The MoneyShow folks have now been asking to come back for five years. Each year it is a great time, and I love to get in front of the investing public.

As the spring show is held in Las Vegas, I thought it would be appropriate to cover some gaming related income stocks.

When it comes to the choice between being a tenant or a landlord, I like being on the landlord side, collecting a rent check every month.

At the end of the day (quarter and year) that is what being an investor in real estate investment trusts (REITs) means. Becoming a commercial property landlord through REIT ownership lets you become a first dollar investor in a wide range business types and industries.

The companies that lease from a REIT have a first dollar commitment to pay those rent checks. Yet often, a REIT will be able to participate in any positive business results produced by the tenant companies.

Gaming companies are a tough group of stocks to own. Profits swing wildly based on economic conditions and the tremendous competition in the areas that allow casino type gaming. Also, most of the gaming companies carry a large amount of debt. It costs a lot of money to build casinos!

It was the debt loads that pushed several publicly traded gaming companies to start to spin-off properties into REIT holding companies. The sponsored REITs gave the gaming companies a way to monetize assets and pay down debt. The gaming REITs are growth focused through the acquisition of additional properties to help support the growth of the sponsor gaming companies.

These three come to mind for your investment consideration.

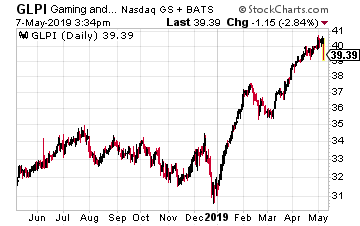

Gaming and Leisure Properties (GLPI) was the first gaming focused REIT when it was spun-out in 2013 by Penn National Gaming.

At that time the new REIT received 21 casino and racetrack properties. The company now owns 44 properties that are leased to and operated by Penn National Gaming, Casino Queen, Eldorado Resorts and Boyd Gaming.

In 2018 the company acquired five casinos from Tropicana Entertainment as the real estate part of the takeover of Tropicana by Eldorado Resorts. Of the three REITs here, GLPI is the most independent, with the ability to put together property and lease deals with a range of gaming companies. The REIT has an $8.7 billion market cap.

The dividend has grown by 5.6% per year over the past three years, and the GLPI shares yield 6.7%.

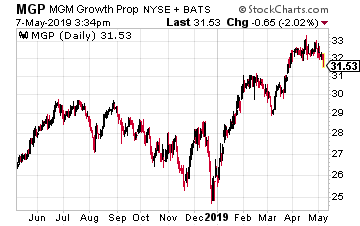

MGM Growth Properties LLC (MGP) was spun out in 2016 by MGM Resorts International. The initial REIT portfolio consisted of 10 MGM run properties, including seven on the Las Vegas strip. MGP now owns 14 properties all leased to MGM.

MGM Growth Properties has a triple-net master lease agreement with MGM Resorts which means all the REIT properties are on a single lease and the gaming company cannot single out one to close or not pay rent.

EBITDA from MGM coverage of the master lease payment is 6.2 times. The lease as a built in 1.8% rent escalator and MGP will also share profit growth at the casinos.

The MGP dividend has grown by 30% since the IPO and the shares yield 5.5%. MGP has a $9.2 billion market cap.

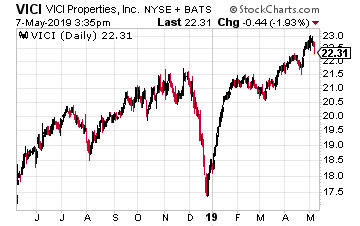

In October 2017 VICI Properties Inc. (VICI) was spun-off by Caesars Entertainment as part of the casino company’s bankruptcy reorganization.

Initially VICI owned 19 Caesars managed properties and that number has grown to 23. VICI has a triple-net master lease arrangement. The REIT has call options or right of first offering on six additional Caesar properties with another seven targeted for likely acquisition. VICI has a lot of growth potential.

VICI’s current market cap is $9.4 billion. Only four full quarter dividends have been paid.

There has been one dividend increase of 9.5%. Current yield is 5.0%.

Get your hands on my most comprehensive, step-by-step dividend plan yet. In just a few minutes, you will have a 36-month road map that could generate $4,804 (or more!) per month for life. It's the perfect supplement to Social Security and works even if the stock market tanks. Over 6,500 retirement investors have already followed the recommendations I've laid out.

Did the latest tariff tiff set the stage for the next pullback in stocks? Will this bull market actually die of old age?

The macro picture is dicey and stock valuations are pricey, but we must stay invested. The stock market goes up about two-thirds of the time. Permabears miss out on compounding and it’s not as easy to be a part-time bear as it sounds.

To illustrate this let’s consider a study by Hulbert Financial. The firm looked at the best “peak market timers”–the gurus who correctly forecasted the bursting of the Internet bubble in March 2000 and the Great Recession in October 2007.

These were the clairvoyant advisors who had their clients out of stocks and mostly in cash when the S&P 500 was about to be chopped in half. Surely their clients did great over the long haul, given their capital was largely intact at the market bottoms, right?

Wrong. None of these advisors turned in top performances. The reason? While they were good at timing tops, they were terrible at timing bottoms! The bearish advisors didn’t get their clients back into stocks anywhere near the bottom. They had their capital intact, but they didn’t deploy it–and they largely missed out on the epic bull markets that followed these crashes.

Think about the advisors and investors who sold in late December when the “bear market” became official. They moved to cash at the worst possible moment and have been on the sidelines waiting for a low risk “retest” of the lows. Mr. Market loves to confuse the most amount of people, and he really outdid himself this time!

Barely a Bear Market…

… And Right Back to a Bull!

Now we can be smart about staying in the market. While bull markets may not die of old age per se, this one is ten years old. They don’t run forever, so we should focus on pullback-proof names. Here are five rules to follow for 15% per year returns regardless of what the broader market does.

Recession-Proof Rule #1: Trust Your Dividends

Secure dividend yields are truly the “rubber duckies” of the investing world. Mr. Market can push them underwater for a period of time, but eventually, they rocket back up to the surface.

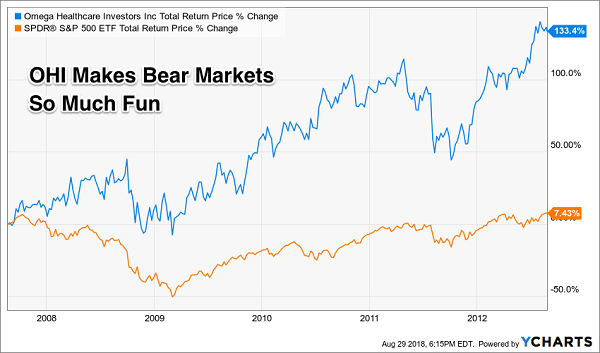

Let’s consider Contrarian Income Report favorite Omega Healthcare Investors (OHI), a big paying landlord in the skilled nursing space. It’s rewarded CIR subscribers with steady 8.1% returns per year, mostly from well-funded quarterly payouts. Anytime OHI rallies I get questions about whether we should book profits. Well, we rarely want to sell a great dividend stock like this–even when our crystal ball forecasts impending doom.

We’ll rewind 11 years to the top of the last extended bull market. If you were savvy enough to time the top in 2007, you would still have been doing yourself a disservice by selling your OHI shares (not least, how would know when to have “gotten back in?”)!

This Dividend Payer Barely Went Below the Water

Five years later, as the S&P 500 barely recovered its crash losses, OHI investors had enjoyed 133% returns (including steady, fat payouts throughout). And while the presence of a dividend does not guarantee protection from losses, examples like this one show that payout-focused investors have a serious edge in the markets because:

Buying stocks for their dividends alone makes day-to-day price action irrelevant.

Of course, you know this already! And you’re probably already wondering how we turn OHI’s 8% returns into 15% per year, so let’s get into rule number two.

Recession-Proof Rule #2: Buy Fast Growing Dividends

Dividends are magnets that pull their share prices along with them. If you’re looking for the stock market’s tail that wags the dog, pay attention to the payouts attached to a given share price.

