There are two phrases that can make investing seem a bit easier than it actually is: “The trend is your friend” and “A rising tide raises all boats.”

A perfect example to how these can distort your successful investing is the energy sector.

Energy prices are rising for a variety of reasons. One is OPEC nations are reducing supply to raise prices — remember, Saudi Arabia is funding a war in Yemen and Iran is trying to keep its economy going.

Two, the global economy is recovering, so the engines of growth are cranking up, so demand is growing. Crude oil — including West Texas Intermediate (WTI) — is sitting around $68 a barrel, with Brent around $73. Those are healthy levels compared to the sub-$50 level it was at for years.

But this trend isn’t necessarily your friend. And this rising tide won’t lift all boats in the energy patch; some are taking on water fast.

Below are 10 energy stocks that are leaking rather than sailing to open water.

Energy Stocks to Sell: Williams Partners (WPZ)

Williams Partners LP (NYSE:WPZ) is a master limited partnership that operates in the U.S. natural gas business. It operates natural gas — and natural gas liquids (NGLs) — pipelines and fracking in the Utica and Marcellus shales as well as around the Gulf of Mexico (Texas, Louisiana, Mississippi, Alabama).

It has been a tough business for a while now, as NGL pricing is very cyclical, and operations are also tied closely with economic growth. But as that trouble gets put behind WPZ, it faces a new challenge — the debt it has racked up in the meantime.

Also, in March the Federal Energy Regulatory Committee has taken away MLPs’ income tax break for cost of service rates. Part of MLPs’ attraction has been their tax-favored status.

WPZ recently sold off an NGL subsidiary to free up cash to pay down some of its debt, but that may not be enough.

There’s no reason to hold and hope — things could get ugly here.

Energy Stocks to Sell: Energy XXI Gulf Coast (EGC)

Source: Shutterstock

Energy XXI Gulf Coast Inc (NYSE:EGC) is a small exploration and production (E&P) company that operates offshore and onshore in the Gulf Coast.

Low prices forced the company into restructuring, which took all its shareholders down with it. That left them with a bad taste in their mouths as EGC has now reemerged and is trying to make up for lost time as prices for oil and natural gas begin to rise.

But EGC stock has been volatile and year to date is merely keeping its head above water.

EGC remains in a tenuous position and there’s no guarantee that a rebounding energy market will save it. What’s more, if the market reverses, EGC will be one of the first to suffer.

Energy Stocks to Sell: Advantage Oil & Gas (AAV)

Source: Shutterstock

Advantage Oil and Gas Ltd. (NYSE:AAV) is a Canadian E&P firm from Alberta, Canada that focuses on natural gas and NGLs.

At this point, AAV stock is off 24% year to date because gas prices remain low, which has meant AAV has had to reduce production. It also has tried to ramp up NGL production to compensate, but this isn’t as easy as flipping a switch.

Earlier this month, it updated it 2018 guidance and it wasn’t good. Because it’s fiddling with production, costs are rising, which will mean margins will be shrinking. That’s never a good thing.

The only real hope is rising gas prices or a huge upturn in NGL demand. And that’s not worth betting on.

Energy Stocks to Sell: NuStar Energy (NS)

Source: Shutterstock

NuStar Energy L.P. (NYSE:NS) is off more than 56% in the past year. It’s a pipeline and storage company based out of San Antonio.

The best news for NS, as it noted in its Q1 earnings statement released earlier this week, was that insurance will pay for a majority of damage done to its facilities by hurricanes last year.

Aside from that (and a whopping current dividend), there’s more risk than attraction here — the new FERC ruling getting rid of an important tax break for the industry; NS high level of debt; and increasing competition from other players are all making recovery difficult.

It has also delivered half the return on equity of the industry average (10%) in the past year. That’s a long road back, and there’s no point in joining its journey until its further along.

Energy Stocks to Sell: Contango (MCF)

Source: Shutterstock

Contango Oil & Gas Co (NYSEAMERICAN:MCF) had one piece of good news in its Q4 earnings released in early March — it lost less money in the quarter than it had the year before.

