Earlier this month, a Georgia man pleaded guilty to securities fraud. That may not sound so unusual but bear with me.

This is unusual because even judged by the standards of great Wall Street crooks, this conman’s scam stands out.

For one, Syed Arham Arbab is hardly a would-be Master of the Universe. Instead, he’s a 22-year-old undergrad at the University of Georgia. Still, he was able to run a $1 million hedge fund, (or more accurately, Ponzi scheme), out of his frat house!

Let me repeat that again. He ran a phony hedge fund out of his fraternity house. (Whatever happened to keggers?)

I have several questions, and most of them strain credulity.

Arbab tricked 117 people into investing in his fake fund. Instead of going into stocks, the money was used for booze, gambling, and strip clubs. Shocking, I know.

Arbab admitted that he lied about his track to dozens of investors. He promised guaranteed risk-free returns of up to 56%. That’s an impressive track record even for being complete make-believe.

Arbab also confessed to the court that he told investors he was getting his MBA at the school’s Terry College of Business and that a famous NFL player and UGA alum had put money into the fund. In reality, Arbab was rejected from UGA’s MBA program, and the football player had never invested in his fund.

Ironically, the gambling and strip club was probably the closest he ever got to acting like a real hedge fund titan.

Honestly, I’m torn by stories like this. I feel bad for the victims, many of whom, I’m sure, lost their life-savings. Yet I have to wince when I think of their naivety. How could you trust a 22-year-old who was running the show out of his frat house?

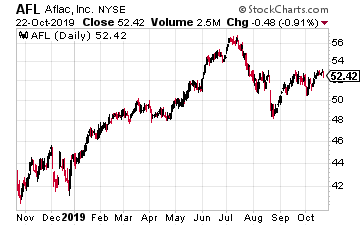

The example of Arbab is a perfect counterexample to one of my favorite stocks, also based in Georgia, which is AFLAC (AFL).

When most people hear the name AFLAC, they usually think of the duck ads. By the way, that’s now considered to be a legendary marketing campaign. In a few years, AFLAC’s name recognition went from 2% to 90% thanks to those duck ads.

But what many people, especially new investors, may not realize is what a sound and well-run company the duck stock is. Consider that AFLAC has increased its dividend every year for the last 37 years in a row.

AFLAC was founded in 1955, but its remarkable success began in 1970. That’s when John Amos visited the World’s Fair in Osaka, Japan. When he got there, he was astounded by the number of people who walked around the crowded cities wearing surgical masks.

Amos instantly recognized a golden business opportunity. Amos, along with his two brothers, ran a small insurance company based in Columbus, Georgia called the American Family Life Assurance Co. He figured that if people in surgical masks wouldn’t buy insurance, no one would.

In 1974, the Japanese government awarded American Family a monopoly on Japanese cancer insurance, which is very rare for a gaijin. The only reason they got it was because no Japanese firms were interested. Today, 95% of all the listed companies in Japan offer American Family’s products.

I’m going to let you in on a little secret Wall Street doesn’t want you to know about. Although it may appear to be boring, insurance is insanely profitable. Most investors have no idea of the goldmines they ignore just because insurance is dull as dirt. Warren Buffett built his investment empire on insurance.

Business has been going quite well for AFLAC. Three months ago, the company reported it made $1.13 per share for Q2. That topped estimates by six cents per share. Dan Amos, the current CEO and John’s nephew, said the duck stock aims to buy back $1.3 to $1.7 billion worth of stock this year.

AFLAC didn’t exactly raise guidance this summer, but they said that earnings should come in at the high end of their current range, which is $4.10 to $4.30 per share. That means the shares are going for a little over 12 times this year’s earnings. Earnings are due out again on Thursday, October 24.

Look for an earnings beat from the insurance stalwart…and steer clear of any frat house “geniuses.”

President Trump is now officially on the record as saying…

“The race to 5G is a race America must win, and it’s a race, frankly, that our great companies are now involved in.”

But here’s what Wall Street and the media won’t tell you…

The great companies Trump is referring to are NOT just Verizon, Sprint, or AT&T.

New evidence suggests Trump may have been referring to this secret 5G company. It’s not a household name… but experts say it’s ready for “Amazon-like” growth.

Get your hands on my most comprehensive, step-by-step dividend plan yet. In just a few minutes, you will have a 36-month road map that could generate $4,804 (or more!) per month for life. It's the perfect supplement to Social Security and works even if the stock market tanks. Over 6,500 retirement investors have already followed the recommendations I've laid out.

