Large-cap tech stocks have led the great market rebound of 2019. Today we’ll look at three of the top stocks to trade in the sector.

Chart watchers are detectives seeking clues. These signals reveal the path of least resistance for prices and enable traders to discover attractive buy points that offer low risk and high reward. In analyzing the technology sector, two items stand out that suggest it should maintain a leadership role.

First, unlike the S&P 500 and Russell 2000, the tech-heavy Nasdaq saw increasing momentum on its last upswing. Trends with growing momentum have a higher likelihood of continuation than reversal. The second piece is related to the first: the tech sector’s relative strength. The tech sector’s outperformance is a good omen that should continue attracting performance chasers.

Here are three top stocks to trade.

Click to EnlargeSource: ThinkorSwim

Advanced Micro Devices (AMD)

Advanced Micro Devices (NASDAQ:AMD) is an active trader’s dream stock. Its massive volatility delivers quick profits to those on the right side of the trend. And it exhibits clean trending behavior responding well to common support and resistance zones.

Last week’s breakout resulted in a rapid three-day 20% surge amid heavy accumulation. Spectators who missed it now have a second chance. With this week’s pullback, AMD stock has now returned to the scene of the crime. This is as good a buy-the-dip pattern as there is. Watch for signs of an upside reversal such as breaking a prior day’s high, then buy.

Options traders might consider selling the May $22 puts for $90 of cash flow per contract.

Click to EnlargeSource: ThinkorSwim

Alphabet (GOOGL)

This year’s uptrend in Alphabet (NASDAQ:GOOGL,NASDAQ:GOOG) has been incredibly orderly. The series of higher pivot lows is consistent, and both the 20-day and 50-day moving averages are rising in bullish fashion. Additionally, the past three upswings have seen strong bullish candles with upside follow through. This type of clean price action has made GOOGL one of the easier stocks to trade of late.

With today’s mild selloff, GOOGL stock is working on its fifth down day in a row. The lower-than-average volume suggests we’re seeing garden-variety profit taking versus widespread distribution. Potential support looms close at $1150 and $1140, so I suspect a bounce is nigh.

If the stock can take out today’s intra-day high ($1,177), then buy the May $1175/$1195 bull call spread for around $5.

Click to EnlargeSource: ThinkorSwim

Microsoft (MSFT)

Microsoft (NASDAQ:MSFT) rounds out today’s trio with a shallow retracement pattern. The software king notched a fresh record high last week — $120.82 — on strong momentum. The reach to new heights came following a high volume breakout of last year’s high water mark.

Given all the bullishness, I see little reason why the current dip won’t get gobbled up like all its predecessors.

Implied volatility is low making long option plays attractive. I like buying the May $115/$125 bull call for around $4.

As of this writing, Tyler Craig held bullish positions in AMD. Check out his recently released Bear Market Survival Guide to learn how to defend your portfolio against market volatility.

One of the big, sparsely covered parts of President Trump’s plan to overhaul the government is his administration’s focus on revamping how many government agencies operate.

In 2018 the White House put out proposals to transform agencies in the areas of food, education, social services and air travel. Top on the list are to get the federal government less involved in the mortgage insurance business with the overhaul of Fannie Mae and Freddie Mac, the two mortgage securitization and guarantee companies that were nationalized by the Federal government during the 2007-2008 financial crisis. A recapitalization of the two mortgage giants would be a huge benefit to one particular high yield stock.

Fannie (founded 1938) and Freddie (in 1970) were set up as private corporations to expand the availability of home mortgages through securitization and guarantees of payment of principal and interest. The two were created by Acts of Congress and were commonly referred to as government sponsored entities (GSE’s). What you had were private companies whose businesses had an implied Federal government backing.

You may remember that the 2007-2008 financial crisis was triggered by an implosion of the mortgage-backed securities markets. As the largest issuers of this type of securities, the two GSE’s faced total collapse and went to the government for a bailout. On September 7, 2008, Federal Housing Finance Agency (FHFA) director James B. Lockhart III announced he had put Fannie Mae and Freddie Mac under the conservatorship of the FHFA. The action has been described as “one of the most sweeping government interventions in private financial markets in decades”. The two GSE’s have been “wards” of the government ever since, which is now going on 11 years.

Under complete government control, the two companies have continued to provide mortgage insurance, buy mortgages and issue new mortgage securitizations. The companies are profitable and have been paying out those profits as large dividends paid into the Federal Treasury.

Before the government takeover, Freddie and Fannie were both publicly traded corporations. Shares of the two remain in investor hands. The problem is that investors currently get no benefit from the business success of the two. The Trump plan involves getting Fannie and Freddie out from under government control and back into the public arena. Details need to be worked out between the White House and Congress.

What will happen with Fannie and Freddie unleashed with be a more competitive mortgage origination and mortgage services market place. High-yield New Residential Investment Corp. (NYSE: NRZ) is one company that has built a very well run business in the mortgage securities and mortgage servicing world. The potential synergies of doing synergetic business with the two GSE’s should be extremely beneficial to New Residential.

NRZ’s primary business is owning and managing an investment portfolio of mortgage servicing rights (MSRs). These are the payments taken from every mortgage payment to pay the servicing company. When purchased at the right price, this is a very profitable business. The company has consistently generated mid-teens annual returns with this very specialized financial instrument. I can see New Residential collaborating with Fannie and/or Freddie in the area of MSR management for the benefit of both parties.

In 2018 New Residential acquired a full service mortgage servicing business. The GSE’s are not engaged in servicing so, being able to offer the full range of mortgage servicing services to Fannie and Freddie would be another area of collaboration. As the world now works, NRZ is a very well run and profitable company that pays big dividends, resulting in a high-yield stock. The proposed government spin-off of Fannie and Freddie would only increase NRZ’s growth potential. The shares currently yield 12.1%.Mueller Report a Dud: Trump unleashes the greatest income stream in American history

While Congress and the media were too busy looking for Russians, 16 of Trump’s Executive Orders could’ve just launched a little-known income opportunity called ‘venture royalties.’

They’re approved by Congress and Americans are collecting checks every month for $2,123… even $9,586. Everyone is asking me about income right now, I’m pointing to venture royalties. Here’s how to collect 14 royalty checks this year. Click here.

The 5G revolution is coming, and to help you cash in on the transformation, these are the best 5G stocks to watch in 2019.

