly cheap. But a takeover at some point does seem possible, if not necessarily likely. And in the meantime, investors can receive a 2.8% dividend yield as they wait.

Takeover Stocks: Mattel (MAT)

Source: Shutterstock

Mattel (NASDAQ:MAT) is not a stock for the faint of heart. Execution missteps and weak demand have led MAT stock to drop by about 62% over the past five years, and 32% over the past three, even with a recent rally. The loss of a key licensing deal with Disney to rival Hasbro (NASDAQ:HAS) has only added to the pressure.

But Mattel appears to have entered the realm of takeover stocks, and with some reason. Hasbro could be a suitor, although antitrust concerns are an issue. The company itself said it had rejected an offer from MGA Entertainment in May.

The huge amount of debt is a big problem, as markets are valuing that debt as low as 82 cents on the dollar, making it less likely that an acquirer would want to pay par and provide a premium to equity owners. Still, rumors continue to swirl, and if Mattel can make some progress on its turnaround, the calls for a sale likely will only get louder.

Yet takeover speculation has continued, with recent rumors suggesting Alphabet (NASDAQ:GOOGL, NASDAQ:GOOG) should be interested as it builds out its cloud business. Any interest could start a bidding war, with other tech giants including Microsoft (NASDAQ:MSFT) perhaps becoming interested.

Whether there’s room for more premium is unclear, with RHT still trading at a dear 34x+ forward P/E multiple. But given its growth potential and importance in such a key space, Red Hat could become a target at any time.

Takeover Stocks: Sprouts Farmers Market (SFM)

Source: Shutterstock

Grocery stocks have struggled for the past year, ever since Amazon announced its acquisition of Whole Foods Market. And with the industry’s majors looking to increase scale and stand out from the crowd, Sprouts Farmers Market (NASDAQ:SFM) seems like an intriguing target.

Analysts have called out Sprouts as an attractive target. And indeed, Sprouts itself has taken steps down that path. Its CEO said in December that Sprouts was amenable to a takeover. It held talks with Albertsons early last year, though after they fell through, that giant instead chose to merge with Rite Aid (NYSE:RAD). Target (NYSE:TGT), Walmart (NYSE:WMT) and Kroger (NYSE:KR) all potentially make sense as buyers.

The concern is that — like many of these takeover stocks — some M&A premium is already priced in. And SFM did fall hard after a disappointing Q1 report in early May. But the stock has regained most of those losses, and it has held up despite the pressure on the space. That’s likely because the market believes that at some point, a buyout offer will come along.

Takeover Stocks: AeroVironment (AVAV)

Source: Shutterstock

Drone manufacturer AeroVironment (NASDAQ:AVAV) has been a logical M&A target going back to the last decade. Longstanding relationships with the U.S. Army and the Department of Defense, along with a generally heavy cost structure, theoretically made AVAV a natural target for a major defense contractor like Lockheed Martin (NYSE:LMT) or General Dynamics (NYSE:GD).

But the recent gains in AVAV stock, which has tripled from late 2016 lows, are coming from improvements in the business, not takeover speculation. Margins are improving. AeroVironment has two key opportunities in commercial applications (notably for agricultural use) and a joint venture with Softbank (OTCMKTS:SFTBY) to offer 5G wireless from high-altitude drones.

Still, there’s a potential M&A case here, with the only concern being its valuation. AVAV looks awfully stretched from here, trading at ~45x forward earnings. There are a lot of costs to cut, but it remains to be seen if the savings, and the potential growth, are large enough to justify more gains for AVAV.

Takeover Stocks: W.R. Grace (GRA)

Source: Shutterstock

Chemical producer W.R. Grace (NYSE:GRA) doesn’t get a lot of attention from investors, despite a $5 billion market cap. But there is increasing belief that Grace could be a takeover target relatively soon.

In April, chatter surrounding a Honeywell (NYSE:HON) bid sent GRA shares up over 6%. Before that, RBC cited the company as one of five likely takeover targets. And the 2016 spin-off of GCP Applied Technologies (NYSE:GCP) made a potential sale easier, as Grace’s CFO admitted at the time.

More recent speculation names Cisco (NASDAQ:CSCO) as potentially having interest. And several firms, including Morgan Stanley, have added CIEN to their list of takeover stocks.

Will this time be different? Possibly. But in the meantime, Ciena has a healthy balance sheet, a focus on margin expansion, and a reasonable valuation. Even if a takeover doesn’t (finally) materialize, there could be some value left in CIEN stock.

Square (NYSE:SQ) seems like a classic takeout candidate. It’s disrupting a payment space largely led by giants. The business could benefit from increased scale, and an acquirer could gain from lower sales and marketing spend.

The only question at this point is whether SQ stock is too expensive. I’ve long been bearish from a valuation perspective, but so far, I’ve been completely wrong.

In my defense, I’m not alone. At $65, SQ stock is well ahead of the consensus Wall Street target of $57. And at nearly 10x revenue, there’s a question as to whether the valuation can support anything left in the way of premium. Companies like PayPal (NASDAQ:PYPL) and even Visa (NYSE:V) and Mastercard (NYSE:MA) could be logical suitors. But can they — and will they — pay what Square shareholders would ask for?

Just a few years ago, beverage maker National Beverage Corp. (NASDAQ:FIZZ) was a sleepy producer of smaller soft drink brands. But the company’s LaCroix sparkling water brand took off, and so did FIZZ stock. It has risen 484% in the past five years alone.

