Markets maintained their positive demeanor Wednesday, with oil up over 5% and minutes from the latests Federal Reserve meeting showing the Fed is willing to take a measured and patient approach to raising interest rates this year. While it was another up and down day, the major averages all finished in the green. News from the ongoing U.S./China trade talks was also encouraging with reports that both sides are making progress toward a resolution of the tariff war. Some analysts are pointing to the recent economic decline in China as an indicator that the country is under pressure to get a deal done even on less than favorable terms.

On the negative side of the ledger, it appears the partial government shutdown in D.C. may go on for an extended time. An address by the President Tuesday night, followed by a rebuttal from Democratic leaders, showed the parties no closer to a resolution than when the shutdown began. The public appeals were followed by a face-to-face meeting today which apparently ended with the President walking out and proclaiming the meeting a “waste of time”. January 15th will be the first day on which an additional round of government employees will not receive pay, adding to the growing impact of the shutdown.

Synnex Corporation (SNX) and FuelCell Energy (FCEL) report earnings Thursday. Synnex, an IT supply chain services company, has made a habit of falling after earnings announcements the past few quarters. But, the stock appears to have put in a solid support level around $75 the past few months. The company is expected to report $3.08 per share on Thursday, or an increase of 10.4% year-over-year on revenue of $5.4 billion. FuelCell Energy is expected to lose $.17 per share when it reports after the close Thursday. FCEL has dropped over 70% since last January and currently trades at less than $1.

Jobless claims will be released Thursday morning and are expected to come in at 224K. The claims number has been leveling off after touching a recent bottom in September 2018. Wholesale trade numbers, scheduled to be released Thursday, may be delayed due to the government shutdown, but they are expected to rise .4%. The inventory increase would be on par with growth in wholesale sales numbers reported earlier. Fed Chairman Powell is scheduled take part in discussions at the Economic Club of Washington at 12:45 pm. The Chairman’s remarks have given the market reason to rally the past week.

Due to declining oil prices at the end of 2018 the CPI is expected to drop between .1 and .2 percentage points for December when it is released Friday. Year-over-year numbers are projected to rise 1.9%. Falling housing prices have been partially offset by rising medical costs to keep the index elevated. The index has been relatively flat since May of 2018.

Infosys Limited (INFY) will report earnings before the open Friday. India based Infosys is expected to report flat operating margins as it has been spending heavily on upgrading its digital capabilities. Analysts will be focused on revenue growth and are looking for a possible announcement of a buyback of company shares.

The science of medicine, as well as pharmaceutical companies, is moving more and more toward personalized medicine. That is, specialized cell and gene therapies designed to attack a patient’s unique condition.

Curing a patient of once-fatal diseases will save our healthcare system an enormous amount of money… but only over the long-term. These treatments require enormous upfront outlays. Keep in mind that, in some cases, only one treatment is required to cure the patient.

And therein lies the problem – how can these ultra-expensive medicines be funded? One option is under serious consideration by several European drug companies – a “reinsurance model” in which a third party underwrites the catastrophic case of someone having one of these terrible conditions.

Pharma and Reinsurance

This solution seems to solve the problem. First, pharmaceutical companies will get paid for providing the life-saving treatment.

And for the reinsurance industry, which backstops insurance companies, helping healthcare systems and governments smooth out the costs of such treatments could provide an additional revenue source.

The industry could use an additional revenue source as reinsurers face increasing competition from rival sources of risk capital (private equity, etc.). Reinsurers could make financing for personalized treatments easier by pooling the costs of these treatments provided by different drug companies and also across countries.

The reinsurance industry already provides a backstop to employer health insurance plans, and has signaled a strong willingness to expand into the medical sector. In response to the Ebola crisis in West Africa, the World Bank in 2017 teamed with reinsurers to provide coverage against future pandemics, so outbreaks could be tackled quickly.

The world’s largest reinsurance companies include Berkshire Hathaway (NYSE: BRK.A & BRK.B) as well as the long-established European giants – Swiss Re (OTC: SSREY), Hannover Re (OTC: HVRRY) and Munich Re (OTC: MURGY).

The drug companies that are the most interested in teaming with reinsurance firms are the European drug giants. Let me explain…

Novartis – the Pioneer

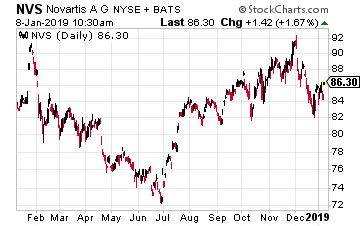

Leading the way here is the Swiss drug company Novartis (NYSE: NVS), which is also innovating in another promising area of medicine – digital therapeutics. I told you about this in the September 26 edition of The Market Cap.

The reason for Novartis interest in reinsurance is quite straightforward as explained by CEO Vas Narasimhan to the Financial Times: “Given that we’ll have five gene therapies in the clinic next year (2019) and we plan to continue to have a steady pace of gene therapies, we acknowledge we need to work with the system to come up with new solutions.”

Novartis has become a pioneer of “outcome-based pricing” models, through its blood cancer Car-T medicine Kymriah: 90% of children treated with the drug have not relapsed. It has offered to waive the $475,000 price tag for pediatric use in the U.S. if remission is not achieved within 30 days of treatment.

The company has also developed a gene therapy treatment for spinal muscular atrophy, a rare genetic condition that often kills sufferers before the age of two. Clinical trials suggest that, four years after a single treatment in the first few months of life, children are progressing normally.

The 10-year costs, if borne by healthcare systems, of treating such ultra-rare diseases range from $2 million to $5 million, according to economic analysis presented by Novartis at a recent investor day. So the need for unique solutions, like working with reinsurance companies, is obvious.

Novartis Is Not Alone

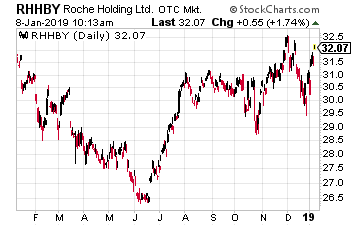

Novartis’ suggested reinsurance model is actually not a novel strategy in the healthcare industry. Its fellow Swiss drug giant RocheHoldings(OTC: RHHBY) has been working with the aforementioned reinsurance company Swiss Re to provide cancer treatments in China since 2012.

According to a 2010 agreement, Roche provides healthcare data to Swiss Re to help the latter tailor its insurance policies, and in return Swiss Re re-insures five Chinese insurers, thus circumventing Chinese laws banning foreign firms from selling insurance in the country.