In fact, the revolution could be as great as the rollout of personal computers and the introduction of the Internet. These made fortunes for investors who got in early.

In October 2018, Verizon Communications Inc. (NYSE: VZ) said it had started to activate the first-ever 5G network in the United States. The 5G capability, rolled out in four U.S. cities, is expected to expand throughout 2019 and 2020.

Currently, data networks in the United States run on 4G. Your smartphone, for example, is likely a 4G phone.

But the upgrade to 5G won’t just mean a faster connection – it could transform the entire economy. 5G will enable self-driving cars to become a reality because autonomous cars need continuous, rapid access to real-time data. That also means they need the constant, high-speed connection 5G offers.

The Internet of Things (IoT), which will enable devices to talk to each other across businesses and homes, will move faster and more conveniently on 5G.

Plus, broadband-like speeds will allow you to connect to the Internet anywhere. That could change how we look at Internet services and cable television.

Fortunately, all the disruption 5G networks will bring is creating an opportunity for investors.

These are our best 5G stocks to watch in 2019, and they’re poised to reward investors.

Best 5G Stocks to Watch in 2019, No. 5: Keysight Technologies Inc.

Keysight Technologies Inc. (NYSE: KEYS) is a U.S. electronics firm that develops equipment and software for measurement and analysis of electrical statistics.

That may sound niche, but Keysight has developed its business to be crucial to the 5G expansion of networks. 5G will require a network of hardwiring and towers to function properly. To put the network together, 5G companies will need to analyze and collect data. Keysight makes the instruments necessary to do this.

Two years ago, KEYS worked with semiconductor company Qualcomm Inc. (NASDAQ: QCOM) to demonstrate the first 5G data connection with a modem chipset.

It’s very likely to become a key player given that history.

Further, Wall Street analysts forecast a $100 share price in the next 12 months – a nice 17% advance from the current $84.94 share price.

Best 5G Stocks to Watch in 2019, No. 4: Intel Corp.

Venerable semiconductor maker Intel Corp. (NASDAQ: INTC) is the second largest global chipmaker.

It doesn’t intend to be a slouch in the 5G market, either. In fact, the company has spent the last 10 years making sure it dominates the market.

Eight years ago, INTC bought Infineon, a modem maker based in Germany. It’s the only company that supplies modems to tech giant Apple Inc. (NASDAQ: AAPL). AAPL uses the modem chips from Infineon to connect iPhones to networks.

So now INTC has an exclusive supplier relationship with Apple, one of the biggest device makers on the planet.

INTC plans to launch a 5G modem in 2019 too. That will be a big help in ushering the iPhone into the 5G world.

But the 5G modems are also planned for automakers for use in self-driving cars and for industrial manufacturers for the IoT.

Wall Street analysts have a target price on INTC of $70 – a nearly 30% climb from today’s $54 share price.

INTC currently has a 3.75 VQScore. While it’s a good buy, you are likely to get an even better price – and therefore better potential price appreciation – if you buy on the next dip.

Best 5G Stocks to Watch in 2019, No. 3: Apple Inc.

And just like we said above, tech behemoth Apple is primed for the 5G revolution.

Apple has been seeing the effects of lagging sales for its flagship product, the iPhone, driven by weakening sales in China and throughout the globe.

So much so that AAPL’s earnings report in January showed a drop in revenue of 5%. And the company lowered guidance for future quarters. Sales in the current quarter are forecast to decline up to 10%.

Apple needs to breathe new life into its old products. And 5G phones could be the innovation the company needs.

Apple and Intel are working together to see that they both capitalize on the new 5G networks.

Plus, Apple has been working on a self-driving car beginning in 2014. 5G is likely to be a gigantic boost to these plans.

AAPL enjoys an excellent 4.45 VQScore, putting the stock right in the “Buy Zone.” Analysts on Wall Street project that AAPL shares could rise up to 40% over the next 12 months, which might turn out to be overly conservative.

Best 5G Stocks to Watch in 2019, No. 2: Micron Technology Inc.

Micron Technology Inc. (NASDAQ: MU) produces hardware used in manufacturing both semiconductors and computers worldwide.

It has been making plans for the 5G revolution for some time, developing a multichip package for use in 5G modems.

Its current product was developed to provide modems with the capability to run as much as 20 times faster than current modems.

MU’s products will be used in every sector that uses 5G.

Right now, MU has the highest VQScore of the 5G stocks bunch, at 4.75. Wall Street analysts have set a $90 target price on the stock. That’s an almost 125% increase from today’s $39.75 share price.

But our top 5G stock to watch is flying under the radar right now…

Best 5G Stocks to Watch in 2019, No. 1: Skyworks Solutions Inc.

Skyworks Solutions Inc. (NASDAQ: SWKS) is a U.S. semiconductor producer based in Massachusetts. It makes analog chips for 5G.

SWKS is going to benefit from two trends related to 5G. The first is the sheer number of sectors that are going to need 5G chips. You name the sector; it’s going to be moving into 5G.

But the second and even more significant trend is the role of 5G in mobile devices – and the profit picture for the company.

Every time the mobile network upgrades, Skyworks’ products get more profitable.

For 3G network phones, SWKS booked a profit of about $8 per phone. For 4G network phones, that figure rose more than 100% to $18.

Management forecasts that 5G phones will make the company $25 per phone, another 38% increase in profit.

Not only that, but mobile phones make up 73% of sales as of the first quarter. That means that the climb in mobile phone profit will be really good news.

Wall Street analysts forecast that the company’s shares will sell for $173 once the 5G revolution is underway, a 113% jump from the current $83.26 level.

But this could be the true breakout stock once 5G gets here…

U.S. equities are recovering on Tuesday thanks to a steepening of the yield curve. Put more simply, the bond market is suddenly feeling a little less worried about the specter of a recession after long-term rates fell below a critical short-term rate recently.

Stocks are taking their cue from this larger and much more important marketplace, helping the S&P 500 push back over the critical 2,800 level. Will the move above this threshold, which has confounded the bulls repeatedly since October, finally be definitively crossed?

If it is, newfound strength in the energy sector will be a key driver. Quietly, hoping not to attract attention to itself, crude oil has been steadily gaining ground since bottoming in December. With the start of the summer driving season near, West Texas Intermediate is once more flirting with the $60-a-barrel level. The Energy Select Sector SPDR (NYSEARCA:XLE) is following suit, preparing for a move up and over its 200-day moving average.