Along with that increased valuation has come increased attention. Short sellers have targeted FIZZ stock. And rumors of a takeover have only amplified.

After all, LaCroix looks like a big winner. It has massive market share in sparkling water, a category that is taking share from diet soda (and regular soda as well). Quirky branding, design and marketing has garnered the label a cult following.

And so an acquisition makes sense — if one of the majors can’t undercut the LaCroix business. PepsiCo (NASDAQ:PEP) is trying to do so with its Bubly line. Coca-Cola Co (NYSE:KO) has rolled out Dasani sparkling water and acquired Topo Chico. But if LaCroix continues its dominance, Pepsi or Coke may simply decide to buy out National Beverage. Acquisitive Dr Pepper Snapple Group (NYSE:DPS) could be in the mix as well.

The rumor mill is as hot around Campbell Soup (NYSE:CPB) as any of the takeover stocks right now. In May, disappointing numbers and the exit of its CEO sent CPB stock to its lowest levels in nearly five years. But reports that Kraft Heinz Co (NASDAQ:KHC) is interested in buying the company have sent CPB shares soaring.

From here, the logic of a Kraft-Campbell’s tie-up seems minimal. Adding one zero-growth, indebted manufacturer to another doesn’t seem like an attractive combination. But at the least, it does seem like CPB’s family ownership group is accepting the need for a sale. And with activist pressure helping, that could lead to a buyout, whether by Kraft or by someone else.

Takeover Stocks: Hain Celestial (HAIN)

Source: Shutterstock

A common trend in the food industry the last few years has been for larger companies to buy smaller, faster-growing brands in the natural and organic spaces. But Hain Celestial (NASDAQ:HAIN) seems to have missed out.

Over the past few years, Hain has been cited as a possible target for a number of companies, including Kraft Heinz, Campbell’s and Hormel Foods (NYSE:HRL). But a somewhat unwieldy portfolio, which includes personal care, meats and snacks, has made a straight sale difficult. In the meantime, HAIN stock has taken a big hit, touching a six-year low in late May before a recent rebound.

But a sale finally may be on the way. An activist has taken a 9.9% stake and is pushing for a sale. HAIN probably won’t get a price close to its peak, and it may have to break itself up to create incremental value for existing shareholders. There is some value here, however, and a clear motivation to — finally — get a deal done.

Takeover Stocks: Wynn Resorts (WYNN)

Source: Shutterstock

Takeover speculation has ramped up around Wynn Resorts (NASDAQ:WYNN) this year. Once founder Steve Wynn stepped down amid sexual harrassment allegations in February, the path to a sale actually became a bit clearer.

Rival Las Vegas Sands (NYSE:LVS) seemed like the most logical acquirer. Rumors followed in April that MGM Resorts (NYSE:MGM) was interested in a takeover.

And with WYNN pulling back over the past few weeks, largely due to concerns surrounding its operations in Macau, the case for a takeout looks stronger. U.S. casinos have been in full-out M&A mode, with Eldorado Resorts (NASDAQ:ERI) buying up Isle of Capri and other assets and Penn National Gaming (NASDAQ:PENN) merging with Pinnacle Entertainment (NASDAQ:PNK), among many other moves. Similar logic would work for a takeout of Wynn.

Earnings season is upon us again — and it’s a big one. The market has traded sideways for several months now, and a solid batch of earnings reports could be just the catalyst to move broad markets back to new all-time highs.

Of late, investors have alternated between optimism toward a strong U.S. economy and fears about higher interest rates and potential trade wars. Moving the headlines to what should be at worst a solid earnings season could be good news for U.S. equities.

After all, there’s still a lot to like. Lower tax rates will help the majority of reporting companies. The economy looks like it’s at — or getting very close to — full employment. The effect of inflation in areas like labor and commodities bears watching, and could pressure margins and profit growth. But overall it seems like the majority of earnings reports should be good news.

This week kicks off the season — led by several key financials. But leaders in both the consumer and industrial spaces should also signal the health of their respective sectors. Strong reports from these five companies could send their stocks higher and also give investors reason for confidence heading into the next few weeks.

5 Earnings Reports to Watch: PepsiCo (PEP)

Source: Shutterstock

Earnings Report Date: Tuesday, before market open

PepsiCo (NASDAQ:PEP) has had a roller-coaster 2018. As of late January, PEP stock traded at an all-time high. By early May, it reached a 29-month low. An ugly start to the year for consumer products stocks was a key culprit. Not even a solid Q1 report in April could stem the bleeding.

Pepsi stock has rallied into earnings, however, rising 14% from those May lows. It can keep the momentum going with another beat on Tuesday. But caution might be advised. CPG stocks have struggled this year — for good reason, as I wrote in May. The new Bubly line, meant to compete with LaCroix from National Beverage Corp. (NASDAQ:FIZZ), needs to be a win — and may not be. Declining soda consumption, particularly relative to diet varieties, presents another long-term headwind.

PEP has outperformed rival The Coca-Cola Co (NYSE:KO) for years now. It may still do so going forward. But given the pressures on the industry, that doesn’t necessarily mean PEP stock is going up … either on Tuesday or beyond.

5 Earnings Reports to Watch: Fastenal (FAST)

Source: Shutterstock

Earnings Report Date: Wednesday, before market open

One sector that has been notably weak this year has been construction. Distributor Fastenal Company (NASDAQ:FAST) could buoy the space with strong results on Wednesday morning.

After all, FAST sales are a key data point relative to demand from builders and contractors. As such, it’s possible that a good quarter for Fastenal could do as much — if not more — to help other stocks than its own. Strong revenue results will suggest confidence from Fastenal’s suppliers and a continuation of solid growth in the industry.

