The multitudes faster 5G wireless technology will start rolling out around the globe over the next few years. Under the 4G system, mobile data has grown 17-fold over the past five years. Verizon predicts that 5G will allow data speeds up to 20 times faster than 4G. This means 20x as much data will be shared and much of it stored. The higher 5G speed will result in many more connections to the wireless network, including current wireline connected equipment and currently unconnected devices that will join the Internet of Things.

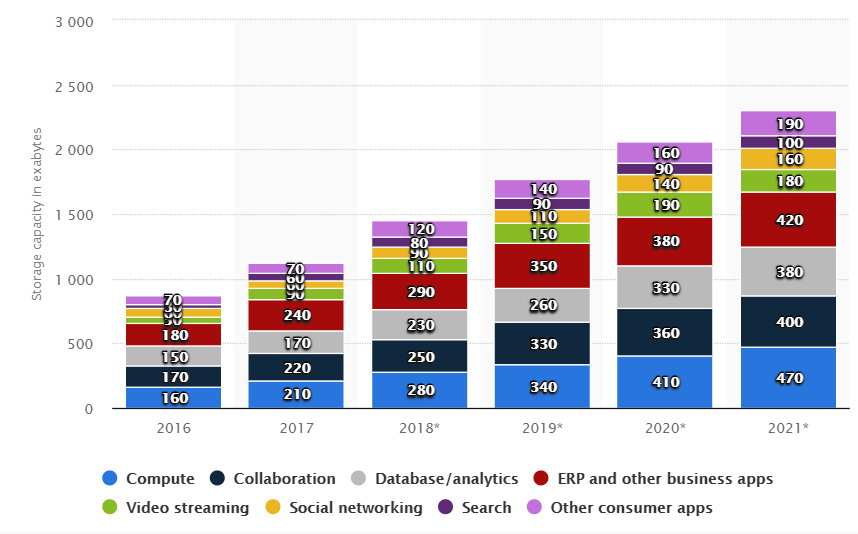

Exponential growth of data sharing means similar growth levels required for data storage. The tech industry, really all industries, rely on data centers for data storage. These are dedicated facilities with specific design feature to house servers, routers, switches, backup servers and the connections required to so data can be transmitted, accessed and stored. In the current world these are very large, high-tech facilities with advanced cooling and power generation capabilities. Data center storage is a growth business, as show by this chart showing data center storage data amounts for 2016 through 2021 from statista.com.

Data centers are a great, longer term way to participate in both 5G and data storage requirements growth. There are a handful of real estate investment trusts (REITs) that operate exclusively in providing data center services to the tech sector and other industries. Here are three to consider.

Equinix, Inc. (Nasdaq: EQIX) is the $35 billion market cap, the large-cap standard of the data center industry. The company converted from corporate tax payer to REIT status at the start of 2015. The company is a colocation and interconnection service provider. Colocation is a data center facility in which a business can rent space for servers and other computing hardware. Typically, a colocation facility provides the building, cooling, power, bandwidth and physical security while the customer provides servers and storage.

The company’s services currently give 9,500 customers 300,000 interconnects between data centers and world’s digital exchanges. According to the current Investor Overview presentation, Equinix owns over 200 data centers in 24 countries, on five continents. This is truly an international company. Over the last decade the company has produced in excess of 20% compounding annual revenue and EBITDA growth. This results in mid-teen per share cash flow growth.

For 2019 the company forecasts 11% FFO per share and dividend increases.

The shares currently yield 2.3%.

Digital Realty Trust, Inc. (NYSE: DLR) is a $24 billion market cap REIT that owns 198 data centers in 32 metropolitan areas. Digital Realty has over 2,300 customers.

Like Equinix, Digital Realty is also a colocation and interconnection services provider.

This REIT’s customer list includes some of the largest technology and telecommunications companies.

In the top 10 are IBM, Oracle, Verizon, Linked In, and even Equinix.

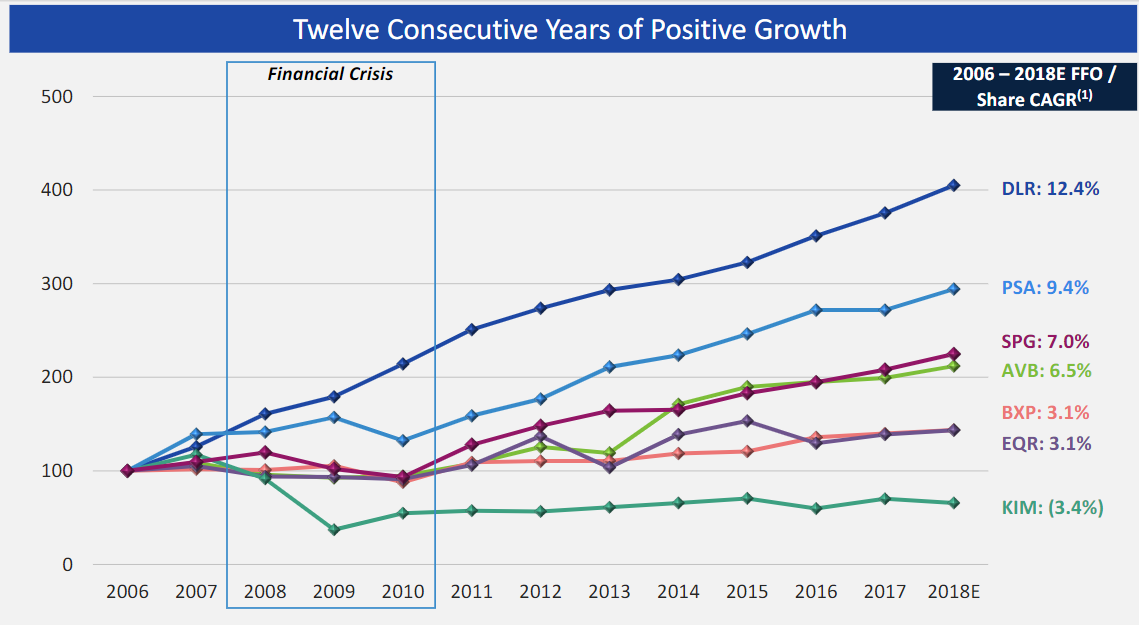

According to the current investor presentation, Digital Realty has grown FFO per share for 13 straight years. Over that period cash flow to pay dividends has grown by a compounding 12% per year.

This chart shows the FFO growth compared to large REITs in other sectors:

The DLR dividend has grown by 10% plus per year for the last decade. The shares currently yield 3.6%.

CoreSite Realty Corp (NYSE: COR) is a $3.9 billion market cap REIT that owns 22 data centers in eight strategic U.S. cities.

The company’s focus is to provide colocation services to enterprise, network, and cloud services companies. The company has over 1,300 current customers. CoreSite is the high growth, higher risk company out of the three covered here.

Since 2011, FFO per share has grown by 23% compounded and the dividend by more than 30% per year. Future results will cycle from relatively flat to high growth years. An investment in COR will not be as stable as with the large cap data center REITs. The flip side is the potential for large dividend increases and corresponding share price gains.

Calendar 2018 was a big year for initial public offerings, or IPOs. The number of IPOs in 2018 rose more than 20% year-over-year to nearly 230, the highest mark since 2014 and the third highest mark over the past ten years.

Yet, there’s reason to believe that 2018 was just the beginning of a multi-year IPO boom. Here’s the thing about the IPO market: it runs in cycles. Multiple consecutive years of low IPO volume are followed by multiple consecutive years of high IPO volume. From 2015 to 2017, we had three years of below-average IPO volume. Calendar 2018 broke that trend with 200-plus IPOs. History tells us that 2019 and 2020 should be more of the same.

