The social stigma against marijuana continues to slowly dissipate.

Source: Shutterstock

A construction worker’s pick-up truck passed me twice during a recent walk, apparently looking for a job site, the smell of marijuana smoke redolent in the air. It’s still illegal to smoke in Georgia, but that doesn’t mean the illegal market isn’t operating …

But what about the legal market?

Stock in Tilray (NASDAQ:TLRY), the Canadian pot company, now sits finely poised between earnings due on today after the bell and a shortage of stock to short.

Tilray stock is expected to lose 12 cents per share on revenue of $14.15 million. (Earnings Whispers puts the numbers for earnings and revenue at -15 cents and $17.69mm, respectively.) But that may be less important to speculators than Tilray’s efforts to create credibility with the marijuana and general investor communities.

Consider the following: Tilray has appointed Andrew Pucher, a former managing director at Goldman Sachs (NYSE:GS), as chief corporate development officer.

Pucher joins a team that now includes former executives from Nestle (OTCMKTS:NSRGY), Diageo (NYSE:DEO), Coca-Cola (NYSE:KO) and Starbucks (NASDAQ:SBUX). Further, Tilray has a partnership with Novartis (NYSE:NVS), a joint venture with Anheuser-Busch InBev(NYSE:BUD) and a production agreement with the privately-held Authentic Brands Group.

Finally, Tilray last week announced a deal to buy Manitoba Harvest from Compass Group(NYSE:CODI) for about $315 million.

With all this corporate star power and deal-making, you would think Tilray would be a major pot producer.

What About the Product?

What product?

Tilray sold no marijuana during the first two weeks after Canada legalized it in October. CEO Brendan Kennedy insisted that this will have changed by this quarter, while simultaneously announcing he bought producer Natura Naturalsfor $26.3 million. If all this is leaving you skeptical about the company, you’re not alone …

Tilray short interest recently stood at 4 million shares, 24.62% of the company’s float, and there’s no more available to borrow. That’s why shares of a company that may report revenue of $17 million trade at a market capitalization of almost $7 billion.

The other is that most of the shares don’t trade, with over 78% held by “individual stakeholders.” There are 79 million shares outstanding.

The Marijuana Market

Speculators are betting that over the next few years, many more U.S. states will legalize marijuana sales and are looking to legislators for guidance.

But despite the examples of Colorado and Washington, the path to legal pot is still not a straight line.

Minnesota Republicans recently rejected a legalization effort, prospects are dimming in New Mexico and New York’s move is being held up by black legislators who want specific provisionsfor their communities to benefit.

As a result, most moves lately have been toward legalizing medical marijuana, with doctors’ prescriptions and extensive regulation. Florida is moving in that direction. So is Oklahoma.

All that said, marijuana remains an illegal drug under U.S. law.

People are still being put in jail for marijuana offenses and Tesla (NASDAQ:TSLA) CEO Elon Musk may lose his SpaceX security clearance after being shown on video smoking pot on a podcast.

Tilray and its competitors are preparing for an opportunity that may not come to them for years. Meanwhile, marijuana stocks have been bid well beyond fundamentals. A lot of people are cashing big paychecks, and the dream of a well-regulated American pot market remains hazy.

Data current as of market close 03/14/19.It is stocks like these that make up the high-yield portfolio (current average is over 8%) used in the Monthly Dividend Paycheck Calendar, a wealth creation system used by thousands of dividend investors enjoying a steady, reliable income.

The Monthly Dividend Paycheck Calendar is set up to make sure you receive a minimum of 5 paychecks per month and in some months 8, 9, even 12 paychecks per month from stable, reliable stocks with high yields.

It has been a challenging start to 2019 for real estate investment trust (REIT) investors. At the start of the year, the REIT indexes zoomed higher. The last few weeks have investors wonder if the party is already over for the year.

The financial media is placing blame in many places including trade wars, slowing growth and interest rate uncertainty. Many believe interest rates on the long end of the yield curve could rise with the growing Federal deficit. Which if true does not give confidence in REIT values. Fortunately, history shows that the belief that rising interest rates are bad for REITs value is a false assumption.

The current doldrums for the REIT sector may likely end up as a great buying opportunity for future gains.

Both Forbes and the NAREIT website note that historically, REITs have generated returns greater than the S&P 500 during periods of rising rates. How can this happen? As income investments, investors tend to lump REITs in with fixed income investments, i.e. bonds.

When interest rates go up, mathematically bond prices must fall producing negative returns for bond investors. REIT shares are ownership stakes in businesses. Rising interest rates are usually the result of economic growth.

For the REIT sector, an improving economy typically means rising commercial property values and the potential to increase rental rates. A significant portion of the REIT sector sees significantly greater benefits from economic growth than they experience from higher interest expense.

These factors are especially true in the current market. Companies have had several years to prepare for higher rates. This means that well managed REITs have locked in low interest rates with long-term fixed rate debt. These REITs should be able to improve profit margins by boosting lease rates, even as they keep interest expenses low.

There are REITs to avoid. Stay away from any companies that have variable rate borrowing costs. These will see profits squeezed by rising rates.

Avoid REITs that do not have histories of dividend growth. Part of staying ahead of rising rates is to own those REITs that can grow dividends faster than the increases in interest rates and inflation. With the recent retrenchment in REIT values, you can find shares with very attractive yields.

The next step is to ferret out companies that will grow dividends at greater than the rate of inflation. Here are three to get started with.

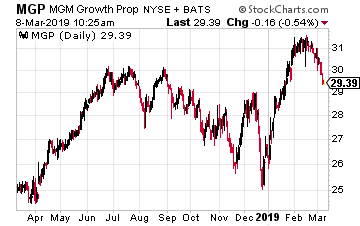

MGM Growth Properties LLC (NYSE: MGP) is a REIT that was spun-off by MGM Resorts International (NYSE: MGM) in April 2016. In the IPO MGP received ownership to a larger portion of the MGM owned real estate, primarily casino hotel resorts.

The properties are leased back to MGM Resorts on a long-term master net lease. Lease terms are very favorable for MGM Growth Properties. The master lease means that MGM makes a single lease payment and cannot get out of paying for individual properties. All new acquisitions from MGM are added to the master lease. The lease includes annual rent escalators and profit sharing from the portfolio resorts.

The MGP dividend has been increased five times since the IPO and is forecast to grow by 8% in 2019. As the name states, this is a growth focused REIT. They have made offers on Las Vegas properties not owned by MGM.

The stock currently yields 6.0%.

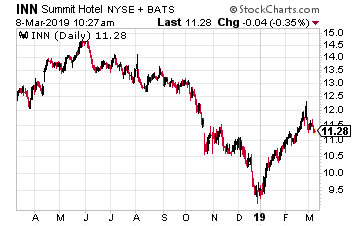

Hotels are a commercial real estate sector that benefit from economic growth and can quickly pass along higher costs as higher room rates.