And with those suppliers not threatened by Amazon.com (NASDAQ:AMZN), investors might see less risk in them. FAST does trade at a seven-month low, so a good report can help its own stock. But investors across the sector will be watching closely as well.

5 Earnings Reports to Watch: J.P. Morgan Chase (JPM)

Source: Shutterstock

Earnings Report Date: Friday, before market open

After a huge post-election run, financials have weakened – and that includes J.P. Morgan Chase(NYSE:JPM). JPM actually trades at a seven-month low at the moment.

It’s difficult to see why. Fed rate hikes, which should help net interest margin for JPM and other banks, seem likely to be on the expected pace. Federal Reserve stress tests went well, leading Josh Enomoto to recommend JPM as one of three bank stocks to buy.

I agree with Enomoto; I recommended JPM myself back in March. I still like Bank of America (NYSE:BAC) best in this sector, but investors can’t go wrong with JPM, either. And a strong earnings report on Friday should remind investors why this is a stock worth owning long-term.

5 Earnings Reports to Watch: Wells Fargo (WFC)

Source: Shutterstock

Earnings Report Date: Friday, before market open

For Wells Fargo (NYSE:WFC), Friday’s Q2 release will be less about what the company is doing right – and more about what it’s doing better. Wells continues to struggle with its past scandals, with the Fed deciding back in February to cap its asset growth as a result.

Strong numbers will help the stock’s cause. But the quarter — and the earnings call — will be more about restoring investor confidence. Wells Fargo’s largely new management will try and make the case that the bank is headed in the right direction.

On that front, I’m still skeptical. Particularly with JPM and BAC on sale, there are simply easier ways to make money in the financial space. It will take quite a bit from Wells Fargo’s Q2 report to suggest that past failures truly are behind the company.

5 Earnings Reports to Watch: Citigroup (C)

Source: Shutterstock

Earnings Report Date: Friday, before market open

Citigroup (NYSE:C) similarly has taken a hit of late. The stock actually touched an 11-month low last month before a modest rebound. And the low price sets up a potentially interesting report of its own on Friday morning.

After all, C stock looks like the cheapest of the big banks. It still trades below book value and at barely 9x 2019 EPS estimates. A recently boosted capital return program will add to buybacks and move the stock’s dividend yield to nearly 2.7%.

But Citi has its own regulatory issues to worry about. It still feels much more like a turnaround play than JPM or BAC. It’s not executing as well as those peers in either consumer or investment banking.

That leaves room for upside if Citigroup can improve its operations. That’s what investors will be watching for on Friday — and if they like what they hear, C stock could become a near-term out-performer.

Get up to 14 dividend paychecks per month from safe, reliable stocks with The Monthly Dividend Paycheck Calendar, an easy-to-use system that shows you which dividend stocks to pick, when to buy them, when you get paid your dividends, and how much. All you have to do is buy the stocks you like and tell them where to send your dividend payments. For more information Click Here.

As you well know, it only takes a handful of stocks to make — or break — your portfolio.

The economic turmoil of the past decade has drained investors’ portfolios, leaving many to stay in the work force well into their “Golden Years,” and has left those already in retirement wondering if there will be enough money at the end of the day.

That’s why I’ve put together this collection of my top eight stocks you should own now and hold for the long term.

Buy now for earnings growth and profits in the year ahead and hang onto them because they represent some of the best long-term stocks in the market today.

Top Growth Stocks: IPG Photonics (IPGP)

Source: Shutterstock

IPG Photonics (NASDAQ:IPGP) is the world’s leading provider of high-power fiber lasers. These lasers are used in a variety of different devices and applications, ranging from materials processing to broadband internet to medical pumps.

The bottom line is, the demand for fiber optic laser technology is a growth industry for a very long time, and IPGP is one of the major players.

Fiber lasers are the next generation of laser technology and offer many advantages over traditional lasers. They’re more energy efficient, they’re easier to maintain and they last longer.

As companies upgrade their current technologies with fiber-laser applications, IPG Photonics’ sales and earnings continue to soar.

In March IPGP entered the S&P 500, which is a big deal because every index fund linked to S&P 500 performance now needs to own the stock.

But IPGP stock has been up and down on tariff talk, so it’s a great time to get in.

Top Growth Stocks: Ferrari (RACE)

Source: Shutterstock

Ferrari NV (NASDAQ:RACE) is the world-renowned Italian sports car maker. Founded by Enzo Ferrari, the company developed and built its first sports car back in the late 1940s.

Today, Ferrari offers seven vehicle models, including four sports cars (488 GTB, 488 Spider, F12 Berlinetta and special series F12 Tour de France) and three GT cars (California T, FF and GTC4Lusso). The company also plans to replace the F12 Berlinetta with the 812 Superfast coupe.

Demand for its cars continues to rise and its line of clothing and accessories is also growing at a brisk pack.

Ferrari expects to ship more than 9,000 vehicles in 2018 and is looking for revenues of 3.4 billion euros. Company management also noted that it expects to double core earnings to 2 billion euros ($2.5 billion) by 2022.

RACE stock is up nearly 30% year to date, so none of this trade war talk or political turmoil in Italian politics is slowing its performance.

Top Growth Stocks: Weibo (WB)

Source: Shutterstock

Known as “China’s answer to Twitter,” Weibo (NASDAQ:WB) is a social media company that allows Chinese users to express themselves, connect with others, discover Chinese-language content and use push notifications on their mobile devices.

