Most cryptocurrencies are decentralized, meaning they don’t have a corporate entity that one could invest in.

A typical cryptocurrency (what I like to call “crypto”) is, like bitcoin, governed by its users, miners and usually a nonprofit foundation.

So there’s no way to invest in bitcoin as a company. You can buy coins, but there is no stock or equity.

However, there is a dynamic and fast-growing community of private businesses being built around crypto today.

If crypto continues to take off, these companies could be the financial giants of the future.

I’ll tell you about a few of the crypto startups I’m watching, and why I’m excited about the increasing number of these companies using equity crowdfunding.

Bitwise

Bitwise aims to be the “Vanguard of cryptocurrency.” The fintech startup just revealed its first investment product, the HOLD 10 Private Index Fund. It’s a basket of the top 10 cryptocurrencies by market cap.

Co-founder Hunter Horsley told Coindesk…

We want to create a meaningful and secure way to own a portfolio of cryptocurrency. We feel that, today, it’s too hard and it’s too expensive.

The company plans to charge 2% per year, with no additional fees. That’s a bargain compared to most crypto hedge funds, which take at least 20% of profits, plus 2% annually.

Bitwise has attracted notable Silicon Valley investors, including AngelList co-founder Naval Ravikant.

For now, the HOLD 10 fund is only available for accredited investors. This is likely due to the fact that the SEC hasn’t approved any bitcoin ETFs yet, but I fully expect Bitwise to go after the broader market eventually.

Coinbase

Founded by Brian Armstrong in 2012, Coinbase has grown exponentially to become the world’s largest cryptocurrency exchange.

With 10.8 million users and 36 million wallets, Coinbase is a force in the crypto community.

Coinbase has processed more than $25 billion in transactions in 2017, according to a Fortune article published in August. It also offers crypto payment processing tools for roughly 40,000 merchant accounts.

The company just announced a $100 million round of funding at a $1.6 billion valuation. Investors in its latest round include top venture capital firms IVP, Greylock and Spark Capital.

This August fundraise made Coinbase the first crypto “unicorn” startup (one that has grown to a $1 billion-plus valuation). Its earliest investors include members of FundersClub, an online investment platform for accredited investors.

The company’s explosive growth has caused some growing pains, however, and Coinbase is struggling to keep up with customer service inquiries. U.S. laws dictate that it follow certain rules designed to prevent money laundering, and partly as a result, the company’s pipeline is clogged.

The good news is it appears to be putting the new round of capital to good use, having recently launched phone support for users. If it can overcome these issues, Coinbase is well-positioned to become a dominant financial institution in this new market.

Bittrex

Bittrex is a fast-growing and disruptive cryptocurrency exchange.

The biggest difference between Bittrex and Coinbase is the number of digital currencies they offer.

Coinbase offers three: bitcoin, Ethereum and Litecoin.

Bittrex allows users to trade 200 different cryptocurrencies, including all the top ones offered by Coinbase. The other 197 “altcoins” are what really set Bittrex apart.

Altcoins have exploded in popularity over the last year, as the price of Ethereum rose from less than a dollar in 2016 to $294 today, giving it a $27 billion market cap.

On Bittrex, users can search for the next big opportunity. Many of the coins on this exchange are tiny, with market caps in the low millions.

Bittrex also offers a flat trading fee of 0.25%, while the fees on Coinbase vary and tend to be higher.

The one drawback to using Bittrex is that you can’t buy coins directly with dollars or other fiat currency, as you can on Coinbase.

Still, it’s a great example of a disruptive startup shaking up the incumbents of a new industry. By offering users a much wider selection of alternative cryptocurrencies, Bittrex is gaining ground on crypto powerhouse Coinbase.

Bittrex’s founding team has deep experience in web security, having worked at Amazon, Blackberry and Microsoft.

With a talented team, great tech and impressive growth, Bittrex is definitely a crypto startup to watch.

Crowded Startup Pipeline

We’re just beginning to see how transformative and disruptive the crypto market can be.

An entire ecosystem of new financial technology is being created. This sort of thing doesn’t happen very often, to say the least.

Many crypto startups will launch over the next few years, and some are likely to become the fintech titans of tomorrow.

We’ve already started to see a few high-quality crypto deals utilize equity crowdfunding.

Just last month we recommended one to members of our research service, First Stage Investor. It’s called Balance, and it’s building a user-friendly financial dashboard app that tracks not only your traditional financial transactions, but your crypto ones too. Soon users will be able to buy and sell cryptocurrencies directly through its app, and many more features are in the works.

The deal was quite popular, and it filled up after the company raised the maximum allowable $1.17 million. With a focus on simplicity and ease of use, Balance is well-positioned to help bring crypto to the mainstream.

Balance is among the first crypto- and blockchain-related startups to utilize equity crowdfunding, and it certainly won’t be the last.