Indeed, calendar 2019 should be one for the record books in the IPO market. The list of potential 2019 IPOs is long, diverse, and includes some of the biggest and fastest growing private companies. Those companies promise to make an unforgettable splash when they go public later this year.

More than that, I think many of these IPOs will be extremely successful. The batch of companies going public this year include the batch of companies that were birthed out of the Financial Crisis a decade ago. They are disruptive and innovative, and cut from a different cloth than current public companies. Most importantly, most of these companies are employing coordinated economic principles to give power back to the people, and in so doing, are aligned with the biggest trend of the century.

As such, not only does the 2019 IPO market project to be one for the record books, but it should also yield some big winners. With that in mind, let’s take a look at a list of seven IPOs that investors should be excited for in 2019.

Uber

At the head of this list is Uber, the ride-sharing company which has already entirely disrupted the transportation industry.

Investors should be excited about the Uber IPO because this company has truly optimized transportation services, and in so doing, has established a massive driver base which will be hard for anyone else to replicate, and from which multiple valuable business opportunities can be created. In a nutshell, Uber is the quintessential coordinator. Before Uber, transportation services were performed by the few (namely, taxis). Uber democratized the supply of transportation services, and said anyone with a car can now perform this service, creating a surge in supply. Uber coordinated that supply, so that it would satisfy demand-side expectations. Net result? Supply caught up to robust demand, price points fell, and convenience went up. Uber won.

Now, Uber has a driver base that numbers several million globally. Uber can use that unparalleled driver base to optimize price and convenience in other transportation-related industries, such as delivery and last-mile logistics. The sum potential of all these industries numbers in the hundreds of billions of dollars, and potentially even in the trillion dollar range if Uber wins the race to self-driving. As such, while Uber’s rumored $120 billion IPO valuation may drop some jaws, it’s worth it.

Lyft

Uber isn’t the only ride-sharing company going public in 2019. In fact, before Uber ever hits public markets, its competitor Lyft should have already spent a few months on Wall Street.

Lyft is planning to launch its IPO roadshow in mid-March. That means that by the summer of 2019, Lyft should be a publicly traded company. That’s exciting news. Much like Uber, Lyft is a quintessential coordinator who has helped democratize and coordinate supply in the transportation industry to meet robust demand. In so doing, Lyft has huge opportunities in front it to not only become a solid second player in the ride-sharing market, but also the number one or number two company in a plethora of other transportation-related markets.

The attractive thing about the Lyft IPO is that the valuation is rumored to be under $25 billion. That is just a fraction of Uber’s valuation. To be sure, Uber is much bigger than Lyft in terms of total revenues and rides. But, Lyft is supposedly growing much more quickly than Uber, and the company has largely avoided negative press (much unlike Uber). Consequently, investors should be excited about the upcoming Lyft IPO, given its discounted valuation relative to Uber and that the company is apparently gaining share in ride-sharing.

Airbnb

The coordinated economy hasn’t just hit the transportation industry. It has also hit the accommodations industry, thanks to Airbnb, who also projects to go public in 2019.

Much like Uber, Airbnb has become a quintessential coordinator. Before, accommodation services were provided by the few (namely, hotels). Airbnb democratized supply in that market, and said that anyone who has an extra room or living space can rent it out for accommodation purposes. Supply surged. Airbnb coordinated that supply to satisfy demand-side expectations. Consequently, supply caught up to demand, prices fell, and convenience rose.

Much unlike Uber, however, Airbnb doesn’t have any big second competitor that is also set to IPO in 2019. Thus, the competition landscape for Airbnb is quite attractive for the foreseeable future. Also, Airbnb is in an optimal position to jump into other accommodation-related industries, like the travel and car rental industries, meaning the long term opportunity here is quite large.

Postmates

Following in the footsteps of Uber, Postmates took those same coordinated economy principles and applied them specifically to the delivery process.

While you may be inclined to compare Postmates to food-delivery services including UberEatsand GrubHub (NYSE:GRUB), that’s not entirely accurate. Postmates will also deliver items from local stores such as groceries, alcohol, and other items–making for a nice moat. (Though for these other items, they may eventually have to compete with the likes of Amazon(NASDAQ:AMZN), which is no joke for any company, but for now, same-day delivery isn’t widespread and it isn’t under an hour or so wait time.) But the (prepared) food-delivery market will be really big one day (like $100 billion-plus big), and Postmates is maintaining steady double-digit market share. Plus, the current valuation on Postmates is reasonable ($1.85 billion).

Thus, in the big picture, Postmates is a solid growth company in a big growth industry. There’s some competition, but the valuation reflects those competitive risks, and is actually quite attractive considering the market growth potential. As such, the Postmates IPO is one to watch for later this year.

Pinterest

The last big social media app to IPO was Snap (NYSE:SNAP). That didn’t go too well. But, there’s reason to believe that the next big social media app to IPO, Pinterest, will have a different outcome.

Snap struggled for three reasons. The user base fell flat, engagement proved difficult to monetize, and margins were weak. Pinterest won’t have those problems. The platform has about 250 million monthly active users, and is growing that base at a fairly consistent 50 million new users per year. Also, given Pinterest’s curation focus, data indicates that engagement on the platform can be very easily monetized, as consumers are already using Pins to influence purchasing behavior. Perhaps most importantly, Pintrest’s gross margins are north of 45%.

All in all, Pinterest looks positioned for big success on Wall Street. User growth is healthy. Engagement is easily monetized. Margins are high. There’s a lot to like here, meaning that Pinterest stock will likely have a much better start on Wall Street than Snap stock.

Pinterest filed for IPO at the end of last week, seeking a valuation of at least $12 billion.

Slack

If you thought social networking was exclusive to the personal level, think again. Enterprise social networking, or ESN, is a rapidly expanding industry, and at the heart of all that growth is Slack, yet another company set to IPO in 2019.

One aspect of the cloud tech boom is the growing demand for enterprise cloud solutions tailored to addressing intra-business communication and workflow needs. ESN is the market which addresses those needs, as it includes a portfolio of platforms which allow for seamless intra-business communication and workflow sharing. The most popular of those platforms is Slack, which has gone from 365,000 daily active users to 10 million daily active users in just four years. Indeed, some say Slack is the fastest growing software-as-a-service (SaaS) company ever.

Going forward, there are two important things to note here. One, demand in the ESN space will only continue to grow. Two, Slack has beaten out competition from Facebook (NASDAQ:FB) in this space. As such, Slack has a proven ability to beat top-quality competition in a big growth market. That positions the company for robust growth for a lot longer, which roughly translates into Slack stock doing well on Wall Street.

Palantir

Peter Thiel is an important and impressive guy. He co-founded PayPal (NASDAQ:PYPL), and was the first major outside investor at Facebook. Now, his latest venture, Palantir (which Thiel founded in 2003), is set to go public in 2019.

At its core, Palantir provides solutions which enable companies of all sizes to make sense of big data. This is a very important service. Big data is of increasing importance when it comes to enterprise decision making. But, the quality of insights device from big data relies on the quality of analysis done on that big data. That’s where Palantir excels — providing the best of the best analysis on such data.

The long-term outlook for Palantir looks good. So long as data becomes increasingly important, Palantir’s services will have growing demand. The only big concern is competition. But, this market projects to be so big one day that it will support multiple players at scale. Consequently, the Palantir IPO should be successful.

As of this writing, Luke Lango was long GRUB, FB, and PYPL.