While its Twitter of China description was pretty accurate in its early days, now it’s much more diversified — it’s more like the Facebook of China at this point.

Weibo now offers online games and mobile apps that have created a very complete social media experience in a young, enthusiastic consumer demographic.

It’s no surprise then that WB has experienced tremendous growth since its launch in 2010, and it shows no signs of slowing down.

Trade war talk has soured the market on WB, but that’s to our advantage. WB has enormous potential growth in China and Asia, without any need to look to the U.S.

Top Growth Stocks: Arista Networks (ANET)

Based in San Jose, California, Arista Networks (NYSE:ANET) provides cloud networking solutions to 4,000 customers across five continents.

Arista specializes in high-speed network switches that enable cloud service providers, internet companies and data centers to run faster networks. Arista also provides technical support, hardware repair and parts replacement.

When it comes to the lucrative high-speed network switches market, Arista Networks goes toe-to-toe with Cisco Systems (NASDAQ:CSCO). But while its larger competitor is struggling to grow sales and earnings, Arista Networks is growing by leaps and bounds.

Part of ANET’s competitive advantage is that it isn’t tied down to legacy systems like CSCO is. Its equipment is next generation, built for the next iteration in networking and cloud services.

It has had a bumpy ride in 2018, but this is a long-term player with huge potential. It is a force in crucial megatrend sectors that will grow regardless of economic ups and downs.

Top Growth Stocks: Nvidia (NVDA)

Source: Shutterstock

Nvidia (NASDAQ:NVDA) is a leading computer graphics company, making graphic processing units (GPUs) for consumers and businesses.

These GPUs enhance the processing capability of its users’ computers.

The company has been in the computer graphics business for more than two decades — it invented the GPU in 1999 — so it is a well-established player.

In a recent earnings report, company management noted that NVDA “achieved another record quarter, capping an excellent year.” The fact is, this could be almost any quarter since 2016.

If you look at NVDA’s historic price chart, you can see that the stock goes parabolic in 2016. That’s when the mobility trend took off and enabled all the sectors that NVDA has come to dominate: cloud, augmented reality, virtual reality, Internet of Things, Big Data, smart devices, etc.

NVDA is to the future of computing what Amazon (NASDAQ:AMZN)has become to ecommerce.

Top Growth Stocks: Sociedad Quimica Y Minera de Chile (SQM)

Sociedad Quimica Y Minera de Chile (NYSE: SQM), or the Chemical & Mining Co. of Chile, is the largest producer of specialty plant nutrients, lithium and derivatives, iodine and derivatives, industrial chemicals and potassium in the world.

Not surprisingly, given that list of materials, its products have a range of uses.

Its Specialty Plant Nutrition division provides nutrients and fertilizers to boost crop output. Increasing productivity is crucial to farmers, especially when prices (and margins) are low.

Its Iodine division offers derivatives that are used in medical and industrial applications, as well as in antiseptics, disinfectants and polarizing films for LCDs.

Its Lithium division provides lithium carbonates for batteries, heat-resistant glass, air conditioning chemicals and more. With electric and hybrid vehicle demand growing, consistent lithium supplies are crucial.

Its Industrials Chemicals division produces industrial nitrates that are used to manufacture glass and explosives.

Its Potassium division focuses on the sales of two potassium fertilizers. Trade issues have discounted the stock and make it a bargain long-term investment now.

Top Growth Stocks: UnitedHealth Group (UNH)

Source: Shutterstock

UnitedHealth Group (NYSE:UNH) is the largest single health carrier in the United States. It serves more than 85 million people worldwide and is a parent company to six businesses, including UnitedHealthcare — health insurance that offers policies to businesses and individuals, including Medicare and Medicaid policies.

Its other main branch, Optum, administers everything from mental health and substance-abuse programs to mail-order pharmaceuticals.

While many drug store stocks were rocked by the news that Amazon has now entered the pharmacy business, UNH has been relatively undisturbed because of its integrated strategy.

Looking ahead to full-year 2018, the healthcare giant is targeting adjusted earnings between $12.30 and $12.60 per share, which is a 22% to 25% year-over-year increase and up from its previous guidance of $10.55 to $10.85 per share.

Additionally, cash flows from operations are expected to be in a range between $15 billion and $15.5 billion, and UnitedHealth Group is calling for total revenues between $223 billion and $225 billion.

Intuitive Surgical (NASDAQ:ISRG) is in a business that sounds like it comes straight from a science-fiction novel: Surgical robotics.

However, luckily for patients around the world, this revolutionary technology is not only possible, it is becoming more and more integrated into everyday hospital use.

Intuitive Surgical got its big break in 1999 when it introduced the da Vinci surgical system. Complete with a surgeon’s console, a patient-side cart, a 3-D vision system and wrist instruments, this system allows doctors to perform minimally invasive surgery with enhanced dexterity, precision and control.

In the end, this technology benefits the patients, who usually experience less pain, a shortened hospital stay, fewer infections and less scarring.

Nearly 20 years later, the company has developed several models of this surgical system and even offers a training program that brings surgeons up to speed on this technology.

This system has steadily caught on in the healthcare industry; last year alone, the company’s systems were used in 650,000 procedures around the world.

ISRG stock is up more than 30% so far this year, but that is still just the beginning for this next generation healthcare company.

Get up to 14 dividend paychecks per month from safe, reliable stocks with The Monthly Dividend Paycheck Calendar, an easy-to-use system that shows you which dividend stocks to pick, when to buy them, when you get paid your dividends, and how much. All you have to do is buy the stocks you like and tell them where to send your dividend payments. For more information Click Here.