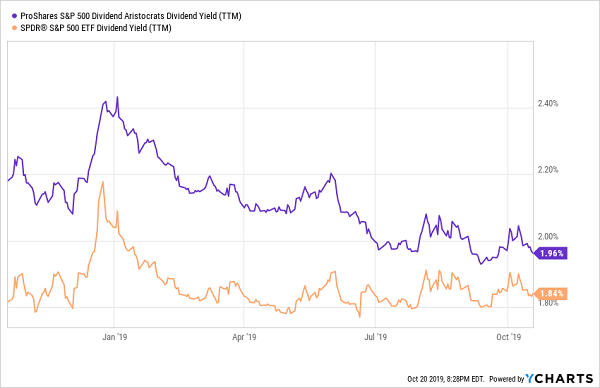

Dividend yields are so low today that dividend growth is actually becoming cool. Income investors are combing over “Dividend Aristocrats”–stocks that have raised their payouts for 25 straight years–in desperation to find any meaningful yield.

Problem is, these stocks are so popular and richly valued that they don’t pay much today. Nor will they yield much more tomorrow, even with yearly raises. Our princely picks pay less than 2% today, which is going to net you less than $20,000 on a million bucks.

Dividend Aristocrat Yields Head Towards Zero

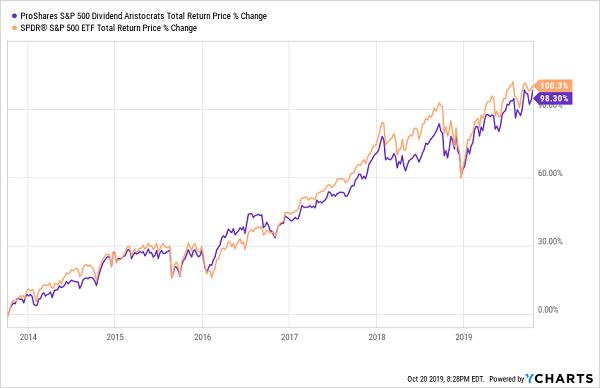

The Dividend Aristocrats are the well-worn, oft-recommended dividend growers of the S&P 500. All 57 Aristocrats have improved the amount of their total annual payouts every year for at least 25 years (and in many cases, they have done it for much longer.)

Yes, reliably increasing income matters. After all, the dividend-growth strategy in my Hidden Yields product is roughly doubling our money every four years with a 17%+ yearly return since inception.

But the Aristocrats are starting with too much of a handicap. As you can see above, the ProShares S&P 500 Dividend Aristocrats ETF’s (NOBL) yield is better than the market, but still below 2%.

The actual average among all 57 components isn’t much better, at 2.4%. In fact, only 13 components yield more than 3%. And just two—AT&T (T) and AbbVie (ABBV)—yield more than 5%.

That’d be OK if we were sacrificing high nominal yields for great price performance, but we’re not. In fact, NOBL has actually underperformed the S&P 500 since 2013 inception.

My take? Cherry pick ‘em. A few Aristocrats are truly royalty among the entire world of publicly traded stocks. Others actually have promising growth prospects that you wouldn’t expect from supposedly stodgy dividend plays.

Let’s look at a six-pack of the best and worst Dividend Aristocrats together.

McCormick & Co. (MKC) Dividend Yield: 1.4%

Let’s start with McCormick & Co. (MKC), a frequent cupboarder in American kitchens. Whether it’s the namesake spices, Old Bay seasoning, Stubb’s barbecue sauce, Zatarain’s rice mixes, French’s mustard or Frank’s Red Hot, our food has often been flavored up by its products.

In fact, you probably enjoy McCormick more often than you realize, given that it also provides spices and condiments to restaurants. Overseas, too, as its international reach spans roughly 150 countries and territories.

All this makes McCormick & Co. a recession-resistant play hiding in your pantry corner. When times are tight, folks eat out less and prepare more food at home.

Check out our last mega-recession as an example. While the S&P 500 was trashed during the bear market of 2007-09, MKC managed to tread the boiling water for most of the downturn:

Bam!

Its dividend, which has improved for 33 consecutive years, has grown by a nice 43% since the start of 2015. But it yields less than a 10-year T-note today, which is not good enough for us income seekers.