Today I’m going to show you a closed-end fund (CEF) yielding 13.7% that sounds—and is—too good to be true.

If you hold it, now is the time to sell.

The fund I’m talking about is Eagle Point Credit Company (ECC). Today we’re going to dive into all the reasons why ECC is a CEF to avoid. I’ll also give you five takeaway tips you can use to steer clear of funds like it in the future.

Let’s get started.

CEF Danger Sign No. 1: NAV and Market Price Go Haywire

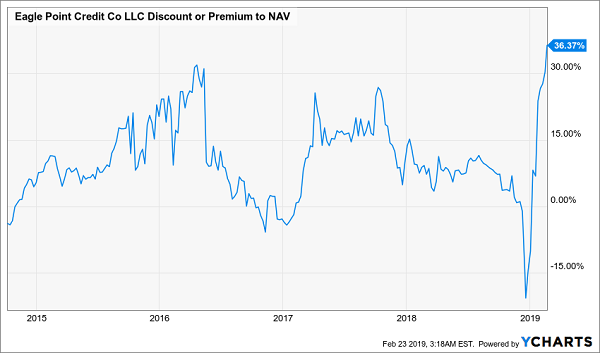

As you can see below, ECC recently saw its net asset value, or NAV, plummet 26%, erasing three years of gains overnight:

ECC’s Underlying Portfolio Collapses …

In a normal situation, you’d expect investors to sell fast. But in the world of CEFs, things don’t always happen that way. Zooming in on the past two months, when this NAV crush occurred, we see that the fund’s price actually soared.

… And Investors Cheer!?

This is obviously an extreme example, but when a CEF’s market price soars while its NAV heads south, it’s time to pay extra attention. Which leads me to my second red flag.

CEF Danger Sign No. 2: What Goes Up …

The widening chasm between ECC’s market price and NAV has put the fund’s investors in a dangerous spot, because it’s sent its premium to NAV soaring to the highest point in history in a very short period—and that can’t last. Check out this chart:

Stratospheric Premium Has One Way to Go

Such a poor NAV performance shouldn’t be rewarded with such a high premium, yet here we are. That leads us to the inevitable question: what caused ECC to lose a quarter of its NAV so quickly—and why didn’t investors respond immediately? Cue up my next warning sign.

CEF Danger Sign No. 3: The Fund Holds Complex, Hard-to-Value Investments

A major problem with ECC is that it only announces its official NAV with every quarterly earnings release, along with a rough estimate every month. This isn’t the norm for CEFs. Of the near-500 CEFs tracked by CEF Insider, 99% report NAV on a daily basis. But you don’t know what ECC’s portfolio is worth until it announces earnings each quarter.

This has to do with the collateralized loan obligations (CLOs) ECC invests in. CLOs are a type of derivative on loans similar to the mortgage-backed securities that tanked the economy in 2008.

CLOs pool a variety of loans, then cut these pools into sections investors can trade on the secondary market. These complicated assets aren’t traded daily, which makes it tough to mark them to market (or determine their NAV if they were all sold immediately). That’s why ECC only does this once a quarter.

As a result, you could buy ECC at what you think is a big discount only to find out, days or weeks later, that you actually bought at a premium.

CEF Danger Sign #4: High Fees

ECC is also expensive from a fee perspective, as we can glean from the table below.

High Fees Hurt Shareholder Profits

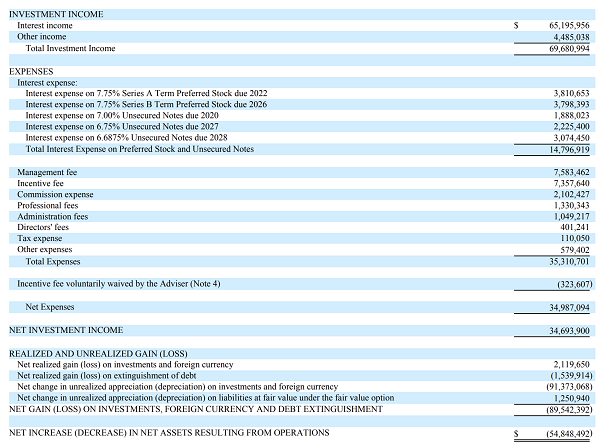

Source: Securities and Exchange Commission

There’s a lot going on here, but you only need to look at two numbers: total investment income of $69,680,994 (near the top) and $34,987,094 in net expenses (two-thirds of the way down). Over half the fund’s profits went to a variety of fees! As a result, ECC’s fees amounted to a whopping 12.3% of its NAV in 2018.

CEF Danger Sign No. 5: A Shift in the Fund’s Sector

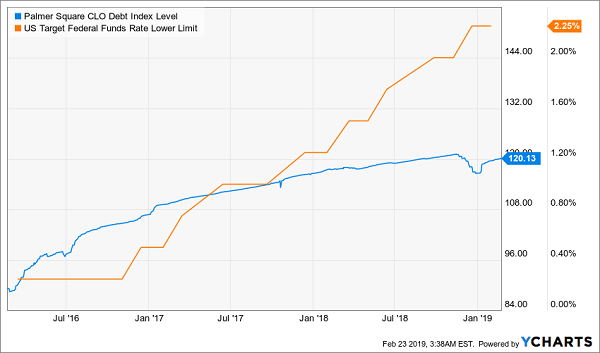

I’ve left the biggest reason for ECC’s underperformance for last: the late-2018 market crash and a sea change with CLOs themselves. If we look at the Palmer Square CLO Debt Index, we see that CLOs’ value took a hit at the end of 2018—as did just about everything else:

A Massive Drop for CLOs

As a CLO fund, ECC is expected to drop with the index, but we should still ask why the index plunged in the first place. Late 2018’s selloff is part of the story, but interest rates are another part. That’s because CLOs have benefited from the rising-rate environment we’ve seen since 2015, as higher rates boost their interest income:

CLOs Rise With Rates

However, the Federal Reserve has made it clear that the aggressive rate-hike plans it laid out in 2018 won’t happen in 2019. And the fact that CLOs had priced in a long string of rate increases caused them to crash in late 2018.

They should have stayed down, but irrational exuberance kicked in, making CLOs—and ECC itself—overvalued again.

For the most part, initial public offerings are a sucker’s game.

IPOs, especially for name-brand tech companies, generate lots of hype. And even if the company is solid, it often can’t justify its debut stock price – let alone any surges in its first few days on the market.

But that doesn’t mean you can’t get in on some of the most exciting upcoming IPOs – like Uber, Lyft, Slack, Pinterest, or Airbnb – and still limit your risk.

In fact, we’ve got a pick today that gives you some of the hottest IPOs while taking all the guesswork (and grunt work) out of trying to pick winners.

Plus, we’ll also give you the opportunity to grab multiple upcoming IPO picks in a red-hot industry that are ready to hit the market in 2019. Each of these is capable of unleashing millions of dollars into the market, so you won’t want to miss these opportunities.

But first up, one of best ways to approach the IPO market – especially if you don’t have the time or patience to research every new offering individually – is through a well-managed ETF.

Well-managed doesn’t just mean selecting the most promising public offerings. It also means holding onto the ones that still have room to grow. That way you both minimize your risk and maximize your gains.

That’s why we like one particular ETF that gives you access to the broad IPO market while blending both new offerings and older ones.

Have 28 Seconds? You could make $2,353 – and you won’t need to buy a single share of stock up front to collect this cash, or spend a nickel on anything. Click here to learn more…

And before you worry that an ETF is going to dilute your gains too much, keep in mind that this pick has beaten the S&P 500 by more than 50% over the last two years.