One constant in the human journey remains the creativity of the human mind. Ideas can emerge from this wellspring that not only change the way we live, they also bring new businesses to the market. From a stock market perspective, this leads to new up-and-coming stocks. Other ideas breathe new life into old stocks whose older business lines fell out of favor. In reality, investors do not make outsized returns by buying stocks like Apple Inc (NASDAQ:AAPL) or Amazon.com, Inc. (NASDAQ:AMZN) at their current sizes. They make money buying the future Apple or Amazon that has not yet become well-known.

What the technology world has experienced recently has become nothing short of another Industrial Revolution. I believe historians will look back upon the 2010s as a time when many of these ideas spring forth.

Fortunately, several up-and-coming stocks have appeared that will allow investors to profit from this growth and change. These 5 stocks hold potential for investors to bolster their portfolios on revolutionary change.

5 Up-And-Coming Stocks: ETFMG Alternative Harvest ETF (MJ)

Source: Shutterstock

Marijuana is by no means a new substance. This revolution is more of an attitudinal change which has brought the market numerous up-and-coming stocks. The ETFMG Alternative Harvest ETF (NYSEARCA:MJ) stands at the forefront of this revolution. As of now, this has become the first and currently only marijuana ETF to trade on U.S. exchanges.

ETF inflows have stagnated as of late while as their counterparts on the Toronto Exchange continue moving higher. This pause likely hinges on the uncertainty surrounding federal marijuana laws in the U.S. However, I think this uncertainty creates opportunity. And this opportunity comes from an attitudinal change from an unexpected source: the Republican party.

Former House Speaker John Boehner, once a staunch opponent of cannabis, joined the board of a marijuana company. President Donald Trump recently proposed removing legal restrictions on marijuana. And just this week, Oklahoma, one of the most deeply Republican states in the Union, approved a permissive medical marijuana law.

Such changes will only bolster the cannabis industry, especially with regard to U.S. companies. Though the ETF holds several U.S. stocks, Canadian stocks The Green Organic Dutchman Holdings (OTCMKTS:TGODF), Canopy Growth (NYSE:CGC), and Aurora Cannabis (OTCMKTS:ACCBF) stand as its largest holdings. It also trades about 25% below its January high, despite the solid performance of many of its Canadian holdings. Between Canada’s legalization and loosening restrictions in the U.S., MJ stock should provide a safe and profitable segue into the cannabis industry.

5 Up-And-Coming Stocks: IPG Photonics (IPGP)

Source: Shutterstock

IPG Photonics Corporation (NASDAQ:IPGP) develops and manufactures high-performance industrial lasers. Industries ranging from automotive to aerospace to semiconductors use IPG’s technology in their manufacturing processes. In addition to lasers, it also produces equipment for medical and telecom applications.

Growth has remained both robust and steady. Both revenue and profits have increased at an annual rate of about 20% for the last five years. Although revenue growth will likely slow in future years, earnings increases should maintain their current pace for the foreseeable future.

Recent geopolitical events have created opportunity in IPGP stock. IPG earns about one-third of its business from China. The escalating trade dispute with China had led to a massive selloff. IPGP stock has fallen by over 17% since the beginning of June as a result.

Despite this drop in the stock price, massive growth has defined this stock for most of the decade. Few up-and-coming stocks have seen this level of growth. The stock has risen from a low below $7 per share in 2009 to as high as $264 per share. However, even with this increase, IPGP stock trades at around 32 times current earnings. With this high level of growth expected to continue for the foreseeable future, interested investors should take advantage of this China uncertainty to buy into IPGP.

5 Up-And-Coming Stocks: iRobot Corporation (IRBT)

Source: Shutterstock

iRobot Corporation (NASDAQ:IRBT) should serve as one of the more recognizable up-and-coming stocks. It leads its industry in the emerging field of consumer robots. Founded in 1990 by a group of MIT graduates, it expanded the reach of artificial intelligence (AI), settling on a niche in consumer robots. Its most commercially successful robot has become the Roomba vacuum. Its floor mopper, Braava, and other consumer robots also continue to sell well.

The Bedford, Massachusetts-based company has enjoyed years of high growth as a result. Annual revenue growth tops 15% per year. Profits have also seen double-digit percentage growth in most years. In fact, analysts expect yearly profit growth to exceed 20% per year through 2021.

Considering the stock price has increased by more than tenfold since its 2009 low, the company trades at a fair valuation. That growth has taken the market cap to about $2.1 billion. Its current PE now stands at about 40. While that may appear high, it also trades at about 2.3 times sales and around 4.2 times its book value.

It also has fallen substantially from its 52-week high. SharkNinja has posed a challenge to iRobot’s market dominance. Between July and February, IRBT stock lost over 50% of its value as Shark claimed a market share exceeding 20%. However, since early May the stock has jumped from about $56 per share to around $76 per share today. Although analysts expect its 60% market share to fall, profits should continue growing at 20% per year. And with only about 11% of U.S. households owning a robotic vacuum, growth should continue for years to come.

5 Up-And-Coming Stocks: Nokia (NOK)

Source: Shutterstock

As the oldest company on this list, Nokia Oyj (ADR) (NYSE:NOK) makes the up-and-coming stocks list on reinvention. The company began its history in the mid-19th century in present-day Finland as a pulp mill. As late as the 1960s, they produced toilet paper. Moving from that point to achieving the domination of the mobile phone market required a radical change. With the decline of non-smart mobile phones, Nokia has reinvented itself once again. It now stands at the forefront of the 5G revolution.