And actually, Roche has been active in China since 2007 working with insurance firms and healthcare networks to develop policies that will cover cancer treatments and next-generation diagnostics. The country’s overall public health system is still that of a developing economy, making what Roche and Swiss Re are doing an absolute necessity.

With more than 4.2 million people diagnosed with the disease every year, cancer is a major public health problem and one of the leading causes of death in China. Most cancer patients in China have to pay for their treatment out of their own pocket, in spite of the government’s efforts to expand healthcare coverage. For some cancer medicines, a full treatment course can cost ten times the average Chinese worker’s annual income!

This approach for Roche has been very successful in China. In 2015, it started a partnership with the Shenzhen Reimbursement Authority and the leading Chinese insurance company Ping An. Shenzhen became the first city in China where all four of our targeted cancer therapies approved in the country – MabThera/Rituxan, Avastin, Herceptin and Tarceva – were reimbursed by Chinese insurance firms. Based on this success, Roche is expanding the model to include additional cities across China.

This just goes to show how creative approaches can improve access to healthcare, even in China. So now, Roche is adapting the model and rolling it out in countries around the world.

Two Winners

I absolutely love companies that think outside the box as these two drug companies. That alone makes them investment-worthy. Then add in the fact that both stocks are actually up in the past year – Novartis is up about 3% and Roche about 1% and with both yielding roughly 3.5% in very safe dividends – and you have two stocks to weather any sort of further market downturn.

A Pizza Company More Profitable Than Amazon? Forget Tesla, Amazon, Netflix and Google! A Pizza Company has beat every single one of these tech giants... and made its investors over 2,500% since 2010. It's all thanks to a $100 Trillion ‘Digital Helix’ and it could make YOU 2,537% profits if you act before November 29. Click here to find out more...

If you’re like many income investors I hear from, you’re probably worried that 2019 is already shaping up to be a repeat of 2008. The media doesn’t help – the talking heads like to conjure up fear because it draws eyeballs to the TV screen and clicks to Internet articles.

But what if they’re right? In a moment we’ll discuss the safest dividends for a serious pullback.

First, let me calm you down and add that a 2008 rerun is not our most likely scenario. As generals tend to fight the last war, investors tend to fear the last bear market. The next bear is likely to have its own unique “charm” – causes and effects – and we’d like to figure out that flavor ahead of time.

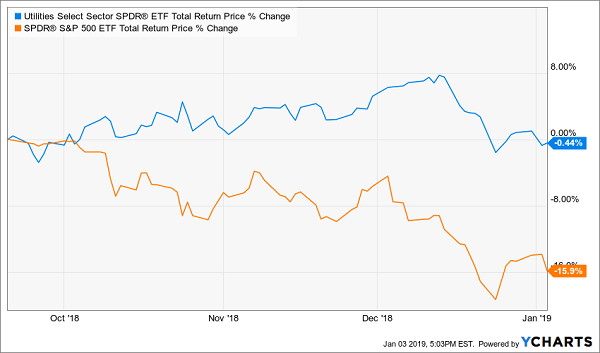

If there’s more to this pullback than we’ve seen, then its affinity for utility stocks is worth noting. The S&P 500 made its recent high on September 20, but don’t tell that to these dividend payers because they’ve shrugged off the broader market’s pullback

This Bear’s Favorite Buy: Utilities?

I’ve been down on the utility sector for two years now and have specifically picked on blue chips Duke Energy (DUK)and Southern Company (SO) repeatedly. I don’t have anything against these firms, but I also don’t recommend buying them when their stocks are pricey and their yields are low, as they are today.

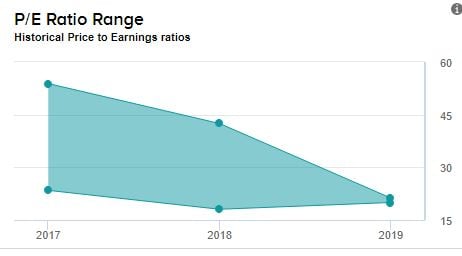

The problem with “dividend desperation” – paying too high a price for too low a yield – is that you end up collecting your payout but losing as much or more in price when the stock’s multiple contracts to its usual levels. And that’s exactly what’s played out with DUK and SO. Their price-to-earnings (P/E) ratios have contracted by 5% and 6% respectively as investors pay less for the same dividend. This has resulted in total returns of… not much:

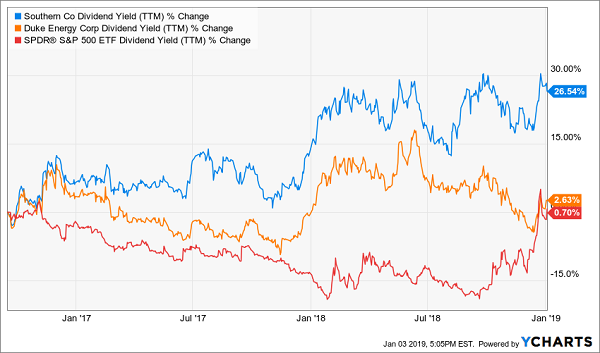

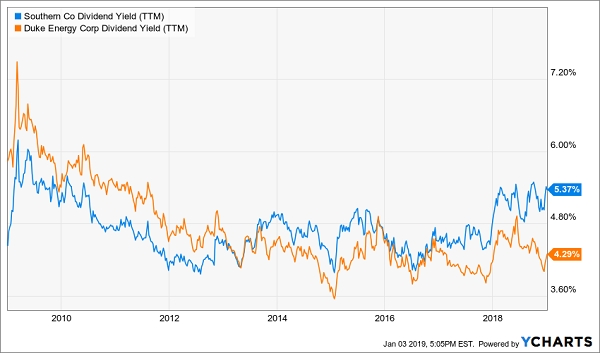

Our Utility Pans Treaded Water

Is this recent “divergence” between these two large utilities and the broader market a significant tell? Perhaps, but neither stock interests me yet because both are still pricey. Their current P/Es, still around 20, are higher than they’ve been over much of the past decade. And their yields, at 4.3% and 5.4% respectively for DUK and SO, aren’t yet high enough to qualify for our 8% No Withdrawal Portfolio.

Fortunately we don’t have to settle for these pedestrian utility yields or their expensive stock prices. We can run these stocks through my Dividend Conversion Machine to double their yields to 8%, 9% and more – without adding any additional risk!