Summit Hotel Properties, Inc. (NYSE: INN)recently announced very good 2018 results, with expectations of continued growth in 2019. Revenue per Available Room (RevPAR) is the metric to watch with hotel companies.

After two years of flat RevPAR, the metric took started to improve in 2018. Continued profit growth should lead to a 5% to 6% dividend increase this year. The current dividend rate is just 50% of FFO per share.

The continued positive economic outlook should allow INN to grow dividends in the high single digit range.

The stock yields 6.3%.

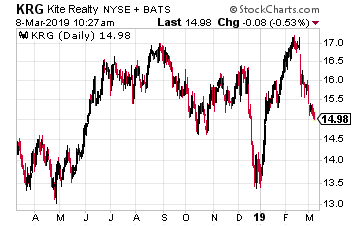

Kite Realty Group Trust (NYSE: KRG)neighborhood and community shopping centers in selected markets. These shopping centers are different from the malls and are integral to the function of the communities where they are located.

These properties are anchored by internet-resistant tenants like restaurants, grocers, entertainment, and specialty stores. Kite Realty has been a steady 5% per year dividend growth REIT. This will not change even if the investing public gets negative on anything that looks like a mall REIT.

In the retail sector there are great differences between different companies and the types of properties they own. Kite Realty is an undervalued, stable dividend growth REIT.

The current 8.4% yield makes KRG shares very attractive.

All across the U.S. these days, retail stores are very much like the Walking Dead.

Ironically, on paper at least, this would seem to be an ideal time to operate a retail store.

After all, we are in the best jobs market we’ve seen in more than 40 years, and the economy remains in great shape. Virtually across the board, high-tech firms have been reporting stellar fourth quarter results.

Retailers, not so much…

But even chain-store firms who managed to beat Wall Street’s forecasts can’t seem to defy the steady shift in power to the web and well-run e-commerce portals.

Consider that the Foot Locker Inc.(NYSE: FL) recently reported its growth more than doubled expectations in its most recent quarter. And yet, just days ago, the sports chain said it will shutter 165 stores.

That was part of a series of store closings that totaled 465 in just 48 hours.5

With that in mind, today I’m going to reiterate a stock I have recommended many times as one that will benefit from the shift from brick-and-mortar retail to e-commerce.

And of course, it’s a firm with market-crushing gains…

Check it out…

Shopping Carnage

The carnage in the shopping landscape actually shows no signs of slowing down. We can see that by the firms that have announced store closings. Besides the Foot Locker, there are:

The Gap Inc. (NYSE: GPS) is closing 230 stores after reporting that during the Christmas holiday, quarter same-store sales fell 7%.

Victoria’s Secret, which is privately held, said same-store sales fell during the holidays by 3%. It’s closing 53 stores this year.

J.C. Penny Co. Inc. (NYSE: JCP) said it is closing 18 of its 850 stores. But analysts expect more closures in the near future.

And let’s not forget that a company that was once the top retailer of its day recently filed for bankruptcy protection from its creditors.

Sears was America’s original “everything” store. Between its actual physical locations and its massive catalogue operations, it offered consumers the opportunity to buy hundreds of goods, covering everything from clothes to tires to furniture.

But like many other retailers, Sears simply failed to keep up with the times. Today’s consumers can buy just about anything they need in a matter of minutes online from the convenience of their computers or mobile devices.

Indeed, data compiled by Statista shows e-commerce continues to ramp up sales with a high compound growth rate.

Total sales for the sector are expected to hit $735.4 billion by 2023. That’s a 64.5% increase from the $446.8 billion level set in the base year of 2017.

Changing the Game

Amid all this chaos, one firm stands out as the preeminent e-commerce firm in the world today. It’s making so much money online that it can now afford to challenge physical retailers at their own game.

When you look on how massive and profitable Amazon.com Inc. (Nasdaq: AMZN) has become, it’s hard to believe that it started off in 1994 with a simple mission of selling physical books over the Web.

Today, the firm continues to deliver growth rates that make regular retailers green with envy. In fact, I think the Amazon stock price could soon reach $2,000 per share.

Consider that at the start of the current decade, Amazon had $34 billion in sales. By next year, that figure should surpass $325 billion. That’s nearly 1,000% growth.

I’ve been watching this firm for years, and was one of the first people to tell you that the share price would handily pass the $1,000 mark. That finally happened in 2017, and now in the early days of 2019, the $2,000 mark is fast coming into focus.

What Doesn’t Amazon Sell?

Of course, Amazon is still a massive bookseller, but now it sells so much more.

We could spend a lot of time talking about all of various kinds of things you can buy through Amazon. It’s likely easier to think of what Amazon doesn’t sell.

Of course, the real secret to Amazon’s success is not based on the stocking and shipping of hard goods. Instead, it’s an uncanny use of technology that touches on everything the firm does.

Take cloud computing as an example. Amazon began to realize that it had built such an impressive global computing platform that it could save massive sums by running its business on its own massive cloud platform.

Soon enough, Amazon began selling its cloud-based web services to others, and that’s now a business that will be bringing in $71 billion in revenue by 2022, according to banking firm Jefferies & Co.

AI Will Help Propel the Amazon Stock Price to $2,000

Amazon has also deeply embraced artificial intelligence (AI). Today, AI brings a lot of smarts to Amazon’s Alexa assistant. And Amazon has big plans to extend AI throughout every one of its business units.

All of these growth areas have enabled Amazon to generate so much cash that it can afford to buy its way into whole new lines of business.

The firm made a high profile 2017 purchase of healthy grocer Whole Foods for $13.7 billion. Now, it’s using the know-how it picked up to make an even deeper push into the grocery market through a chain of stores separate from Whole Foods, according to the Wall Street Journal.

When you consider that Amazon knows how to make a profit where others fail, I have no doubt that the move into groceries will become highly lucrative for Amazon – and its investors.

Simply put, Amazon has the Midas touch. It becomes dominant in every new category it enters. That’s by design, not accident. Amazon only enters into a new category when it knows it has the resources and skills to succeed – on a massive scale.

It’s of no use to examine where this stock has been. You only need to know that its tried-and-true business savvy will help it succeed with each new market it enters.

That’s why this is truly a stock to hold for the long haul, as Amazon adds more growth from its hybrid sales approach.

Most tech stocks have staged impressive comebacks so far in 2019. However, in the next few weeks, we might witness a battle between investors and traders, where there will be considerable profit-taking in several of Wall Street’s tech darlings, including Netflix (NASDAQ:NFLX), PayPal(NASDAQ:PYPL) and Snap (NASDAQ:SNAP).