I can’t reveal any details yet, but developments are coming that will merge the equity crowdfunding and crypto worlds in ways I couldn’t have even imagined a year ago.

It’s going to be a very exciting time.

Good investing,

Adam Sharp

Co-Founder, Early Investing

Can a $10 Bill Really Fund Your Retirement? The digital currency markets are delivering profits unlike anything we’ve ever seen. 23 recently doubled in a single week. And some like DubaiCoin have jumped as much as 8,200X in value in 18 months. It’ unprecedented... but you won’t receive any of the rewards unless you put a little money in the game. Find out how $10 could make you rich HERE.

Source:

Early Investing

That is simply due to the exorbitant cost of building a new plant to make semiconductors, which are called foundries or fabs. Even back in 2010, a new foundry set Taiwan Semiconductor (NYSE: TSM) back $9.7 billion. Today, that cost is likely doubled.

That is simply due to the exorbitant cost of building a new plant to make semiconductors, which are called foundries or fabs. Even back in 2010, a new foundry set Taiwan Semiconductor (NYSE: TSM) back $9.7 billion. Today, that cost is likely doubled.

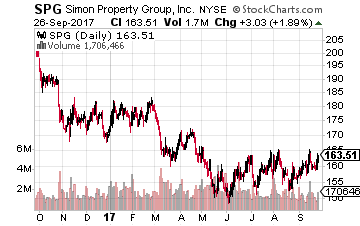

With a $50 billion market cap, Simon Property Group Inc (NYSE: SPG) is the largest publicly traded REIT. Simon owns and operates premium shopping and outlet malls. If a company needs to have retail stores, it wants to locate them in Simon run malls. The SPG dividend has been increased 15 times in the last five years, with the payout growing by 80%. This is a very successful mall operator. This stock is on sale, with a current share price down 30% from the July 2016 peak. Yield is 4.6%.

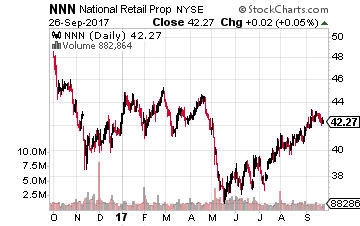

With a $50 billion market cap, Simon Property Group Inc (NYSE: SPG) is the largest publicly traded REIT. Simon owns and operates premium shopping and outlet malls. If a company needs to have retail stores, it wants to locate them in Simon run malls. The SPG dividend has been increased 15 times in the last five years, with the payout growing by 80%. This is a very successful mall operator. This stock is on sale, with a current share price down 30% from the July 2016 peak. Yield is 4.6%. properties. The company owns over 2,500 stores, leased to 400 tenants operating in 40 different retail categories. Most of these categories are businesses which cannot be replaced by ecommerce alternatives. Business such as restaurants, health clubs, fuel and convenience stores and auto parts stores. National Retail Properties has increased its dividend for 28 Sconsecutive years. Dividend growth will be in a 3% to 5% annual range. NNN shares are down 19% since the 2016 high and yield 4.5%.

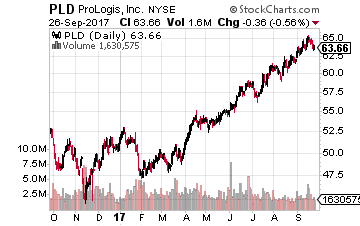

properties. The company owns over 2,500 stores, leased to 400 tenants operating in 40 different retail categories. Most of these categories are businesses which cannot be replaced by ecommerce alternatives. Business such as restaurants, health clubs, fuel and convenience stores and auto parts stores. National Retail Properties has increased its dividend for 28 Sconsecutive years. Dividend growth will be in a 3% to 5% annual range. NNN shares are down 19% since the 2016 high and yield 4.5%. Prologis, Inc. (NYSE: PLD), with a $33 billion market cap, is a global logistics giant. The company owns or partially owns properties and development projects across 676 million square feet in 20 countries spanning four continents. Industrial/warehouse REITs are one of the hot REIT sectors. These companies can easily fill new projects and realize nice rental rate growth on existing properties. Prologis has increased its dividend by 50% over the last four years. The stock yields 3.4%.

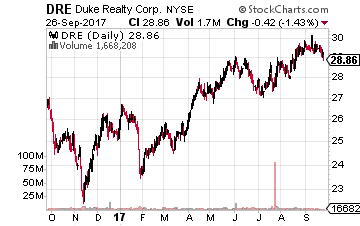

Prologis, Inc. (NYSE: PLD), with a $33 billion market cap, is a global logistics giant. The company owns or partially owns properties and development projects across 676 million square feet in 20 countries spanning four continents. Industrial/warehouse REITs are one of the hot REIT sectors. These companies can easily fill new projects and realize nice rental rate growth on existing properties. Prologis has increased its dividend by 50% over the last four years. The stock yields 3.4%. pure play, domestic only industrial REIT. The company owns 475 facilities in Tier 1 markets. Duke is highly focused on serving e-commerce sales and fulfillment. The company notes that projected e-commerce growth through 2020 will require almost 300 million square feet of additional industrial space. Amazon.com is Duke Realty’s largest tenant. The DRE dividends should grow by about 6% per year. The stock yields 2.6%.