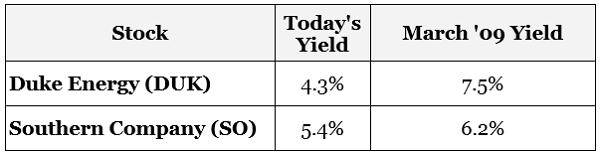

A Dividend Party Like It’s 2009

Nobody wants a repeat of 2008, but everyone wants another chance at 2009! Unfortunately most investors were too scared then to take advantage of once-in-a-lifetime yields. Our two utilities, for example, were paying their highest levels in years:

Generous Dividend Yields – For a Moment

More dividends for your dollar. Such were the “good times” that income investors could have enjoyed in 2009:

Just Released: How to “Force” a 7.5% Dividend From Duke Energy

I’ve found 4 mysterious “Dividend Conversion Machines” that let you rewind the clock: buy stocks like Duke, but instead of grabbing today’s 4.4% dividend, you’ll get the same incredible 7.5% CASH payout folks who bought in 2009 bagged instead!

But there’s a vital difference: you won’t have to take a stomach-churning plunge to get it, like you would have back then.

Sure, handy slogans like “Buy when there’s blood in the streets” are easy to say. But actually overcoming fear and hitting the buy button at a time like that is almost impossible for most people.

But with these 4 amazing “Dividend Conversion Machines,” you’ll grab the same massive dividend yields the best blue chips were paying in that fleeting moment back in 2009 right now—TODAY.

And these life-changing payouts are safe, backed by these very same household-name stocks.

Massive Upside and 7.5% to 8%+ Dividends—in 1 Buy

What’s more, you can grab these lofty payouts whenever you’re ready: all at once, on an automatic yearly or monthly schedule … or simply whenever you have new money to invest.

It’s all up to you!

Best of all, each of these 4 incredible investments are about to explode and give us massive price upside, too.

How massive?

I’m talking 20%+ yearly price gains, on top of dividends of 8%, 10% and up—without having to buy in the middle of a meltdown, like our 2009 buyers did.

Editor's Note: The stock market is way up – and that’s terrible news for us dividend investors. Yields haven’t been this low in decades! But there are still plenty of great opportunities to secure meaningful income if you know where to look. Brett Owens' latest report reveals how you can easily (and safely) rake in 8%+ dividends and never worry about drawing down your capital again. Click here for full details!

The market’s big headline to start 2019 was that tech juggernaut Apple(NASDAQ:AAPL) cut its first-quarter guidance because the world’s hottest economy, China, is rapidly slowing. The news chopped off 10% from an already beaten up Apple stock. It also brought the tech-heavy Nasdaq down 2%.

That makes sense. A lot of tech stocks have exposure to China. As such, if a monster like AAPL of them all is reporting considerable weakness in China, chances are high that almost every other tech stock is having trouble in China, too.

But, this doesn’t universally apply to the whole Nasdaq. There are a handful of tech stocks out there that don’t have any exposure to China. Yet, these stocks were also being sold off due to widespread and indiscriminate selling as a result of Apple’s weak guide.

From this perspective, there is opportunity in the early 2019 rubble. Broadly speaking, China is slowing rapidly, and that is significantly hurting Apple’s business. Every tech stock is dropping in response. But, there’s a handful of tech stocks that don’t have exposure to the rapidly slowing China economy. These are the stocks that are worth taking a look at during this sell-off.

With that in mind, let’s take a look at seven tech stocks that do not have China exposure.

Source: Shutterstock

At the top of this list is arguably the most troubled big tech stock in the market. But, it is also a big tech stock that has zero exposure to the China market.

It was a rough 2018 for Facebook (NASDAQ:FB). The social media and digital advertising giant was hit with a flurry of problems ranging from regulation to slowing growth to rising costs. All together, Facebook stock dropped about 25% in 2018, and currently trades at its lowest level in two years, and its all-time lowest valuation.

Because there has been so much weakness in Facebook stock, further weakness will need to actually be warranted by a drop in the fundamentals, not a drop in sentiment. Fortunately, the biggest fundamental risk to stocks right now is exposure to a rapidly slowing Chinese economy. Facebook has no such exposure, since its digital properties are largely blocked in China.

As such, with Facebook stock, you have a really beaten up stock trading at an all-time-low valuation, with zero exposure to one of the market’s biggest risks right now. That seems like an attractive combo which should provide downside protection for the foreseeable future.

Source: Shutterstock

Much like Facebook, digital advertising giant Alphabet (NASDAQ:GOOG, NASDAQ:GOOGL) had a rough 2018 due to regulation fears, slowing growth and rising costs. Also much like Facebook, GOOG stock now trades at a multiyear low valuation, yet has limited exposure to the China economy due to the Great China Firewall.

That is an attractive combination which implies healthy downside protection for the foreseeable future. But the upside thesis is from the notion that the sum of this company’s growth initiatives are being undervalued by the market.

We all know Google Search as the backbone of the internet. That positioning in and of itself is extremely valuable, and means the digital ad business is a stable growth machine. But, beyond that, Alphabet is also a leader in the nascent and rapidly growing AI, cloud, IoT, and self-driving markets.

With the stock trading at its lowest forward earnings multiple since 2016, the current valuation doesn’t seem to reflect much optimism regarding this company’s promising growth narrative. As such, the risk-reward on GOOG stock skews towards the upside here, especially with the stock closing in on a historically strong support level at $1,000.

Source: Shutterstock

Much like Facebook and Alphabet, social media company Twitter(NYSE:TWTR) does not have a presence in China. Also, unlike Facebook and Alphabet, Twitter’s growth rates and margins have actually been on an upward trajectory over the past several quarters. Yet, despite having zero exposure to one of the market’s biggest risks and coming off off a multi-quarter streak of revenue growth acceleration and margin expansion, Twitter stock has been hugely beaten up over the past several months. Since July 2018, the stock has fallen 40%. There are two big culprits behind the sell-off: user drops and valuation. User drop concerns are overstated. The company’s monthly active user base has dropped for two consecutive quarters, yet revenue growth has accelerated higher in each quarter. The reason for this is that the company is deleting “fake accounts.” That is technically shrinking the user base, but it’s also making it more authentic and valuable. Thus, ad revenues are still climbing, and that’s all that matters. On the valuation front, Twitter’s trailing P/S multiple has dropped from 14 in July 2018, to a much more industry-average level around 7.8 today. Thus, with user drop and valuation concerns now behind it, Twitter stock looks ready to bounce back from this sell-off.