So if you’ve always wanted to get into the IPO game but were (rightly) concerned about volatility and overhyped offerings, this is your ticket to cutting edge of the stock market.

And you can get there without sweating endlessly over a new offering’s financials…

Your Quickest, Easiest Entry Point into Venture Capitalism

First Trust US Equity Opportunities ETF Fund (NYSE: FPX) is an ETF with roughly 100 holdings. These include some of the biggest companies to go public in the last few years. They include Match Group Inc. (NASDAQ: MTCH), Coupa Software Inc. (NASDAQ: COUP), and Wayfair Inc. (NYSE: W).

Because most of the stocks in FPX only make up about 1% each of the portfolio, no one stock is going to sink the fund. And First Trust balances out those young startups with some big names that have been around for a while, like Hewlett Packard Enterprise Co. (NYSE: HPE), Tyson Foods Inc. (NYSE: TSN), and Kraft Heinz Co. (NASDAQ: KHC), which provide an extra layer of protection.

The principle in play here is that it’s foolish to invest in IPOs and then drop them once they’re no longer new. So FPX holds on to select stocks for the long haul. That way the fund doesn’t get burned by selling stocks before the initial volatility has settled down.

One great feature of FPX is how diversified it is. It’s not just grabbing tech stocks – though there are certainly plenty of them – but includes offerings across the finance, auto, retail, and energy industries.

And because the fund’s managers are researching every IPO before they decide to include it in the fund, you can rest assured that your money isn’t going into every overhyped offering that hits the market.

Let’s take a look at some of the winners this fund has chosen over the years…

Square Inc. (NYSE: SQ) is probably best known for the adapters people can attach to their smartphones to accept credit cards, leveling the playing field for artists and small startups. It now offers a wide range of products for financial transactions, including the popular Cash App for consumer-to-consumer transactions. That app can now also be used to purchase Bitcoin, and we can no doubt expect even more functionality in the future. Now at more than eight and a half times its debut price in November 2016, this stock likely still has room to run.

SailPoint Technologies Holdings Inc. (NYSE: SAIL) is a provider of identity governance services for more than 1,000 global customers. Identity governance is one of those less exciting, but critical services, allowing enterprises to manage their cloud-based and on-site applications and data effectively, efficiently, and safely. SailPoint stock is up 162% since its November 2017 debut, and the need for its services is only growing.

Etsy Inc. (NASDAQ: ETSY) brings e-commerce to the arts, crafts, and vintage items market. Its earnings per share (EPS) soared into the black in the 2017 fiscal year, and according to FactSet, is projected to triple between now and 2021. Despite a rough start to its appearance on the market, Etsy has now doubled since its November 2015 debut.

ZenDesk Inc. (NYSE: ZEN) is bringing customer service into the 21st century, providing software solutions to make the process run quickly and efficiently. Like Etsy, ZenDesk’s EPS went sharply positive within the last couple years. More impressively, it is expected to multiply nearly seven times by 2022. Those rising fortunes have boosted the stock 768% since it debuted in May 2014.

That said, if you want to up your game and grab a potential rocket stock on the IPO market, we’ve got an opportunity – a whole series of opportunities, in fact – you won’t want to miss.

Let’s face it: this frothy market has made it much tougher to uncover the big, cheap dividends you need to fill out your retirement portfolio. So today we’re going to fight back with my top 2 “off-the-record” strategies for honing in on 7.4%+ dividends that still have a lot of upside ahead.

First, to get a sense of the vice the rebound has locked income investors in, check out this chart:

Stock Bounce Crushes Yields

That amounts to an 18% bounce since Christmas Eve, which has sliced 15% off the S&P 500’s dividend yield (because yields fall as prices rise). As I write, the average S&P 500 name dribbles out a 1.9% payout—less than inflation!

Which brings me to the first strategy I’ll show you today.

Contrarian Tip No. 1: When They Go Short, We Go Long

Short interest is one of my favorite ways to “time” stock buys.

If you’re unfamiliar, short selling involves selling a stock you’ve borrowed, with a commitment to buy it back later, hopefully at a lower price. Your profit lies in the difference between the selling price and the price at which you have to buy it back.

It’s a dangerous path that can expose you to unlimited losses (because there’s no limit on how high a stock can rise, while your “regular” buys can only go to zero).

But don’t worry—we’re not going to “short” stocks ourselves. Instead, we’re going to sit back and cash in on the short sellers’ greed.

Here’s how: if a stock attracts a lot of short interest and the price moves up, the “shorts” will scramble to buy and cover their positions. That’s great for us because it can create a “feedback loop” where the rising price triggers short covering, driving the price higher, triggering more short covering, and so on.

All we have to do is relax, let the chaos unfold, and watch our stock rocket higher! And these “squeezes” can be truly epic, like the one that caused Volkswagen to explode 82% in a single day in 2008.

So how do we find our own Volkswagen (and better yet, one with a 7%+ dividend)?

A good rule is that short sellers tend to be the most wrong at the extremes, so we’ll look for short interest that’s wayhigher than usual, then jump in. You can see this in action with Omega Healthcare Investors (OHI), a real estate investment trust (REIT) I’ve recommended in my Contrarian Income Report service:

Short Covering Sends OHI Ripping Higher

Notice how rising short interest kept a lid on OHI’s price, until it peaked in January 2018? If you’d jumped in then, you would have bagged a 35% price gain in just over a year, as short covering helped pry the stock higher.

And that’s just in price gains! Never mind that OHI pays a 7.4% dividend now (and would have paid nearly 10% when short interest peaked). Throw the payout in, and your gain jumps to 48%in just one year.

So much for the common “wisdom” that you can’t get big gains and big dividends from a single stock!

Now let’s move on to our next contrarian buy signal.

Contrarian Tip No. 2: Check In as Analysts Check Out

You can catch another big windfall by paying close attention to analyst ratings—but not the way most people think.

Remember, everyone loves to follow the herd, and analysts are often the lead lemmings. That’s why, when most folks research a stock, they look for those with a lot of buy ratings from Wall Street—if they look at these ratings at all.

But they’ve got it backwards! Because if every analyst already has a buy rating on a company, there’s no hope of upgrades, which can send shares stair-stepping higher.

That’s what happened with self-storage REIT CubeSmart (CUBE), payer of a 4.2% dividend that’s skyrocketed in the last five years. As you can see below, CUBE’s shares nearly doubled from June 2014 to March 2016, as the number of analysts recommending it also nearly doubled, from four to seven.

Wall Street Optimism Drives an Easy Double …

Fast-forward to today, and just one analyst has a “buy” on CUBE, even though the Federal Reserve has halted further rate hikes, a big plus for the entire REIT sector. That sets the stock up for another strong run as analysts climb back aboard.

21 Cash-Spinning Buys for 7.5% Payouts and BIG Gains

Here’s the roadblock most regular folks slam into with “second level” indicators like these: the big brokerages keep ALL of this powerful research to themselves!

Free services, like Yahoo Finance, give us crumbs, with buy recommendations limited to just the last four months. Basing a buy decision on that tiny slice of data could send you straight off a cliff.

Don’t Buy ANY Stock Based on This!

Source: Yahoo! Finance

Finding short interest is even harder. Your only real option here is a paid service like Ycharts, but that will set you back hundreds of dollars a year!

[Editor’s note: This story was originally published in August 2018. It has since been updated and republished.]

The stock market’s volatility in recent months has not made me less bullish on the five cheap stocks profiled in this article. Among these stocks, market movements can cause some noise. But the investment thesis on cheap stocks is predicated on huge moves higher in the long-term. Thus, in the near-term, macro-driven movements amount to nothing more than a sideshow.