Regardless of what the stock market does during any given trading session (or month, or whatever), share prices eventually follow their dividends higher. For example, let’s consider Texas Instruments (TXN), which has increased its payout (orange line below) by an amazing 600% over the last decade. Its stock price (blue line) was pulled higher by its dividend:

TXN’s Dividend Magnet

My Hidden Yields subscribers have made 55% in two years from TXN. Two generous dividend raises have provided much of this fuel. And the kicker? We bought when shares were “due” to pop because they had fallen behind their dividend curve.

Recession-Proof Rule #3: Find the Lagging Stock Price

The best time to buy a stock like TXN is nearly anytime. But we can “cherry pick” our entries (and put option sales) by focusing on times when TXN’s price falls behind its payout curve.

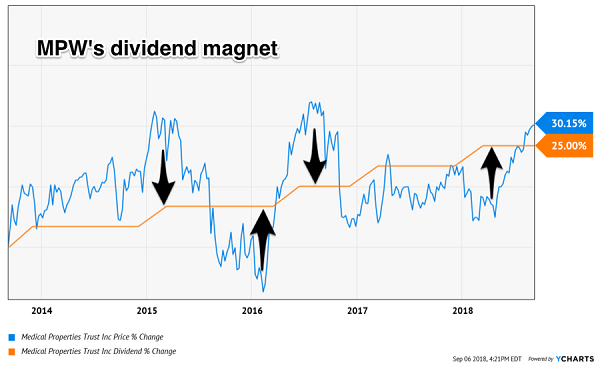

Regular readers will remember Medical Properties Trust (MPW), a hospital landlord we bought and later sold for 105% total returns. MPW’s dividend magnet was part of our secret, and the fact that we bought when the price was lagging dividend growth and sold after it had overtaken it. The “up” arrows below show good times to be a buyer, while the “down” arrows indicate times to hold or sell:

The Cues from a Dividend Magnet

Recession-Proof Rule #4: Buybacks Are a Nice Bonus

Share repurchases can provide fuel for dividend growth. When a firm buys back stock, it saves cash on dividends because it doesn’t have to “dish out” for those retired shares.

Buybacks today are the gifts that keep on giving tomorrow. By reducing the share count, they make every “per share” metric of profit and cash flow look better. Plus, they make it easier to grow the dividends because there are fewer shares to pay them to!

Buybacks work best when the stock itself is cheap. After all, the price you pay for something always matters. Smart management teams take advantage of depressed stock prices to provide their investors with a nice bonus.

Recession-Proof Rule #5: Low Payout Ratios: Where the Party’s At

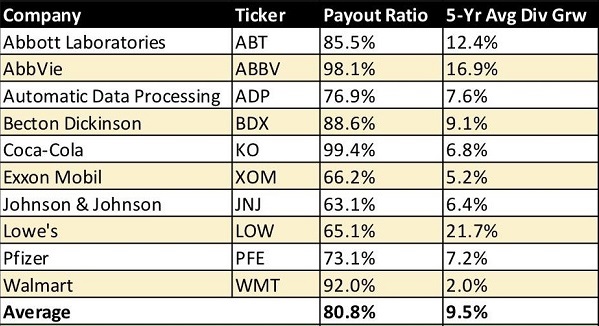

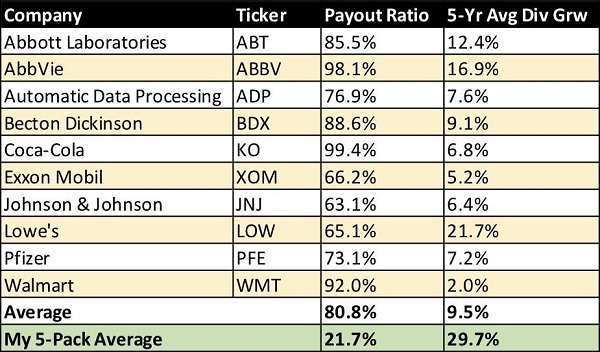

Some dividend-income investors think they are following this strategy by purchasing dividend aristocrats, or stocks that have increased their payouts every year for 25 straight years:

“Brett, I don’t own the S&P 500 index for income. I choose the best companies in the index, the ones whose dividends have gone up and up. The dividend aristocrats.”

Problem is, many of these monarchs have their best years behind them. Check out these payout ratios, or the percentage of profits that these aristocrats are paying out as dividends:

Sky High Payout Ratios

The 9.5% average dividend growth rate above is nice but it’s not sustainable. These firms are already paying 80% of their profits as payouts, when anything more than 50% can spell trouble! This means their upside potential for the next five years is likely limited.

So, let’s look past these paupers for lesser-known bargains that are primed to double their dividends and prices over the next five years. Some will double within three!

How is this possible? These five stocks are only paying 20% of their earnings as dividends, which means they could multiply their payouts by 2X, 3X or even 4X today and still have room to grow without risk of a dividend cut.

They won’t do it overnight, however. These firms will bump their dividends by 15%, 20% and even 25% or more per year. Which means their stock prices will eventually follow, and investors who buy today will double their money with these safe dividends.

7 Dividend Stocks That’ll Double Your Money Every Few Years

Since inception, our Hidden Yields portfolio has exceeded our lofty 15% benchmark, returning 16.4% per year. This means our inaugural subscribers are well on their way to doubling their money with safe dividend stocks. With patience and persistence, you too can enjoy the same types of returns by following our dividend double strategy.

Today, I want to share seven of my recession-proof “Hidden Yield Stocks” with you.

My research indicates each of these investments could easily pay you 15% per year. That’s enough to double your money in under 5 years. Imagine, turning a retirement ‘pot’ of $250,000 into $500,000… or… $500,000 into $1,000,000… and on it goes.

Imagine no more fear of your savings running dry… no more worrying about wild market swings or crashes… no more risky-bets on penny-stocks or cryptos… no more penny-pinching in your golden years.

So, if you’re not quite as wealthy as you hoped you’d be… if you wish you had more money in your retirement account… and… if you’re looking for safe, secure growth over the next 5, 10, 15, even 20 years—as well as predictable income—this could be the most important investment advice you ever read.

Editor's Note: The stock market is way up – and that’s terrible news for us dividend investors. Yields haven’t been this low in decades! But there are still plenty of great opportunities to secure meaningful income if you know where to look. Brett Owens' latest report reveals how you can easily (and safely) rake in 8%+ dividends and never worry about drawing down your capital again. Click here for full details!

I’ve uncovered two high-yield closed-end funds (CEFs) that are perfect for this “earnings down, stocks up” market.

I’m going to show you both of these bargain-priced, cash-spinning plays—one of which yields an incredible 9.2%, five times more than the typical S&P 500 stock—shortly.

First, we need to talk about where stocks stand now. Because you’re probably wondering how the market can keep ticking up when first-quarter earnings are actually down from a year ago.

You’re right to be concerned, because it makes zero sense—on the surface. But dig deeper and you’ll see that this is a good news story, and a perfect opportunity for contrarians like us to grab big gains (and dividends).

Let’s get into it.

When a Loss Is a Gain

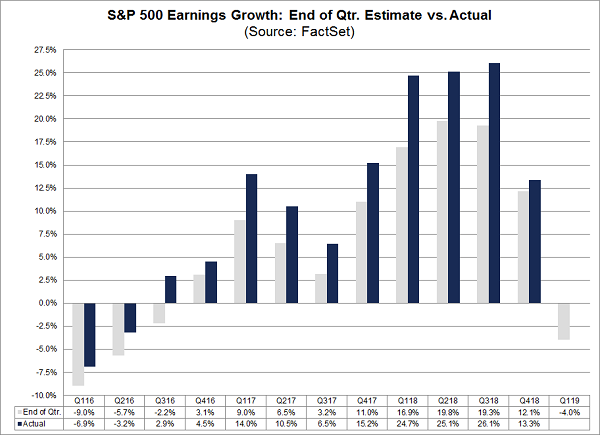

With earnings season half over, profits have fallen 2.3% year over year. That sounds bad, but it’s actually better than the 4% drop analysts predicted before the season started.