While I’ve recently discussed a few mega-cap energy stocks, here is a look at four slightly smaller names that are worth a look:

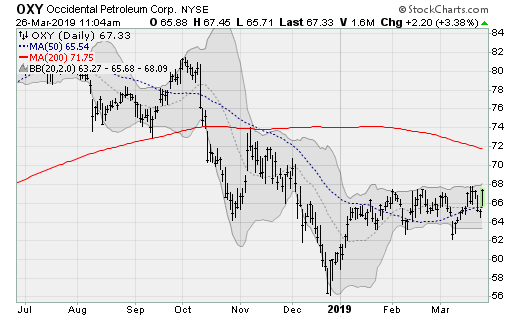

Occidental Petroleum (OXY)

Shares of Occidental Petroleum (NYSE:OXY) are preparing to break up and and out of a tight three-month consolidation range as it extends away from a rising 50-day moving average. Next stop is a test of the 200-day average, which would be worth a gain of 6% from here. The company recently announced that it plans to double crude exports to 600,000 barrels per day in 2020.

The company will next report results on May 8 after the close. Analysts are looking for earnings of 76 cents per share on revenues of $4.1 billion. When the company last reported on February 12, earnings of $1.22 per share beat estimates by six cents on a 33.8% rise in revenues.

ConocoPhillips (COP)

ConocoPhillips (NYSE:COP) shares are rising again above its 200-day moving average, returning to the upper end of a trading range going back to late October. Already enjoying a 20%+ rally off of its late December low, watch for a move to prior highs near $78 — which would be worth a gain of more than 14% from current levels.

The company will next report results on April 25 before the bell. Analysts are looking for earnings of 76 cents per share on revenues of $8.5 billion. When the company last reported on January 31, earnings of $1.13 per share beat estimates by 11 cents on over $9.1 billion in revenue.

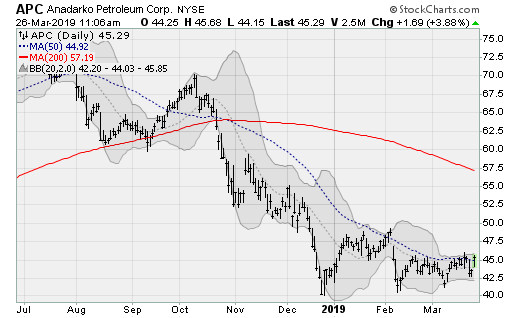

Anadarko Petroleum (APC)

Anadarko Petroleum (NYSE:APC) shares are coiling up nicely within a four-month consolidation range, readying a powerful breakout that should see a test of the 200-day moving average. Such a move would be worth a gain of nearly 30% from here. The stock has been stock in a multi-year trading range, with resistance near $75 (first reached in 2011) and support near $40 (in place since late 2017).

The company will next report results on April 30 after the close. Analysts are looking for earnings of 19 cents per share on revenues of nearly $3 billion. When the company last reported on February 5, earnings of 38 cents per share missed estimates by 24 cents on a 14.3% rise in revenues.

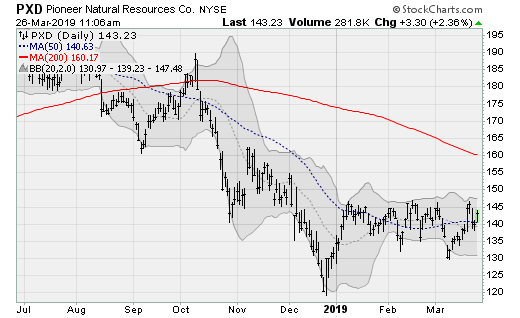

Pioneer Natural Resources (PXD)

Similar to other names on this list, Pioneer Natural Resources (NYSE:PXD) is enjoying a solid base of support after months within a tight consolidation range that sets up a run at its 200-day moving average. Such a move would be worth a gain of more than 11%. Shares of shrugged off some bad news, including a downgrade from Mizuho on March 19.

The company will next report results on May 1 after the close. Analysts are looking for earnings of $1.52 per share on revenues of $2.2 billion. When the company last reported on February 13, earnings of $1.18 per share missed estimates by 16 cents despite a 75.4% rise in revenues.

As of this writing, the author held no shares in the aforementioned securities.

Don’t become complacent with your dividends! Your portfolio and your income are at the whim of Fed Chair Jerome Powell—now more than ever.

I realize he’s acting like a “good boy” at the moment. But what if JP decides to go rogue again and exercise his independence? A surprise rate hike would be catastrophic to many income portfolios.

That means you need to “Fed-proof” your nest egg and your dividends. Today we’ll discuss four funds paying dividends up to 10.7% that do just that.

These four closed-end funds (CEFs) have been left for dead in this market rally. That makes them great “Fed insurance”: they’re cheap, so they’ve got built-in upside if the rally goes into overtime.

If stocks flame out, they’ll likely just trade flat. And we’ll still grab their outsized dividends!

More on these four “Fed-proof” plays—ranked from worst to first—shortly. First, we need to talk about Jerome Powell.

Stocks: Say the Magic Word

Let’s rewind to the holiday season.

Back then, the first-level crowd—beaten down by the selloff—was desperate for any reason to jump into stocks. They found it in early January, when Powell said the central bank would be “patient” with the pace of rate hikes.

Between then and the end of the month, when the minutes of the latest Federal Reserve meeting came out, stocks did this:

“Boring” Fed Excites Investors

Here’s the crazy thing: those January 30 minutes said nothing—the Fed just said “patient” a few more times. And investors doubled down!

More “Patients,” More Gains

No, it wasn’t economic numbers that drove this “second stage” of gains: unemployment was 3.8% in February, a bit lower than 3.9% in December. Fourth-quarter earnings rose double-digits, as they’ve done for five straight quarters now.

That leaves us with the Fed, which we can thank (or curse, if you’re hunting for cheap dividends) for this market run.

Time to Buy “Fed Insurance”

Nobody knows how long this “Fed rally” will last. Powell’s “patient” line could be drowned out tomorrow. Or he could roll out a rate cut, igniting stocks again.

