When it comes to investing, too many folks ignore the signal and listen to the noise.

Case in point: one of the biggest stories of 2018—a looming trade war between America and China. Lately, the story has mutated into one about a trade war between America and, well, just about everyone—Europe, Asia, Mexico, even Canada!

But this trade war is noise—2018 has been a great year for stocks, and it’s going to get even better. Further on, I’ll give you a couple great ways to cash in.

First, a look at the facts, which are plain for everyone to see … and they clearly prove the naysayers wrong. You only have to look as far as corporate earnings.

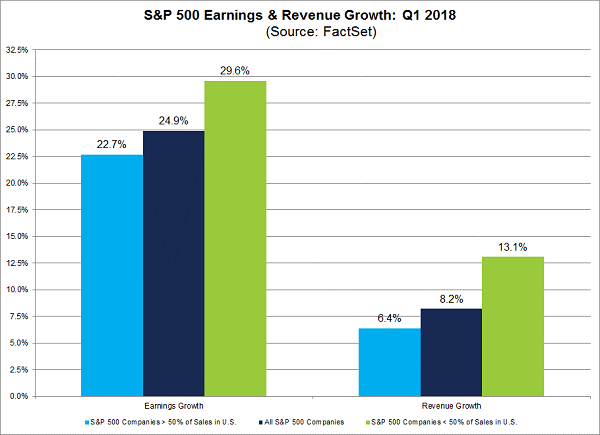

American Businesses Are Booming

In the first quarter, profits soared a shocking 24.9% and went even higher for companies selling outside the US. At the same time, exporters saw 13.1% sales growth, while all S&P 500 companies’ sales were up 8.2%.

So all great news, right?

Funny thing is, while this news was trickling out, the stock market did this:

Mr. Market Takes a Nap—and Gives Us Our Shot

While the data told us companies’ stocks should be soaring, they were grounded—and the early-year correction held on, even as the data got better. More recently, stocks have been rebounding, as investors finally noticed 3 locked-in trends driving the market higher.

#1: Fatter Profits, Higher Stocks (it’s inevitable)

Second-quarter earnings look strong, with 19% gains expected. And that trend of exporting companies outperforming importing ones is still there (net exporters are expected to see 23.9% earnings increases), again proving the trade-war hysteria wrong.

And I know I don’t have to tell you that where profits go, stock prices follow.

Here’s yet another reason why now is a great time to get in: because of this breakneck earnings growth, the S&P 500’s forward 12-month P/E ratio is 16.6, lower than the long-term average of about 17. But most folks miss the fact that since the S&P 500 is dominated by tech companies that didn’t exist decades ago, and since tech firms tend to have higher P/E ratios, that 16.6 level is even lower than it looks.

#2: Sales—the Key to Rising Profits—Are Heating Up

If a company is growing earnings while revenue slides, it’s probably cutting costs and not investing in itself. But if revenue is rising, obviously the market wants more of its product, and that’s never bad.

And revenue growth is going up. In the first quarter, sales rose 8.2% for the S&P 500, and they’re expected to rise 8.7% in Q2. Simply put: it’s getting easier for businesses to grow, and who wouldn’t want to invest in that kind of market?

#3: No Bubbles in Sight

What’s more, there’s nothing in the economy (with the exception of Bitcoin and cryptocurrencies, which I warned about at the start of 2018) that looks like a bubble.

Corporate-debt levels are modest; default rates have been falling since the end of 2015 (even though this is when the Federal Reserve started raising interest rates); housing-price growth keeps moderating; and other indicators (consumer-debt ratios, inflation, unemployment) look strong.

In short, despite the immature politics and hysterical panic we read about every day, Americans and companies are managing their financial lives in a mature, healthy and sustainable way. And that’s great for the market.

Please don't make this huge dividend mistake... If you are currently investing in dividend stocks – or even if you think you MIGHT invest in any dividend stocks over the next several months – then please take a few minutes to read this urgent new report. Not only could it prevent you from making a huge mistake related to income investing, it could also help you earn 12% a year from here on out! Click here to get the full story right away.

Source: Contrarian Outlook

Plains All American Pipeline LP (NYSE: PAA) is a $30 billion enterprise value MLP focused on crude oil pipelines and terminals. Plains has focused on the Permian and is investing $1.6 billion in growth capital to expand its crude oil gathering and pipeline takeaway capacity in the Basin.

Plains All American Pipeline LP (NYSE: PAA) is a $30 billion enterprise value MLP focused on crude oil pipelines and terminals. Plains has focused on the Permian and is investing $1.6 billion in growth capital to expand its crude oil gathering and pipeline takeaway capacity in the Basin. Targa Resources Corp (NYSE: TRGP) is an $11 billion market cap energy midstream company focused on the gathering, processing, transport and export of natural gas liquids (NGLs). These energy liquids are a big part of the value process of energy production in the Permian, North Texas and Oklahoma.

Targa Resources Corp (NYSE: TRGP) is an $11 billion market cap energy midstream company focused on the gathering, processing, transport and export of natural gas liquids (NGLs). These energy liquids are a big part of the value process of energy production in the Permian, North Texas and Oklahoma. NuStar Energy LP (NYSE: NS) is an MLP whose business operations are a balance of pipelines and storage facilities for both crude oil and refined energy projects. In May 2017 the company acquired an integrated crude oil and transport system in the heart of the Permian Basin.

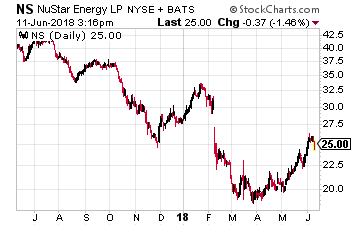

NuStar Energy LP (NYSE: NS) is an MLP whose business operations are a balance of pipelines and storage facilities for both crude oil and refined energy projects. In May 2017 the company acquired an integrated crude oil and transport system in the heart of the Permian Basin.