Investors who own individual stocks like to watch the markets and financial news websites for new information about the stocks they own. With some companies, there is news every week or every few days, and this stream of information can drive share prices up and down.

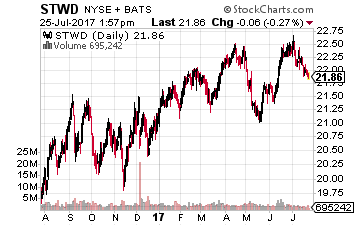

The flip-flops are hard to predict and are mentally draining. Starwood Property Trust, Inc. (NYSE: STWD) is a company that does not get much financial press coverage – which is a good thing.

Starwood Property Trust is a finance real estate investment trust, also called a REIT. The company’s primary business is the origination of commercial property mortgage loans. The loans are then held in Starwood’s portfolio. The company also operates a commercial mortgage servicing arm and owns a small portfolio of commercial real estate properties.

The finance REIT universe consists of about 30 publicly traded companies. Most of them operate in the residential mortgage space. The most common business model is to own a highly leveraged portfolio of residential mortgage backed securities (MBS) with the goal of profiting from the interest rate spread between short-term borrowing costs and the rate paid on MBS. That model is very sensitive to changes in both short and long-term interest rates.

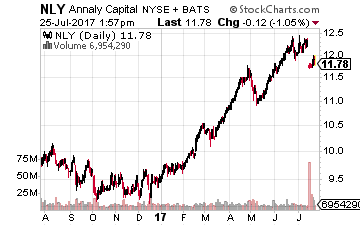

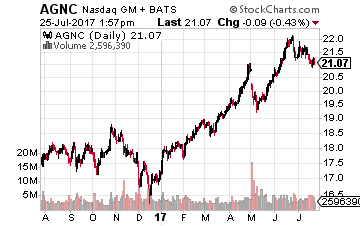

Investors familiar with the high yield residential MBS REITs may be surprised to learn that Starwood Property Trust is the third largest company by market cap in the sector. Only Annaly Capital Management, Inc. (NYSE: NLY) and AGNC Investment Corp (NASDAQ: AGNC) are valued higher than the STWD $5.7 billion market capitalization.

Investors familiar with the high yield residential MBS REITs may be surprised to learn that Starwood Property Trust is the third largest company by market cap in the sector. Only Annaly Capital Management, Inc. (NYSE: NLY) and AGNC Investment Corp (NASDAQ: AGNC) are valued higher than the STWD $5.7 billion market capitalization.

The larger finance REITs and many of the much smaller companies in the sector are the subjects of far more financial press coverage and analysis. The reason for the lack of news about Starwood Property  Trust is that the company is a safe and steady cash flow generator. There are no risks in the Starwood balance sheet or income statement that would give a financial writer something interesting to dig into for an article. Safe and conservative doesn’t sell in the financial news world. It sounds pretty good for an individual investment portfolio.

Trust is that the company is a safe and steady cash flow generator. There are no risks in the Starwood balance sheet or income statement that would give a financial writer something interesting to dig into for an article. Safe and conservative doesn’t sell in the financial news world. It sounds pretty good for an individual investment portfolio.

There are no risks in the Starwood balance sheet or income statement that would give a financial writer something interesting to dig into for an article. Safe and conservative doesn’t sell in the financial news world, but it sounds pretty good for an individual investment portfolio.

Consider these facts about the Starwood Property Trust financials:

- STWD has a 1.4 times debt to equity balance sheet. The typical residential MBS REIT is leveraged 6 times or more to equity.

- In its commercial loan portfolio, STWD has a very conservative 63.3% loan-to-value. Starwood has never booked a commercial mortgage loss.

- With eight years as a public company, STWD has never reduced its dividend rate. The dividend has been increased several times in the company’s history. The current $0.48 per share quarterly payout has been in effect for three years. Most of the residential mortgage REITs have slashed dividends during the last three years.

- Starwood has been making selective commercial property acquisitions that enhance the long-term stability of the company’s revenue and free cash flow stream.

The bottom line is that Starwood Property Trust gets little financial news press because it is so well run that writers and analysts can’t find anything that would cause problems for the company. This is a dividend paying stock that will not fluctuate much in share price and will pay that attractive dividend quarter after quarter. With a current 8.7% yield, it is a good time to initiate or add to a position in STWD. I very much like the idea of earning near 9% without drama.

Turning your retirement savings into a consistent stream of income is no easy task. You might spend hours researching what stocks to buy, only to end up with more questions than answers.

There are thousands of stocks to choose from, but only a small percentage of that group are the right stocks for you to own. The best high-yield stocks need to have safe long-term businesses that print money every year no matter what the market does. Those are the only companies that can pay consistent dividends.

That’s a tall task for most companies, and unless you have a degree in finance or worked on Wall Street, picking the best companies to own, out of all of the other ones, is an extremely difficult task.