Either way, we’re not going to sit on the sidelines. Our next move starts with …

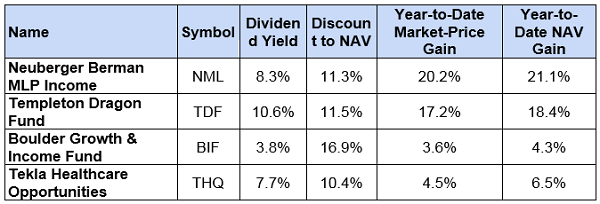

4 “Fed-Proof” Dividends on the Cheap

As you can see, each is cheap in two critical ways: a double-digit discount to NAV (in other words, their market prices are way below their portfolio values), and NAV gains that have outraced their market-price gains this year.

Translation: management is putting up better numbers than it’s getting credit for!

But that doesn’t mean they’re all great buys now. Let’s take a trip through these four, in order of appeal:

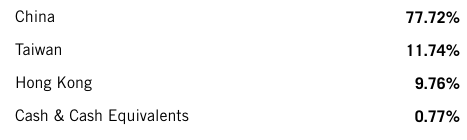

Worst: Templeton Dragon Fund (TDF)

TDF boasts the biggest dividend yield of our quartet (10.6%!), the biggest discount to NAV (11.5%) and a portfolio that has topped the fund’s market price this year.

That’s where the good news ends for TDF.

For starters, as its name suggests, the fund has 78% of its assets in China, whose economy is slowing, partly due to President Trump’s trade war.

A Lead Weight

Source: FranklinTempleton.com

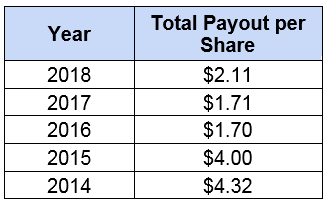

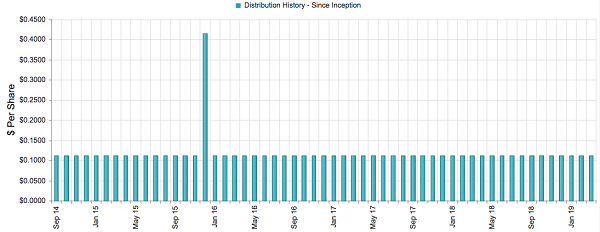

What’s more, TDF’s dividend is as erratic as they come: according to Templeton’s website, the rate is set “based on current market conditions,” and the payout only goes out semi-annually. That makes TDF unappealing for anyone trying to set up a predictable income stream. Check out how lumpy TDF’s payout has been:

TDF’s Gyrating Dividend

Source: CEFConnect.com

So let’s pass on TDF and move on to a fund with a bit more appeal, thanks to its deep roots in the USA.

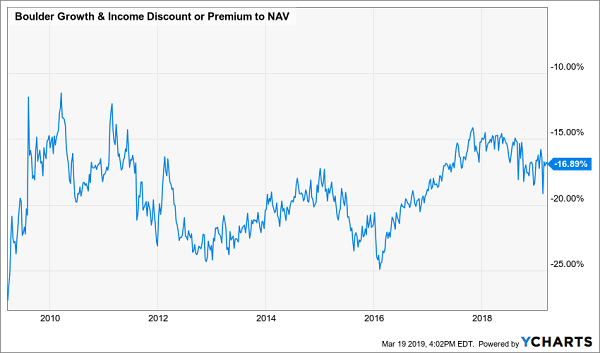

Mediocre: Boulder Growth & Income Fund (BIF)

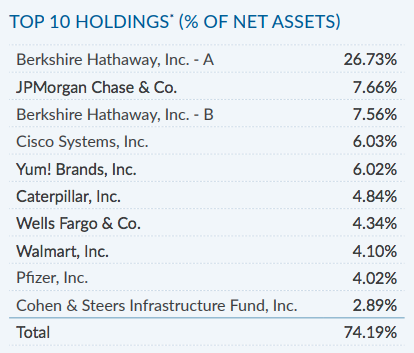

BIF sports the biggest discount of our quartet, at 16.9%. It also has the best pedigree, tapping the value-investing strategies of Warren Buffett.

If you’ve wanted to hold Buffett’s Berkshire Hathaway (BRK.A) but have shied away because it lacks a dividend (and a class A share goes for $307,000!), BIF, with its 3.8% yield, is for you: Berkshire accounts for a third of its holdings:

Source: Boulder Growth and Income Fund Fact Sheet

So why is BIF only my third-best pick?

First, the dividend is paltry for a CEF, and BIF recently switched from a quarterly to a monthly payout—a monthly dividend is a better deal if you’re leaning on your portfolio for income, because your cash flow matches up with your bills.

(You can get my favorite monthly payers now in my “8% Monthly Payer Portfolio,” which I’ll give you when you click here).

Second, by leaning so heavily on one stock, management isn’t providing a lot of value for their 0.98% fee. And third, BIF’s 16.9% discount has been locked at a low level for a decade, so it’s tough to see any “snap-back” upside here:

BIF’s Never-Ending Sale

Still, if you want to buy Berkshire and other big caps, BIF could be worth a look; you’ll get a dividend that doubles the yield on the SPDR S&P 500 ETF (SPY).

Better: The Neuberger Berman MLP Income Fund (NML)

NML holds pipeline master limited partnerships (MLPs) and has posted the biggest market-price gain of our group—a run that’s been topped by its NAV. There’s reason to expect more: even after its rebound, NML’s market price is still well off the two-year highs it hit in January 2018.

That’s because it started from a low base: energy generally, and NML in particular, took a hard hit in the 2018 selloff, illustrating a big risk of holding NML: volatility. The CEF sports a beta rating of 1.4, making it 40% more volatile than the S&P 500.

However, it does trade at an 11.3% discount to NAV—below the 9.2% average in the past year—so there’s potential for some discount-driven gains here, too, as US oil production continues to rise: NML’s holdings are all in the US.

The dividend is sustainable at 8.3%, thanks to that big discount. That’s because the yield on NAV—or what NML needs from its portfolio to keep its payout steady—is just 7.3%, way below the 21% total NAV return it’s already seen this year.

Finally, most MLPs will kick you a K-1 tax form around your return deadline and annoy you and your accountant. NML gets around this by issuing you one neat 1099.

But if you’re still leery about the always-wild energy space after this big run-up, put NML on your watch list and go with my top “Fed-proof” buy.