Like most tech stocks, NFLX, PYPL and SNAP are high momentum stocks. In other words, when the broader markets go up or when the company’s earnings beat expectations, both investors and momentum traders tend to hit the ‘buy’ button fast, expecting superior gains within days or weeks.

However, if markets suffer a decline or if the company cannot keep up with the rising expectations, investors’ risk appetite decreases fast and these stocks can fall much harder than less volatile stocks.

I am expecting some stock price weakness in the near-term in all these three stocks. If you already own any of the Netflix, PayPal or Snap stock, you might want to hold your position. However, within the parameters of your portfolio allocation and risk/return profile, you may consider placing a stop loss at about 5-7% below the current price point. Expect nearer-term trading in these stocks to sell to be choppy at best.

If you are an experienced investor in the options market, you may want to protect your portfolio with a covered call or possibly a put option spread with a 3-month time horizon. If you do not yet hold any of these stocks, you may want to wait several weeks to buy into the shares at the next dip.

With all of that in mind, here’s a deeper look into why these tech stocks might join many other “stocks to sell” lists in the upcoming days.

Netflix (NFLX)

Many investors have put Netflix in their sights as a possible stock to sell soon, as various headwinds have hammered down the positive sentiment surrounding its longer-term outlook.

Specifically, the price of NFLX stock went from an intraday low of $233.68 on Dec. 24 to an intraday high of $371.49 on Feb. 25. Netflix’s quarterly release on Jan. 17 showed that the company beat earnings with earnings-per-share of 30 cents per share. Although its overall numbers were strong, the company cut revenue projections for 2019.

Over the past decade, the company has increased annual revenues from $1.6 billion in 2009 to $15.8 billion in 2018.

With a trailing price-to-earnings ratio of 137, Netflix is a growth stock as well as a speculative stock. Analysts value NFLX stock on the expectation of continued high revenue growth that would lead to future profits. But whenever Wall Street fears the company is failing to meet growth or profit expectations, NFLX stock gets penalized. Hard.

Currently, the most critical metric investors pay attention to is Netflix’s subscriber growth. This number needs to remain strong every quarter to justify the high valuation. For the first quarter of 2019, NFLX is expecting to add 8.9 million paying subscribers.

However, new competitors, including Disney (NYSE:DIS), Amazon (NASDAQ:AMZN) and AT&T(NYSE:T), are increasingly entering the content distribution space. Before too long, the market might become oversaturated.

The upcoming competition from Disney is particularly daunting. Its new streaming service Disney+ will launch by the end of the year and include original movies and TV shows from Disney’s brands, including Marvel and Pixar. The platform is expected to concentrate largely on offering content for families. In preparation for this service, Disney is expected to pull its movies off Netflix. Both companies know that content is king.

Netflix’s current focus is on original content development as well as international expansion. Original content production is a costly business, as it requires the company to part with upfront cash and thus it contributes to Netflix’s negative cash flows. Therefore, as Netflix has to constantly borrow to keep on growing, it faces demanding pressure to ensure that it meets its growth targets. Otherwise, it cannot pay its debts easily.

If NFLX cannot keep up with the aggressive growth assumptions or increase its prices, especially in international markets, then its margins and the stock price would suffer. As these competitors make their mark in the marketplace in 2019, investors may decide to have a wait-and-see attitude, pressuring the recent price gains.

Disney’s ESPN+ platform — the DTC sports entertainment video service — already has over 2 million subscribers. On Apr. 11, Disney will hold an investor day when it will provide a first look at Disney+ and its original content. Meanwhile, on Mar. 25, Apple will also hold an event, where the company is expected to announce its new TV service to rival Netflix. Around both dates, I am expecting volatility in NFLX stock.

Shorter-Term Technical Analysis: Year-to-date, the NFLX stock price is up over 33%. Shorter-term momentum indicators, which describe the speed at which prices move over a given period, have become extremely overbought as a result.

Although these indicators can stay overbought for quite a long time, it would not be not surprising to see some profit-taking following the earnings report.

In other words, the excessive uptrend we have witnessed over the past month, cannot possibly be sustained. The level I’d be watching is $335. If Netflix stock approaches this level, I’d take it as an early warning that price risk is likely to increase.

If you believe in the fundamental bull case for Netflix stock, you might consider waiting for a better time to go long, such as around the low-$300’s or even upper $280’s.

For now, NFLX remains one of the top tech stocks investors are likely to sell in the upcoming weeks.

PayPal (PYPL)

Global online payments company Paypal is also one of the tech stocks that will likely be joining investors’ stocks to sell lists soon.

The price of PYPL stock went from an intraday low of $76.7 on Dec. 24 to an intraday high of $99.45 on Mar. 1.

As fintech competition is heating up, this pioneering company in the digital payments sector still dominates the first-person payments sphere. It has 267 million customer accounts, 21 million of which are merchant accounts. Unlike Netflix, PayPal is a cash generating machine.

When PayPal reported earnings on Jan. 30, it met revenue expectations for the quarter which rose 13% to $4.23 billion. Its adjusted earnings came at 69 cents per share, up 26% from a year ago. The growth in total transaction volumes and in the number of active users was behind the impressive numbers. However, its revenue forecast for 2019 was about 1% below analyst’s estimates and thus, PYPL stock went down the next day.

As a digital wallet, PayPal’s profitable business model depends on processing personal and merchant customer transactions on its global suite of payments platforms. In 2013, when PayPal acquired Braintree, which specializes in payment systems for e-commerce ventures, it also became the owner of Venmo, a peer-to-peer (P2P) mobile payment app. Sending money electronically peer-to-peer with a few taps has taken off among U.S. consumers.

In this market, which is expected to grow by double-digits in the next few years, Venmo has almost 25 million users and is ahead of its closest competitors. According to the latest quarterly report, Venmo processed approximately $19 billion of total payment volume, up 80% year-over-year. Through Venmo, PayPal is reaching a younger customer base.

However, PYPL stock may fundamentally suffer in the coming months if negative global economic and political conditions dominate the headlines. In January, the International Monetary Fund (IMF) warned of a global economic decline as China — the world’s second-biggest economy — has been slowing down considerably.

Likewise, German markets have been particularly worried about the stall in the Chinese economy, as Germany exports heavily to China.

Furthermore, if we do not have a resolution to the U.S.-China trade war in early 2019, the markets may throw in the towel in frustration and another selloff might begin.

Finally, on Mar. 29, the United Kingdom is set to leave the European Union. The U.K. now finds itself without a clear path forward on Brexit. The U.K. and European financial markets are increasingly edgy about the outcome we may have on that day.

In other words, risks for the financial markets are skewed to the downside and in case of a global slowdown, the demand from PayPal customers may soften, denting the price of PYPL stock.

Shorter-Term Technical Analysis: YTD, the PayPal stock price is up over 15%. As in the case of the Netflix technical chart, shorter-term momentum indicators are overbought, signaling potential profit-taking in the shorter term.

