If you’re like most folks, you probably think it’s tough for any fund to beat the S&P 500, especially in a year when the index jumped some 15%.

But you’d be wrong.

Truth is a lot of funds are doing better, with over 660 beating the S&P 500. And the top-performers share 3 common themes that could tell us a lot about which sectors are poised to take off next year.

Let’s dig in. Along the way, we’ll hone in on the 33 funds that are cashing in as these breakthrough trends head higher.

Trend No. 1: Skyrocketing Faith in Technology (11 Funds)

Markets have always believed that technology will improve the global economy. But every once in a while investors get too excited and see value in all the wrong places.

A classic example? The boom and bust of dot-com IPOs in the late 1990s. The market was right about the Internet changing the world, but it failed to pick the winners and losers.

So we shouldn’t treat the market’s latest bets as gospel. But the trend is clear: bitcoin, hardware and biotech are the real game changers now.

That’s why the Bitcoin Investment Trust (GBTC) is by far the biggest winner of 2017, with 477.5% gains so far. That’s way ahead of the other winning tech ETFs, though many have clocked impressive returns, too:

If you missed the bitcoin wave but still put your money in tech ETFs, you did very well as long as you chose the ARK Innovation ETF (ARKK), ARK Web x.0 ETF (ARKW), Global X Lithium & Battery Tech ETF (LIT), ARK Genomic Revolution Multi-Sector ETF (ARKG), Global X Robotics & Artificial Intelligence ETF (BOTZ), Virtus LifeScience Biotech Clinical Trials ETF (BBC), MG Video Game Tech ETF (GAMR), ARK Industrial Innovation ETF (ARKQ), Global X Social Media ETF (SOCL) and SPDR S&P Biotech ETF (XBI).

These funds are all over the place, betting on social media, biotech, battery technology, genomic research and video games. What they have in common is a belief that many technological revolutions are starting now—and there are identifiable companies that will profit.

Trend No. 2: Greenback Slump Spurs Emerging Markets (19 Funds)

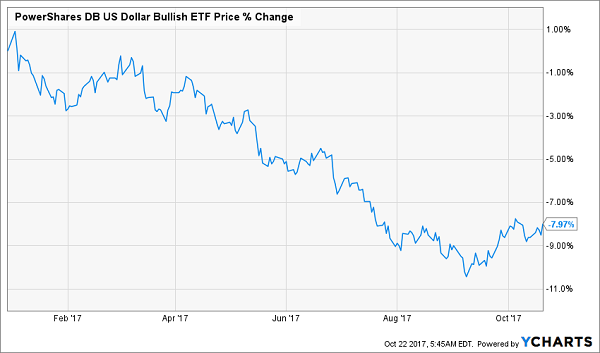

It’s no secret that the US dollar has had better times. After a bull run through 2015 and 2016, the greenback has given up a lot of those gains to emerging market currencies, the euro and even the post-Brexit pound. If you bet on a stronger dollar through, say, the PowerShares DB US Dollar Bullish ETF (UUP), you probably aren’t happy:

Dollar Droops, UUP Dives

On Wall Street, a lot of analysts and traders made the mistake of betting on a dollar recovery in the middle of the summer. Boy, were they wrong! And while that’s not good for Americans looking to vacation abroad, it’s been great in other parts of the globe, particularly emerging markets and Asia.

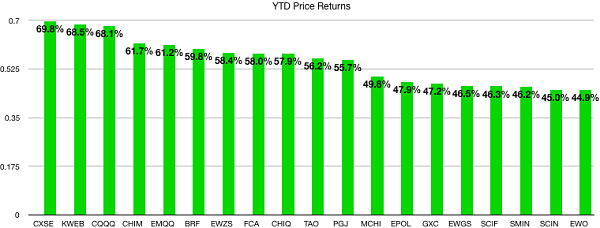

So great, in fact, that many China- and emerging market–focused ETFs are up over 50% and a few are close to that mark. This emerging-market strength has also benefited Germany, whose euro currency is getting stronger; the country also sells lots of technology to China.