Source: Shutterstock

Much like Facebook and Alphabet, social media company Twitter(NYSE:TWTR) does not have a presence in China. Also, unlike Facebook and Alphabet, Twitter’s growth rates and margins have actually been on an upward trajectory over the past several quarters.

Yet, despite having zero exposure to one of the market’s biggest risks and coming off off a multi-quarter streak of revenue growth acceleration and margin expansion, Twitter stock has been hugely beaten up over the past several months. Since July 2018, the stock has fallen 40%.

There are two big culprits behind the sell-off: user drops and valuation. User drop concerns are overstated. The company’s monthly active user base has dropped for two consecutive quarters, yet revenue growth has accelerated higher in each quarter. The reason for this is that the company is deleting “fake accounts.” That is technically shrinking the user base, but it’s also making it more authentic and valuable. Thus, ad revenues are still climbing, and that’s all that matters.

On the valuation front, Twitter’s trailing P/S multiple has dropped from 14 in July 2018, to a much more industry-average level around 7.8 today. Thus, with user drop and valuation concerns now behind it, Twitter stock looks ready to bounce back from this sell-off.

Source: Shutterstock

When you think about e-retail and cloud giant Amazon (NASDAQ:AMZN), you usually think about a company with global growth exposure. But, thanks to China’s own versions of Amazon, Alibaba (NYSE:BABA) and JD(NASDAQ:JD), Amazon has a very small presence in China.

Thus, the overall health of the Chinese economy doesn’t really impact Amazon’s ongoing operations. Instead, what impacts Amazon’s operations are the health of more developed markets like the U.S., Canada and Europe. Apple’s big update included some reassuring comments about developed market strength, while developed market economic data still remains broadly positive. Also, the 2018 holiday season appears to be have been a robust one, especially on the e-commerce front. The ad business continues to gain traction, and the cloud business remains the head-and-shoulders leader in a secular growth market.

All together, the fundamentals underlying AMZN stock remain favorable, despite a slowdown in China. At current levels, Amazon stock is trading at a multiyear low valuation. A multiyear low valuation on top of still-favorable fundamentals is a winning combination which should power Amazon stock higher in the near-to-medium term.

Much like Amazon, Shopify (NYSE:SHOP) is an e-commerce company with robust exposure to developed markets like the U.S. and limited exposure to developing markets like China. Given Apple’s comments regarding emerging market weakness and developed market strength, this is a favorable position to be in given the current global economic environment.

The near-term bull thesis on SHOP stock is compelling. This is a 50%-plus revenue growth company with expanding margins that just recently turned the corner into consistent profitability. Growth isn’t slowing by all that much, and analyst estimates have been consistently moving higher. Despite all that, the stock trades at its lowest P/S multiple since March 2017 — right before the stock doubled over the next six months.

The long-term bull thesis is even more compelling. The world is becoming more digital and more decentralized than ever before. Shopify exists in the overlap of these two trends. The company provides e-commerce solutions for retailers of all shapes and sizes, and in so doing, essentially serves as the e-commerce version of a storefront. Eventually, all retailers will need an e-commerce storefront, and most of them will turn to Shopify. Competition is muted. Growth is big. Gross margins are high. There’s lot to like here if you’re a long-term investors with a multiyear horizon.

Source: Shutterstock

One of the more obvious choices for this list is global streaming giant Netflix(NASDAQ:NFLX). Netflix doesn’t have a China presence, but they have a huge and rapidly growing presence everywhere else. Also, given Netflix’s price advantages over linear television packages, a global economic slowdown could actually help accelerate global Netflix adoption, especially in emerging markets.

As such, Apple’s big warning about rapidly slowing growth in China and other emerging markets isn’t big news for Netflix. Instead, the big news here is that Netflix’s original content continues to get better, more innovative, and more watched than ever before. For example, Black Mirror: Bandersnatch is a revolutionary interactive Netflix original that scored super high among fans, while Sandra Bullock-led Bird Box broke Netflix records for most viewers.

So long as Netflix maintains competitive pricing and continues to pump out quality original content, this global growth narrative will remain on track. That will help keep shares on a long-term uptrend. In the near term, the stock could get a boost as rate hike fears back off amid a rapidly slowing global economy.

An under-the-radar tech stock that has solid fundamentals and zero exposure to the slowing Chinese economy is digital education giant Chegg(NASDAQ:CHGG).

Chegg is a digital education company that builds connected learning tools for high school and college students across America. From this perspective, the company has zero exposure to China or any other emerging market. The growth fundamentals are aligned with a secular rise in digital consumption. And, the company’s operations are somewhat recession resilient since education is spend is one thing that likely won’t fall during an economic slowdown.

As such, with Chegg stock, you have a robust growth narrative with defensive qualities. That makes this stock an attractive addition to any portfolio during times of market turbulence.

As of this writing, Luke Lango was long AAPL, FB, GOOG, TWTR, AMZN, JD, SHOP, NFLX, and CHGG.

This ‘Overlooked’ Sector Produced the Biggest Winners of the Last Decade Wall Street is oblivious to it, yet you can earn 2,537% profits from an overlooked "blue chip" sector. The same group of stocks that has produced some of the biggest winners of the last 10 years. Investors have earned 618%, 834%, and up to 2,500% - performing better than Amazon, Netflix and Facebook. Click here to get in on your own 2,537% windfall.

Undoubtedly, most investors were hoping that the first rally of the New Year was going to stick around for more than just a few days. The jury is still out whether or not the market is going to continue its bearish trend. But, the surprising news from Apple (NASDAQ: AAPL) certainly casts a shadow over the brief glimmer of hope from investors.

In case you missed it, AAPL preannounced poor earnings based on slower than expected sales – primarily in China. The company lowered revenue guidance for the first time in 12 years and it sent a ripple through the markets. If one of the largest companies in the world is struggling, what’s that mean for everyone else?

It does seem to show that the trade/tariff war between the US and China is having real consequences on American companies. AAPL shares dropped 10% on the day after the announcement, with the S&P 500 pulling back 2.5%. Once again, that’s not the day bulls were hoping for after several up days in a row.

Given all the uncertainty in the market these days, it’s important for investors to understand the value of hedging. That is, every investor who owns stocks should know how to protect against downside risk. This includes those holding single stocks, ETFs, index funds, and other mutual funds.