5G promises to increase connection speeds by as much as 100-fold from the current 4G technology. Most of the major wireless companies throughout the world will each invest tens of billions of dollars to upgrade their wireless networks. Since Nokia has become a leading producer of 5G equipment, it will derive massive benefits from this upgrade.

Still reeling from its loss of the mobile phone market, NOK stock still trades under $6 per share. However, 5G leads the way in its comeback. The company expects earnings of between 23 and 27 euro cents (between 27 and 31 cents) per share this year. By 2020, NOK expects earnings to reach between 37 and 42 euro cents (between 43 and 49 cents per share). For 2018, this takes the forward price-to-earnings (PE) ratio to between 18.8 and 21.6.

Growth would also remain in the double-digits by even the most conservative estimates. If NOK stock can maintain such a growth pace, perhaps it could return to the $42 per share high it saw in 2007 and maybe beyond.

Teladoc Inc (NYSE:TDOC) is one of the up-and-coming stocks that continues to bolster its dominance in the emerging telehealth industry. The Purchase, New York-based provider boasts of a 75% market share in an industry that could claim a significant percentage of the market for doctor’s office visits.

For $40, patients can visit a Teladoc doctor 24 hours a day, seven days aweek. Assuming the doctor can evaluate the patient this way, the patient can receive a diagnosis and, if necessary, have a prescription sent to a pharmacy within a few minutes. Similar services from an in-person physician can run more than three times the cost and are only available during regular business hours. TDOC also offers similar services for behavioral health services.

Analysts believe this service, which serves under 1% of patients now, could cover up to 30% of all doctor visits within a few years. It will also receive a boost when it begins to cover Medicare Advantage patients starting in 2020.

Best of all, TDOC stock has worked to expand what might otherwise be described as a thin moat. In 2017, it acquired Best Doctors to improve its diagnosis capabilities. This year, it acquired Advanced Medical. This will bring Teladoc’s services to several other countries.

Investors will have to exercise patience as a positive net income remains a few years off. However, revenue continues to grow by about 50% per year. The number of patient visits increases by nearly the same amount. With that level of growth and its market share, TDOC stock has positioned itself to both grow quickly and dominate the telehealth industry.

Get up to 14 dividend paychecks per month from safe, reliable stocks with The Monthly Dividend Paycheck Calendar, an easy-to-use system that shows you which dividend stocks to pick, when to buy them, when you get paid your dividends, and how much. All you have to do is buy the stocks you like and tell them where to send your dividend payments. For more information Click Here.

In 2018, the stock market has been presented with two major risks:

Inflation

Trade

These risks have reared their ugly heads from time to time, and caused broader market volatility. Each time, though, the market has shrugged off the risk to ultimately head higher.

Right now, inflation concerns are subdued as the 10-Year Treasury yield has backed off 3%. But trade risks are at all-time highs as President Donald Trump continues to impose tariffs. Simultaneously, no one on the global political landscape appears willing to stand down, so tensions are escalating and the likelihood of a trade war breaking out is rising.

If things go on like this, trade talk will get ugly and the stock market will suffer.

But not all stock should be treated equally. Indeed, there are certain “trade war stocks” out there which should be largely immune to tariffs and trade talk. These stocks should head higher regardless of what happens on the trade front.

With that in mind, here’s a list of my three favorite trade war stocks to buy if all this trade talk takes a nasty turn.

Trade Wars Stocks to Buy: Facebook Inc (FB)

Source: Shutterstock

The FANG stocks are largely insulated from trade war risks for two major reasons: 1) they are giant internet companies that benefit consumers globally via services that won’t be affected in a trade war, and 2) they don’t have a presence in or reliance on China.

Of the FANG stocks, perhaps the one best positioned to succeed amid rising trade war fears is social media giant Facebook (NASDAQ:FB).

Facebook is a global digital ad giant that benefits everyone, everywhere, regardless of nationality. Facebook’s ad services won’t be adversely impacted by tariffs, nor will the volume of ad dollars that flow through the company’s ecosystem or the amount of people who access Facebook every month.

Instead, Facebook will keep doing business as usual. They will keep providing the best, most robust, and most effective digital advertising solutions in the world, and they will continue to roll out new growth initiatives like Messenger/WhatsApp monetization, Workplace, Marketplace and smart home products.

Last quarter, “business as usual” was represented by 50% revenue growth. Trade war risks won’t affect that growth rate. Instead, over the next several years, growth will remain in the 30%-plus range because of the company’s multiple growth catalysts.

Facebook stock trades at less than 30-times forward earnings. A 30 multiple for 30%-plus revenue growth is a bargain, especially considering that the big growth isn’t at-risk to prevailing trade war fears.

As such, Facebook stock is definitely one of the top trade war stocks to own here and now.

Trade War Stocks to Buy: Alphabet (GOOG)

Source: Shutterstock

The other top trade war stock from the FANG group is Alphabet Inc (NASDAQ:GOOG).

Much like Facebook, Google is a global digital advertising giant that benefits everyone, everywhere. The company’s advertising services will not be materially affected by trade war fears or tariffs. The amount of money being pumped into the Google ad machine also won’t be affected, nor will the number of people using Google search.

Instead, much like Facebook, Google will keep doing business as usual. All the trade war talk is just noise in the background.