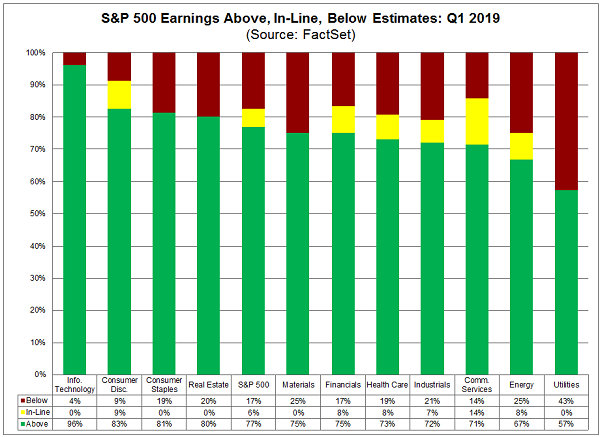

The reason? Surprises. A total of 77% of companies are reporting earnings above estimates, thanks to better-than-expected 5.1% sales growth. Sales are the lifeblood of profits, so this makes it easier to beat profit expectations.

Those earnings beats are also evenly distributed across sectors, with over half of companies in all sectors showing better-than-expected results:

Beating Expectations Across the Board

Again, the common theme is that sales are growing across sectors: people are buying more stuff, and that’s helping earnings across the market.

But Why Are Earnings Down?

That brings us to the question of why earnings are down at all. If things are so good, why aren’t profits up? There are two answers: the first is that year-ago profits were so strong that they’re tough to build on.

A Big Hill to Climb

In the first quarter of 2018, earnings jumped 24.7% and stayed at that level for the next two quarters. As you can see above, such growth is unusual—and a tough act to follow!

That’s why analysts were modest in their earnings estimates for this quarter. But now earnings are coming close to the mark set a year ago, showing that the economy is still strong, and companies are still in great shape.

The second reason for the lack of earnings growth is that the first quarter tends to be weak. The post-holiday period is no time to load up the credit card, so Q1 expectations are often modest.

In fact, any growth in the first quarter following growth a year earlier is exceptional. That makes 2018’s 24.7% profit jump unusual, since it followed 14% growth a year previous. To expect three straight years of first-quarter growth would be very optimistic indeed.

The takeaway? The economy isn’t getting overheated but isn’t cooling down, either.

Next Leg of Growth About to Kick Off

With first-quarter economic growth ticking along at 3.2%, according to the Commerce Department, it’s no surprise that companies are seeing sales jump 5.1%. That growth also positions them up to expand their operations and set themselves up for higher sales and profits in the future. And companies are doing just that: they spent more on buying, building and upgrading assets in 2018, and that trend is continuing.

But the market hasn’t priced this growth in—not even close. And this is where our opportunity shows up.

A Buying Opportunity in Disguise

Stocks are up less than 10% since before earnings saw three consecutive quarters of 25% growth, which is below the average return stocks deliver in the long term. That means it isn’t too late to get into the market, even if the rebound we’ve seen this year makes it feel that way.

And you’ll be able to buy in even cheaper with the two CEFs I mentioned off the top. Let’s move on to those now.

Two CEFs to Ride the Market Higher (and bag yields up to 9.2%)

Our first high-yield play is the Boulder Growth & Income Fund (BIF), which focuses on bargain-priced large caps. This fund holds much of its portfolio in Warren Buffett’s Berkshire Hathaway (BRK.A, BRK.B), along with other top-quality stocks like JPMorgan (JPM) and American Express (AXP).

So why buy BIF instead of cutting out the middleman and just buying its collection of well-known names on your own?

Simple: as I write, BIF trades at a massive 16.8% discount to net asset value (or NAV, another name for the value of the stocks the fund owns). That means you’re getting these top-quality large caps for 87 cents on the dollar! And while BIF’s 3.7% dividend yield is low for a CEF, it’s still double what the typical S&P 500 name pays.

Finally, you can juice your income stream more with the 9.2%-yielding Cohen & Steers Income Builder (INB), holder of some of the best companies in America, with Microsoft (MSFT), Visa (V), Philip Morris (PM) and Amazon (AMZN) standing out among its top holdings.

Here’s the key point to remember about INB: its NAV has returned 14.2% this year (including dividends and price gains). But investors are giving it very little credit, because the fund still trades at 10.8% below its NAV! That’s one of the widest gaps in the CEF space, and it points to more upside as that discount narrows.

NEW: The 4 CEFs You Must Buy Now (8.7% Dividends, Double-Digit Gains Ahead)

As I just showed you, stocks are still a great buy as investors (slowly) discover there’s still time to get in on this “goldilocks” economy.

And as you saw with BIF and INB, you’ll do better (and grab far higher dividends) if you make your move through a CEF. The best of these funds give you the best of all worlds: huge dividends, market outperformance and bargain prices—often all in one buy.

I know that sounds crazy: a fund that’s still cheap even after a monster gain. But it’s a familiar story with CEFs, thanks to their weird discounts to NAV.

Consider one of my four favorite CEFs now, which I’ll show you when you click right here. This fund focuses on high-yield utilities and real estate stocks, yields an impressive 7.9% and has thoroughly bested the market this year, with a 23% return:

A Market-Beating Fund

Here’s the surprising part: despite that gain, this fund is still cheap! It trades at a 13% discount to NAV, which gives us two advantages you’ll never get buying stocks individually or through an ETF. That’s why I’m forecasting 20% price upside in the next 12 months, to go with that rich 7.9% payout.

Michael Foster has just uncovered 4 funds that tick off ALL his boxes for the perfect investment: a 7.4% average payout, steady dividend growth and 20%+ price upside. — but that won’t last long! Grab a piece of the action now, before the market comes to its senses. CLICK HERE and he’ll tell you all about his top 4 high-yield picks.

By now, it’s fairly common knowledge among financial market observers that the 2019 IPO stocks will be big, headlined by a slew of tech unicorns that are finally ready to hit the public markets. Names in this group include Uber, which will likely debut at a $100 billion-plus valuation, and Airbnb, which will likely command a $30 billion-plus valuation. There’s also Palantir with a rumored $30 billion-plus valuation, Slack with a $10 billion-plus valuation, and WeWork with a potential $40 billion-plus valuation.

But, the first big player in this group to IPO in 2019 was Lyft (NYSE:LYFT), and the results were far from spectacular. Lyft popped on its first day of trading, but it has been nothing but down and out since then. As of this writing, LYFT stock actually trades more than 15% below its IPO price.

The ostensible failure of the Lyft IPO has some fearful about upcoming IPOs. But, the failure of the Lyft IPO is getting too much press, and investors shouldn’t read much into it. While the Lyft IPO did ostensibly fail, there have been a ton of other IPO stocks in late 2018 and early 2019 which have been huge successes, and which imply that future IPOs in 2019 will do just fine.

Which IPO stocks fall into this category of big winners so far on Wall Street? Let’s take a deeper look at 6 red hot IPO stocks that all investors should be watching.

Zoom (ZM)

Gain From IPO Price: 100%

At the top of this list is a freshly public tech company which Wall Street has fallen in love with in just a few days.

Zoom (NYSE:ZM) is a video conferencing company which priced its IPO at $36 per share, opened up 80% above that IPO price, and has continued to soar ever since en route to a 100%-plus gain from that $36 IPO price. Why the huge demand for Zoom stock? The hyper-growth tech company checks off every box growth investors are looking for. It’s growing revenues at 100%-plus rate, with a small revenue base in a secular growth and very large video conferencing market. Gross margins are sky high around 80%, while opex rates are surprisingly low for a small company, and Zoom is actually profitable already.

All in all, you have a hyper-growth video conferencing company that’s already profitable. That has investors salivating.

But, the valuation on ZM stock is pretty rich here and now, and the stock has come very far, very fast. As such, caution is warranted here, especially considering that the video conferencing market isn’t light on competitors.