From this perspective, now might be a good time to pile into some stocks under $5. These stocks are a high-risk bunch. But they do have high-reward potential, too.

With that in mind, here is a list of five cheap stocks, which I think have big upside potential.

Source: Shutterstock

Pier 1 (PIR)

PIR Stock Price: 88 cents

Furniture retailer Pier 1 Imports (NYSE:PIR) has had a tough time getting its act together for several years.

Peer Restoration Hardware (NYSE:RH) has seen its stock rise 30% over the past year thanks to a red-hot housing market and robust demand for home furnishings. PIR stock, however, has collapsed during that same stretch. These problems aren’t new. Over the past five years, this stock has lost more than 90% of its value.

Having said that, there is visibility for a turnaround in PIR stock in the near future.

At its core, Pier 1 has been killed by rising e-commerce threats creating huge pricing and traffic headwinds. Pier 1, which stands somewhat square in the middle of price and quality, doesn’t really have anything special about the business to protect against these headwinds. Consequently, sales and margins have dropped in a big way.

But, the company has a three-year strategic plan to turn the business around. The plan includes bigger investments in omni-channel commerce capabilities and marketing.

No one knows whether this plan will actually work. But home furnishings is a market with enduring demand, so that helps.

Meanwhile, PIR stock is dirt cheap. This company used to have earnings power of $1 per share. Even half of that earnings power (50 cents) would be huge for a stock trading under $1. At 50 cents per share in earnings power, it wouldn’t be unreasonable to see this stock hit $8 (a market-average 16x multiple).

Source: Shutterstock

Groupon (GRPN)

GRPN Stock Price: $3.50

Much like Pier 1, savings-king Groupon (NASDAQ:GRPN) feels like one of those companies that were loved yesterday but will be forgotten tomorrow. But I don’t think that’s true. I get that the savings and deals market is commoditized now. I also understand that Groupon really isn’t a household name for coupons like it used to be.

But I’m a numbers guy. And Groupon’s numbers are pretty good. Its margins are improving thanks to management’s focus on higher-margin businesses. Operating expenses are also being removed from the system, so the company’s overall profitability profile is improving.

Aside from the numbers, Groupon launched an aggressive advertising campaign last year with hyper-relevant Tiffany Haddish that scored just shy of 100 million views. I think this campaign will have a long-term positive effect on usage, which could drive the stock higher.

Put it all together, and it looks like GRPN stock could have a big-time rally in 2019.

Note: ZNGA stock rose over $5 since this article was originally published.

I’m not a huge fan of the mobile gaming sector. It’s a tough space plagued with competition and low margins. Plus, competition is only building thanks to social media apps becoming increasingly multi-purpose.

But mobile gaming company Zynga (NASDAQ:ZNGA) seems to have found the key to success in the mobile gaming world.

Zynga used to be a mega-popular browser game company with tons of users. But then the company overreached by branching into games that had heavy overlap with the traditional video game market, like sports titles. They couldn’t compete in that market. Eventually, the over-extension sparked user churn, and ZNGA stock spiraled downward.

That forced Zynga to re-invent itself into something much more relevant and defensible. They did just that. Zynga has transitioned its business model from web-focused to mobile-first while narrowing its gaming title focus. This pivot has streamlined operations, re-invigorated top-line growth, cut costs and improved profitability.

Consequently, the numbers supporting Zynga are pretty good. In Q4, its revenue rose 7% year-over-year and its bookings jumped 19% YoY. Finally, its operating cash flow soared 241%.

From where I sit, this pivot appears to be in its early stages. Mobile is a secular growth narrative, and ZNGA has developed a gaming portfolio that is focused and tailored to that growth narrative. Thus, so long as mobile engagement heads higher, Zynga’s numbers should get better. Better numbers will inevitably lead to a higher stock price.

There is no hiding the fact that the defense sector has been hot under President Trump.

Trump came into office, upped the ante on defense and military spending, and in response, the whole world is spending more on defense and military.

Defense contractors win when this happens. That is why mega-cap defense contractors like Lockheed Martin (NYSE:LMT) and Boeing (NYSE:BA) have been on fire for the past several quarters.

But one micro-cap defense contractor that has missed out on this rally is Arotech (NASDAQ:ARTX). Over the past several years, the financials at Arotech haven’t gained any ground. Five years ago, its revenues were $103.5 million and its net income was $3.5 million. In 2017, its revenues were $98.7 million and its net income was $3.8 million.

In other words, its profits haven’t risen much in five years. When profits don’t go up, the stock tends not to go up. It is a simple relationship.

But its profits are stabilizing. When profits go from declining to stabilizing, they usually go to growth next.

And, when profits go up, stocks tend to go up.

As such, it looks like Arotech is finally joining the tide when it comes to big boosts in defense and military spending. This tide will inevitably lift Arotech’s earnings power substantially, and ARTX will rally as a result.

Source: Shutterstock

Blink Charging (BLNK)

BLNK Stock Price: $3.05

When it comes to cheap stocks, there are few as volatile as Blink Charging (NASDAQ:BLNK).

Over the past two years, BLNK stock has gone from $10 to $3, and popped from $4.50 to $8 … it now sits at a paltry $3.04. This volatility won’t give up any time soon. Thus, if you want to avoid volatility, I’d say avoid BLNK stock.

That being said, if this company’s secular growth narrative surrounding building a network of electric vehicle charging stations globally materializes within the next five years, this stock could be a 5-to-10 bagger.

It is a big risk. But, eventually, global infrastructure will need to match demand. At that point in time, there will be some huge contracts awarded to electric vehicle charging station companies.

Will Blink be one of them? Perhaps. Tough to tell. But if they do land some big contracts, this stock could have another huge pop in a short amount of time.

As of this writing, Luke Lango was long FB, PIR, GRPN and ARTX.

Stock-market selloffs provide great times to buy big dividends. The stock market was a relentlessly receding tide in the fourth quarter, which is bad for “buy and hope” investors but quite helpful for income specialists like us.

Let’s consider high-quality real estate investment trust W.P. Carey (WPC). This REIT looks good at most prices, but the market gave us an exaggerated dip in December-early January that spiked its yield to nearly 6.5%. Savvy, patient investors who bought on this dip (like my Contrarian Income Report subscribers) didn’t just enjoy an excellent yield on the higher end of its five-year range – they also are sitting on 17% gains in just a matter of weeks!

W.P. Carey (WPC): Why It Pays to Wait for Dividend Deals

The problem for bargain hunters right now is that the market’s red-hot 2019 recovery has brought many stocks back to the bloated valuations they traded at before the fourth quarter provided a little valuation relief.

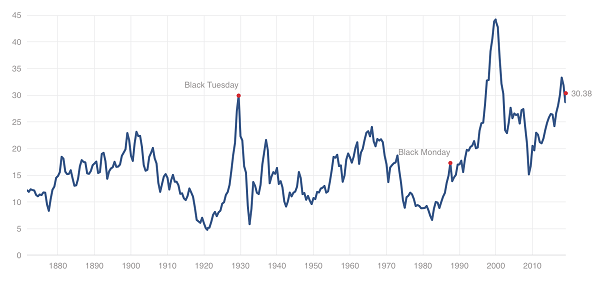

In fact, we’re still in the midst of one of the most expensive markets ever.

If You’re Buying Stocks Right Now, You’re Probably Overpaying

Source: Multpl.com

But there are a few deep values left in this marked-up market. A few stocks I’ve been monitoring have been pared by between 25% and 65% in less than a year. And as a result, these battered dividend plays, which typically yield 3%-4%, are dishing out yields between 5.3% and 6.6%!