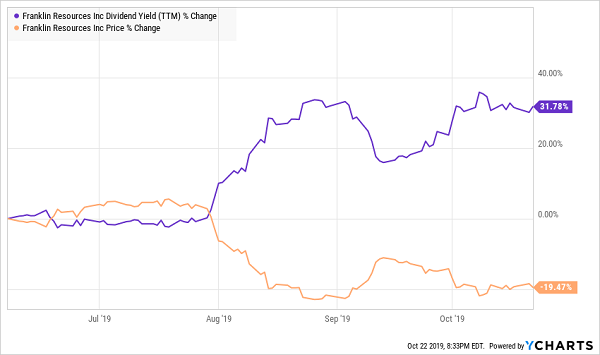

Franklin Resources (BEN) Dividend Yield: 3.8%

Franklin Resources (BEN), the name behind the Franklin Templeton investment firm, has expanded its payout for 37 years. Recently shares have jumped 73% since the start of 2015 plus the firm dished a generous $3-per-share special dividend at the start of 2018 as a way of giving back after the passage of the Tax Cuts and Jobs Act. That translated into an additional 9 percentage points of yield for the year!

However, Franklin’s yield has recently rocketed higher for the wrong reasons. Its business is in the tank, and the dividend looks increasingly dicey as a result.

In June, I highlighted BEN as one of several “zombie dividends” to sell. The company has been suffering from dwindling assets under management for years, and it was way behind the curve with ETFs, finally launching its first suite of passive products in 2017. Since we called out this loser, it quickly dropped 20%:

The Wrong Way to Increase Yield

Walmart (WMT) Dividend Yield: 2.8%

Walmart (WMT) is one of the few retailers that can compete with (and potentially topple) Amazon.com. Sales through Walmart’s website and mobile app are booming. Its e-commerce revenue is growing at a brisk 43% clip year-over-year.

In my college days at Cornell we operations research and industrial engineers (ORIE) actually studied Walmart’s supply chain. It was one of the finest examples of ORIE applied to market domination. “Wally World” is one of the few retailers positioned to compete with Jeff Bezos and Amazon on same-day delivery, thanks to its logistics expertise and deep bench of brick and mortar locations. Really the firm is one partnership with Uber away from getting you anything you want within the hour.

Clorox (CLX) is a consumer staple that needs no introduction. But to get an idea of just how wide its reach is, understand that Clorox is far more than just Clorox. It’s also Pine-Sol, Brita water filters, Fresh Step cat litters, Glad trash bags, Liquid Plumr, Burt’s Bees lip balms and even Hidden Valley ranch sauces.

These are durable brands that have no-brainer recession appeal. But the company is taking a decided step back.

Earlier this month, Clorox presided over a dour analyst meeting in which it cut its full-year guidance from $6.50-$6.30 per share to $6.25-$6.05 per share. That led to several price-target downgrades, including by JPMorgan’s Andrea Teixeira (Underweight rating), who trimmed her outlook from $143 per share to $137. What’s particularly concerning is she sees additional downside earnings risk.

There’s little criticizing CLX’s dividend growth. Payouts have been on the rise for 42 consecutive years, and have improved 43% since the start of 2015.

But the sub-3% yield is nothing to fawn over, especially given Clorox’s growth issues. It’s also curiously priced at 23 times profits.

Clorox’s (CLX) Merely Market-Matching Performance Could Slow Even More

Dover (DOV) Dividend Yield: 1.9%

Near the end of 2018, I told Market Wrap host Moe Ansari that the key to finding potential doublers is to home in on boring stocks.

And Dover (DOV) is a publicly traded bottle of ZzzQuil.

Dover is a diversified industrial that makes everything from product-tracing technologies to bench tools to chemical dispensing systems and even commercial refrigeration units. That kind of revenue diversification always keeps Dover in the game, and more importantly, it has helped finance one of the longest-standing payout increases among the Aristocrats.

Indeed, I mentioned Dover in July 2018. Since then, it has announced two more annual dividend increases to extend its streak to 64 years. It has also quadrupled the broader market with 43% in total returns.

The Saucy Side of Fluids and Food Equipment

Dover is a little pricey at the moment, but it should keep slowly churning out growth of about 3% annually over the next few years. The bottom line is what’s more encouraging–analysts are looking for a 17% bump this year and a still-respectable 8% improvement on top of that in 2020.