Red Hot IPO Stocks: Pinterest (PINS)

Source: Shutterstock

Gain From IPO Price: 40%

Second up is a social media company with a lot reach and a ton of potential to monetize that wide reach.

Unlike digital ad IPO stocks before it, the Pinterest (NYSE:PINS) IPO has been a huge success thus far. After pricing the IPO at $19 per share, PINS stock has rallied in a big way ever since, and is now up 40% from that IPO price. The rationale behind the rally is simple. This is a company which has a ton of users (265 million monthly active users), and is monetizing those users at a low rate (ARPU of just over a $1 last quarter), so the runway for robust revenue growth through ARPU expansion is promising. Plus, margins are healthy, the international user base is growing rapidly and the valuation is reasonable.

All together, then, PINS stock has been a big winner because the fundamentals are healthy, the upside potential is good, and the valuation is cheap. So long as those three things remain true, PINS stock will stay in its IPO honeymoon phase.

Red Hot IPO Stocks: YETI (YETI)

Source: Yeti

Gain From IPO Price: 100%

Third we have an outdoors consumer product company that didn’t have a huge IPO pop, but has been a steady winner in its short life as public company.

Meet YETI (NYSE:YETI). YETI is an outdoors consumer products brand that specializes in coolers and drinkware. YETI went public at $18 per share in late 2018 without much fanfare. The stock actually traded down on its first day on Wall Street. But, YETI stock has doubled ever since as the company has reported back-to-back strong earnings reports which ultimately underscore that this company has healthy growth drivers, in a healthy market, with a healthy margin profile.

In other words, YETI is a healthy company. Under $20, YETI stock wasn’t priced for healthy. That’s why the stock rallied. Above $30, the IPO stock is priced for healthy. But, not entirely. As such, so long as the numbers remain good (which they should for the foreseeable future), then YETI stock should remain on an uptrend until valuation becomes an issue. That won’t happen until around $40.

IPO Stocks: Jumia (JUMIA)

Source: Shutterstock

Gain From IPO Price: 140%

Maybe the most interesting stock on this list is Jumia (NYSE:JMIA).

Long story short, Jumia is Africa’s e-commerce juggernaut, and that means this company is oozing with long-term growth potential. Africa is the last great frontier of the tech revolution. Internet penetration rates on every continent outside of Africa measure north of 50%, and ex Asia, they measure north of 60%. But, in Africa, the internet penetration rate is roughly 36%. That number won’t stay low forever. Over the next several years, thanks to a combination of factors such as urbanization, expansion of the middle class, and heavy technology infrastructure investments, Africa’s internet penetration rate is expected to surge higher, and that surge will spark enormous growth in Africa’s internet sectors.

One of those sectors is e-commerce. Less than 1% of all retail sales in Africa were conducted online in 2018. As internet penetration rates rise, online retail’s penetration will likewise rise, and that will create a huge growth opportunity for players in the market. The largest player in the African e-commerce market today? Jumia, which has 4 million active consumers and a gross merchandise value near $1 billion.

If Jumia can maintain its market leadership position as the African e-commerce market dramatically expands over the next decade, then JMIA stock is a multi-bagger in the making. But, there’s a lot of risks regarding execution and valuation, so this IPO stock isn’t for the faint of heart. Best way to look at Jumia? A high-risk, high-reward play on the potentially enormous African e-commerce market.

Tencent Music (TME)

Gain From IPO Price: 35%

One of the more interesting recent IPO stocks is the company which many people are calling the Spotify (NYSE:SPOT) of China.

Tencent Music (NYSE:TME) is the premiere music streaming platform in China. China is a huge market with a rapidly expanding digital economy. As such, the upside potential for Tencent Music to grow with the rapidly expanding Chinese digital economy is enormous. But, there are a few problems here. Namely, there’s a ton of competition, the company gets most of its revenue from virtual gifts, there’s only 25 million paying subs, and the valuation is huge.

Thus, TME stock is a high-risk, high-reward play on the music streaming market in China. If consumers in that market start paying up for music services, then TME stock will explode higher. If not, TME stock could be stuck in neutral for the foreseeable future.

Levi Strauss (LEVI)

Source: Shutterstock

Gain From IPO Price: 35%

Last (and maybe least) on this list is an older company which recently made its return to Wall Street.

Blue jeans giant Levi Strauss (NYSE:LEVI) returned to the public markets in late March. The IPO was a smashing success. The stock opened up more than 30% above its $17 IPO price. LEVI stock has since largely held onto those gains — but not added to them — as first quarter numbers were a mixed bag that implied positive but slowing growth going forward.

Ultimately, it’s tough to see the upside scenario in LEVI stock. The athleisure trend remains as hot as ever, and that trend continues to steal share from the jeans market. As such, Levi Strauss finds itself on the wrong side of the apparel tracks. To be sure, that doesn’t mean growth will flat-line. But, it will put a lid on growth, and a lid on growth will hurt LEVI stock, which currently trades at above what I peg as a reasonable 2019 price target for the stock.

As of this writing, Luke Lango was long LYFT, PINS, YETI, and SPOT, and may initiate a long position in JMIA within the next 72 hours.

Get your hands on my most comprehensive, step-by-step dividend plan yet. In just a few minutes, you will have a 36-month road map that could generate $4,804 (or more!) per month for life. It's the perfect supplement to Social Security and works even if the stock market tanks. Over 6,500 retirement investors have already followed the recommendations I've laid out.

Up until last February, the Cboe’s VIX (S&P 500 Volatility Index) was the only market volatility index which could be traded through derivative products. The index itself is not tradeable, but VIX futures, options on those futures, and VIX-related ETFs are all widely popular products. While the usage of these products varied based on the user, the one thing they have in common is using the VIX as the underlying instrument.

However, in February, the SPIKES index launched on the MIAX exchange – a collaboration between T3 Indexes and the MIAX itself. SPIKES is similar to the VIX in that it measures market volatility using options on the S&P 500. However, the VIX uses SPX options for pricing purposes (the S&P 500 index itself), while SPIKES relies on SPDR S&P 500 ETF(SPY) options for its calculations.

So how can SPIKES compete against the 500-pound VIX gorilla? In order to attract customers, SPIKES offers significantly lower fees than VIX. SPY also tends to be more liquid, with more active strikes than the SPX. This is particularly important in times of high volatility, where price accuracy can be an issue if liquidity dries up. (SPIKES also uses a proprietary price-dragging method to keep accurate prices in place if things get too crazy.)

In the coming months, MIAX will likely launch SPIKES futures to go along with the existing options market. The addition of futures should allow SPIKES to compete on an equal basis with the VIX. It also means SPIKES-based ETFs will be a possibility down the road.

But what about the performance? While the SPX and SPY are very similar instruments, they aren’t identical. In fact, the big difference comes from the SPY offering a quarterly dividend (which isn’t the case with SPX). So then, historically, how do the VIX and SPIKES compare?

A new white paper by Dr. Peter Carr delves into this issue. First off, Peter Carr is perhaps the most respected name in options and volatility research. He is to this field what Warren Buffett is to value investing.

Dr. Carr is chair of the Department of Finance and Risk Engineering at NYU. He was previously managing director of market modeling at Morgan Stanley. He’s also won just about every accolade available in the field of financial engineering and risk modeling. All that is to say, you can bet any paper by Peter Carr is going to be immediately taken as if written on stone tablets.

So what did Dr. Carr discover in his research?

First and foremost, in the period from 2005 to 2018, the difference between SPIKES and VIX was negligible on average. In other words, from a medium to long-term view, you could have used the two indexes nearly interchangeably.

In the short-term, there were some noticeable differences around SPY’s quarterly dividend, as you’d expect. Most of this different was due to what’s called the early exercise premium, a phenomenon exclusive to American-style (early exercisable options). In a nutshell, the ability for SPY options holders to exercise their options early (to collect a dividend once a quarter) can cause a higher level of volatility in the options around those periods.