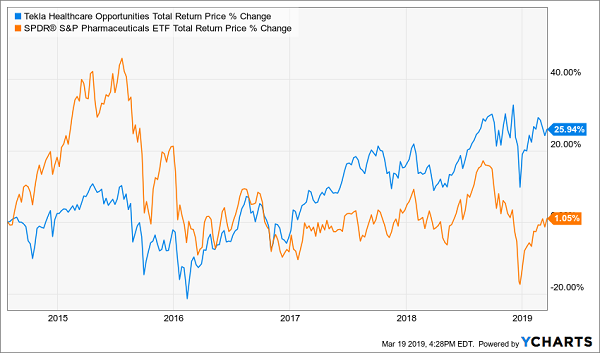

Best: The Tekla Healthcare Opportunities Fund (THQ)

The biggest upside is with THQ, whose NAV has overshot its price by a mile this year. It’s only a matter of time before its price closes that gap again:

THQ’s “NAV Magnet”

Plus, its discount, currently 10.3%, has been as narrow as 6.25% in the last 18 months—the second ingredient for at least 10% upside here.

THQ is no dividend slouch, either, with a 7.7% yield on market price translates to just a 7% yield on NAV, which is already nearly covered by its 6.5% year-to-date NAV return. A 7% yearly NAV return is a cinch for Tekla going forward, too. It employs financial pros and medical researchers to get a jump on the next pharma breakthrough.

That strategy is proven: check out THQ’s lifetime return versus the SPDR S&P Pharmaceuticals ETF (XPH):

Expert Management Pays Off

Finally, THQ pays dividends monthly—a nice extra benefit for retirees and anyone else leaning on their portfolio to pay the bills.

Rx for a Happy Retirement

5 More “Fed-Proof” Monthly Dividends Up to 9.9%

THQ is just one monthly dividend payer I’m pounding the table on now.

My Contrarian Income Report portfolio boasts 5 more monthly paying stocks and funds that are also terrific buys, as the market sits on pins and needles, waiting for Powell’s next change of heart.

Each of these income powerhouses gives us the sky-high yields (7% on average, with one paying an incredible 9.9% in cash!) and steep discounts we need to thrive, no matter what happens with the Fed—or the economy.

They’re just a click away—all you need to do is take CIR for a quick, no-commitment road test to get your hands on these 5 cash machines now, plus all 19 income plays in this dynamic portfolio (average yield: 7.4%; highest yield: 11.9%!).

That’s not all, either, because you also get …

“Monthly Dividend Superstars: 8% Yields With 10% Upside”

This breakthrough Special Report lays out my top monthly paying buys—the very best of the best picks for your portfolio right now. You’ll discover:

An 8% payer that’s set to rake in huge profits from an artificially depressed sector.

The brainchild of one of the top fund managers that’s giving out generous 9.1% yields.

A steady Eddie high-yielder that barely blinks when stocks plummet. (This one is my favorite “Fed insurance” play of all.)

There are generally two reasons why a stock a sudden, big move. Either the overall market is having a big up or down day (the systemic effect). Or, the company itself has some specific news item causing a large move (the idiosyncratic effect). Most stock specific news is related to earnings or product announcements, although sometimes it can be something entirely random.

Sticking with the more standard explanations, we tend to see gap moves in stocks after a surprising earnings announcement or an unexpected product announcement. Earnings surprises are generally straightforward but product surprises are a different matter. What kind of product announcement can cause a stock to gap (usually higher)?

In most cases, a surprise product announcement is one that comes entirely out of left field. We’re not talking about the next edition of an iPhone, but instead the unveiling of an entirely new product line.

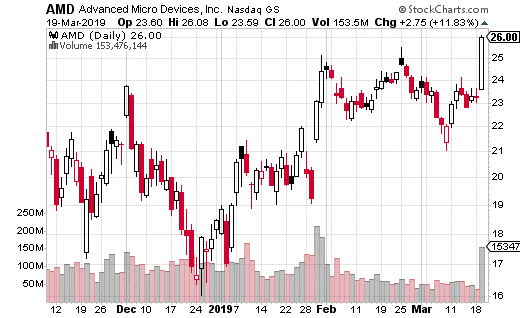

For a perfect example, look what just happened with Advanced Micro Devices(NASDAQ: AMD).

AMD is one of the biggest graphic card companies in the world (GPUs). The company’s Radeon line of graphics cards are particular prevalent in the gaming universe. The video game industry is huge and continues to grow as e-sports becomes a more mainstream phenomenon.

So, when Alphabet(NASDAQ: GOOGL) announced a new video game streaming platform called Stadia, it was huge news. What was even bigger news for AMD is that Google announced it would be using their GPUs to render the graphics for its new gaming system.

The response by investors was overwhelming positive for AMD – and why it shouldn’t it be? There’s a massive amount of potential with this service and it will clearly boost sales and profits for the company. In fact, the stock jumped 12% on the day of the announcement.

What’s more, bullish options action in AMD substantially increased. The 30-day average for bullish trades on AMD was at 60% of activity. But, the day of the announcement, bullish activity jumped to 76% of all options activity.

One strike and expiration which saw a lot of action in particular was the 27.5 strike expiring on April 5th. With the stock price around $25.50 about 2,000 of these calls were bought for about 40 cents. That’s a breakeven price of $27.90 for roughly a two-week trade.

The stock closed at $26 the day of the spike, so the trader clearly thinks the stock will keep running. The buyer is spending about $80,000 on this bullish trade, but could generate $200,000 per $1 above the breakeven price.

If you want to make a short-term bet on AMD continuing its climb, buying those short-term calls is a reasonable trade. However, you can also buy yourself more time without spending too much more in premium.

The April 18th 27 calls cost about $1 with the stock at $26. So, for a full month before expiration (and with the stock 50 cents higher and the strike 50 cents lower) you can spend $1 instead of $0.40. The breakeven point is still right around $28, but you have 2 additional weeks (and about 4 total weeks) for the trade to work.

That’s a reasonable tradeoff in my opinion and will give you a better chance to succeed if the stock keeps climbing. Given the massively bullish news, it certainly wouldn’t shock me if the stock takes a shot at $30 or above in the near future.

The next U.S. economic recession is coming. Guaranteed!

It is likely that you are reading many predictions concerning the next recession. Last year the pundits were predicting one for 2019. Now I am seeing more predictions for a recession in 2020 or 2021. These predictions are mostly about marketing, because the people making the guesses on the next recession are betting on a sure thing. The economy does cycle, so at some point in the future we will go through a period of negative economic growth.

Predicting the timing of the next recession is a harder task.