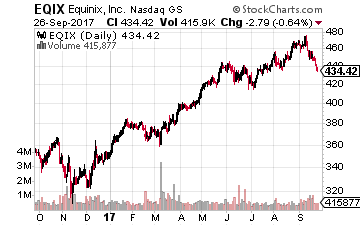

pure play, domestic only industrial REIT. The company owns 475 facilities in Tier 1 markets. Duke is highly focused on serving e-commerce sales and fulfillment. The company notes that projected e-commerce growth through 2020 will require almost 300 million square feet of additional industrial space. Amazon.com is Duke Realty’s largest tenant. The DRE dividends should grow by about 6% per year. The stock yields 2.6%. Equinix, Inc. (NASDAQ: EQIX) is a 19-year old S&P 500 company which became a REIT in 2015. Equinix owns and operates the largest global network of data centers, which focuses on connectivity and interconnection. The company’s revenues and EBITDA are growing at a high teens annual rate. AFFO (adjusted funds from operations) per share is increasing by over 20% per year. The dividend was increased by 14% this year. Equinix also has a history of paying large stock + cash special dividends. EQIX yields 1.8%.

Equinix, Inc. (NASDAQ: EQIX) is a 19-year old S&P 500 company which became a REIT in 2015. Equinix owns and operates the largest global network of data centers, which focuses on connectivity and interconnection. The company’s revenues and EBITDA are growing at a high teens annual rate. AFFO (adjusted funds from operations) per share is increasing by over 20% per year. The dividend was increased by 14% this year. Equinix also has a history of paying large stock + cash special dividends. EQIX yields 1.8%. connectivity, primarily in eight major US markets. Here are the company’s amazing annual compound growth rates for the last six years.

connectivity, primarily in eight major US markets. Here are the company’s amazing annual compound growth rates for the last six years.

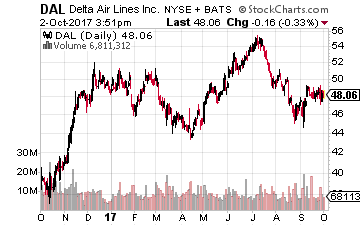

Delta operates a fleet of over 700 aircraft and serves more than 170 million customers annually. Its revenues fell 3% in 2016 to $39.64 billion, giving its efforts to reduce its debt levels more urgency. Its management is also maintaining capacity discipline while simultaneously trying to modernize its fleet and expand its operations.

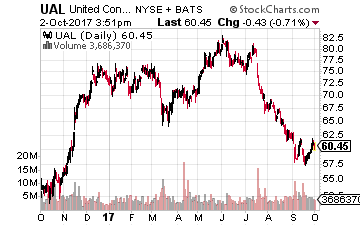

Delta operates a fleet of over 700 aircraft and serves more than 170 million customers annually. Its revenues fell 3% in 2016 to $39.64 billion, giving its efforts to reduce its debt levels more urgency. Its management is also maintaining capacity discipline while simultaneously trying to modernize its fleet and expand its operations. United is the world’s largest airline, operating about 5,000 flights a day. However, the merger of UAL with Continental has left the merged company with a significant debt load. Its significant exposure to Houston also means it was greatly affected by Hurricane Harvey.

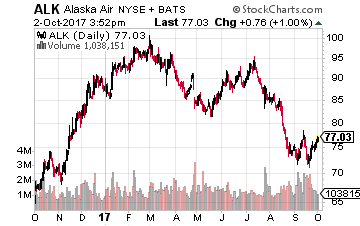

United is the world’s largest airline, operating about 5,000 flights a day. However, the merger of UAL with Continental has left the merged company with a significant debt load. Its significant exposure to Houston also means it was greatly affected by Hurricane Harvey. Alaska Air operations cover the western U.S., Canada and Mexico as well as, of course, Alaska. I like the purchase of Virgin America, despite the rise in the amount of debt it now has. The company’s August traffic report showed that its load factor (percentage of seats filled by passengers) increased to 86.2% from 85.8% in the year ago period as traffic growth exceeded capacity expansion.

Alaska Air operations cover the western U.S., Canada and Mexico as well as, of course, Alaska. I like the purchase of Virgin America, despite the rise in the amount of debt it now has. The company’s August traffic report showed that its load factor (percentage of seats filled by passengers) increased to 86.2% from 85.8% in the year ago period as traffic growth exceeded capacity expansion.