There are few points to consider. The early exercise premium is influenced by both dividends and interest rates, although interest rate contributions to options pricing are usually minor. Furthermore, the impact of the early exercise premium is probably not very impactful to out-of-the-money options, from which both the VIX and SPIKES are largely priced.

Here’s the bottom line. If we assume constant interest rates and dividend yields the difference between SPIKES and VIX due to the early exercise premium is generally trivial. When there is uncertainty surrounding these variables (generally in the short-term) there can be an additional volatility premium in SPIKES.

To put it simply, there may be a short-term period where SPIKES is higher than VIX when dividends are a factor. This is due to the extra volatility of the early exercise premium. How big that gap can get is something that will certainly be researched by interested parties. In the meantime, savvy investors may be able to take advantage of this gap to make money when it occurs.Read this if you’ve ever lost money trading options

Does everything seem to go wrong right after you place an options trade?

You watch the stock and everything is going right.

Then you open the trade… and within an hour, you’ve lost money.

It’s not your fault. You just simply weren’t given the “behind the scenes” knowledge every options professional knows.

If you knew how they worked, in 2018 – when the markets lost 6% – you could’ve booked gains of:

127% in 23 days on GLD

148% in 28 days on SQ

229% in 36 days on SMH

213% in 13 days on Netflix

79% in 22 days on SPY

63% in 24 days on SPY

117% in 21 days on SPY

96% in 36 days on QQQ

114% in 42 days on MRVL

Just like I did.

The road to success for your first big, triple-digit options win is simple.

This is the year of 5G. The possibilities opened up by 5G’s significantly faster data transfer opens up a brave new world. It will enable the newest technologies from autonomous vehicles to virtual reality gaming to advanced robotics to the Internet of Things.

Don’t believe me? Then listen to Paul Lee, the head of telecoms, media and technology research at Deloitte. Lee recently said: “The last 10 years of smartphones have been about invigorating the consumer experience and entertainment. Now it is about the digital transformation of enterprise.” He predicted that 5G-enabled smart devices will soon displace laptops.

Of course, 5G is about a lot more than smartphones. The debate going on about national security and who provides the next generation telecommunications equipment tells you that. Since it has been in the news headlines so much, I want to give you a quick primer on what the heck 5G is all about.

What Is 5G?

5G is the fifth generation of wireless network technology. Browsing web pages on mobile phones caught on with the advent of 3G, while data transmission became faster and more reliable with 4G.

With speeds 100 times faster than current networks, 5G will enable transmission of huge amounts of data with little time delay. 5G can also support more connected devices than current technology—as many as one million devices per square kilometer!

With the new 5G technology, more devices than ever before can be connected in real time, bringing the concept of the “Internet of Things” closer to reality. The CEO of Vodaphone, Nick Read, says that 5G will be around 10 times more efficient than 4G.

A report from the research firm IHS Markit forecasts that 5G will enable $12.3 trillion of global economic output by 2035, fostering new sectors such as smart cities, smart agriculture and autonomous vehicles.

However, it will take time for the faster 5G networks to become seamless enough to support self-driving cars, so consumers are likely to benefit first from faster data speeds in select areas. For example, you will be able to livestream videos in crowded areas without frustration.

But costs will be a major headache. The European Commission estimates the cost of rolling out 5G and full fiber infrastructure across the continent to be in the range of 500 billion euros. This means the ‘pick and shovel’ companies that supply the equipment and components for 5G are going to make a lot of money.

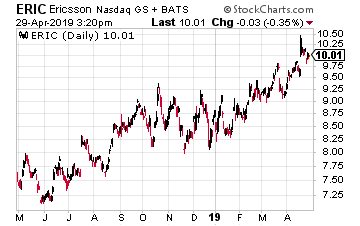

That leads me to my top 5G pick, which is Ericsson (ERIC). The Swedish telecom player is making a big bet on 5G, and that bet seems to be paying off. Ericsson expects there to be 3.5 billion Internet of Things connections running over 5G by 2023, with 20% of global mobile data carried by 5G in 2023, and one billion consumers on the faster networks, representing 12% of projected mobile subscriptions.

Ericsson is right to put such an emphasis on 5G, but the company has struggled since 2016 with quarter after quarter of losses. It had been caught out with a high cost base just as global telecom providers cut spending drastically ahead of the rollout of 5G networks.

So now, the company’s recovery plans are closely tied to an uptick in spending by network operators on 5G networks along with restructuring, cost cutting and new partnerships such as that with Japan’s Fujitsu to develop 5G base stations.

A restructuring, I might add, that is still ongoing. In January, it said it would cost about $850 million to restructure a unit that provides digital services to telecom operators.

However, the restructuring is already taking hold and shows signs of momentum. Ericsson’s gross margin in Q4 of 2018 rose to 36.3%, a nice uptick. And here’s what caught my eye: in 2018, Ericsson returned to full-year top-line growth for the first time since 2013!

Ericsson Beats Earnings…Again

Then on Wednesday, April 17, Ericsson did it again. The company reported adjusted earnings of nine cents per share. That nearly doubled Wall Street’s estimates of five cents per share. That’s their fifth earnings beat in a row. Consider that about 40% of the world’s mobile phone traffic is currently carried through Ericsson networks.

Wall Street is taking notice. The day after Ericsson’s earnings report, the shares jumped 7.3% to touch a four-year high. Digging through the numbers, the details look very encouraging. For the quarter, Ericsson’s gross margin improved to 38.4%. Sales rose 7% to $5.33 billion driven by strength in North America. Bear in mind that Ericsson reported a loss for the same quarter one year ago.

Ericsson says spending on 5G is exceeding its expectations both in volume and speed of the uptake. It gained market share in North America even though it was raising prices.

In fact, it says it currently lacks enough personnel in North America to keep up with the demand from the likes of Verizon and AT&T. That’s a good problem to have and one that the company can fix quickly to take advantage of the fact that it is likely that 5G will have a longer spending period than prior 3G and 4G rollouts.

In addition, 5G should create more opportunities for the company’s software and services within Internet of Things device networks. Clearly, Ericsson is benefiting from a major turnaround as it helps usher in the Age of 5G.Buffett just went all-in on THIS new asset. Will you?

Buffett could see this new asset run 2,524% before the end of 2019. And he’s not the only one… Mark Cuban says “it’s the most exciting thing I’ve ever seen.” Mark Zuckerberg threw down $19 billion to get a piece… Bill Gates wagered $26 billion trying to control it…

What is it?

It’s not gold, crypto or any mainstream investment. But these mega-billionaires have bet the farm it’s about to be the most valuable asset on Earth. Wall Street and the financial media have no clue what’s about to happen… And if you act fast, you could earn as much as 2,524% before the year is up.

Buffett just went all-in on THIS new asset. Will you? Buffett could see this new asset run 2,524% in 2018. And he's not the only one... Mark Cuban says "it's the most exciting thing I've ever seen." Mark Zuckerberg threw down $19 billion to get a piece... Bill Gates wagered $26 billion trying to control it... What is it? It's not gold, crypto or any mainstream investment. But these mega-billionaires have bet the farm it's about to be the most valuable asset on Earth. Wall Street and the financial media have no clue what's about to happen...And if you act fast, you could earn as much as 2,524% before the year is up. Click here to find out what it is.

We retirees and soon-to-be retirees have a dilemma. The traditional pension is just about gone. Social Security won’t support the lifestyle most of us want. We are left to our own devices.

But even if we do build up a fat balance in a 401(k) or other company retirement plan, how do we make it last? Especially when the bank pays “zero point nothing.” Today, you can’t find anything that pays significant “interest.”

This is becoming a crisis in the US. We are told that stocks provide the best returns over the long term, but retirees need income now. Most retirement investors prefer dividend income to long-term gains, but yields haven’t been this low in decades! The S&P 500 pays a measly 2% or so today. If you have a million-dollar portfolio, that’s a lousy $20,000 per year in income, or $385 a week. That’s no retirement.

