Although stocks have experienced a rough ride in 2018, some stocks still have a big chance to shine through year-end. The best stocks to buy now go above and beyond the normal growth prospects. While looking for these kinds of investments, I examined six of the best stocks to invest in, all with huge upside potential and support from the Street’s top analysts.

The best way to find these stocks is with TipRanks’ Top Analyst Stocks tool.

Why? Well, the tool reveals all stocks with strong buy ratings from Wall Street’s best-performing analysts. You can then sort the stocks by upside potential to pinpoint compelling investing opportunities.

At the same time, I was careful to avoid stocks that have big upside potential simply because share prices have crashed recently. Check the price movement over the last three months to be sure shares are moving in the right direction.

With that being said, let’s get straight down into taking a closer look at these six stocks to buy now — all of which I believe look undervalued.

Stocks to Buy Now: Cloudera (CLDR)

Big-Data cruncher Cloudera (NYSE:CLDR) has upside potential of 100% say the Street’s top analysts! Currently, the stock is trading at $11.37 but analysts see it hitting $22.88 in the coming months. The stock has experienced some volatility this year, but it is now in a very promising setup. Indeed, since its downturn in April, Cloudera has surged 50%!

Michael Turits, a five-star analyst from Raymond James, reiterated his Cloudera “buy” rating yesterday at $24.

We can see from TipRanks that this ‘Strong Buy’ stock has a lot of Street support. Indeed, in the last three months, CLDR has received five buy ratings, including an upgrade from D.A. Davidson.

Stocks to Buy Now: Dave & Busters (PLAY)

The hybrid game arcade and restaurant chain Dave & Buster’s Entertainment (NASDAQ:PLAY) scored a rebound this year, but more upside is to come. Specifically, analysts expect 20.5% from the current share price — all the way from $59.18 to $71.29.

However, Maxim Group’s Stephen Anderson is more bullish than consensus — he believes the stock can soar to $71. Even though the stock has experienced some short-term sales volatility, he says that valuation remains very compelling.

Ealier, Anderson described PLAY stock as “deeply inexpensive relative to Casual Dining Peers” and ultimately: “Our core thesis on PLAY, which is comprised of; (1) high-margin entertainment revenue growth; (2) robust unit expansion; and (3) longer-term comp growth of at least 2%, remains intact.” PLAY should also benefit big-time from the upcoming tax reform.

In the last three months, PLAY has received an impressive seven consecutive buy ratings. As a result, the stock has a ‘Strong Buy’ analyst consensus. Out of these ratings, five come from best-performing analysts.

Stocks to Buy Now: CBS Corp (CBS)

Media stock CBS Corporation (NYSE:CBS) can climb nearly 20% in the next 12 months, say top analysts. This would see the stock trading at nearly $70 versus the current share price under $60.

Just a couple of days ago, Imperial Capital’s David Miller reiterated his “buy” rating. This was accompanied with a very bullish $71 price target. Miller expressed positivity in the outlook following strong fundamentals from “positive initiatives” put in place by the former CEO.

Previously, Benchmark’s Daniel Kurnos said, “that the demise of Network ad revenues is greatly exaggerated.” He even says that this bearish talk is overshadowing “the positive traction CBS is seeing in its ancillary revenue streams.” The underlying business model is very strong and “the pressure on the media sector has created a buying opportunity for the content leader.”

Meanwhile, out of nine recent ratings on CBS, six are buys. This means that in the last three months only three analysts have published hold ratings on the stock.

Stocks to Buy Now: Neurocrine (NBIX)

Neurocrine Biosciences’ (NASDAQ:NBIX) top analysts believe this biopharma still has serious growth potential left to run in 2019. Specifically, the Street sees NBIX rising from $87.17 to $137, or 57.16% upside.

The Street is buzzing about Neurocrine’s Ingrezza drug. This is the first FDA-approved treatment for adults with tardive dyskinesia (TD). A side effect of antipsychotic medication, TD is a disorder that leads to unintended muscle movements. Stifel analyst Paul Matteis is very optimistic, reiterating his recommendation with a price target at $140.

Encouragingly, the stock has received no less than 10 consecutive buy ratings from analysts in the last three months. Seven out of the 10 of these buy ratings are from top-performing analysts.

Stocks to Buy Now: Sinclair Broadcast (SBGI)

Sinclair Broadcast Group (NASDAQ:SBGI) is one of the U.S.’s largest and most diversified television station operators. SBGI stock has had a rough 2018, but top analysts see strong upside potential ahead.