The upside in Google stock comes from valuation and the company’s unparalleled data-set, which positions it to be a leader in tomorrow’s data-driven and an artificial intelligence-dominated world.

Google has forever been a 20%-plus revenue growth company thanks to its robust digital advertising platform. But that growth could be super-charged over the next several years as Google turns its unrivaled database on consumer searches and preferences into unrivaled AI and automated technologies.

Indeed, at the current moment, Google is the innovation leader in tomorrow’s big growth spaces like self-driving (Waymo) and AI (Google Duplex). Google’s leadership position in these markets will only grow over the next several years since data is what powers advancements in AI. Accordingly, Google’s growth could get a super-charged lift over the next 5-plus years.

But like Facebook stock, Google stock trades at under 30-times earnings. That multiple is just too cheap. Consequently, Google is not only one of the best trade war stocks to own now, but also a great long-term investment.

Trade War Stocks to Buy: Verizon (VZ)

Source: Shutterstock

Perhaps the best trade war stock to own amid rising trade-related fears is telecom giant Verizon Communications Inc. (NYSE:VZ).

At its core, Verizon provides telecommunications services exclusively in the United States. This business inherently has mitigated exposure to tariffs and trade. Consequently, regardless of what happens on the global trade stage, Verizon’s U.S.-based telecom business will be largely unaffected.

Moreover, Verizon is a big dividend payer with a yield of nearly 5%. As broader market fears escalate, investors tend to flock to dividend safe-havens with big and sustainable dividends. Verizon is exactly that.

And then there is the whole improving fundamentals part of Verizon stock.

For years, the wireless service industry was one defined by ruthless competition, price cuts, market saturation, and margin erosion. But those fundamentals are starting to change, mostly due to the forthcoming roll-out of 5G coverage. That will allow Verizon to differentiate itself from the pack, thereby allowing Verizon to lift prices and grow market share. Revenues, margins, and profits will trend higher as a result.

Overall, then, Verizon is one of the best trade war stocks to own right now given its lack of international exposure and huge dividend yield. Moreover, improving fundamentals in the wireless services industry pave the path for meaningful earnings growth and stock price appreciation over the next several years.

As of this writing, Luke Lango was long FB, GOOG and VZ.

Get up to 14 dividend paychecks per month from safe, reliable stocks with The Monthly Dividend Paycheck Calendar, an easy-to-use system that shows you which dividend stocks to pick, when to buy them, when you get paid your dividends, and how much. All you have to do is buy the stocks you like and tell them where to send your dividend payments. For more information Click Here.

On Monday morning, investors came out strong and bought the trade-war dip. On Tuesday, it took more convincing, but bulls reluctantly bid U.S. equities off their lows. I don’t know how much longer they can handle it though and if trade talks intensify, U.S. stocks look likely to head lower. That’s why on days like this, I like to look for strength, which you’ll see in our top stock trades below.

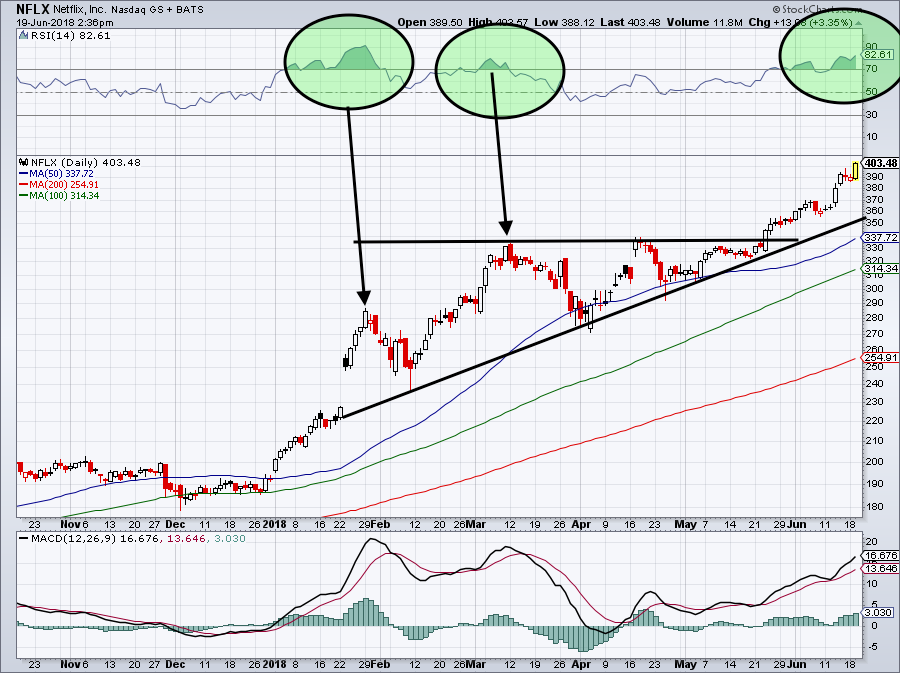

Top Stock Trades for Tomorrow No. 1: Netflix (NFLX)

Talk about a juggernaut — Netflix, Inc. (NASDAQ:NFLX) has powered higher again on Tuesday, now up more than 3% and above $400. Thought you could get this on a pullback? Well think again, apparently.

Shares are now up a laughable 110% this year and more than 160% over the past 12 months. FANG is hanging tough amid the selling too, with Amazon.com, Inc. (NASDAQ:AMZN) racking up another all-time high on Tuesday as well.

So what do investors do with NFLX? For the love of God, please don’t short the thing. We’ve preached over and over not to short strength and this is a perfect example as to why, regardless of the valuation.