But aside from that, there wasn’t much to cheer about for the E&P player that works offshore in the Gulf off of Texas as well as in the Rocky Mountains.

MCF stock is off more than 50% over the past year, and this knife my still be falling. Onshore fracking is cheaper than offshore drilling and natural gas prices aren’t moving.

MCF isn’t a big enough operation to shunt production of one resource for another. So, while it’s true NGL prices are rising, it won’t do much for MCF’s bottom line.

Energy Stocks to Sell: Westmoreland Resource Partners (WMLP)

Source: Shutterstock

Westmoreland Resource Partners LP(NYSE:WMLP) is an MLP not in the oil and gas space, but in the coal sector. It is a surface miner that produces thermal coal.

While there remains demand for coal as an energy resource, this isn’t exactly a growth industry. And when you add to that the FERC ruling to limit tax advantages of MLPs, you start with two strikes for this stock.

So, what did its Q4 numbers reveal earlier this month? Strike three. Earnings were off 25% for the quarter and 13% for the year. While coal demand was up 18% in the U.S., it was off 41% for Canada.

There’s no doubt that coal will be a valuable resource for years to come, but it’s not the core energy source at this point. And betting on this niche in transition when there are so many better choices it far more risk than your likely reward is worth.

Energy Stocks to Sell: Hess Midstream Partners (HESM)

Hess Midstream Partners LP (NYSE:HESM) is a midstream player in the integrated Hess petroleum organization. It’s not unusual for integrated energy companies to spin off various upstream and downstream units to leverage performance in good times and deflect trouble in bad.

HESM is set up as an MLP, which means stockholders (technically called “unitholders”) are essentially business partners that receive their profits in the form of dividends. Right now, HESM stock is delivering a 6.3% dividend.

That may sound tantalizing, but when you realize HESM stock is trading nearly 20% off for the last year, it sounds less interesting, hopefully.

It released Q1 earnings this week and they weren’t bad … but they also weren’t good enough to have your money sit on the fence. Not even 6% is worth the risk at this point.

Energy Stocks to Sell: Ultrapar Participacoes (UGP)

Ultrapar Participacoes SA (ADR) (NYSE:UGP) is a Brazilian energy firm that focuses on storage, distribution and chemicals.

Basically the firm uses these imported energy products and sells them to the various markets that use oil, liquified petroleum gas (LPG) and NGLs for their products.

It’s a solid business but UGP stock is off 18% in the past year.

There are two key issues here. First, as energy prices rise, so will its inputs for selling NGLs and other variants. That means lower margins since not all the price increases will be distributed to vendors and customers.

Second, Brazil is an emerging economy that runs faster in both directions than developed nations. If the broader economy stumbles, it will hit Brazil’s economy much harder.

Given the volatility that’s already in place, there’s no reason to look for even more.

Energy Stocks to Sell: Camber Energy (CEI)

Camber Energy Inc (NYSE:CEI) is a small E&P that works mainly out of Texas and Oklahoma.

At this point the stock is off about 95% in the past year, so there isn’t much left of this company, at least unless it gets more oil out of the ground and to market.

Last month, it received another $1 million in funding from its sixth funding tranche. Basically that means it’s looking for more money to fund operations but isn’t in a position to go to a bank for funding. It’s going through investors.

The problem with this way of funding the company is, it dilutes the shares that current shareholders are holding. There’s nothing wrong with this kind of funding; small firms do it all the time.

The problem is, if you’re an investor while CEI is raising capital, there’s no guarantee your stock will be fully valued.

Energy Stocks to Sell: Ultra Petroleum (UPL)

Ultra Petroleum Corp (NADSAQ:UPL) is an independent E&P that owns properties in Wyoming and Utah.

In the past three years the stock is off a fulsome 82%. The fact that it has only two properties to seek its fortune is certainly a hindrance.