That’s good. Plus these deep discounts also mean there’s potential for short-term pops of 20% or more.

Of course each of these firms has business hurdles to overcome. Let’s dig in to dividend stock bargain bin:

Weyerhaeuser (WY) Dividend Yield: 5.3%

REITs have held up pretty well over the past half-year or so, which makes timber real estate play Weyerhaeuser’s (WY) performance since July stick out like a sore, black-and-blue thumb.

Weyerhaeuser (WY) Has Been Taken to the Woodshed

The primary tailwind on Weyerhaeuser? The Fed.

In short, the Federal Reserve’s ramping up of interest rates finally started to weigh on the housing market in a big way, which in turn finally popped a bubble in lumber prices that had been keeping WY aloft.

Source: MacroTrends.net

There are a few things to like about Weyerhaeuser. Timber is a very niche REIT realm, providing some serious diversification, and the company has been a beacon of dividend growth, upping its annual payout every year since converting into a real estate investment trust in 2010. And prior to its lumber-related plunge last year, it had outperformed the Vanguard REIT ETF (VNQ) by 135% to 86% on a total return basis over the past decade.

But is WY a value?

While lumber prices appear to be stabilizing, they’re still doing so at levels considerably lower than their 2018 highs. Moreover slower rate hikes from the Federal Reserve will take a little pressure off the housing market. But the data is still grim. November housing starts (the last available data thanks to the temporary government shutdown) showed single-family starts at a 1 ½-year low. Third-party gauges for December activity, namely permits, also were in a downtrend.

The dividend is a potential problem, though. Weyerhaeuser did improve the payout again last year, in August, by 6.3%. But the company paid out $995 million in dividends against $748 million in profits last year, and its projected annual payout of $1.36 per share in 2019 is far more than analysts’ expectations for 83 cents in profits.

This could be a short-term bump in the road, but the path out isn’t clear yet. That, combined with the dividend situation, makes WY look less like a value, and more like a high-yield value trap.

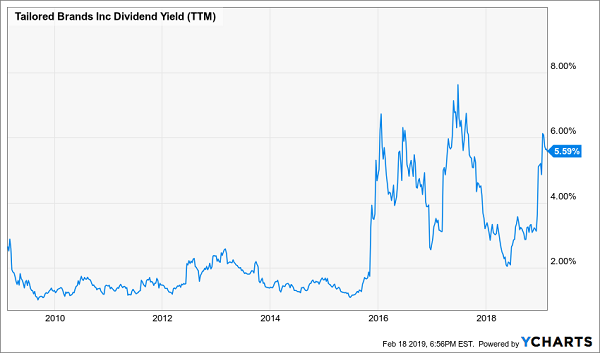

Tailored Brands (TLRD) Dividend Yield: 5.6%

Tailored Brands (TLRD) isn’t a familiar name outside the investing space, but most people will know its two primary brands: Men’s Wearhouse and Jos. A. Bank. The men’s suit stores engaged in a nasty bout of M&A maneuvering starting in October 2013 before eventually completing a merger in June 2014. Men’s Wearhouse switched to a holding-company structure in January 2016, adopting the Tailored Brands moniker in 2016.

Shares have been bludgeoned over the past year, losing roughly two-thirds of their value since May 2018. Some of the biggest hits included disappointing same-store sales growth in June, a report in December that Men’s Wearhouse traffic was sliding (thanks to several factors, including increased competition from the likes of Bonobos) and another report in January in which the company lowered its fourth-quarter guidance on weakness at Jos. A. Bank.

What’s to like about this apparent train wreck?

For one, the yield on TLRD is now well north of 5%, which is on the very high end of its range since the merger. But despite the company’s woes, it will pay out just 32% of its expected full-year earnings ($2.28 per share) in dividends. In short, the payout is extremely safe for a company that has been trounced so hard.

Another Yield Spike for Tailored Brands (TLRD)

At the same time, TLRD is making strides on paying out its debt. The stock also is a deep value at these levels, trading at just five times future earnings estimates. And despite its woes, analysts still see the Tailored Brands averaging high-single-digit profit growth over the next half-decade.

But cheap stocks can get even cheaper.

Tailored Brands warned significantly on comps, but said it wasn’t sure why they had weakened so much. They’re so much of an outlier compared to past quarters, in fact, that this could just be a blip on the radar. If so, TLRD could be a dividend-and-value double play. But if this is a glimpse into a shift in consumer tastes, Tailored Brands will be forced between a rock (falling sales) and a hard place (returning to deep discounts, slicing margins).

Altria (MO) Dividend Yield: 6.6%

I’ve warned about the long-term difficulties facing cigarette maker Altria (MO) for some time – namely, that the U.S. is in a never-ending crackdown on cigarettes, threatening the company’s core business. Shares have indeed been caught in a downward trend since 2017, but reality really started to catch up with Altria in Q4 2018, as shares plunged far deeper than the broader market. Now MO sits about 15% lower than where it was the last time I cautioned my readers on the stock.

But maybe, just maybe, there’s a contrarian play here?

Wells Fargo seems to think so. Analyst Bonnie Herzog, who rates the stock “Outperform” and has a $65 price target that implies 33% upside from here, doesn’t see any end to Altria’s decline in cigarette sales. But she does think vaping might be the company’s savior, pointing to the company’s $13 billion, 35% stake in e-cigarette maker Juul, announced in December. The money quote:

“One of the key points that continues to be misunderstood, in our view, is that while MO’s cigarette volumes will likely decelerate faster…, the incrementality from MO’s stake in JUUL — strong U.S. share/margin growth and huge upside internationally — is underestimated since we predict MO’s equity income from JUUL will more than offset MO’s shrinking cigarette volume pool.”

And like Tailored Brands, Altria is at least showing big value-and-income numbers. Its yield has plumped up to north of 6%, and its forward P/E of 11 is well, well below the market average.

Altria’s (MO) Yield Hasn’t Been This High Since the Turn of the Decade

Credit where credit is due: Altria isn’t sitting around praying that cigarette sales will magically recover. The investment in Juul was a pricey risk, but one the company needs to take if it wants to stave away irrelevance as its core product deteriorates into a pile of legislative ash.

That said, Juul isn’t immune from the same pressures. The company faces class-action lawsuits in Philadelphia and New York federal courts over the company’s marketing tactics and over its disclosure of nicotine levels. Juul also temporarily halted sales of most of its flavored nicotine pods in November in hopes of getting out in front of aggressive federal regulators worried about spiking e-cigarette use.

If this sounds familiar, it should. This is the same treatment cigarettes have gotten for years … and why Altria still could be in trouble long-term despite its creative wheeling and dealing.

Live Off Dividends Forever With This “Ultimate” Retirement Portfolio

If you’re mapping out a successful retirement portfolio, these three stocks illustrate the right idea: high yields with price potential. We all know you need enough income to cover all of your regular expenses, but investors often overlook the importance of growing their nest egg in retirement – that way, if the unexpected happens, you won’t cripple your dividend-producing potential to dig out of trouble.

But you also need security – and you can’t do that by taking flyers out on deeply troubled stocks like the three picks I just covered.

On April 7, 2017, Tesla (NASDAQ:TSLA) stock cleared $300 for the first time. Tesla stock would close that day at $302.54. Yesterday, TSLA stock closed at $302.56.

Source: Shutterstock

Over the last 22+ months, TSLA stock has risen… 0.07%. Given the intensity of the debate over TSLA — without a doubt the biggest battleground stock in the market — the lack of movement is beyond ironic.