A ton of winners here, so let’s list them:

Columbia India Small Cap ETF (SCIN)

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ)

First Trust China AlphaDEX ETF (FCA)

Global X China Consumer ETF (CHIQ)

Global X China Materials ETF (CHIM)

Guggenheim China Real Estate ETF (TAO)

Guggenheim China Technology ETF (CQQQ)

iShares MSCI Austria Capped ETF (EWO)

iShares MSCI Brazil Small-Cap ETF (EWZS)

iShares MSCI China ETF (MCHI)

iShares MSCI Germany Small-Cap ETF (EWGS)

iShares MSCI India Small-Cap ETF (SMIN)

iShares MSCI Poland Capped ETF (EPOL)

KraneShares CSI China Internet ETF (KWEB)

PowerShares Golden Dragon China ETF (PGJ)

SPDR S&P China ETF (GXC)

VanEck Vectors Brazil Small-Cap ETF (BRF)

VanEck Vectors India Small-Cap ETF (SCIF)

WisdomTree China Ex-State-Owned Enterprise ETF (CXSE)

There have been so many foreign-ETF winners that it’s been tough to pick a loser! All you had to do was see that the dollar’s recent gains couldn’t last after an unprecedented run.

Trend No. 3: Fear Is Disappearing (3 Funds)

The third big trend is, paradoxically, the one that has scared a lot of people. And that’s because a lot of people aren’t scared.

Confused?

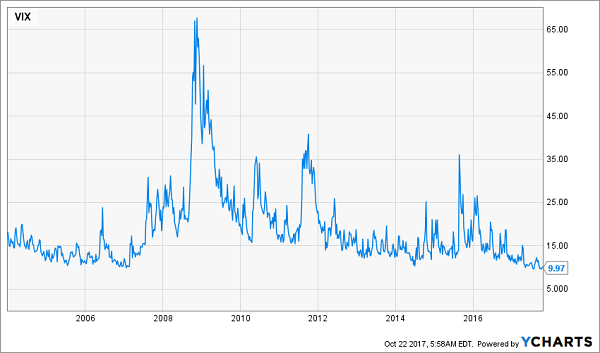

It’s an old belief that’s the cornerstone of contrarian investing. The idea is simple: bubbles form when everyone gets greedy, no one is fearful, and asset prices get too pricey. The market has definitely moved away from fear. No evidence of that is clearer than the VIX.

The what?

The VIX, or the CBOE Volatility Index, is a measure of S&P 500 price fluctuations. A higher number represents more uncertainty—that is, more fear. A lower number represents more confidence that a crash is unlikely.

The VIX is currently at 9.95, far from 13.75 a year ago, really far from its long-term average of 18.7 and even further from its all-time high of 67, in the midst of the financial crisis.

The VIX: A Picture of Tranquility

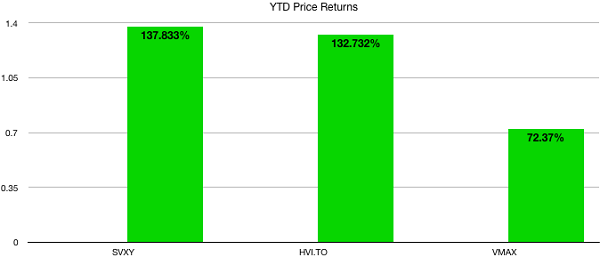

While a lot of pundits have spent 2017 warning that the VIX is due to rise “any day now,” anyone betting that the opposite would happen has made out like a bandit. Just behind bitcoin, the best performing ETFs of 2017 have been short volatility:

Michael Foster has just uncovered 4 funds that tick off ALL his boxes for the perfect investment: a 7.4% average payout, steady dividend growth and 20%+ price upside. — but that won’t last long! Grab a piece of the action now, before the market comes to its senses. CLICK HERE and he’ll tell you all about his top 4 high-yield picks.