However, the one thing it has going for it is, UPL has been around since 1979, so it has seen its share of boom and bust cycles and has endured, if not thrived. It also has a $1.4 billion line of credit it can tap into, which is better than diluting shareholders’ positions by raising money through issuing more stock.

But that is little reason to invest.

If the big industrial firms are cautious on economic growth in coming quarters, then looking to buy beaten-down small-cap energy companies isn’t a good choice right now.

[FREE REPORT] Options Income Blueprint: 3 Proven Strategies to Earn More Cash Today Discover how to grab $577 to $2,175 every 7 days even if you have a small brokerage account or little experience... And it's as simple as using these 3 proven trading strategies for earning extra cash. They’re revealed in my new ebook, Options Income Blueprint: 3 Proven Strategies to Earn Extra Cash Today. You can get it right now absolutely FREE. Click here right now for your free copy and to start pulling in up to $2,175 in extra income every week.

Source: Investor Place

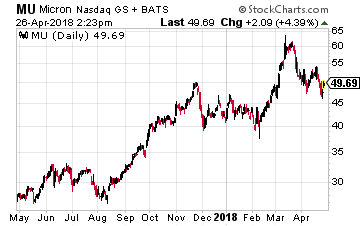

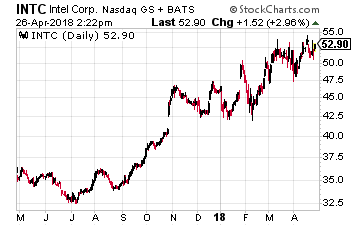

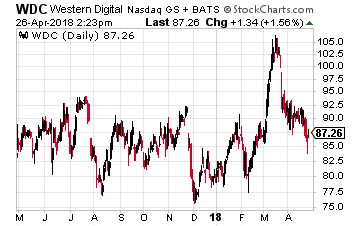

The company that is set to become China’s national champion in semiconductors is Tsinghua Unigroup. That name should be familiar to anyone that follows the chip industry. It made a $23 billion bid for Micron Technology (Nasdaq: MU) and tried to become a major shareholder in Western Digital (Nasdaq: WDC). But those moves were blocked by the U.S. government on national security grounds. So now it is going a different route.

The company that is set to become China’s national champion in semiconductors is Tsinghua Unigroup. That name should be familiar to anyone that follows the chip industry. It made a $23 billion bid for Micron Technology (Nasdaq: MU) and tried to become a major shareholder in Western Digital (Nasdaq: WDC). But those moves were blocked by the U.S. government on national security grounds. So now it is going a different route.

While China’s move is not good news for Samsung, it is so well diversified it will survive. Other companies will be much more affected including Sk Hynix, Toshiba, Western Digital (Nasdaq: WDC) and Micron Technology (Nasdaq: MU).

While China’s move is not good news for Samsung, it is so well diversified it will survive. Other companies will be much more affected including Sk Hynix, Toshiba, Western Digital (Nasdaq: WDC) and Micron Technology (Nasdaq: MU).

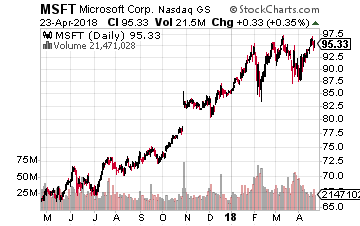

At the top of that stock list is Microsoft (Nasdaq: MSFT). When Satya Nadella first became the CEO, he said the company would pursue a “cloud-first, mobile-first” strategy. But in 2017, Nadella updated the strategy to say that Microsoft is all about the “intelligent cloud and intelligent edge.” The company has filed nearly 300 patents in the field.