In the next few weeks, I do not expect any substantial positive momentum to push the PYPL stock price over the psychologically significant $100 level. Even if it goes over $100, it is not likely to stay up for long.

The two levels I’d be watching are first $95 and then $85. If PayPal approaches $85, then there is likely to be further selling.

If you believe in the fundamental bull case for PayPal stock, you might consider waiting for a better time to go long, such as around the low-$80’s or even upper $70’s.

Snap (SNAP)

Snap Inc joins this list of tech stocks to sell in March as it is also demonstrating signs of near-term volatility. But the possible pain in SNAP stock can be attributed to reasons other than those that affect NFLX and PYPL.

The price of SNAP stock went from an intraday low of $4.82 on Dec. 21 to an intraday high of $10.29 on Feb. 25.

Since its Initial Public Offering in March 2017, SNAP investors have not had much reason to be pleased with the performance of SNAP stock. After an IPO price $17, and a subsequent high of almost $30, it has not rewarded its early shareholders.

However, when SNAP reported earnings Feb. 5, investors welcomed the revenue increase of 36%. Meanwhile, it posted a loss of 4 cents per share, vs. an expected loss of 7 cents a share; its net loss also improved by $158 million to a loss of $192 million. The next day, the price of SNAP was up over 30%.

Now, analysts seem divided as to what is next for the company from a fundamental standpoint. Will it be able to continue its positive growth trend and increase its user numbers? Or will it once again disappoint investors who fear that SNAP does not have a viable business model where it can monetize the app’s popularity?

In other words, Wall Street is currently debating whether every “cool” app will become a successful publicly traded company.

I believe it will take at least a few more quarterly reports to fully appreciate the fundamental story of Snap. But until we have a better picture of the execution of management in 2019, I expect SNAP stock to be volatile.

Shorter-Term Technical Analysis: YTD the price of SNAP stock is up over 80%. In the next few weeks, I do not expect any substantial positive momentum to push the stock price over the psychologically significant $10 level once again. Even if it goes over $10, it is not likely to stay up for long.

If you believe in the fundamental bull case for Snap stock, you might consider waiting for a better time to go long, such as between $7-$8.

As of this writing, Tezcan Gecgil did not hold a position in any of the aforementioned securities.

With my Dividend Hunter service, I provide a list of high-yield investments that I have deeply researched, and my analysis shows provide an attractive combination of current yield and dividend stability.

As a high-yield stock expert, I often get asked questions about other stocks or investments that are not on my recommendations list. Sometimes a question will show me a new, attractive income investment. Others are learning opportunities on what not to do when picking high-yield investments.

One investment category that generates a lot of questions is closed-end funds (CEFs).

A closed-end fund is an investment pool with shares that trade on the stock exchange. Investors are drawn to CEFs because many have double digit yields and most paid monthly dividends.

Unfortunately, with most closed-end funds there are usually more negatives than positives when evaluating one for investment potential. Here are a few of the problems you could see.

Opaque communications from management on how a CEF is managed. There are not a lot of reporting requirements and any information you find on a fund’s portfolio may be months old. I sometimes refer to the CEF universe as the swamp of managed investment products.

CEF shares can trade at a discount or premium to the net asset value (NAV). Fund sponsors do not redeem shares, so the only place to buy or sell is on the stock exchange. If you buy a fund trading at a premium, you are paying more than a dollar for a dollar’s worth of assets. Not a good deal. A CEF trading at a deep discount can be a danger sign that the management has been making some bad investments.

Dividends classified as return-of-capital (ROC) are a big danger sign. Technically, return-of-capital are dividends/distributions that are not from earned income such as dividends or interest. While there are types and circumstances where ROC is not destructive to a fund’s NAV, unless you know for sure where the ROC comes from, it’s a danger signal to a CEF’s long term viability.

To recap, the problem with many CEFs is that they are hard to analyze with several factors that on their face are dangerous to your long term investment success. With over 700 publicly traded CEF’s, it is too much work to dig a handful of good ones out of the majority of swamp muck. Here are three high yield CEF’s to dump now if you own them.

Cornerstone Strategic Value (NYSE: CLM) is a CEF with $570 million in assets that owns a portfolio of global equity (stocks) securities.

CLM currently yields over 20%. There are two big danger signals for this fund. First, it is trading at an 11% premium to NAV. The high yield has caused unwitting investors to bid up the share price to 11% above what they would be worth if the fund is liquidated.

The current monthly dividend is 20.53 cents per share. Out of that just one cent is earned income and two cents are capital gains. The remaining 19.3 cents per share is classified as ROC. Historically, most of the dividends have been ROC, which is reflected in the steadily deteriorating NAV.

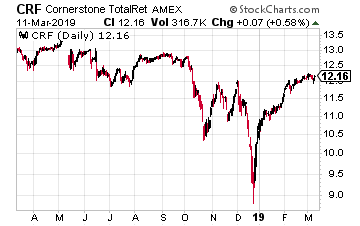

As typically happens, Cornerstone Total Return (NYSE: CRF) is a similar fund managed by the same advisory firm with the same problems.

This fund is trading at a 12.5% premium to NAV. That is very rich pricing in the CEF world.

The distributions breakdown also is like CLM. The current 19.85 cents month dividend has been paid for since the start of 2019. Each month 18.7 cents of the payout have been classified as return of capital.

Ignore the 20% yield and avoid or sell CRF.

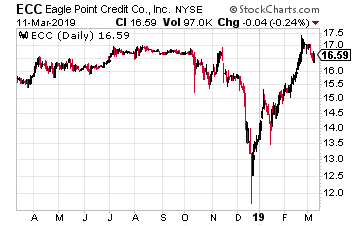

Eagle Point Credit Company LLC (NYSE: ECC)yields 14%. Due to recent large drops in the NAV, the shares trade at an eye-watering 23% premium to NAV.

Out of the 20 cents per share monthly dividends, 7 cents have recently been classified as ROC. Put another way, ECC is earning just 65% of the dividend it’s paying to shareholders.

Here’s the scariest part, the fund’s investment strategy: We seek to achieve our investment objectives by investing primarily in equity and junior debt tranches of CLOs. In plain English, they own the junkiest of the junk in the high-yield debt world.

After a brutal late 2018 selloff, financial markets have been on a healthy and stable recovery path thus far in 2019. Through the first three months of the year, the S&P 500 is up 12%, marking one of its best starts to a calendar year in recent memory.

As broader financial markets have stabilized, growth stocks have come back into favor. Indeed, one could say that they’ve done much more than come back into favor. Many of them have rushed to fresh all-time highs in 2019, and that’s after big corrections in late 2018. That means that a handful of these growth stocks have staged huge rallies over the past three months.

Which stocks fit into this category? And can these big rallies last?