At the current time I would say any prediction that ends up correct was more of a lucky guess than from astute analysis. The economy continues to chug along at a moderate 2% to 3% annual GDP growth rate. The economic indicators that traditionally are leading clues for the next economic slow down are giving mixed signals, with a slight bias towards continued growth. Yet it is good to have a plan and some investments in your portfolio that are recession resistant. There is always the possibility of an unforeseen economic event that pushes the economy into negative growth.

Recession resistant income stocks are those that meet two criteria:

First, they have businesses that will continue to generate revenue and free cash flow even in a negative growth economy.

Second, we want to own shares of companies with above average free cash flow coverage of the current dividend rate. Excess cash flow gives a company’s board of directors’ confidence to not cut dividend rates when the economy is under pressure.

Understand that in a recession driven bear market all stock prices will fall.

As high yield stock investors we want to ride through the bear market and subsequent stock recovery with our dividend earnings intact. This allows us to buy more shares when prices are down and boost portfolio income coming out the other side. Remember for the same reasons a recession is inevitable, so is the following recovery. The economy goes through cycles.

Here are three stocks that should be able to sustain and possibly grow their dividends through the next economic recession.

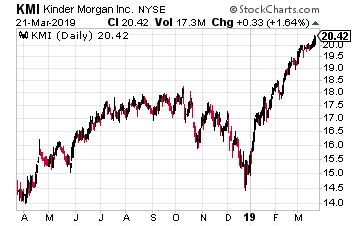

Kinder Morgan Inc. (NYSE: KMI) is a large-cap owner and operator of energy infrastructure assets.

The company owns an interest in or operates approximately 84,000 miles of pipelines and 157 terminals. The pipelines transport natural gas, refined petroleum products, crude oil, carbon dioxide and more. The terminals store and handle petroleum products, chemicals and other products.

Management guidance has 2019 distributable cash flow $5 billion, providing 2.2 times coverage of this year’s dividend payments. That is much better than the typical 1.3 to 1.5 times coverage prevalent in the energy infrastructure space.

Kinder Morgan plans to increase the dividend by 25% this year and next year.

The shares yield 4.0%.

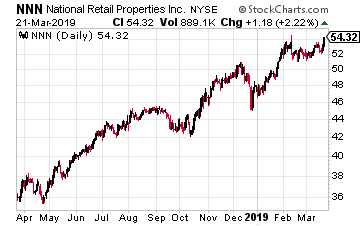

National Retail Properties, Inc. (NYSE: NNN) is a triple-net lease REIT that 3,000 single tenant retail properties in 48 states.

The properties are leased and operated by businesses that won’t go out of business in an economic recession. Think of your local convenience stores, auto parts shops and movie theaters.

For 2018, the company’s dividend payout ratio was 77% of adjusted funds from operations (AFFO). This is very solid dividend coverage for a net lease REIT.

This company has increased its dividend for 29 consecutive years, which means the dividend has grown through the last several economic recessions. That’s a record a Board of Directors will not want to stop.

NNN shares yield 3.8%.

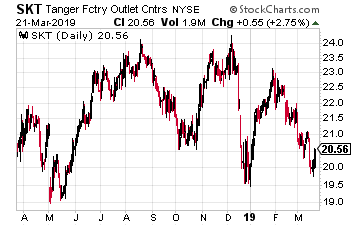

Tanger Factor Outlet Centers (NYSE: SKT) owns and operates 44 outlet center type shopping malls.

Tanger was an originator of this type of mall and is the only pure play outlet center REIT. This type of mall will outperform other retail sectors when the economy is going through a slowdown. People always will shop. They are more likely to shop at an outlet mall if they believe times are tough.

Tanger operates very conservatively, with a low debt ratio and dividend well covered by cash flow. The SKT dividend has been increased every year since the company’s 1993 IPO.

So close, and yet so far. That sums up the state of the markets recently, with investors jittery over the sudden chill surrounding U.S.-China relations. In an about-face on the trade dispute, President Trump conceded that tariffs on Chinese goods may remain for a “substantial period of time.” Simultaneously, this hurts the broader markets but it also raises prospects for cheap stocks.

I know what you’re thinking: why should I consider cheap stocks to buy when blue-chip names are also available for deeply discounted prices? Far be it from me to disagree with that logic. Typically, you accrue the biggest profits from striking while others are panicking. But after you’re comfortable with your high-probability bets, penny stocks provide exceptionally robust return potential.

We should also discuss the “under-the-radar” argument. News such as the trade-war dispute disproportionately hurt the blue chips because they’re usually multinational corporations with global vulnerabilities. While penny stocks also suffer the trickle-down effect, they’re more likely to move on sector-specific developments.

With that in mind, let’s take a look at three (very) cheap stocks to buy that are worth every penny:

Entrée Resources (NYSEAMERICAN:EGI) is one of the penny stocks that actually benefits from broader and sector-specific trends. With all eyes focused on the suddenly deteriorating trade-war dispute, investors get nervous. When investors get nervous, they buy gold. Naturally, as a gold miner, EGI has a lot to gain.

Another thing that intrigued me about EGI as a candidate for cheap stocks to buy is its locality. Most speculative miners have projects in extremely unstable countries just begging for nationalization. While Entrée’s main property in Mongolia isn’t the greatest region for stability, it’s also not the worst. Over the last few years, Mongolia improved its standing for ease of doing business.

Additionally, the gold price has also improved, gaining roughly 10% since the first of October. That’s a net positive for EGI stock, especially since it might go higher still. However, keep in mind that gold is extremely volatile, so don’t lever yourself excessively.

Genius Brands International (GNUS)

Source: Shutterstock

The entertainment industry is a tough sector in which to survive, let alone thrive. What works and what doesn’t often seem arbitrary. Moreover, maintaining relevance is a gargantuan task once you’ve accomplished the already difficult task of delivering a hit. But the prospect of finding that hit drives Genius Brands International(NASDAQ:GNUS).

GNUS specializes in creating compelling content and characters. Where it differs compared to other cheap stocks in the entertainment field is the company’s core audience: toddlers to tweens. This is an exceptionally challenging market to crack because you’re dealing with two audiences: the young consumer and their parents/guardians.

At the same time, GNUS has a viable pathway to profound growth. The reason? Brands such as cartoon characters translate very well internationally. If it resonates in America, it will probably resonate everywhere else.