Essentially, downside risk can be hedged with any asset that makes money as the market goes down. It’s a way to counter the losses you may incur from your long stock/fund positions. The easiest way to do this is with inverse ETFs and options.

Both inverse ETFs and options (long puts) are easy enough to implement as hedges. I’m going to focus on options in this article.

In most cases, simply buying a put option on the asset you want protected is all you need to do. A put option will only cost a fraction of the cost of the stock, so even if you lose money on the put (which is preferable) you won’t sacrifice your upside return all that much (in most cases). And since options use leverage, if your put pays off, it can cover most or all of your losses on the asset on a down move.

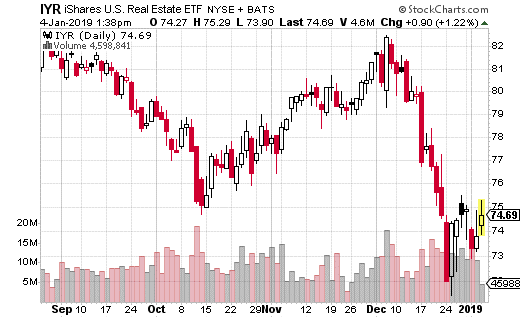

It’s easier to look at a hedge through an example. So here’s an actual hedge trade against real-estate stocks that recently hit the tape. By the way, that’s the beauty of an options hedge. You can pick the time frame you want, while protecting against any sort of asset class – as long as it has an ETF available (which is pretty much all of them).

The trade I’m referring to occurred in iShares US Real Estate ETF(NYSE: IYR). With IYR at $74, the trader purchased the January 11th 71.5 put for $0.32. This is essentially a one-week hedge that protects against the real estate ETF falling below $71 (technically $71.18 is the breakeven point).

The trader bought about 7,000 of these puts for roughly $220,000 in premium, which is also the max loss on the trade. However, if the market sells off sharply over the next week and takes real estate stocks down with it, the hedge will really pay off.

As a matter of fact, for every $1 below the breakeven point, the hedge will generate about $700,000. If you’re concerned about a short-term drop in real estate stock prices, this is a really good method of protecting your portfolio. Paying just $0.32 per option is a reasonable price to pay for downside protection for a week, especially given how volatile the market has been the last several months.

Stocks remained in positive territory Monday, though it was another volatile session, as investors remain hopeful that a trade deal can be worked out between the U.S. and China. The Chinese Trade Ministry released positive statements indicating the Chinese may be moving closer to negotiating a deal. Energy stocks helped market gains, as oil looks to have put in a near-term bottom and has finished higher the past 5 trading days. But, there was still no word on resolution of a partial U.S. government shutdown, as President Trump and House Democrats have not reached an agreement on funding a border wall with Mexico. Several government agencies, such as the TSA, have been able to find funding to pay workers through mid-January, but the extended shutdown will begin to be felt more severely if it continues through this week.

Helen of Troy (HELE) and AZZ Inc. (AZZ) report earnings on Tuesday. The consumer housewares company rewarded investors with an excellent year in 2018, and analysts are keen to delve into sales in the health and beauty line when Helen of Troy reports before the open. AZZ, a provider of specialized welding, galvanizing services and electrical equipment, may provide insight into recent weakness in Federal Reserve manufacturing numbers. The company is expected to earn $.61 per share on revenue of $241 million.

The NFIB Small Business Optimism Index, Redbook retail numbers, and job openings, or JOLTS data, will all be released Tuesday. The business optimism number is expected to drop to 104 from November’s 104.8. While the number is still high, November saw a decline from October and analysts believe the index may have topped and be heading into a downtrend. It is very likely the Redbook retail numbers will see a decline from the 9.3% year-over-year levels of last week, but that should be expected after the holiday buying season. Also on tap Wednesday is the kickoff of the Consumer Electronics Show (CES) in Las Vegas. The annual event has a slew of technology company CEOs delivering speeches. 5G smartphones, and highly anticipated 5G network content, are expected to be a major focus of the show this year.

Wednesday, investors will parse through the MBA mortgage application numbers as well as the EIA petroleum status report. Mortgage applications were off a horrendous 9.8% last week but may show signs of life after a drop in rates, which began after the first of November. Petroleum numbers are of particular interest to traders right now as they try to decipher whether oil truly found a bottom in late December, and where the market is headed from here. FOMC minutes will also be released Wednesday afternoon. It is unlikely the minutes will have much impact on the market, unless there are statements which contradict the softer stance Chairman Powell seemed to take in his panel discussion last week with former Fed Chairs Bernanke and Yellen.

In addition to mortgage application numbers on Wednesday, KB Homes (KBH) and Lennar Corporation (LEN) both report earnings. With homebuilder stocks beginning to show signs of a bottom, the earnings reports from the two companies are being closely watched. With a potential near term top in mortgage rates, both stocks have started off 2019 in positive territory. Analysts are hoping for an improvement in outlook from the two companies as possibly setting the stage for a turn, or at least stabilization, in the housing market.

Get up to 14 dividend paychecks per month from safe, reliable stocks with The Monthly Dividend Paycheck Calendar, an easy-to-use system that shows you which dividend stocks to pick, when to buy them, when you get paid your dividends, and how much. All you have to do is buy the stocks you like and tell them where to send your dividend payments. For more information Click Here.

Investing in stocks with strong dividend growth has historically proven to be a powerful total return strategy. Mathematically, for a stock to stay at a certain yield, the share price must increase at a rate that equals the annual dividend growth rate. Long term results show that dividend growth stocks produce average annual returns that end up very close to the average dividend growth rate plus the average dividend yield.

Energy infrastructure stocks have a long-term record of attractive current yields and steady dividend growth. These are the companies that own pipelines, storage facilities, and loading/unloading terminals.

The energy commodity crash of 2015-2016 forced a lot of companies providing infrastructure services to restructure their growth plans and strengthen the balance sheets. A further drag on the energy infrastructure sector was that many of the companies in the group were organized as master limited partnerships (MLPs).

Over the last three years, MLPs have gotten a bad rap from investors. Few investors want to jump into a sector where values are falling and there are additional tax reporting requirements.

While many energy midstream (another term for the infrastructure sector) companies chose to cut or stop growing dividend rates, a handful of quality businesses have continued or restarted dividend growth. However, the market has not rewarded stocks with growing dividends with higher share prices to match the dividend increases.