These are questions investors should be asking as we head into what projects to be a more volatile time for financial markets throughout the balance of 2019. As such, let’s take a look at seven growth stocks which have raced to all-time highs in early 2019, and analyze whether or not their big rallies can continue.

iRobot (IRBT)

Why It’s at All-Time Highs: Shares of consumer robotics giant iRobot (NASDAQ:IRBT)have run up to all-time highs prices on the back of a strong double-beat-and-raise fourth-quarter earnings report that emphasized a few positive trends, including continued robust robotic vacuum market expansion, strong margin growth and a mitigated tariff impact.

Where It’s Going Next: The long-term IRBT growth narrative is positive. This company is morphing into a consumer robotics leader with minimal competition, and as such, will be a big revenue and profit grower for a lot longer as the consumer robotics space expands. Such big revenue and profit growth will keep IRBT stock on a long-term winning trajectory. But, in the near term, the valuation seems stretched at nearly 40x forward earnings. This stock needs to trade sideways for the foreseeable future to allow the fundamentals to catch up.

Shopify (SHOP)

Why It’s At All-Time Highs: Shares of e-commerce solutions provider Shopify (NYSE:SHOP) have notched new all-time highs thanks to renewed macroeconomic confidence and a strong Q4 earnings report in which growth hardly slowed and margins continued to move higher.

Where It’s Going Next: In the big picture, Shopify stock is powered by a secular growth narrative that goes something like this: the world is becoming increasingly decentralized thanks to technology democratizing creation and distribution processes. Shopify is enabling and empower this decentralization in the retail world. As this decentralization trend continues to play out over the next several years, Shopify’s merchant base will grow by leaps and bounds. Revenues will roar higher. Profits will, too. So will SHOP stock. As such, the long-term narrative here is very bullish — bullish enough to make this a long-term buy-and-hold stock.

Cronos (CRON)

Why It’s At All-Time Highs: Shares of Canadian cannabis company Cronos (NASDAQ:CRON) have more than doubled in 2019 and run to fresh all-time highs on the back of a multi-billion dollar investment from tobacco giant Altria (NYSE:MO). Investors have interpreted this investment as a major vote of confidence from a well respected global tobacco giant, at a time when global cannabis market fundamentals are improving. Consequently, they have bid up CRON stock to new highs.

Where It’s Going Next: The cannabis market projects to be really, really big one day. With a multi-billion dollar investment from Altria in its back pocket, Cronos has the necessary financial resources, business know-how, and distribution networks to one day turn into a major player in this global market. It’s fair to say that the stock has gone too far, too fast, and needs to cool off. This is likely what will happen. But, after that cooling off period, CRON stock will resume its uptrend, because the long-term fundamentals here of Cronos turning into a global cannabis giant are quite promising.

Wayfair (W)

Why It’s At All-Time Highs: Shares of online home retailer Wayfair (NYSE:W) have surged over the past few weeks to all-time highs thanks to two things. One, confidence in the macroeconomic environments in the U.S. and Europe has dramatically improved. Two, Wayfair’s margins finally stabilized last quarter, and that stabilization coupled with continued robust domestic and international growth served as justification for what had been several quarters of big investment. Investors rallied around those numbers, and bid up W stock to new highs.

Where It’s Going Next: Wayfair is a big growth story. This company has differentiated itself as the leader in a secular growth online home retail market, and this market is very big. Management pegs it at $600 billion in the U.S. and Europe. Revenues were under $7 billion last year, and grew by over 40% year-over-year. Thus, there is lots of runway for Wayfair to remain a big growth company for a lot longer. Having said that, the valuation is a tough pill to swallow here, especially with profit margins still very weak. As such, I wouldn’t chase this rally. But, I would buy any big dips.

The Trade Desk (TTD)

Why It’s At All-Time Highs: Programmatic advertising leader The Trade Desk (NASDAQ:TTD) has exploded to all-time highs over the past few weeks thanks to a robust double-beat-and-raise fourth quarter earnings report which underscored that this company’s growth narrative is still accelerating, and that big growth is here to stay for a lot longer.

Where It’s Going Next: The Trade Desk is a secular growth company powered by still accelerating tailwinds in automation and advertising. Over time, all $1 trillion worth of global ads will be transacted programmatically. That means that Trade Desk, which had under $3 billion in gross spend last year, has a huge opportunity in front of it to grow gross ad spend towards $100 billion-plus. If management successfully executes on that opportunity, TTD stock will head significantly higher in a long term window.

Etsy (ETSY)

Why It’s At All-Time Highs: Shares of Etsy (NASDAQ:ETSY) have surged to all-time highs over the past few weeks thanks to robust holiday numbers which were strong across the board, including robust community, sales, margin, and profit growth. Investors cheered those results, and bid up ETSY stock to fresh highs.

Where It’s Going Next: Etsy is a big growth company with strong growth drivers in e-commerce. But, there’s lots of competition here, from Amazon (NASDAQ:AMZN), eBay (NASDAQ:EBAY), and others. To be sure, Etsy has held off that competition, but that’s because Etsy dominates a niche of the market, meaning that growth won’t remain big forever. Eventually, it will tap out, and so will margins. That may happen sooner than most expect, and at over 60x forward earnings, a slowdown could be catastrophic for ETSY stock.

Chegg (CHGG)

Why It’s At All-Time Highs: Digital education platform Chegg (NASDAQ:CHGG) has roared to all-time highs on the back of a strong Q4 earnings report which included robust subscriber, revenue, and profit growth, as well as a healthy first quarter and fiscal 2019 guide.

Where It’s Going Next: CHGG stock will head higher from here. Why? Because the company is the unchallenged leader in the digital education market, and that market is far bigger than what the company is currently penetrating. At scale, Chegg will transform into a must-have digital education tool for all high school and college students. It is only a fraction of that today. As such, big growth is here stay for a lot longer. Such big growth is also accompanied by big margins. The combination of big growth and big margins will inevitably power CHGG stock higher in the long run.

It has been a challenging start to 2019 for real estate investment trust (REIT) investors. At the start of the year, the REIT indexes zoomed higher. The last few weeks have investors wonder if the party is already over for the year.

The financial media is placing blame in many places including trade wars, slowing growth and interest rate uncertainty. Many believe interest rates on the long end of the yield curve could rise with the growing Federal deficit. Which if true does not give confidence in REIT values. Fortunately, history shows that the belief that rising interest rates are bad for REITs value is a false assumption.

The current doldrums for the REIT sector may likely end up as a great buying opportunity for future gains.

Both Forbes and the NAREIT website note that historically, REITs have generated returns greater than the S&P 500 during periods of rising rates. How can this happen? As income investments, investors tend to lump REITs in with fixed income investments, i.e. bonds.

When interest rates go up, mathematically bond prices must fall producing negative returns for bond investors. REIT shares are ownership stakes in businesses. Rising interest rates are usually the result of economic growth.