Where does Tesla stock go from here? There are cases on both sides. I’ve long leaned toward the bearish case: I argued in December that TSLA would decline in 2019. That prediction has been right so far, with the stock down 9%. But Tesla has managed to confound the doubters so far, and there are still reasons to believe it will do so again.

The Case for Tesla Stock

At this point, the bull case for TSLA has both short-term and long-term aspects. The long-term case is the same as it’s been for years now: Tesla has the opportunity to revolutionize worldwide energy usage. The company isn’t just about the Model 3 — or even just about automobiles. The solar division, Powerwall, and other future initiatives all offer additional profit opportunities.

A $52 billion market capitalization hardly suggests Tesla stock is cheap, but it’s puny compared to what the valuation could be if Tesla achieves even some of its goals across the energy space. ARK Invest famously has put a $4,000 per share bull case price target on TSLA stock — which would suggest a valuation over $500 billion. Given that Exxon Mobil (NYSE:XOM) is worth about $375 billion, including debt, that figure perhaps isn’t as ludicrous as it sounds.

In the short term, meanwhile, Tesla stock is getting to a point where it doesn’t look that expensive. 2020 analyst EPS estimates are over $9 per share, suggesting a 33x forward P/E multiple. That’s a big number as far as auto stocks go — General Motors (NYSE:GM) and Ford Motor Company (NYSE:F) both trade in the single digits — but it’s a valuation that Tesla at least can grow into. As the company expands into Europe and China, its earnings should grow, and that multiple should come down.

The Case Against TSLA Stock

The case against Tesla stock is starting to build, however, and it comes down to one simple problem: trust. For all the arguments over convertible debt maturities and 25% gross margins and weekly production levels, the broad argument is rather simple.

If Tesla can build cars more effectively and more efficiently than existing manufacturers, TSLA stock probably rises. It will make more money per car than anyone else — and enough to fund its moves into semi trucks, energy storage, and other areas.

If it doesn’t, TSLA stock falls. Auto companies aren’t valued at 30x earnings — or even 20x. Earnings expectations come down, multiples compress, and the Tesla stock price comes down significantly. And so far, we’re simply not seeing much evidence that Tesla is that much better than anyone else at production.

Tesla hasn’t released a $35K Model 3 yet, as promised. It built vehicles in a tent. Target after target has been missed. For all the hype about the 5,000 per week production target (sort of) reached in late June, Tesla hasn’t been able to get back to that level on a consistent basis.

There’s a lot of big talk and big promises out of Tesla. The results — thin profitability and missed goals — haven’t been good enough yet.

The Trust Problem

And with each passing month, it becomes harder to trust Tesla and CEO Elon Musk. Musk clearly violated his settlement with the SEC with Tweets this week initially guiding for production of 500,000 cars this week.

The CEO did correct the tweet four hours later, admittedly. But for those bulls chalking the Tweet up to a simple mistake, it’s worth noting that Musk did the exact same thing on the Q4 conference call last month. He projected 350,000 to 500,000 Model 3s in 2019 — after the shareholder letter issued the same day only guided for 360,000 to 400,000.

At this point, investors perhaps don’t care. Soon after the tweet, Tesla’s general counsel resigned after two months on the job, the latest in a series of executive departures. TSLA stock dropped just 1%.

Investors should care, however. Given the goals here, execution needs to be close to perfect at worst. It hasn’t been. A CEO who continually overpromises doesn’t help on that front. Nor does the revolving door of executives.

The biggest reason to see upside in Tesla stock is the big promises — and the big hopes. The biggest risk to TSLA stock is that the company won’t deliver. For 22 months, the market hasn’t made up its mind as to which is more likely. At some point, it will. Right now, it still seems far too difficult to trust this company — and this CEO — to deliver the rewards they promise.

As of this writing, Vince Martin has no positions in any securities mentioned.

Shares of Walmart (NYSE:WMT) rose on Feb. 19, after the big-box retailer reported fourth-quarter numbers that largely topped expectations. Management also doubled down on a healthy fiscal 2020 guide that implies continued strength across the entire business. Walmart stock traded more than 3% higher in response to the news.

Source: Shutterstock

This rally has legs to keep going.

In the big picture, Walmart has rapidly transformed itself into an omnichannel retailer that is more than holding its own in the top retail dog fight with Amazon (NASDAQ:AMZN).

Many of the company’s new growth initiatives, including e-commerce enhancements and product expansions, are still in their early innings and will continue to drive healthy growth over the next several years. Plus, the company’s acquisition of Flipkart puts Walmart front and center of the world’s hottest and fastest growing consumer retail market.

Overall, there’s a lot to like about Walmart stock in the long run. Current fundamentals imply that Walmart can and will continue to grow revenues and profits at a healthy rate over the next several years. If so, then that means Walmart stock has runway to $115 in calendar 2019.

As such, buyers here won’t be disappointed. The rally in Walmart stock is far from over.

When it comes to retail, two things matter most: price and convenience. Those two things never stop mattering most, either. Consumers always want low prices. They also always want high convenience. Thus, so long as a retailer dominates on price and convenience, that retailer will succeed.

Walmart has been the poster child for low prices and high convenience for a long time. But, Amazon (and e-commerce in general) threatened Walmart’s dominance in those categories by making things cheaper, and by allowing consumers to buy those things from their computers or phones. Walmart naturally lost market share.

But, over the past several quarters, Walmart has adapted. They’ve slashed prices and built out a robust e-commerce business that includes things like “buy online, pick up in store”. As such, Walmart has regained a shared dominance with Amazon on the price and convenience fronts, and Walmart’s numbers have consequently improved.

In the fourth quarter, comparable sales rose 4.2%. That’s a strong mark for any retailer, especially one of Walmart’s size. On a two-year stack basis, comparable sales rose nearly 7%, and that’s the best mark in nine years for Walmart. Traffic growth is positive. Ticket growth is positive. E-commerce growth is red hot. On top of all that, margins are rising, too, for the first time in a long while, as improved top-line results are allowing for expense leverage.

Overall, through developing a robust omnichannel business, Walmart has regained dominance on the price and convenience fronts, and in so doing, has recharged growth throughout the whole business.

Walmart Stock Has More Upside Left

At current levels, Walmart stock has room to move higher over the next several months as revenues and margins move higher, too.

In fiscal 2019, comparable sales rose 3.6%, the best comp mark in years for this company. Next year, comparable sales growth is expected to slow, but not by much (2.75%). Also, revenue growth is expected to remain stable at a multi-year high of 3%-plus. Digital sales growth is guided to remain north of 30%. Margins are expected to move higher, too, excluding one-offs.

In sum, the growth narrative at Walmart is simply getting better. This is turning back into a low single-digit revenue and comparable sales growth narrative with gradually improving margins. Established market growth will inevitably slow over the next several years as current growth initiatives mature. But, such slowing growth will likely be offset by a developing market ramp, especially in India.

As such, Walmart will remain a low single-digit revenue growth company with gradually improving margins for the foreseeable future. Under those modeling assumptions, $7.80 in earnings-per-share seems achievable by fiscal 2025. Based on a historically average 20 forward multiple, that equates to a fiscal 2024 price target of $156. Discounted back by 8% per year (2 points below my average 10% discount rate to account for the yield), that equates to a fiscal 2020 price target for Walmart stock of roughly $115.

Bottom Line on WMT Stock

Walmart has regained its dominance on the price and convenience fronts. So long as Walmart maintains this dominance, the numbers will remain good, and the stock will head higher. Under reasonable growth assumptions, Walmart stock should move towards $115 over the next twelve months.