In the midstream group, dividend cuts have resulted in lower share prices, but dividend increases have not. Currently dividend growth by midstream companies has not resulted in matching share price gains. The result is attractively high yields and the likelihood that share prices could move significantly higher to match both recent and future dividend increases.

Let’s take a look at three high-yield stocks from the energy sector to consider for attractive total return potential going forward.

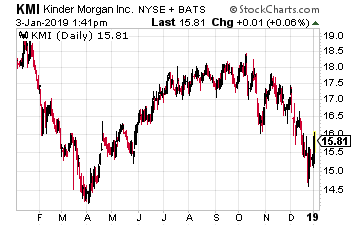

Kinder Morgan Inc. (NYSE: KMI) is one of the largest energy infrastructure companies in North America. The company owns an interest in or operate approximately 84,000 miles of pipelines and 152 terminals. The pipelines transport natural gas, gasoline, crude oil, carbon dioxide (CO2) and more. Terminals store and handle petroleum products, chemicals and other products.

At the beginning of 2016, the KMI dividend was slashed by 75% to a $0.50 per share annual rate. For the 2018 first quarter the dividend was increased by 60% to a current $0.80 annual rate.

Management has stated the dividend will increase by 25% for 2019 and 2020. Dividends are expected to continue to grow strongly after 2020. In contrast the KMI share price was above $22 at the end of 2016 and now trades around $16.

The market has not yet rewarded the strong resumption of dividend growth with a higher share price.

KMI yields 5.0%.

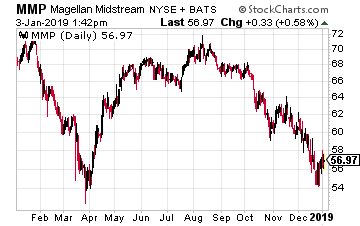

Magellan Midstream Partners LP (NYSE: MMP) is a publicly traded oil pipeline, storage and transportation company organized as an MLP. Currently, Magellan has 9,700-mile refined products pipeline system with 53 connected terminals as well as 26 independent terminals not connected to the pipeline system and an 1,100-mile ammonia pipeline system.

Also owned are 2,200 miles of crude oil pipelines and storage facilities with an aggregate storage capacity of about 28 million barrels, of which 17 million are used for leased storage.

The company operates five marine terminals located along coastal waterways with an aggregate storage capacity of approximately 26 million barrels.

For investors, Magellan has increased its dividend rate for 17 straight years. Unlike the typical MLP practice, the company has not issued additional equity to fund growth. Internal capital generation pays for growth projects.

The MMP distribution increases every quarter, currently at a high single digit growth rate yet the current unit price is down 28% over the last two years.

Current yield is 6.9%.

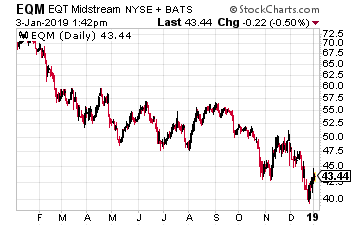

EQT Midstream Partners LP (NYSE: EQM) is an MLP that owns and operates a natural gas transmission and storage system serving the Marcellus and Utica basins.

The company owns a 950 mile FERC-regulated interstate gas pipeline that connects to seven interstate pipelines and is supported by 18 natural gas reservoirs. EQM has been a high distribution growth rate MLP, with the payout to investors growing at a 20% plus annual clip for the past five plus years.

Despite the distribution growth, the EQM value has dropped by 45% over the last two years.

Going forward, the company expects to continue distribution growth at a high single digit/low double digit rate.

Add that growth to the current 10% yield and you get very attractive total return potential.

Starting today you can stop worrying about the market and instead fundamentally transform your income stream from a string of near misses to a steady, reliable flow of income right into your bank account.Pay Your Bills for LIFE with These Dividend Stocks

Get your hands on my most comprehensive, step-by-step dividend plan yet. In just a few minutes, you will have a 36-month road map that could generate $4,804 (or more!) per month for life. It's the perfect supplement to Social Security and works even if the stock market tanks. Over 6,500 retirement investors have already followed the recommendations I've laid out.

Markets staged a rally Friday, recovering from Thursday losses brought on by Apple’s (AAPL) earnings warning. Following comments from Federal Reserve Chairman Powell, at a panel presentation with former Fed Chairs Yellen and Bernanke, that the Fed would watch the data and “be patient” with interest rates, markets kicked into high gear and rallied into the close. The DJIA finished almost 750 points higher and the Nasdaq jumped over 4% as markets rejoiced over what many hope is a softening stance at the Fed.

The comments were enough to overcome continued rancor in Washington as Democrats met with President Trump to discuss the federal budget and the ongoing partial government shutdown. Democrats emerged from the meeting commenting the President had said the shutdown could last for “months or years”. Investors will be watching meetings between China and the U.S. over the weekend for any possible break in negotiations over tariffs. A deal announcement, or even positive news on the tariff front, could fuel a further market rebound.

Commercial Metals Company (CMC) reports earnings Monday. The company painted a rosy picture for investors in its last conference call, reporting its “best quarterly performance since the great recession.” With operations in the U.S. and Poland, analysts will be looking for a gauge on both markets to help paint a picture of industrial vigor. With recent manufacturing numbers showing softness, CMC may be able to provide some clarity given what the the business seeing headed into the first quarter.

The ISM Non-Manufacturing Index, and the TD Ameritrade Investor Movement Index will both be released Monday. The scheduled release of factory orders will be delayed barring an end to the partial government shutdown. Analysts will have a keen interest in the December TD Ameritrade numbers as other measurements have indicated investors dumped stocks heading into year end 2018.

The rest of the week is data heavy as investors take on the first full week of trading in 2019. Tuesday, the small business optimism index and JOLTS numbers will be released. The release of a better than expected jobs number Friday, which initially goosed markets higher in the morning, will have analysts watching the job openings number closely. Mortgage application data, and the Fed meeting minutes, will be released on Wednesday. Investors are still wary of the housing market, which many hope will find some footing in 2019.

Jobless claims and wholesale trade numbers will both be released Thursday. Friday, analysts will focus on CPI, the Baker-Hughes rig count data, and the Treasury Budget. Analysts will be watching the rig count number closely to determine what impact the recent decline in oil has had, and to determine if the bottom has been put in for oil prices for the time being.