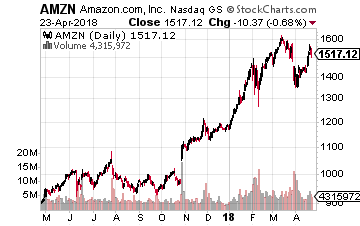

At the top of that stock list is Microsoft (Nasdaq: MSFT). When Satya Nadella first became the CEO, he said the company would pursue a “cloud-first, mobile-first” strategy. But in 2017, Nadella updated the strategy to say that Microsoft is all about the “intelligent cloud and intelligent edge.” The company has filed nearly 300 patents in the field. The next company is Amazon.com (Nasdaq: AMZN), which is the biggest public cloud provider with its AWS service. It has a product called Greengrass that provides a set of computing services directly on IoT devices when public cloud services are not available. Greengrass builds on top of AWS IoT and AWS Lambda, its serverless computing service.

The next company is Amazon.com (Nasdaq: AMZN), which is the biggest public cloud provider with its AWS service. It has a product called Greengrass that provides a set of computing services directly on IoT devices when public cloud services are not available. Greengrass builds on top of AWS IoT and AWS Lambda, its serverless computing service.

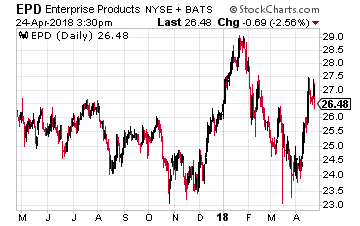

Enterprise Products Partners LP (NYSE: EPD) with a $57 billion market cap is the largest midstream MLP. The company provides the full range of energy infrastructure services. EPD is one of the biggest pipeline service providers to transport crude oil from the Permian to the Texas Gulf Coast. It recently announced that its 416-mile Midland-to-Sealy pipeline is now in full service with an expanded capacity of 540,000 barrels per day (BPD) and capable of transporting batched grades of crude oil.

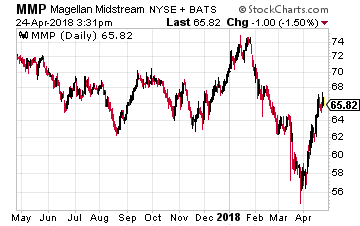

Enterprise Products Partners LP (NYSE: EPD) with a $57 billion market cap is the largest midstream MLP. The company provides the full range of energy infrastructure services. EPD is one of the biggest pipeline service providers to transport crude oil from the Permian to the Texas Gulf Coast. It recently announced that its 416-mile Midland-to-Sealy pipeline is now in full service with an expanded capacity of 540,000 barrels per day (BPD) and capable of transporting batched grades of crude oil. Magellan Midstream Partners LP (NYSE: MMP) primarily owns and operates refined products (gasoline, diesel fuel, jet fuel, etc.) pipelines and storage terminals. The company also owns 2,200 miles of interstate crude oil pipelines. The company provides service to almost 50% of the U.S. refining capacity.

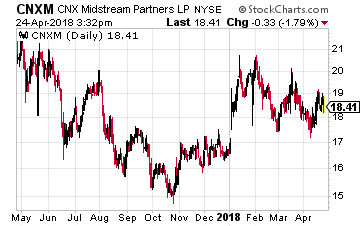

Magellan Midstream Partners LP (NYSE: MMP) primarily owns and operates refined products (gasoline, diesel fuel, jet fuel, etc.) pipelines and storage terminals. The company also owns 2,200 miles of interstate crude oil pipelines. The company provides service to almost 50% of the U.S. refining capacity. CNX Midstream Partners LP (NYSE: CNXM) owns, operates, develops and acquires gathering and other midstream energy assets to service natural gas production in the Appalachian Basin in Pennsylvania and West Virginia. This MLP primarily provides gathering and processing services to CNX Resources Corp (NYSE: CNX), which is also the sponsor and holds the MLP’s general partner interests.

CNX Midstream Partners LP (NYSE: CNXM) owns, operates, develops and acquires gathering and other midstream energy assets to service natural gas production in the Appalachian Basin in Pennsylvania and West Virginia. This MLP primarily provides gathering and processing services to CNX Resources Corp (NYSE: CNX), which is also the sponsor and holds the MLP’s general partner interests.