As of this writing, Luke Lango was long WMT and AMZN.

Brett Owens, Chief Investment Strategist Updated: February 20, 2019

It’s a question I get from investors all the time: “Should I take my dividends in cash or reinvest them through a dividend reinvestment plan (DRIP)?”

My answer: unless you want your cash sitting in your account earning zero, your best bet is to reinvest any dividend money you don’t need to pay your bills.

But we don’t want to practice “buy and hope” investing, either, whether we do it through obsolete DRIPs or the old-fashioned way.

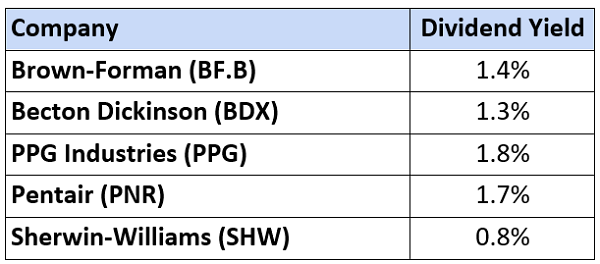

When I say “buy and hope,” I mean putting your cash into household names like the so-called Dividend Aristocrats and “hoping” for higher stock prices when you cash out in retirement.

You’ve probably heard of the 57 stocks on the Aristocrats list, which have raised their payouts for at least 25 straight years. Trouble is, despite their lofty name, these companies hand us a pathetic current dividend of 2.2%, on average. And quite a few pay less than that:

5 Dividend Paupers

So if you invest mainly in the average Dividend Aristocrat (as many people do), you won’t have to worry about reinvesting your dividends. You’ll need every penny of dividend income just to keep the lights on!

That’s because even with a $1-million portfolio, you’re only getting $22,000 in dividend income a year here, on average. That’s not far above poverty-level income for a two-person household.

Pretty sad after a lifetime of saving and investing.

Luckily, there’s a way we can rake in way more dividend cash. I’m talking a steady $75,000 a year in income on a million bucks. And if you’re not a millionaire, don’t worry: a $550k nest egg will bring in $41,200 annually, enough for many folks to retire on.

That’s nearly double the income on our million-dollar Aristocrat portfolio, from a nest egg that’s a little over half the size!

How to Bank an Extra $41,200 in Cash Every Year

I know what you’re thinking: “Brett, that amounts to a 7.5% yield. There’s no way a payout like that can be safe.”

You can be forgiven for thinking that, because you hear it everywhere. But the truth is, there are plenty of safe payers throwing off at least that much, like the 21 stocks and funds in my Contrarian Income Report service’s portfolio (which I’ll show you when you click here).

Right now, these 21 sturdy investments yield 7.5%, on average. And every month I personally run each one through a rigorous dividend-safety check, starting with three things that are absolutely critical:

Rising free cash flow (FCF)—unlike net income, which is an accounting measure that can be manipulated, FCF is a snapshot of how much cash a company is making once it’s paid the cost of maintaining and growing its business;

A payout ratio of 50% or less. The payout ratio is the percentage of FCF that went out the door as dividends in the last 12 months. Real estate investment trusts (REITs) use a different measure called funds from operations (FFO) and can handle higher payout ratios, sometimes up to 90%;

A healthy balance sheet, with ample cash on hand and reasonable debt.

Making DRIPs Obsolete

The best part is, these 21 investments are perfect for dividend reinvestment because each one gives us a dead-giveaway signal of when it’s time to buy, sit tight—or sell and look elsewhere for upside to go with our 7.5%+ income stream.

That makes DRIPs obsolete!

Because why would we mindlessly roll our dividend cash into a particular stock every quarter when, at a glance, we can pinpoint exactly where to strike for the biggest upside?

To show you what I mean, consider closed-end funds (CEFs), an overlooked corner of the market where dividends of 7.5% and up are common. We hold 11 CEFs in our Contrarian Income Reportportfolio, mainly larger issues with market caps of $1 billion or higher.

We don’t have to get into the weeds, but CEFs give off a crystal-clear signal that a big price rise is coming. You’ll find it in the discount to NAV, which is the percentage by which the fund’s market price trails the market value of all the assets in its portfolio.

This number is easy to spot and available on pretty well any fund screener.

This makes our plan simple: wait for the discount to sink below its normal level and make your move. Then keep rolling your dividend cash into that fund until its discount reverts to “normal.”

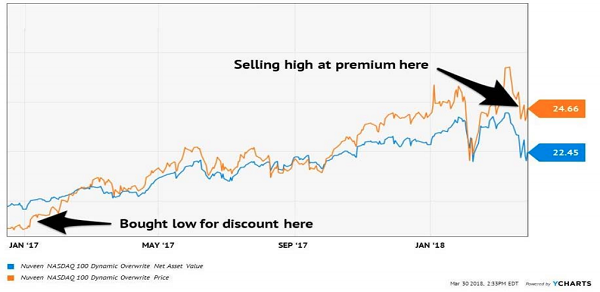

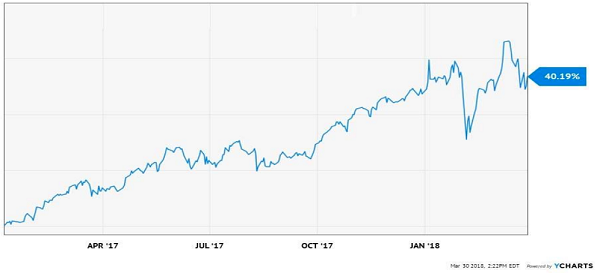

That’s exactly what we did with the Nuveen NASDAQ 100 Dynamic Overwrite Fund (QQQX)back in January 2017—and the results were breathtaking.

How We Bagged a 40% Total Return (With a 7.5% Yield) in 15 Months

QQQX’s management team cherry picks the best stocks on the NASDAQ, juices their high yields with a low-risk options strategy, then dishes distributions out to shareholders. Back on January 6, 2017, QQQX was trading at a 6% discount to NAV and paid a 7.5% dividend.

That triggered our initial move into the fund. And over the next 15 months, we bagged two dividend increases and watched as QQQX’s discount swung to a massive premium—so much so that by the end of that period, the herd was ready to ante up $1.13 for every buck of assets in QQQX’s portfolio!

Discount Window Slams Shut…

That huge swing from a discount to a premium catapulted us to a fat 40% gain (including dividends). But the fund’s outrageous premium meant its upside was pretty well maxed out by the time we took our money off the table on April 6, 2018.

… and Delivers a Fast 40% Gain

And what’s happened since?

QQQX has plunged 6% (including dividends!), far underperforming the market’s 7.8% total return.

Premium Gives Us the Perfect Exit

Forget QQQX: Grab These 8% Monthly Dividends Instead

Here’s the punchline on QQQX: despite the loss it’s posted since last spring, it still trades at a 2% premium to NAV!

Why the heck would we overpay when the ridiculously inefficient CEF market is throwing us bargain after bargain as I write this?

There’s one more thing I have to tell you: many of these cheap CEFs pay dividends monthly instead of quarterly. So if you hold them in your retirement portfolio, their massive dividend payouts will roll in on exactly the same schedule as your monthly bills!

Convenience isn’t the only reason to love monthly payers, though. Because they also let you reinvest your payouts faster, amplifying your gains (and income stream) as you do.

I’m talking about an automatic “set-it-and-forget-it” CASH machine here!

The best news? You can kick-start your monthly income stream without doing a single moment of legwork … because I’ve done it all for you.