Earnings from a number of companies will be released next week. Helen of Troy Limited (HELE), AZZ, Inc. (AZZ) and Lindsay Corporation (LNN) all report Tuesday. Wednesday investors will hear from Bed Bath & Beyond (BBBY) and homebuilders KB Homes (KBH) and Lennar Corp. (LEN). The homebuilders face a tough market right now, and analysts will be looking for forward projections heading into 2019. Thursday investors will focus on earnings from FuelCell Energy (FCEL) and Synnex Corporation (SNX). Infosys (INFY) closes out the earnings week on Friday, before the earnings season kicks into high gear the following week. Pay Your Bills for LIFE with These Dividend Stocks

Get your hands on my most comprehensive, step-by-step dividend plan yet. In just a few minutes, you will have a 36-month road map that could generate $4,804 (or more!) per month for life. It's the perfect supplement to Social Security and works even if the stock market tanks. Over 6,500 retirement investors have already followed the recommendations I've laid out.

Yes, the markets are getting hammered like it’s 2008. But this isn’t because the world is coming to an end, or that the global economic system is about to fail.

This is about transition and risk.

The markets are undergoing a significant amount of transition as most central banks are relinquishing control over monetary policy and letting the markets sort it out. Add to that issue the fact that the Brexit mess is affecting one of the major global currencies.

There’s the fact that the U.S. economy continues to show signs of recovery — job growth is very strong, the participation rate is rising and wages are also increasing. Yet rising interest rates, the trade wars with Europe and China make that footing weaker.

For every bit a good news, there’s the shadow of bad news and the markets have never been a fan of uncertainty.

That’s why now is a great time to check out these nine A-rated safety stocks for a grossly oversold market. They’re highly rated in my Portfolio Grader, and with patience as the watchword now, these great stocks are selling at great prices.

Mr Cooper Group (COOP)

Source: Shutterstock

Mr Cooper Group (NASDAQ:COOP) may not be a household name — unless, of course you use it to start your household. It basically acquires companies that are focused on servicing, origination and transaction-based services for single family homes in the U.S. Its two biggest brands are Mr Cooper and Xome. It’s the leading non-bank mortgage servicer in the U.S.

This is one market that has been on both sides of the interest-rate roller coaster. When rates were high, home sales slowed, but when rates started to fall because of fears about the economy, that helped boost home sales and refinancings.

Its recent purchase of IBM’s (NYSE:IBM) Seterus mortgage servicing platform adds $24 billion of mortgages and 300,000 new customers to it rolls. It’s COOP’s second major purchase in 3 months.

Once this bumpy ride smooths, COOP will be well positioned.

Popular (BPOP)

Source: Shutterstock

Popular (NASDAQ:BPOP) is a holding company that operates financial institutions in the U.S., U.S. Virgin Islands and Puerto Rico. Its parent is Banco Popular de Puerto Rico, which was established in 1893.

Popular opened in the Bronx over 50 years ago and now has U.S. branches in New York, New Jersey and South Florida. Given the amount of Puerto Ricans that call the U.S. home, as well as other Latinos that are drawn by the bank’s roots in the Hispanic culture, BPOP offers a unique opportunity to take advantage of the demographic growth in this sector of the economy with an experienced, successful company.

Up 37% in the past year, and still delivering a 2.1% dividend yield, BPOP is doing very well in all this turmoil.

Medical Properties Trust (MPW)

Source: Shutterstock

Medical Properties Trust (NYSE:MPW) is the only medical real estate investment trust (REIT) that focuses solely on acute care facilities and hospitals where patients must be admitted by doctors.

Its goal is to blend the best of quality healthcare delivery and cost-effective management by maximizing operations management.

MPW started in 2003 and now sports a nearly $6 billion market cap. What’s more, it was up 17% in the past year, and that doesn’t include its generous 6.2% dividend.

It has recently moved into Europe with a big, multi-billion-dollar deal with a healthcare firm in Germany.

Qualys (QLYS)

Source: Shutterstock

Qualys (NASDAQ:QLYS) has done well in the past year, given the fact that it’s a tech stock.

But most of the credit goes to the fact that it’s a tech stock in the cybersecurity sector, and while that sector may have gotten a bit overpriced, it’s still something that is always in demand.

QLYS focuses on cloud security, which is one of the most in-demand aspects of cybersecurity since the growth in mobility and bandwidth demand have increased substantially. And the introduction of a new generation of data delivery — 5G — will make security even more important.

Also, with a market cap around $2.7 billion, QLYS is a tempting morsel for larger tech firms looking to expand their game in this space without having to build out from scratch.

Axon Enterprise (AAXN)

Source: Shutterstock

Axon Enterprise (NASDAQ:AAXN) is the new name for the TASER company, the folks that brought us the stun gun.

If you recall, a few years back there was an alarming number of fatalities linked to use of TASERs by law enforcement and others. Whether it was due to lack of training or abuse, the stain was largely put on the company.

But the name change as well as the company’s diversification into body-worn cameras for law enforcement has built a new line of products that have helped it diversify and regain its reputation as a reliable, non-lethal protection tool for professionals and citizens.

AAXN is up 71% in the past year and there is every reason to believe that kind of growth is achievable moving forward.

DSW (DSW)

Source: Shutterstock

DSW (NYSE:DSW), a big-box discount shoe retailer with more than 500 stores in the U.S., had great Q3 earnings and also raised its guidance for Q4. That happened at the beginning of December.

This is one of those brands that actually became stronger during the recession because that lost decade brought people in who weren’t regular customers previously.

There are two types of regular shoppers — the ones who go in like it’s a treasure hunt, looking for bargains on great shoes and the ones that like the fact that there’s a huge selection to choose from.

During slow economic times, everyone is looking for a deal and DSW is one of the beneficiaries. But now as times improve, it has added to its regular shoppers and instead of returning to premium stores, many shoppers choose to stick with DSW.

It’s why the stock is up 20% in the past year and still delivers a 3% dividend.

Evertec (NYSE:EVTC) is the leading payment processing company in Latin America. It operates in 26 Latin American companies, including Mexico and the Caribbean.

Financial technology, or “fintech” is a huge force in the way financial institutions are transitioning from the old style of banking, to the new digital style. And this affects every aspect of the business, especially between the financial institutions and the businesses that they support.

And these digital standards are especially important in emerging markets, where a traditional financial infrastructure can be tough to come by.

EVTC is up over 100% in the past year and is still only trading at a P/E of 29. There is plenty of growth left in the tank.