Now some dividend-income investors protest, “But I don’t own the S&P 500 index for income. I choose the best companies in the index, the ones whose dividends have gone up and up. The dividend aristocrats.” But are they true monarchs or mere pretenders to the throne.

The problem with growing your dividends for a minimum of 25 consecutive years is that’s a lot of time for your own profit growth to slow down. That means many of your dividend increases are cutting even further into your earnings. You don’t want to break the bank, so your hikes shrink over time–a couple percent here, a couple percent there, just to keep your Aristocrat lapel pin.

I’ll let you in on a secret: Sometimes, the best place to make your dividend-growth play is on the ground floor, in companies that have really only begun to scratch the surface. In fact, two of the picks I’m about to show you have been paying dividends for less than five years.

Let me show you the difference between some of the largest blue-chip Dividend Aristocrats and my plucky group of five turbo-charged dividend growers:

These Blue Chips Are Crawling to the Finish Line

The 9.5% growth rate above is nice but it’s not sustainable. These firms are already paying 80% of their profits as payouts! This stat is great for the last five years, but awful for the next five–and that’s what we care about.

So let’s look past these paupers for lesser-known bargains that are primed to double their over the next five years. Some will double within three!

How is this possible? These five stocks are only paying 20% of their earnings as dividends, which means they could multiply their payouts by 2X, 3X or even 4X today.

They won’t do it overnight however. These firms will bump their dividends by 15%, 20% and even 25% or more per year. Which means their stock prices will probably follow, and investors who buy today will double their money with these safe dividends.

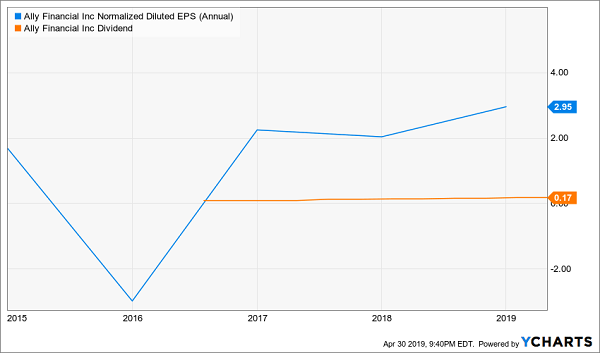

Ally Financial (ALLY) as we currently know it has only been around since 2010, but the company has roots going all the way back to 1919 as General Motors Acceptance Corporation (GMAC) – the financing-providing arm of automaker General Motors (GM).

The company still has extensive automotive operations, providing financing for more than 4 million customers across 18,000 dealerships. But Ally also offers online banking, vehicle insurance and credit cards, among other products. It also re-entered the mortgage business in 2016 via its direct-to-consumer Ally Home, and in mid-April, it announced a partnership with Better.com to launch a digital mortgage platform.

Ally Financial’s top and bottom lines have ebbed and flowed over the past few years, but things are starting to perk up, and the pros are starting to take notice. The company beat Q1 earnings estimates in April, prompting a couple “Buy” calls. That included one from Oppenheimer analyst Dominick Gabriele, who wrote, “We see a long runway for earnings given continued strong management execution that some investors are only just beginning to appreciate.”

The company started dividends relatively recently, at 8 cents per share in 2016, and has already more than doubled it at its current 17 cents per share. That history–as well as optimistic profit-growth estimates of 10% annually through 2024–would almost seem to guarantee breakneck dividend growth going forward … right?

In early April, Ally announced a massive $1.25 billion repurchase program for 2019 that was far more than what most analysts expected. When you factor in that, the financial stock’s total “cash return” payout ratio is actually a hair above 100%. So yes, Ally does indeed have the means to make major dividend increases going forward … but only if it’s less aggressive about buybacks.

Valvoline (VVV) is a global juggernaut in its relatively niche area of the market. It offers automotive services and supplies lubricants to more than 140 countries, including 1,170 quick-lube stores in the U.S. It has roots going all the way back to 1866, though the company is a relative newbie on the public markets, executing its IPO in 2016.

The dividend is just as fresh, so its five-year growth is extrapolated out from its original 4.9-cent dividend to today’s 10.6-cent payout.

That’s a lightning-quick doubler!

The stock hasn’t been nearly so spry, however. VVV has bounced back and forth since it came public, and shares sit about 16% lower than their IPO price. Particularly troubling was its fiscal first-quarter report in February. Not only did Valvoline miss the mark on both earnings and revenues, but it announced a restructuring to “reduce costs, simplify processes and ensure that the organization’s structure and resource allocation are focused on key growth initiatives.” The initiative should save the company about $40 million to $50 million pretax each year starting with fiscal 2020.

Valvoline surely has the room to keep the pedal down on its dividend, though the company’s focus now appears to be reinvigorating growth. I would wait to see green shoots from its restructuring efforts before even considering a move into VVV.

Income investors should know that earnings payout ratios for dividends don’t always tell the whole story. Net income can be manipulated, after all. So I also like to look at free cash flow payout ratios. (You can calculate free cash flow simply by subtracting capital expenditures from operating cash flow.)

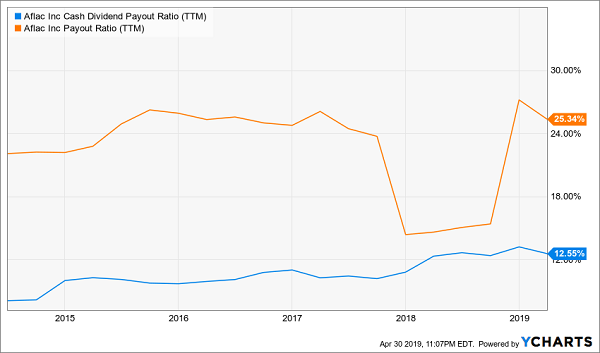

Aflac (AFL) is, and has long been, a reliable dividend stock on that and several other fronts.

Aflac, which we all know from its ubiquitous duck commercials, is a leading provider of supplemental insurance – things such as dental and vision plans, short-term disability insurance and life insurance – serving more than 50 million customers.

The company has been slowly but steadily growing for years, though 2017 earnings spiked thanks to a considerable tax benefit. Analysts see more of the same going forward, with low-single-digit profit-growth estimates for the next couple of years. That’s fine. Aflac is an insurer, not a chipmaker.

That reliable growth has translated into a higher dividend each and every year since 2000. And given payout levels like these, shareholders can count on Aflac continuing to plump up the dividend.

Chemours (CC) is one of the byproducts of years of wheeling and dealing by DuPont … which, following a merger with Dow is now DowDuPont (DWDP) … which recently spun off Dow Inc. (DOW).

That confusing bit of history aside, Chemours–the “performance chemicals” division of DuPont that was spun off in 2015–is pretty straightforward, and really fascinating. For instance, it’s the world’s largest producer of high-quality titanium dioxide, which goes into coatings in automobiles, marine craft and airplanes. It also makes fluor0products such as Teflon, and chemical solutions that cover a wide range of applications, such as acids for semiconductor manufacturing and sodium cyanide production for gold and silver miners.

Chemours’ “performance” isn’t limited to its products. While CC shares had a nasty start in their first year of trading, they’ve exploded by more than 525% off their July 2016 lows, versus 48% returns for the S&P 500 in that time.

The dividend didn’t start to get off the ground until a couple years after the spinoff. What started as a mere 3-cent payout finally took off with a massive jump to 17 cents in 2018, then to 25 cents that same year, where the payout stands today.

Pricing weakness in some of its products have hobbled its performance, and the stock, over the past year, and analysts see earnings weakening this year before returning to 2018 levels in 2020. That’s a lot of sideways movement, which means Chemours would have to inflate its payout ratio to keep up with its red-hot income growth. But considering it distributes just 15% of its net income as dividends … that’s no biggie.

Baconator slinger Wendy’s (WEN) has really come into its own over the past three years.

The House That Dave Thomas Built was only the eighth-biggest fast food chain as of QSR magazine’s August roundup–behind both McDonald’s (MCD) and Restaurant Brands International’s (QSR) Burger King. But it has the happiest shareholders.