For the REIT sector, an improving economy typically means rising commercial property values and the potential to increase rental rates. A significant portion of the REIT sector sees significantly greater benefits from economic growth than they experience from higher interest expense.

These factors are especially true in the current market. Companies have had several years to prepare for higher rates. This means that well managed REITs have locked in low interest rates with long-term fixed rate debt. These REITs should be able to improve profit margins by boosting lease rates, even as they keep interest expenses low.

There are REITs to avoid. Stay away from any companies that have variable rate borrowing costs. These will see profits squeezed by rising rates.

Avoid REITs that do not have histories of dividend growth. Part of staying ahead of rising rates is to own those REITs that can grow dividends faster than the increases in interest rates and inflation. With the recent retrenchment in REIT values, you can find shares with very attractive yields.

The next step is to ferret out companies that will grow dividends at greater than the rate of inflation. Here are three to get started with.

MGM Growth Properties LLC (NYSE: MGP) is a REIT that was spun-off by MGM Resorts International (NYSE: MGM) in April 2016. In the IPO MGP received ownership to a larger portion of the MGM owned real estate, primarily casino hotel resorts.

The properties are leased back to MGM Resorts on a long-term master net lease. Lease terms are very favorable for MGM Growth Properties. The master lease means that MGM makes a single lease payment and cannot get out of paying for individual properties. All new acquisitions from MGM are added to the master lease. The lease includes annual rent escalators and profit sharing from the portfolio resorts.

The MGP dividend has been increased five times since the IPO and is forecast to grow by 8% in 2019. As the name states, this is a growth focused REIT. They have made offers on Las Vegas properties not owned by MGM.

The stock currently yields 6.0%.

Hotels are a commercial real estate sector that benefit from economic growth and can quickly pass along higher costs as higher room rates.

Summit Hotel Properties, Inc. (NYSE: INN)recently announced very good 2018 results, with expectations of continued growth in 2019. Revenue per Available Room (RevPAR) is the metric to watch with hotel companies.

After two years of flat RevPAR, the metric took started to improve in 2018. Continued profit growth should lead to a 5% to 6% dividend increase this year. The current dividend rate is just 50% of FFO per share.

The continued positive economic outlook should allow INN to grow dividends in the high single digit range.

The stock yields 6.3%.

Kite Realty Group Trust (NYSE: KRG)neighborhood and community shopping centers in selected markets. These shopping centers are different from the malls and are integral to the function of the communities where they are located.

These properties are anchored by internet-resistant tenants like restaurants, grocers, entertainment, and specialty stores. Kite Realty has been a steady 5% per year dividend growth REIT. This will not change even if the investing public gets negative on anything that looks like a mall REIT.

In the retail sector there are great differences between different companies and the types of properties they own. Kite Realty is an undervalued, stable dividend growth REIT.

The current 8.4% yield makes KRG shares very attractive.

Today I’m going to peer into my crystal ball and give you the scoop on where high-yield closed-end funds (CEFs)might be headed in 2019.

Then I’ll give you a proven way to zero in on the ones that are the best bargains for your portfolio now.

CEFs Come Out Flying

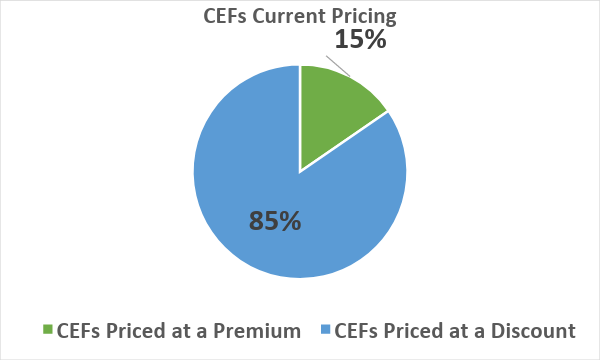

First, if you own stocks through CEFs (and if you don’t, click here to discover why these 7%+ payers are a retirement “must-have”), you’re already outrunning the market: my CEF Insider Equity Sub-Index—a great proxy for stock-owning CEFs—is up 13.7% since January 1, a nice lead on the S&P 500’s 12.3% gain.

Even better, CEFs are cruising upward without getting ahead of themselves—exactly what we want in a rock-solid income play. As you can see below, 85% of these funds are still cheap when you compare their market prices to their net asset values (NAVs, or the liquidation value of their portfolios):

CEFs Are Still Bargains …

Source: CEF Insider

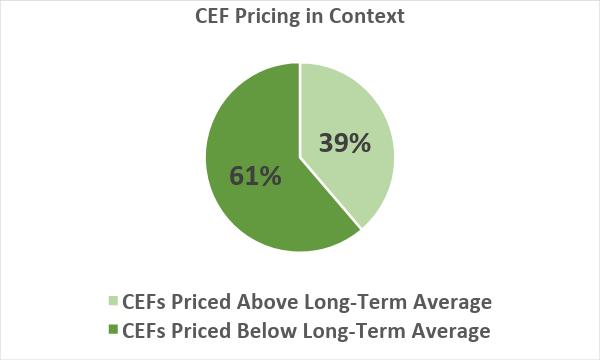

Even better for those of us on the hunt for cheap, outsized dividends, well over half of CEFs are trading at discounts bigger than their long-term averages:

… and Discounts Are Bigger Than Ever

Source: CEF Insider

That points to even more upside for us this year, as we tap the incredible 7%+ dividend payouts you can grab from CEFs (including the 18 in our CEF Insider service’s portfolio, which yield an outsized 7.3%, on average, as I write this)

Two Numbers Point to Big CEF Bargains (and Ripoffs, Too)

So how do we hone in on the highest, safest dividends in the CEF space while hedging our downside?

A great strategy (and one I use myself) is to look at funds where NAV and market-price returns vary widely, then spot whether this gap is justified by what’s happening in the market or in the fund itself.

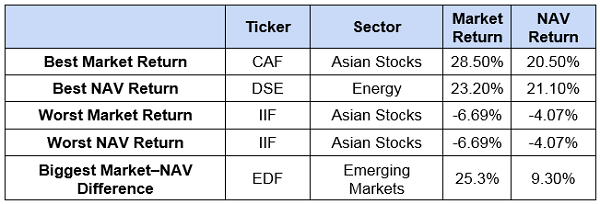

To see this in action, let’s look at the CEFs with the best and worst returns so far this year, by both market price and NAV, plus the fund with the biggest difference between the two:

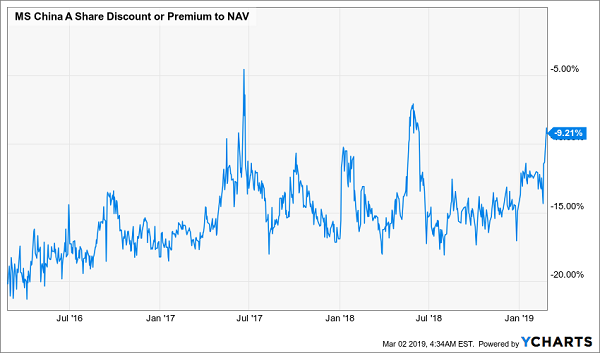

Let’s start with the Morgan Stanley China A Share Fund (CAF), which fell 18% on a NAV basis and 14.3% on a market-price basis in 2018. That mimicked the Chinese market, which dropped 19.2% last year.