Source: Contrarian Outlook

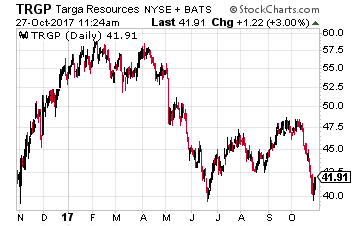

Targa Resources Corp (NYSE: TRGP) engages in the following energy midstream services:

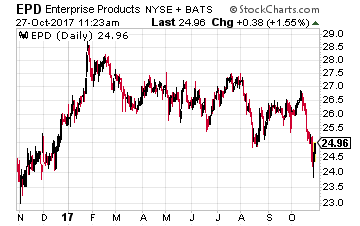

Targa Resources Corp (NYSE: TRGP) engages in the following energy midstream services: Enterprise Products Partners LP (NYSE: EPD) has a market cap more than $50 billion and is the largest MLP by enterprise value. The company’s business segments include:

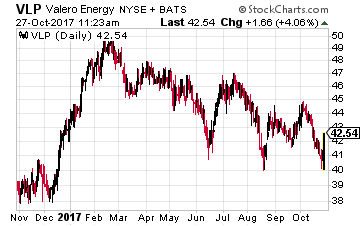

Enterprise Products Partners LP (NYSE: EPD) has a market cap more than $50 billion and is the largest MLP by enterprise value. The company’s business segments include: Valero Energy Partners LP (NYSE: VLP) is controlled by and provides pipeline, storage and terminal services to its sponsor, Valero Energy Corporation (NYSE: VLO). Through asset drops from Valero, the cash flow and distribution growth at VLP is very predictable. The VLP payments to investors will grow 25% in 2017 and at least by 20% in 2018, with high probability for 20% growth in future years. Now at $41, VLP could easily surpass its 52-week high of $51. The units currently yield 4.7%.

Valero Energy Partners LP (NYSE: VLP) is controlled by and provides pipeline, storage and terminal services to its sponsor, Valero Energy Corporation (NYSE: VLO). Through asset drops from Valero, the cash flow and distribution growth at VLP is very predictable. The VLP payments to investors will grow 25% in 2017 and at least by 20% in 2018, with high probability for 20% growth in future years. Now at $41, VLP could easily surpass its 52-week high of $51. The units currently yield 4.7%.

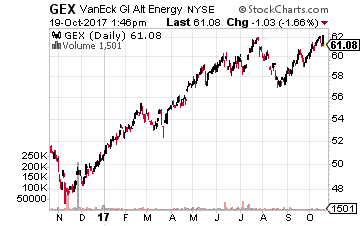

But that doesn’t mean you can’t make money with some U.S.-listed investments. For very broad exposure to the sector, there is the VanEck Vectors Global Alternative Energy ETF (NYSE: GEX). It is up a very nice 21% year-to-date and over 17% the past year.

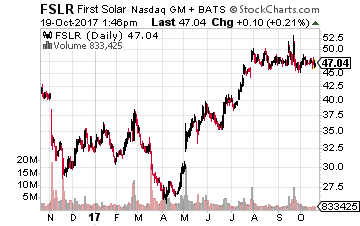

But that doesn’t mean you can’t make money with some U.S.-listed investments. For very broad exposure to the sector, there is the VanEck Vectors Global Alternative Energy ETF (NYSE: GEX). It is up a very nice 21% year-to-date and over 17% the past year. For single stock exposure to solar power, a good choice is First Solar (Nasdaq: FSLR), which is also in GEX’s portfolio. The stock has gained nearly 48% year-to-date. The company is the leading global provider of solar energy solutions with more than 10 gigawatts of installed capacity.

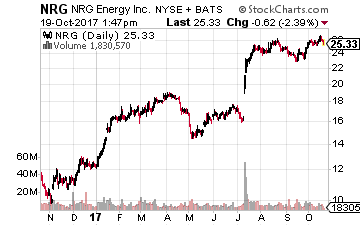

For single stock exposure to solar power, a good choice is First Solar (Nasdaq: FSLR), which is also in GEX’s portfolio. The stock has gained nearly 48% year-to-date. The company is the leading global provider of solar energy solutions with more than 10 gigawatts of installed capacity. Another possible way to play the rush to renewable energy is through a utility that is involved in the sector. One such example is NRG Energy (NYSE: NRG), which is the second-largest U.S. power producer and is expanding its renewable energy operations. Its stock has soared 113% year-to-date and is up 123% over the past 12 months. So even more than the double digits promised in the headline.

Another possible way to play the rush to renewable energy is through a utility that is involved in the sector. One such example is NRG Energy (NYSE: NRG), which is the second-largest U.S. power producer and is expanding its renewable energy operations. Its stock has soared 113% year-to-date and is up 123% over the past 12 months. So even more than the double digits promised in the headline.