Brinker International (NYSE:EAT) owns the Chili’s Grill and Bar and Maggiano’s Little Italy chains. Most of the restaurants are company owned, although Chili’s does franchise some of its properties.

There has been a shift in tastes among customers and these large restaurant chains have begun appealing to new generations of potential diners. Healthier meals, different pricing structures, etc all have been implemented to keep the new breed of diners happy.

Some have had a tough time transitioning, but EAT has not been one of them. Up 15% in the last year, it also delivers a respectable 3.3% dividend.

Aerojet Rocketdyne Holdings (NYSE:AJRD) is a second-tier aerospace and defense contractor. Basically, that means it usually is a subcontractor to the big defense names when it comes to building rockets, propulsion and guidance systems. It also has a long relationship with NASA and other aerospace organizations.

While there is a lot of talk about private aerospace firms entering into the market, the fact is, there is huge potential for the best companies. And given the amount of aerospace work that lies ahead, AJRD will be a major player.

With talk of near-space commercial travel as well as missions to Mars, AJRD will have plenty of work. And the fact that it has been around in various iterations since 1914 shows that it knows how to adapt and thrive.This ‘Overlooked’ Sector Produced the Biggest Winners of the Last Decade Wall Street is oblivious to it, yet you can earn 2,537% profits from an overlooked "blue chip" sector. The same group of stocks that has produced some of the biggest winners of the last 10 years. Investors have earned 618%, 834%, and up to 2,500% - performing better than Amazon, Netflix and Facebook. Click here to get in on your own 2,537% windfall.

Semiconductor stocks are typically the forward indicators for technology stocks. So when Micron Technologies (NASDAQ: MU) confounded the markets with its consistent single-digit price-to-earnings ratio last year, investors should have exercised caution. The good news is that the patient investor may wait out the cyclical downturn in the chip sector. It will take another six to nine months before reaching a demand and supply equilibrium. Within the graphics chip space, Nvidia (NASDAQ: NVDA) has the clearest headwinds to work through. In knowing what inventory it needs to work through, NVDA stock could start recovering within one or two quarters.

Nvidia experienced excess inventory in the channels, which hurt its revenue forecasts. It blamed the crypto hangover for the excess supply imbalance. At significantly lower prices, cryptocurrency is not likely to recover any time soon. This is the bad news for anyone holding crypto. For NVDA and AdvancedMicro Devices (NASDAQ:AMD) shareholders, chances are good that the excess GPUs on the market will clear.

The two firms likely benefited from an increase in sales during the holiday season, after retailers offered rebates and discounts on graphics cards. Once the last-generation card supplies are cleared, game developers will embrace Nvidia’s ray-tracing. RTX card sales slumped in the last quarter and will be weak again for the next two quarters due to cheaper models still on the market.

The fact that Electronic Arts (NASDAQ:EA) was the only big name embracing RTX through its Battlefield 5 title did not help RTX sales. Worsening Nvidia’s near-term prospects was the significant drop in sales of BF V.

Market Opportunity for Ray-Tracing

Nvidia’s Turing brought ray-tracing to games, but pushes its technology forward through the Pro Visualization business. For the last 10 years, the industry simulated such effects as the reflection of light and rays of light bouncing off objects. Ray-tracing processes these effects in real-time. In performance terms, it should bring a 25% – 30% improvement over the Pascal architecture. And at the top-end, performance is 10-fold better.

Within the enterprise space, such as TV, film and Photoshop work, RTX will speed up the development of special effects. Nvidia inserted its graphics technology in around 1.5 million servers, which is worth a few billion dollars in business revenue. As companies slowly embrace RTX, investors should expect the company maintaining and even growing its profit margin.

At a $133 share price, NVDA stock is trading at a more reasonable multiple of around 19 times earnings. With earnings-per-share growth of 15.5% over the next five years, the stock is valued at a PEG of 1.20 times and 19 times forward earnings. AMD, despite falling to $18, still trades at a 30 times P/E multiple.

Fair Value

Analysts did not yet lower their price target on Nvidia. At a $228.50 average price target, based on 30 analysts, the 76% upside (per Tipranks) appears out of touch.

As shown in the table above, only one analyst from RBC Capital posted a report on Nvidia stock. The other analysts did not change their view in the last month.

NVDA Is Too Cheap to Ignore

At a P/E now in the teens, markets severely punished Nvidia for failing to forecast GPU demand.

The selloff, which started in October, is now over-done. When the company reports results in February, it will have a better idea on RTX sales for the year, along with the progress slimming down Polaris inventory.

Investors may consider starting a position in NVDA stock at these levels.

Get up to 14 dividend paychecks per month from safe, reliable stocks with The Monthly Dividend Paycheck Calendar, an easy-to-use system that shows you which dividend stocks to pick, when to buy them, when you get paid your dividends, and how much. All you have to do is buy the stocks you like and tell them where to send your dividend payments. For more information Click Here.

Kinder Morgan Inc. (NYSE: KMI) is one of the largest energy infrastructure companies in North America. The company owns an interest in or operate approximately 84,000 miles of pipelines and 152 terminals. The pipelines transport natural gas, gasoline, crude oil, carbon dioxide (CO2) and more. Terminals store and handle petroleum products, chemicals and other products.

Kinder Morgan Inc. (NYSE: KMI) is one of the largest energy infrastructure companies in North America. The company owns an interest in or operate approximately 84,000 miles of pipelines and 152 terminals. The pipelines transport natural gas, gasoline, crude oil, carbon dioxide (CO2) and more. Terminals store and handle petroleum products, chemicals and other products. Magellan Midstream Partners LP (NYSE: MMP) is a publicly traded oil pipeline, storage and transportation company organized as an MLP. Currently, Magellan has 9,700-mile refined products pipeline system with 53 connected terminals as well as 26 independent terminals not connected to the pipeline system and an 1,100-mile ammonia pipeline system.

Magellan Midstream Partners LP (NYSE: MMP) is a publicly traded oil pipeline, storage and transportation company organized as an MLP. Currently, Magellan has 9,700-mile refined products pipeline system with 53 connected terminals as well as 26 independent terminals not connected to the pipeline system and an 1,100-mile ammonia pipeline system. EQT Midstream Partners LP (NYSE: EQM) is an MLP that owns and operates a natural gas transmission and storage system serving the Marcellus and Utica basins.

EQT Midstream Partners LP (NYSE: EQM) is an MLP that owns and operates a natural gas transmission and storage system serving the Marcellus and Utica basins.