Novavax (NVAX)

Source: Shutterstock

Over the past few years, vaccination captured the public’s attention, and not always in a good way. With President Trump’s election, an increasing number of people became aware of so-called alternative-truth movements. Many of these right-leaning organizations rally fiercely against vaccination, particularly government-imposed protocols.

On the surface, that doesn’t help Novavax (NASDAQ:NVAX), which specializes in the stuff. Nor does the fact that NVAX is one of the riskiest penny stocks to buy. Since Feb. 27, shares have plummeted nearly 71%. Even more concerning is the reason why NVAX fell.

In a clinical trial, the company’s NanoFlu treatment failed to beat placebo. In other words, positive thinking yielded roughly the same efficacy in preventing influenza than the vaccine.

Given that NVAX is a fundamentally poor organization, I’m not surprised that shares fell. However, keep in mind that most Americans support vaccination. Therefore, the broader financial incentive to stay the course until efficacy improves is incredibly high.

With my Dividend Hunter service, I provide a list of high-yield investments that I have deeply researched, and my analysis shows provide an attractive combination of current yield and dividend stability.

As a high-yield stock expert, I often get asked questions about other stocks or investments that are not on my recommendations list. Sometimes a question will show me a new, attractive income investment. Others are learning opportunities on what not to do when picking high-yield investments.

One investment category that generates a lot of questions is closed-end funds (CEFs).

A closed-end fund is an investment pool with shares that trade on the stock exchange. Investors are drawn to CEFs because many have double digit yields and most paid monthly dividends.

Unfortunately, with most closed-end funds there are usually more negatives than positives when evaluating one for investment potential. Here are a few of the problems you could see.

Opaque communications from management on how a CEF is managed. There are not a lot of reporting requirements and any information you find on a fund’s portfolio may be months old. I sometimes refer to the CEF universe as the swamp of managed investment products.

CEF shares can trade at a discount or premium to the net asset value (NAV). Fund sponsors do not redeem shares, so the only place to buy or sell is on the stock exchange. If you buy a fund trading at a premium, you are paying more than a dollar for a dollar’s worth of assets. Not a good deal. A CEF trading at a deep discount can be a danger sign that the management has been making some bad investments.

Dividends classified as return-of-capital (ROC) are a big danger sign. Technically, return-of-capital are dividends/distributions that are not from earned income such as dividends or interest. While there are types and circumstances where ROC is not destructive to a fund’s NAV, unless you know for sure where the ROC comes from, it’s a danger signal to a CEF’s long term viability.

To recap, the problem with many CEFs is that they are hard to analyze with several factors that on their face are dangerous to your long term investment success. With over 700 publicly traded CEF’s, it is too much work to dig a handful of good ones out of the majority of swamp muck. Here are three high yield CEF’s to dump now if you own them.

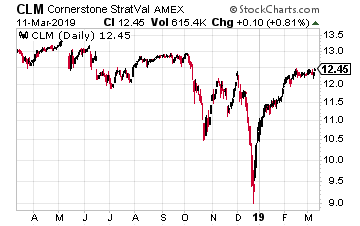

Cornerstone Strategic Value (NYSE: CLM) is a CEF with $570 million in assets that owns a portfolio of global equity (stocks) securities.

CLM currently yields over 20%. There are two big danger signals for this fund. First, it is trading at an 11% premium to NAV. The high yield has caused unwitting investors to bid up the share price to 11% above what they would be worth if the fund is liquidated.

The current monthly dividend is 20.53 cents per share. Out of that just one cent is earned income and two cents are capital gains. The remaining 19.3 cents per share is classified as ROC. Historically, most of the dividends have been ROC, which is reflected in the steadily deteriorating NAV.

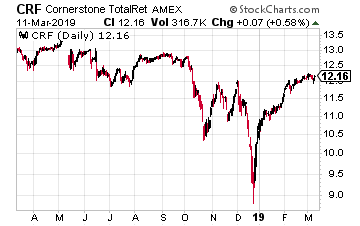

As typically happens, Cornerstone Total Return (NYSE: CRF) is a similar fund managed by the same advisory firm with the same problems.

This fund is trading at a 12.5% premium to NAV. That is very rich pricing in the CEF world.

The distributions breakdown also is like CLM. The current 19.85 cents month dividend has been paid for since the start of 2019. Each month 18.7 cents of the payout have been classified as return of capital.

Ignore the 20% yield and avoid or sell CRF.

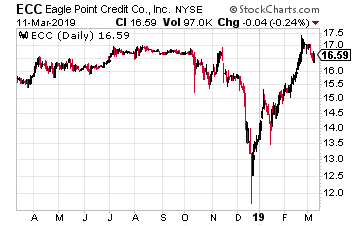

Eagle Point Credit Company LLC (NYSE: ECC)yields 14%. Due to recent large drops in the NAV, the shares trade at an eye-watering 23% premium to NAV.

Out of the 20 cents per share monthly dividends, 7 cents have recently been classified as ROC. Put another way, ECC is earning just 65% of the dividend it’s paying to shareholders.

Here’s the scariest part, the fund’s investment strategy: We seek to achieve our investment objectives by investing primarily in equity and junior debt tranches of CLOs. In plain English, they own the junkiest of the junk in the high-yield debt world.

Cloud stocks are divided into three categories: the cloud owners, the cloud arms merchants, and the cloud users.

The five Cloud Czars — Microsoft (NASDAQ:MSFT), Apple (NASDAQ:AAPL), Alphabet (NASDAQ:GOOG, NASDAQ:GOOGL), Amazon.Com (NASDAQ:AMZN) and Facebook(NASDAQ:FB) — all built clouds with cash flow from existing businesses. Apple and Facebook still run this way.

Clouds are built on open source software and commodity hardware. They’re meant to give their biggest benefits to users. Companies built using the cloud can become huge, like Netflix(NASDAQ:NFLX), Intuit (NASDAQ:INTU), Adobe (NASDAQ:ADBE) and Salesforce.com(NASDAQ:CRM).

Then there are the cloud arms merchants, companies whose main business is providing hardware and services to cloud owners. These include Nvidia (NASDAQ:NVDA), Intel(NASDAQ:INTC), Cisco Systems (NASDAQ:CSCO) and Dell Technologies (NASDAQ:DELL).

Analysts have lately become enamored of cloud arms merchants as large enterprises build their own data centers on the cloud model, creating the “hybrid” cloud. That’s the first place to seek cloud growth today.