3M (MMM) Dividend Yield: 3.5%

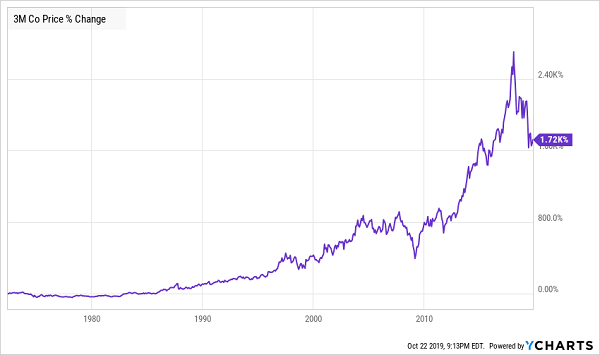

“Broken.”

That’s the word JPMorgan analyst Stephen Tusa used to describe 3M’s (MMM) business model in an early August note.

“There is something that goes beyond the impact of cyclical volume pressure here. (A) structural issue, that there is generally a higher cost to serve than many appreciate, now seems clear.”

It’s yet another sign of just how much has turned for what once was one of the most consistent blue chips on Wall Street. It’s currently mired in its sharpest decline in decades, a 35% drop since early 2018.

The industrial conglomerate that’s responsible for Post-it Notes, Scotch Brite and Nexcare bandages has delivered a few dismal reports in that time. That includes a ghastly earnings miss in April that saw it also cut its full-year forecast, announcement of the layoffs of 2,000 workers, and informed investors it was undergoing some restructuring and other measures to try to cut costs and boost cash flow.

It’s also been bitten by the litigation bug. 3M could face as much as $6 billion in legal liabilities connected to accusations that the company’s chemicals have shown up in groundwater across the country.

3M is one of the longest-tenured Dividend Aristocrats at 61 consecutive years and counting. But even that seems like less of a guarantee than it used to. While the payout is well-covered at less than 70% of profits, Tusa warned that “Another leg down in fundamentals would mean they are on watch for a cut, after 37 straight years of increase.”

Will things degenerate that much? It’s difficult to say. But 3M appears set up to endure more pain before it establishes an enduring recovery.

Better Than Aristocrats: “2008-Proof” Income Plays With 7.5% Yields and Fast 10%+ Upside

It’s remarkable to think that even the most reputable blue chips sporting decades of dividend growth can be so suspect.

But that’s how I can help you separate yourself from “first-level” investors. While they lean on lazy recommendations based on past performance and reputations, I invest using methodical, forward-looking analysis, and sniff out the dangers in supposedly no-brainer plays.

And I want to start by showing you how to get real income. We’re talking safe, sustainable payouts of 3 to 4 times what most Dividend Aristocrats deliver.

This is no time to gamble in a desperate stretch for yield. We’re in the back half of a bull market that’s extra-long in the tooth, and numerous global risks are converging on this fragile market.

Big yields mean nothing if you’re not protecting your hard-earned nest egg, too.

These 5 income wonders deliver two things most “blue-chip pretenders” don’t:

Rock-solid (and growing) 7.5% average cash dividends (more than my portfolio’s average).

A share price that doesn’t crumble beneath your feet while you’re collecting these massive payouts. In fact, you can bank on 7% to 15% yearly price upside from these five “steady Eddie” picks.

With the Dow regularly lurching a stomach-churning 1,000 points (or more) in a single day during pullbacks, I’m sure a safe—and growing—7.5% every single year would have a lot of appeal.

And remember, 7.5% is just the average! One of these titans pays a ROCK-SOLID 8.5%.

Think about that for a second: You can buy this incredible stock right this second, and every single year from now on, nearly 9% of your original buy boomerangs straight back to you in CASH.

If that’s not the very definition of safety, I don’t know what is.

These five stout stocks have sailed through meltdown after meltdown with their share prices intact, doling out huge cash dividends the entire time. Owners of these amazing “2008-proof” plays might have wondered what all the fuss was about!

These five “2008-proof” wonders give you the best of both worlds: a 7.5% CASH dividend that jumps year in and year out, with your feet firmly planted on a share price that holds steady in a market inferno and floats higher when stocks go Zen.

Editor's Note: The stock market is way up – and that’s terrible news for us dividend investors. Yields haven’t been this low in decades! But there are still plenty of great opportunities to secure meaningful income if you know where to look. Brett Owens' latest report reveals how you can easily (and safely) rake in 8%+ dividends and never worry about drawing down your capital again. Click here for full details!