While its actual financial results have been up and down for years, they’re generally trending upward, and analysts expect that to continue this year and next. One of the catalysts for 2019 is a less value-focused environment in the fast-food arena, which is tailor-made for Wendy’s more premium positioning compared to the likes of McDonald’s and Yum! Brands’ (YUM) Taco Bell.

Wendy’s also has managed to double its dividend since 2014 to its current dime per share without stretching the purse strings. The company has a lean sub-20% payout ratio and could double the payout again overnight without dropping a bead of sweat.

I obviously don’t expect that, but I do expect the next few Februaries – when Wendy’s announces its payout increases – to be full of fireworks.

7 More Dividend Stocks That’ll Double Your Money Every Few Years

Since inception, my Hidden Yields portfolio has returned 16.3% per year. This means our inaugural subscribers are well on their way to doubling their money with safe dividend stocks! With patience and persistence, you can enjoy the same types of returns by following our dividend double strategy.

Today, I want to share seven of my recession-proof ‘Hidden Yield Stocks’ with you.

My research indicates each of these investments could easily pay you 15% per year. That’s enough to double your money in under 5 years. Imagine, turning a retirement ‘pot’ of $250,000 into $500,000… or… $500,000 into $1,000,000… and on it goes.

Imagine no more fear of your savings running dry… no more worrying about wild market swings or crashes… no more risky-bets on penny-stocks or cryptos… no more penny-pinching in your golden years.

So, if you’re not quite as wealthy as you hoped you’d be… if you wish you had more money in your retirement account… and… if you’re looking for safe, secure growth over the next 5, 10, 15, even 20 years—as well as predictable income—this could be the most important investment advice you ever read.

Editor's Note: The stock market is way up – and that’s terrible news for us dividend investors. Yields haven’t been this low in decades! But there are still plenty of great opportunities to secure meaningful income if you know where to look. Brett Owens' latest report reveals how you can easily (and safely) rake in 8%+ dividends and never worry about drawing down your capital again. Click here for full details!

Something very weird is happening with high-yield closed-end funds (CEFs): many of them are ridiculously cheap, despite soaring double-digits this year.

(And when I say these are “high-yield” funds, I mean it: nearly all of the five funds I’ll show you shortly yield 7% and up!)

I know that sounds impossible: a big run-up and a bargain in one buy?

It’s true—and it’s the beauty of CEFs: unlike with mutual funds and ETFs, CEFs’ market prices can swing massively from the net asset value (NAV) of their portfolios. That’s because investors often ignore CEFs and fail to bid them up to what they’d be worth if they were liquidated tomorrow.

Situations like that are common in CEF land, and sometimes a fund is badly managed enough to deserve a huge discount. But today, many well-run, top-performing CEFs—including the five below—are priced like laggards. That nicely sets us up to grab more upside to go with their outsized dividends.

Dividend and Income Fund (DNI) Discount to NAV: 24% Year-to-Date Total Price Return: 25.8% Dividend Yield: 6.9%

The S&P 500’s 17.7% return this year is good, but DNI’s 25.8% is better. And that’s an apples-to-apples comparison, by the way, because DNI has a mid-cap portfolio full of S&P 500 stocks like the Walt Disney Co. (DIS), Home Depot (HD) and Apple (AAPL). But DNI’s portfolio is more value-focused, which is why it’s crushing the index.

DNI doesn’t just offer outperformance, either: its near-7% dividend is also more than three times bigger than that of the benchmark SPDR S&P 500 ETF (SPY). In other words, DNI gives you $575 in monthly income per $100,000 invested, while SPY delivers a paltry $149.17.

New Germany Fund (GF) Discount to NAV: 12.3% Year-to-Date Total Price Return: 25.6% Dividend Yield: 1.2%

Germany is having a good year, but GF is having a better one. While the iShares MSCI Germany ETF (EWG) has gained 12.7% in 2019, GF, with its experienced management team, has posted a gain twice that big. This isn’t an anomaly; since its 1998 IPO, GF is up 3.6 times as much as EWG.

So why the big discount if GF is the best way to get in on Germany’s growth? It’s simple: dividends. Most CEF investors are income-crazy, and GF’s 1.2% yield doesn’t excite them. But that’s shortsighted, because GF often pays special dividends, like the 20% payout at the end of 2018. In fact, GF has been paying an annualized double-digit yield for nearly a decade.

Kayne Anderson Midstream Energy Fund (KMF) Discount to NAV: 12% Year-to-Date Total Price Return: 28.5% Dividend Yield: 7.6%

If you’re looking for oil and gas exposure, you’re best to go with an energy specialist like Kayne Anderson. The company’s energy CEFs tend to outperform their indexes over the long term, thanks to the Texas-based management team’s unique market access: KMF combines private-equity investments with well-known publicly traded energy firms like the Williams Companies (WMB),Enbridge Inc. (ENB) and Enterprise Products Partners LP (EPD).

It’s no surprise, then, that KMF’s 28.5% total return this year is way ahead of the 17.7% return of the benchmark Alerian MLP ETF (AMLP). And KMF continues to maintain a 7.6% dividend yield, giving you a nice income stream with your energy exposure.

Salient Midstream & MLP Fund (SMM) Discount to NAV: 15.1% Year-to-Date Total Price Return: 25.9% Dividend Yield: 7.7%

Similar to KMF, Salient’s SMM has crushed the market with its 25.9% return while also maintaining an impressive 7.7% payout. However, unlike Kayne Anderson, Salient focuses on publicly traded shares, which, at least in theory, gives it more liquidity in case of a sudden run on energy investments.

Here’s why this matters: if you want some energy exposure but you’re worried about a sudden shock to oil prices, you may have concerns about a fund that puts some of its assets in smaller investments, like KMF does. In theory, this higher liquidity could help increase SMM’s long-term return, even if oil and gas hit some bumps in the road.

Brookfield Global Listed Infrastructure Income Fund (INF) Discount to NAV: 14.4% Year-to-Date Total Price Return: 27% Dividend Yield: 8%

Brookfield has a long history of investing in infrastructure projects, meaning management has developed a keen eye for undervalued stocks in that sector.

That’s why INF’s 27% return trumps the 14% return you’d have gotten with the SPDR S&P Global Infrastructure ETF (GII) this year, although both funds focus on large-cap infrastructure stocks around the world.

Like the index fund, INF’s portfolio tends to have around half its assets abroad, although recently that’s been closer to a third due to the fund’s savvy bet on a stronger dollar. That’s a big reason why INF’s return has nearly doubled up that of the index, and this approach goes a long way toward easing any worry you may have about being exposed to the wrong currency at the wrong time.

Here’s a SAFE 9.8% Cash Dividend (with upside!) to Buy Now

I’ve uncovered 5 more CEFs boasting even bigger upside in the next 12 months, thanks to their yawning discounts to NAV.

Taken together, the 5 ironclad funds I’ll reveal right here boast an 8.3% average yield—so you’re bagging a cool $8,300 a year in dividends on a $100K nest egg! And one of these CEFs even pays out an incredible 9.8% dividend now.

In other words, if you were to cherry-pick that one fund, $9,800 would come straight back to you, in cash, every year on your $100K.

This cash-rich buy is a biotech fund that’s a perfect contrarian play right now, due to overblown headlines surrounding the healthcare business.

But we love overhyped news reports, because they give us the cheap entry points we need to grab top-notch funds like this cheap. Right now, for example, you can pick up this CEF at a fire-sale 8.4% discount to NAV, or just under 92 cents for every dollar of assets!

That’s totally out of whack when you consider that my pick has dominated in the last decade:

Another Cheap Outperformer

And remember that, thanks to that huge 9.8% dividend, almost all of this gain was in cash. No wonder this fund usually trades at a big premium to NAV—which is why we need to make our move now, before this bargain sale ends.

Michael Foster has just uncovered 4 funds that tick off ALL his boxes for the perfect investment: a 7.4% average payout, steady dividend growth and 20%+ price upside. — but that won’t last long! Grab a piece of the action now, before the market comes to its senses. CLICK HERE and he’ll tell you all about his top 4 high-yield picks.