Benchmark Capital previously named SBGI as one of its Best Ideas for 1H18. Five-star Benchmark analyst Daniel Kurnos says “We see SBGI as one of the best values in the entire media landscape.” He is now eyeing $38 as a potential price target, a double-digit gain from its current perch of $30.37.

According to Kurnos, Sinclair has multiple upcoming catalysts over the next six months. This includes the pending mega-deal between Sinclair and Tribune. Sinclair is currently waiting for regulatory approval for the $3.9 billion takeover that would give Sinclair control of 233 TV stations.

Top analysts are united in their bullish take on this strong buy stock. In the last three months, five analysts have published buy ratings on Sinclair.

Stocks to Buy Now: Laureate Education (LAUR)

Laureate Education (NASDAQ:LAUR) is the largest network of for-profit higher education institutions. This Baltimore-based stock owns and operates over 200 programs (on campus and online) in over 29 countries. Analysts believe impressive upside is on the way. Currently, this is still a relatively cheap stock to buy at just $14.99.

Barrington analyst Alexander Paris, just today, reiterated his “buy” rating on LAUR stock at $20, meaning upside of 34%!

Previously, Stifel Nicolaus analyst Shlomo Rosenbaum notes that Chile’s election result is a “material positive” for Laureate. He says new President Sebastian Pinera is less likely to support legislation for free post-secondary education- the prospect of which has dampened prices to date. Rosenbaum currently has an $18 price target on the stock.

Overall, Laureate certainly has the Street’s seal of approval. The stock has scored four top analyst buy ratings recently. This includes a bullish call from one of TipRanks’ Top 20 analysts for 2017, BMO Capital’s Jeffrey Silber.

Pay Your Bills for LIFE with These Dividend StocksGet your hands on my most comprehensive, step-by-step dividend plan yet. In just a few minutes, you will have a 36-month road map that could generate $4,804 (or more!) per month for life. It's the perfect supplement to Social Security and works even if the stock market tanks. Over 6,500 retirement investors have already followed the recommendations I've laid out.

Click here for complete details to start your plan today.

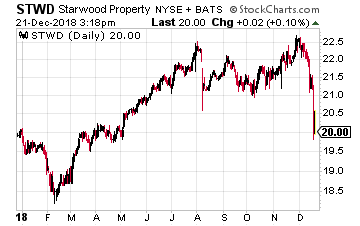

Starwood Property Trust (NYSE: STWD) is a commercial finance REIT. This means it originates mortgage loans for commercial properties, such as office buildings, hotels, and industrial buildings. Starwood has two commercial lending businesses. One is to make large dollar loans to retain in its portfolio.

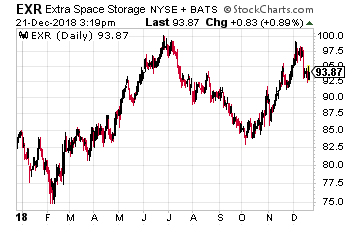

Starwood Property Trust (NYSE: STWD) is a commercial finance REIT. This means it originates mortgage loans for commercial properties, such as office buildings, hotels, and industrial buildings. Starwood has two commercial lending businesses. One is to make large dollar loans to retain in its portfolio. Self-storage REITs are the place to be when the economy gets rough for home ownership. Extra Space Storage (NYSE: EXR) is a large-cap, geographically diversified self-storage REIT.

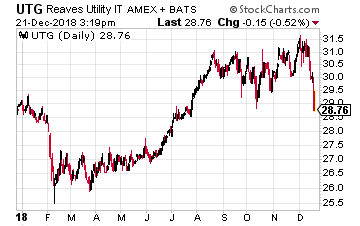

Self-storage REITs are the place to be when the economy gets rough for home ownership. Extra Space Storage (NYSE: EXR) is a large-cap, geographically diversified self-storage REIT. Utilities are supposed to be the safe sector when the stock market goes into a correction. This time utilities are down right along with the rest of the market sectors. Now is a great time to pick up shares of the Reaves Utility Income Fund NYSE: UTG).

Utilities are supposed to be the safe sector when the stock market goes into a correction. This time utilities are down right along with the rest of the market sectors. Now is a great time to pick up shares of the Reaves Utility Income Fund NYSE: UTG).