Here’s how to get your share.

Microsoft (MSFT): The Unpunished Czar

Source: Shutterstock

Elizabeth Warren says she wants to break up the Cloud Czars, saying that they’re too powerful.

Why not break up Microsoft, especially since it’s now the most valuable company on the board, a market cap of over $900 billion, supporting 2018 revenues of $110 billion — nearly one-third of which it turned into operating income?

Maybe it’s because Microsoft pays its taxes, including almost $20 billion worth last year. But it’s also because Microsoft has already been visited by the antitrust police, 20 years ago. It paid dearly, losing its monopolies in PC operating systems and applications and then drifting for over a decade, held down by lawyers and fear.

Satya Nadella relaunched Microsoft as a cloud player in 2014, though Microsoft’s Azure cloud isn’t a monopoly. Nothing Microsoft does is a monopoly any more. Sony (NYSE:SNE) bests it in gaming and its Edge browser and Bing search engine are considered also-rans.

But Microsoft is competitive in every cloud niche, it has a dividend yielding 1.6%, its trailing price-to-earnings ratio sits at under 30 and its public profile is low enough to stay well away from regulators. It is once-burned, twice-shy — a sadder but wiser cloud company.

International Business Machines (IBM): Big Blue Lays it All on Red

Source: Shutterstock

International Business Machines (NYSE:IBM) has bet its future on buying Red Hat(NYSE:RHT) for $34 billion and making itself into a private cloud play.

Since the deal was announced in October, IBM shares are up 25%, well over the 16% gain of the Nasdaq. The shares are still cheap, sporting a P/E ratio of under 15 with a $1.57-per-share dividend paying a yield of 4.5%. Its market cap is just 1.5 times its sales, also cheap for a technology stock.

IBM was late to the cloud party because its older businesses did not need the cloud to operate. Mainframes were sort of clouds before clouds existed, and IBM has monopolized that business for decades. But clouds are slowly sinking that business, and IBM was run out of its old niches in PCs and minicomputers by Chinese competition, eventually selling most of its hardware units to Lenovo (OTCMKTS:LNVGY).

Instead, IBM sank its cash flow into the dividend. It bought a small cloud player called Softlayer, but wasn’t big enough to compete in public cloud. The idea behind the Red Hat deal, as the press release on it stated, was to transform IBM into a “hybrid cloud” provider.

The strategy is simple to describe. Red Hat software, including its Linux operating system and OpenShift (which lets companies put their own software into clouds as self-contained “containers”), will be offered by both Red Hat and IBM’s existing programmers. Enterprises can replace their aging data centers with small clouds, then quickly scale customer services compatible with those internal systems on public clouds.

If the strategy works, the value of IBM stock could easily double from here within a year, as it becomes a premier cloud merchant. But there is a lot of competition. It’s your cheapest speculation in the cloud.

Palo Alto Networks (PANW): Securing the Cloud

Palo Alto Networks (NYSE:PANW) has gone from zero to $22.5 billion in market cap since 2005 on the back of cloud security.

Originally a “next-generation firewall” company, providing security products to keep bad guys out of data centers, Palo Alto has spent over $1 billion on acquisitions in the last two years. Most recently it bought Demisto, an Israeli security company, for $560 million. Demisto is in the business of “orchestrating” or automatically organizing a company’s security efforts using machine learning.

All this has given Palo Alto a cloud-like valuation. That $22.8 billion market cap supports just $2.2 billion in fiscal 2018 revenue. It should grow to $2.5 billion in fiscal 2019, which ends in July. Fast growth means all that money goes back into the business. There are no profits. But operating cash flow has grown consistently and will blow past $1 billion this year.

Palo Alto’s move to cloud is transforming the revenue mix into monthly subscriptions instead of one-time payments, making it a favorite among analysts.

The company is in a key niche, security, and leading with today’s key customers, those with clouds.

ServiceNow (NOW): Automating Workflows in the Cloud

ServiceNow (NYSE:NOW) may be the biggest software company you’ve never heard of, thanks to the cloud.

ServiceNow is in the business of automating workflows. Its cloud-based platform organizes the movement of information among employees and customers. It started within computer departments in 2004, and has since expanded into serving entire enterprises, both internally and externally. The concept is that “work is the killer app,” and its latest update, dubbed Madrid, applies this to the mobile world as well as the desktop.

Shares rose 43% over the last year, despite the tech wreck. More important, they’re up almost 300% over the last five years. The $43.8 billion market cap is held up by $2.6 billion in 2018 revenue, up from $1.9 billion a year earlier. That’s growth people will pay for, even absent profits, and the company came close to break-even last year, losing just $26 million.

That computer workflow management piece of the company includes cloud management, making it a key competitor in the hybrid cloud world. It works with Microsoft but also Amazon’s AWS and VMware (NASDAQ:VMW).

ServiceNow has 37 analysts following it now, 28 of whom give it buy ratings . It’s expected to finally become profitable in 2019, to the tune of $3.10 per share.

VMWare (VMW): Essential Infrastructure

Source: Shutterstock

In addition to commodity hardware, two key technologies were required to make the cloud work.

First comes virtualization, a virtual operating system that runs on top of applications and lets them all run regardless of the operating system they’re written for. Then comes distributed computing, in which jobs can run on part of one computer, on several, or on thousands at once.

So before there could be clouds, there was VMware, serving up virtualization. In the last decade it was the more-profitable spin-off of EMC, and 80%-owned by that company, which makes large data storage systems. Today EMC and VMWare are part of Dell Technologies but its tracking stock still trades, and since its new parent went public at the end of 2018 it’s up 33%.

VMWare is a prize for analysts, investors and Michael Dell, who paid $67 billion for EMC (and its 80% stake in VMware) in 2015, because it is a lean, mean profit machine. Revenues have gone from $6 billion in fiscal 2017 to $8 billion in 2018 and to $9 billion for the 2019 fiscal year, ending Feb. 1, with net income rising to $2.4 billion last year. That means VMWare trading at “just” 8.5 times sales, which is considered affordable for the growth.

For the world of hybrid cloud, VMWare now offers its own operating system, Cloud Foundation,which runs on EMC hardware . This lets companies easily connect their existing VMWare data centers to public clouds like Amazon’s. It has also signed a partnership with Microsoft to converge their previously competitive hypervisors , the software that makes virtualization possible, bringing some of its customers to the Microsoft cloud.