Earnings season is fully upon us now and things are as expected … there are some big winners and some big losers. While growth should be solid this year, it’s not likely to set any records. That makes it important to find the opportunities in the market now, especially since there has been the big tech run-up in Q1. While some of these tech stocks are solid contenders, not all of them can be counted among the top stocks to consider now.

The big run in Q1 just got the market back to breakeven after the horror show in Q4, especially in December.

So now is the time to look for opportunities in select sectors where there should be better than average growth in the coming year. And within those sectors, there are some low-priced stocks with a lot of potential that are worth adding to your portfolio now.

The top stocks under $10 I feature here all have momentum in their favor — as measured by my Portfolio Grader — and their businesses are growing faster than their larger peers. These names also have an A-rating according to my system. Just make sure not to chase them too far from their current prices.

ICICI Bank Ltd ADR (IBN)

Source: Shutterstock

ICICI Bank Ltd ADR (NYSE:IBN) isn’t as much a play on the U.S. as it is the growth in India. It is only one of a handful of Indian stocks that trades in the U.S.

Remember, India’s GDP last year was 7% — 10% faster than China’s growth. And it is likely to continue posting numbers like that for years to come.

But like most emerging economies, it has its fits and starts. That’s why owning a solid bank is a good way to get some exposure without taking on too much risk. And that’s where IBN fits in.

IBN is one of only three privately held major Indian banks and it is growing like a tech company. What’s more, it’s also selling Prudential insurance in India through a majority-owned subsidiary ICICI Pru, a new product with huge potential. And insurance also has healthy margins.

With the U.S. and Chinese economies doing well, it’s a good signal that India will continue to prosper and develop. IBN stock is up more than 30% in the past year and has plenty of headroom left.

First BanCorp (FBP)

Source: Shutterstock

First BanCorp (NYSE:FBP) is a Puerto Rico-based bank that also has operations in the Caribbean and in the U.S. It’s on fire.

Given the massive devastation of the island from the recent hurricane, I mean that in a good way. FBP stock is up nearly 30% year-to-date and more than 50% in the past 12 months.

Much of this is due to the rebuilding efforts that are going on in the region now. It takes a while after a major natural disaster for funding to show up and start getting disbursed.

FBP is now in the middle of rebuilding the island and the various other islands where it has operations. And given its status of a territory of the U.S., native Puerto Ricans live in the U.S. and send money back to family there. This is also strengthening the economy of the island.

While fixing the island will happen over a long period of time, at some point it will end, but expanding new opportunities will present themselves and FBP will be on the front line. And it will have a strong balance sheet to help.

Infosys Ltd (INFY)

Source: Shutterstock

Infosys Ltd ADR (NYSE:INFY) is a global technology, outsourcing and consulting firm that offers an array of services to some of the largest businesses in the world. It’s headquartered in Bangalore, India and has been around for more than 35 years.

With a $46 billion market cap, this is an established company that continues to grow, taking advantage of expanding economies around the world. And where economies are tight, they also look to INFY to help grow their productivity by outsourcing operations that are being solved efficiently in companies’ current operations.

INFY has a respectable 2.9% dividend and is up 10% year-to-date and nearly 20% in the past year. Its last quarter’s earnings beat expectations by a comfortable margin but it warned that this year may not be as strong. But there are plenty of companies that have pointed this out; it’s not a shock. However, it has meant that the stock has lost some ground and is at a good price.

Telefonaktiebolaget LM Ericsson (ERIC)

Source: Shutterstock

Telefonaktiebolaget LM Ericsson(NASDAQ:ERIC) is in the 5G wars right now.

As a leading global telecom company, it is stuck between the leading 5G telecom player in the world — China’s Huawei — and the U.S. government. The U.S. is concerned that Huawei equipment may contain surveillance equipment to tap into telecommunications used over the network and has told allies that the U.S. will not allow aid money to be used to buy Huawei equipment or support a 5G network using its equipment.

And while that may seem like a great thing for ERIC — based in Sweden — the problem is, China isn’t interested in making it easy for ERIC to muscle in on its 5G dominance. The U.S. doesn’t have a native company that can scale up 5G, so there’s an uneasy stalemate among the players.

But regardless of how it shakes out, ERIC is still a major global player. And as networks upgrade and expand, ERIC will be a significant source of the work.

The stock is up 11% YTD and more than 30% in the past year. It may be a little bouncy for a while, but as long as the global economy keeps chugging along, ERIC will be in growth mode.

Cousins Properties (CUZ)

Source: Shutterstock

Cousins Properties Inc (NYSE:CUZ) is a commercial real estate investment trust (REIT) that has been around since 1958. Essentially, it owns and operates commercial buildings in some of the hottest regions of the Southwest, South and Mid Atlantic.

Having been launched and headquartered in Atlanta, Georgia, it is one city where CUZ has significant holdings. Atlanta is one of the fastest growing cities in the U.S. and that growth is continuing.

It also has properties in the tech mecca of Research Triangle in North Carolina as well as Austin, Texas. It also has properties in major markets in Florida and Arizona.

REITs are particularly hot right now for two reasons. First, low-interest rates and a steadily growing economy are helping make financing and new investments easier. Plus, it’s a good market to raise rents in.

Second is a tax advantage that was written into law in 2018 that allows new tax advantages for REITs and their investors.

Plus, the real estate market has been dormant for a while now, so this revival has been a long time coming.

Also, late last month, CUZ merged with Tier REIT (NYSE:TIER) adding another 50% to its market cap as well as a successful group of properties in many of the same markets.

Cleveland-Cliffs (CLF)

Source: Shutterstock

Cleveland-Cliffs Inc (NYSE:CLF) has been around for more than 170 years. It was around 15 years before the Civil War started. That is durability.

Part of the reason it has endured is the fact that it does one thing: It makes iron ore pellets from mines and factories in Michigan and Minnesota for the U.S. steel industry.

This year started strongly on two fronts. First, one of its main competitors, Brazil-based Vale SA (NYSE:VALE) had to cut production when a dam broke at a mining operation in Brazil causing an incredible amount of damage.

Second, the strength of the U.S. economy has meant more demand for steel.

This is why CLF is up 27% YTD and 34% in the past year. And even after this price run, CLF stock is still delivering a 2% dividend.

CLF is a small company — about a $2 billion market cap — but it is a focused company that has seen a lot more economic challenges than most other firms in its sector. It may not be flashy, but it’s hot now and will continue to provide for shareholders.

Vereit Inc (VER)

Source: Shutterstock

Vereit Inc (NYSE:VER) owns and manages single tenant commercial properties in the US.

That means it owns properties that one business occupies, which makes it much more manageable for the REIT. Plus many of its customers are national chains, so it is has a close relationship with major retailers and restaurants.

For example, its top five clients are Red Lobster, Walgreens (NASDAQ:WBA), Family Dollar, Dollar General (NYSE:DG) and FedEx (FDX). Its top 10 clients represent 27% of the company’s total income.

As the U.S. economy continues to expand and consumers continue to spend, this all bodes well for VER.

Up 16% YTD and delivering a whopping 6.7% dividend, this is a great REIT at a great price and at a great time.

Louis Navellier is a renowned growth investor. He is the editor of four investing newsletters: Growth Investor, Breakthrough Stocks, Accelerated Profits and Platinum Growth. His most popular service, Growth Investor, has a track record of beating the market 3:1 over the last 14 years. He uses a combination of quantitative and fundamental analysis to identify market-beating stocks. Mr. Navellier has made his proven formula accessible to investors via his free, online stock rating tool, PortfolioGrader.com. Louis Navellier may hold some of the aforementioned securities in one or more of his newsletters.

Get your hands on my most comprehensive, step-by-step dividend plan yet. In just a few minutes, you will have a 36-month road map that could generate $4,804 (or more!) per month for life. It's the perfect supplement to Social Security and works even if the stock market tanks. Over 6,500 retirement investors have already followed the recommendations I've laid out.