We were all over the breakout in late-May and props to those who are still riding it. $400 is a significant level, but with this high of an RSI (green circle) and after this big of a run, new buyers have to wait for a pullback or some consolidation first.

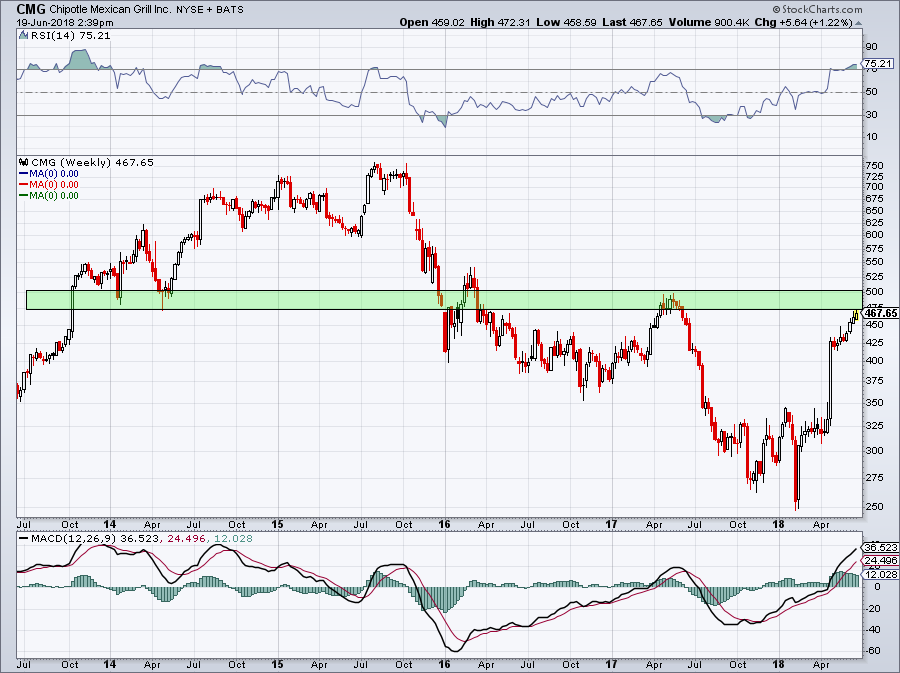

Top Stock Trades for Tomorrow No. 2: Chipotle (CMG)

Want to know another strong stock lately? Chipotle Mexican Grill, Inc. (NYSE:CMG). This burrito monster has been on a tear, almost doubling from its 2018 lows.

Now though, CMG is coming into some pretty notable resistance between $475 and $500. The optimist in me is looking for shares to push through, but the realist in me says that may not happen quite so fast.

You may recall we warned investors not to short CMG after it ran from $325 to $425 in a week. But now we need to see how it handles resistance. If it pushes through, then great, as bulls can buy with a great risk/reward. Buying as CMG enters resistance though is a bad risk/reward.

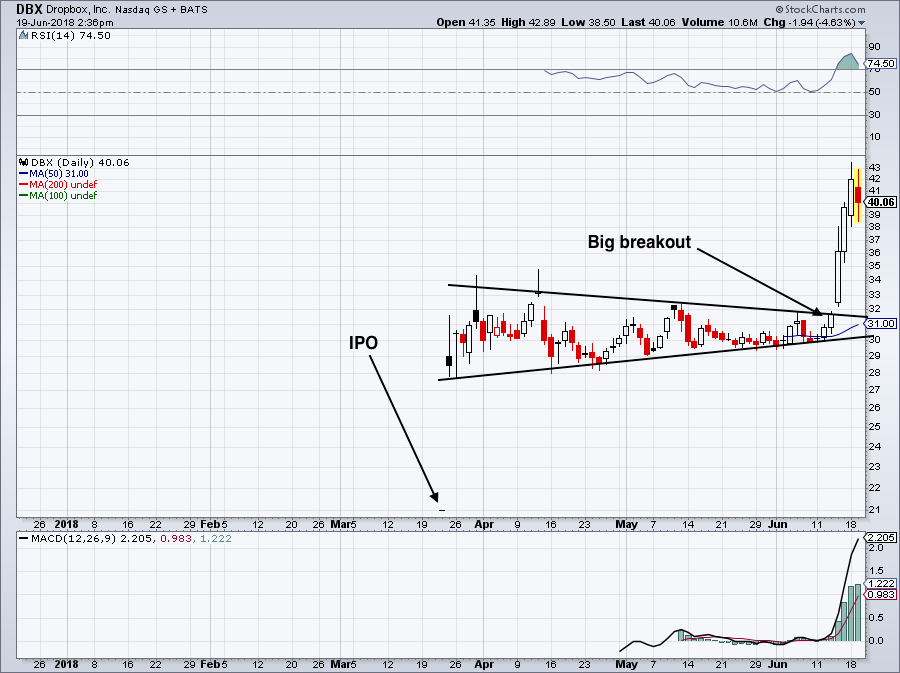

Top Stock Trades for Tomorrow No. 3: Dropbox (DBX)

Another monster? Dropbox Inc (NASDAQ:DBX), which went public in March at $21. After closing at $42 on Monday, the stock is officially a double.

But the story is a little more strange than that. While the stock was holding onto its gains following a successful IPO, shares were getting into a narrow, sideways range. It was the perfect name to watch for a breakout or a breakdown. However, no one expected it go from $31 to $43 in three days. We still don’t really have an explanation, (although there may be some reasoning).