Thus, the fund’s market-price and NAV rebounds in 2019 reflect investors returning to Chinese stocks, which is also driving CAF’s premium to spike suddenly—a common move for the fund after a selloff:

CAF Gets Pricey After a Huge Run

The risks here are clear, but they’re also pretty closely tied to those of Chinese stocks as a whole.

Let’s skip ahead to the India Fund (IIF), because the story there is similar. IIF’s weak NAV return and market return are the result of India’s economy, which is expected to see slowing growth in 2019 and 2020 after beginning to ratchet back in late 2018. Recent tensions with Pakistan don’t help things, so this fund’s decline is pretty rational and unsurprising.

Now let’s consider the Duff & Phelps Select Energy MLP & Midstream Energy Fund (DSE), whose huge NAV return is better than the energy sector’s 15.5% gain for 2019.

Part of DSE’s strong showing in 2019 stems from energy’s rise, but there’s something going on inside the fund, too. In late November, DSE began shifting from investing in energy MLPs to midstream MLPs, a more narrow sector that was extremely oversold in 2018, so has bounced back fast in 2019.

The timing of that change was particularly good, narrowing DSE’s discount slightly, to 9.9%, from where it was in November. Again, a rational response to a change in the fund’s fundamentals.

When a High Yield Signals Danger

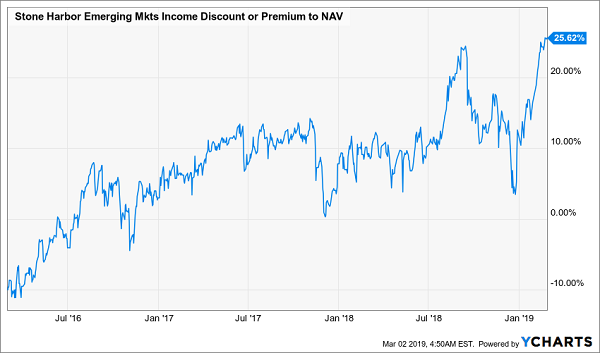

Finally, what’s up with the Stone Harbor Emerging Markets Income Fund (EDF) and the huge discrepancy between its market price and NAV returns? This is where we see the irrationality of the CEF world really shine through.

EDF is a poorly performing emerging-market fund with a high expense ratio (2.96%!). Despite those massive fees, the fund’s total NAV return over the last five years has been a measly 3.4% annualized, far below the S&P 500 and hundreds of other CEFs.

This is partly due to the complex emerging-market debt the fund invests in, partly due to fees and partly due to poor decisions, like holding over 10% of its assets in Argentinian debt (yes, the country that has defaulted more than once). This is a fund that should be sold cheap, but its current premium to NAV is not only one of the highest of any CEF, it’s at an all-time high:

Lousy Performance Brings … a Premium!?

Why has that premium been climbing lately? Yield-chasers are driving up its market price: EDF has never cut its dividend and now pays a shocking 15.9% yield. If you only look at that yield, this seems great. But unfortunately, EDF’s returns are less than a quarter of its yield, which means its dividend is not being covered by gains and will be cut.

And while first-level investors have driven EDF’s price sky-high, the fund is a rarity now; many CEFs are fairly priced (and quite a few are still cheap!), despite strong gains so far this year.

Yours Now: 8.3% Dividends and Big Gains From America’s Top Stocks

CEFs’ discounts to NAV make them hands down the best way to buy stocks.

Why?

Because these weird markdowns are basically free money! Why would you buy a “regular” stock when you could buy through a CEF and get it for 10% to 20% off? It’s a no-brainer!

And don’t let EDF’s spooky 16% dividend drive you away—there are plenty of CEFs paying safe high single- and double-digit dividends, and some even pay them monthly!

Take my 5 favorite CEF picks now (which I’ll reveal when you click right here). They throw off life-changing 8.3% average dividend payouts!

My top pick of the bunch holds some of the best stocks in the pharma and biotech sectors and has clobbered the market, with a monstrous 904% return since inception:

This Market-Slayer Is Still Cheap!

Plus, this fund throws off an incredible 9.8% dividend!

And as I write, this stout income play—which has traded at fat premiums many times in the past—goes for a totally unusual 7% discount. That sets us up for even more “bounce back” upside while we pocket that huge 9.8% payout!

Big technology companies have been under a lot of political and social pressure recently, mostly because said technology companies have become the be-all, end-all of society. The worry is that these companies are gaining too much power, and that too much power is never a good thing. Big technology companies that provide “free” services by monetizing user data have borne the brunt of it, as such companies are coming under heavy scrutiny for the way they use personal data to make money.

A lot of these concerns haven’t materialized into anything other than talk. But there’s one potential legislation which big tech investors should be aware of, if not concerned about: the data dividend.

The concept is simple: tech companies should pay you for your data. Your data is valuable. It’s being monetized broadly. Since you technically own your own data, when your data does get monetized broadly, you should get a piece of those rewards. That piece is the data dividend, and it would essentially amount to a percent of the company’s data-derived revenues.

The idea isn’t new. The academic world has been discussing the idea for some time. Washington state tried to pass data dividend legislation in 2017. But attempts to implement a data dividend have been too far and few between to mean anything. Until now. California Governor Gavin Newsom recently proposed the idea, and the proposition carries weight both because of when (amid heightened data privacy concerns) and where (California is home to many of the world’s tech giants, and is ahead of the curve when it comes to data protection laws) it was proposed.

As such, while it’s still far from a sure thing, a data dividend is now closer to reality than ever before. That’s bad news for any big tech company which uses consumer data to make money.

Which stocks are most affected by a potential data dividend? Let’s take a deeper look.

Facebook (FB)

Data-Related Revenue (% of Total Revenue): $55 billion (99%)

At the top of this list is a social-media giant which essentially makes all of its money from consumer data, meaning that essentially all of its revenues are theoretically subject to a data dividend.

Facebook (NASDAQ:FB) rakes in over $55 billion (and growing) in ad revenue per year. This money comes from advertisements across its four social media apps — Facebook, Instagram, Messenger and WhatsApp — and is all the byproduct of leveraging user data to incorporate relevant and targeted ads. Facebook is arguably the best in the business at using this data to create effective ad campaigns. They also have more data than pretty much anyone in the world.

But those positives also mean that Facebook could be a big loser if the data dividend idea gains national and global traction. Even if a data dividend amounts to just 2% of revenues, that would equate to over $1 billion per year for Facebook. And, that extra cost would come at a time when costs are dramatically rising for improved data protection.

In the big picture, the data-dividend risk isn’t a reason not to own FB stock. FB stock is a long-term winner supported by the stickiest digital ecosystem in the world. But it is something to be aware of and monitor.

Twitter (TWTR)

Data-Related Revenue (% of Total Revenue): $3 billion (100%)

The second of the possible data dividend stocks is another social media company, which makes essentially all of its money through either leveraging consumer data to create ad campaigns or just straight-up selling that consumer data.

Twitter (NYSE:TWTR) rakes in about $3 billion per year in data-related revenue. Roughly $2.6 billion of that is from ads — Twitter leverages user data to create targeted ad campaigns. The other $400 million-plus comes from Twitter’s data licensing business, which is essentially Twitter just selling user data. Thus, if a data dividend were to be introduced on a global scale, all of Twitter’s revenues would theoretically be subject to that dividend.

That’s not a great thing. But it’s not a deal breaker, either. Much like Facebook, Twitter has created an ultra-sticky digital service. That service is only getting stickier, as Twitter is increasingly becoming a go-to and irreplaceable platform for consumers of all shapes, sizes, and backgrounds to voice their opinion. Thus, while the data-dividend risk should be monitored, it isn’t a reason to sell TWTR stock.

Snap (SNAP)

Data-Related Revenue (% of Total Revenue): $1.2 billion (almost 100%)

Third of the data dividend stocks is yet another social media company that makes essentially of its money through digital advertising, which comprises leveraging user data for targeting purposes: Snap (NYSE:SNAP).

To be sure, Snap does have a hardware business through Spectacles. But that business has struggled to gain traction, and revenue from Spectacles thus far has been immaterial. Thus, of Snap’s $1.2 billion in revenue last year, almost all of it was from digital ads. That means almost all of it would be theoretically subject to a data dividend.

Again, this isn’t a deal breaker for Snap. But it is a bigger concern for Snap than it is for Facebook and Twitter. Why? Because Facebook and Twitter are already profitable, and they can absorb a 2% hit on revenues without materially impacting profitability. Snap cannot. The company is far from profitable, and needs a lot more scale in order to be profitable. Thus, the data dividend risk is much bigger for SNAP stock, than it is for FB or TWTR stock.

Alphabet (GOOGL,GOOG)

Data-Related Revenue (% of Total Revenue): $116 billion (85%)

The first non-social media company on this list also happens to be the world’s largest digital advertiser, and therefore bears substantial exposure to a potential data dividend.

Alphabet (NASDAQ:GOOG,GOOGL) isn’t all digital advertising. The company has hardware, cloud, and AI-related businesses which aren’t built on the back of user data. But Alphabet is mostly digital advertising. Of the company’s near $140 billion in revenue last year, about 85% of it came from digital advertising through Google, YouTube, and other online ad networks and properties. Thus, if a data dividend were to be implemented, Alphabet would have to pay a large sum back to consumers.

This isn’t a big deal for GOOG stock. For starter’s, Google is the backbone of the internet, and YouTube is very sticky in the free, online entertainment world. Neither of those ad businesses will be hit that hard by a data dividend. Also, of all major digital advertising players, Alphabet is the one of the most diversified, with burgeoning businesses in cloud, hardware, and AI.

Overall, then, any negative impact on GOOG stock from a data dividend will be mitigated by growth drivers elsewhere in the business.

Yelp (YELP)

Data-Related Revenue (% of Total Revenue): $907 million (96%)

Another company impacted by a potential data dividend isn’t known as a digital advertising giant, yet still derives a majority of its revenue from digital ads that leverage user data.

Yelp (NASDAQ:YELP) reported net revenue of roughly $943 million last year. About $907 million of that, or 96%, was from digital advertising. Thus, although Yelp doesn’t serve consumers ads in the same way that Facebook, Twitter, or Snap do, the company still runs ads based on user data, and those ads are the big driver of the company’s business. Consequently, a data dividend would theoretically be applied to Yelp’s entire business.

A data dividend is just another risk to add to the long list of things not to like about YELP stock, including valuation, competition, slowing growth, lack of scale, and lack of a moat. As such, there’s simply too much not to like here. The data dividend risk is just another reason to stay away from YELP stock.

Amazon (AMZN)

Data-Related Revenue (% of Total Revenue): $10 billion (~4%)

Although the next company on this list also isn’t known as a digital advertising giant, it is quickly building out a giant digital advertising business which is theoretically subject to a data dividend.

Amazon (NASDAQ:AMZN) isn’t known for digital ads. The company is known as an e-commerce and cloud giant. Nonetheless, Amazon is leveraging its huge user-base and reach across Amazon, IMDb, and other digital properties to create a huge and rapidly growing digital ad business. That digital ad business generated $10 billion in revenue last year. To be sure, that’s less than 5% of Amazon’s total revenues. But it’s a much bigger portion of profits (digital ad sales have way higher profit margins than e-commerce sales).

That fact alone is why the data dividend is actually a sizable risk for AMZN stock. Amazon has been counting on ramp in the digital ad business to drive profits higher, while margins in the e-commerce business remain largely weak due to competition. If the digital ad business gets set back due to a data dividend, that would be a set back to the whole Amazon profit growth narrative. As such, while the data dividend risk isn’t a deal-breaker, it is something which AMZN investors should closely monitor.

Microsoft (MSFT)

Data-Related Revenue (% of Total Revenue): More than $12 billion (more than 11%)

Last, but not least, is another big tech company which isn’t known for digital ads, but which nonetheless is one of America’s largest digital advertisers, and consequently has broad exposure to a potential data dividend.

Microsoft (NASDAQ:MSFT) isn’t known for digital advertising or using personal data to generate revenue. Still, the company has a big digital ad business. Microsoft’s search advertising revenues measured $7 billion last year. LinkedIn revenues were around $5.3 billion. The company also makes ad revenue through other segments, but doesn’t break that out. Thus, Microsoft’s total data-related ad revenues measured in excess of $12 billion last year, and likely closer towards $15-20 billion. That would represent about 15% of Microsoft’s total revenues.

Because Microsoft isn’t known for digital advertising, the data dividend risk isn’t a big deal for MSFT stock. The big growth narrative here is cloud, not digital ads. Thus, Microsoft can afford a set back in the digital ad business, so long as the cloud business remains healthy. At the end of the day, as go the cloud businesses, so goes MSFT stock.

As of this writing, Luke Lango was long FB, TWTR, GOOG, and AMZN.