Last week I hosted an online session for my Dividend Hunter newsletter subscribers with InfraCap co-founders Jay Hatfield, CEO and Portfolio Manager and Edward Ryan, CFO and COO. During the hour long discussion we covered MLP investing and the changes to the high-yield InfraCap MLP ETF (NYSE: AMZA).

In January, AMZA announced a dividend policy change, going from quarterly to monthly and reducing the overall annual rate. As a result, the AMZA yield went from over 20% down to 15%. The move will benefit investors in the long term, but I wanted to get Jay and Ed in to discuss the different aspects of managing AMZA with my newsletter subscribers. The following is from my notes on the session.

The discussion started with details on valuations in the MLP space. It was shown on the presentation slides that compared to historical values the MLP yield and yield spread over BBB rated bonds are relatively high, which indicates MLPs are undervalued on historical standards.

The yield for the Alerian MLP Infrastructure Index (AMZI) is just under 8%, while REITs are yielding about 4.7% and utilities are at 4.0%. The slides on Enterprise value (EV) to EBITDA and Debt/EBITDA show that MLPs have as a group fixed their financial issues that caused business stress when energy prices crashed in 2015.

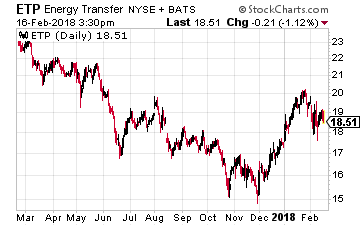

I asked Jay to discuss why he liked Energy Transfer Partners LP (NYSE: ETP) as the largest holding in the InfraCap MLP ETF (NYSE: AMZA). He discussed how ETP had become undervalued due to mechanical selling. When ETP merged with Sunoco Logistics, ETP was suddenly overweight in index tracking MLP funds. These index funds were forced to sell ETP to become balanced with the MLP indexes they are committed to mirror. Then Alerian put a 10% weighting cap on MLPs in the AMZI, and funds tracking that popular MLP index were again forced to sell ETP units to stay in line with the index weightings. The result is that Jay believes ETP with its 12% yield is very undervalued and has lots of upside potential from here.

I asked Jay to discuss why he liked Energy Transfer Partners LP (NYSE: ETP) as the largest holding in the InfraCap MLP ETF (NYSE: AMZA). He discussed how ETP had become undervalued due to mechanical selling. When ETP merged with Sunoco Logistics, ETP was suddenly overweight in index tracking MLP funds. These index funds were forced to sell ETP to become balanced with the MLP indexes they are committed to mirror. Then Alerian put a 10% weighting cap on MLPs in the AMZI, and funds tracking that popular MLP index were again forced to sell ETP units to stay in line with the index weightings. The result is that Jay believes ETP with its 12% yield is very undervalued and has lots of upside potential from here.

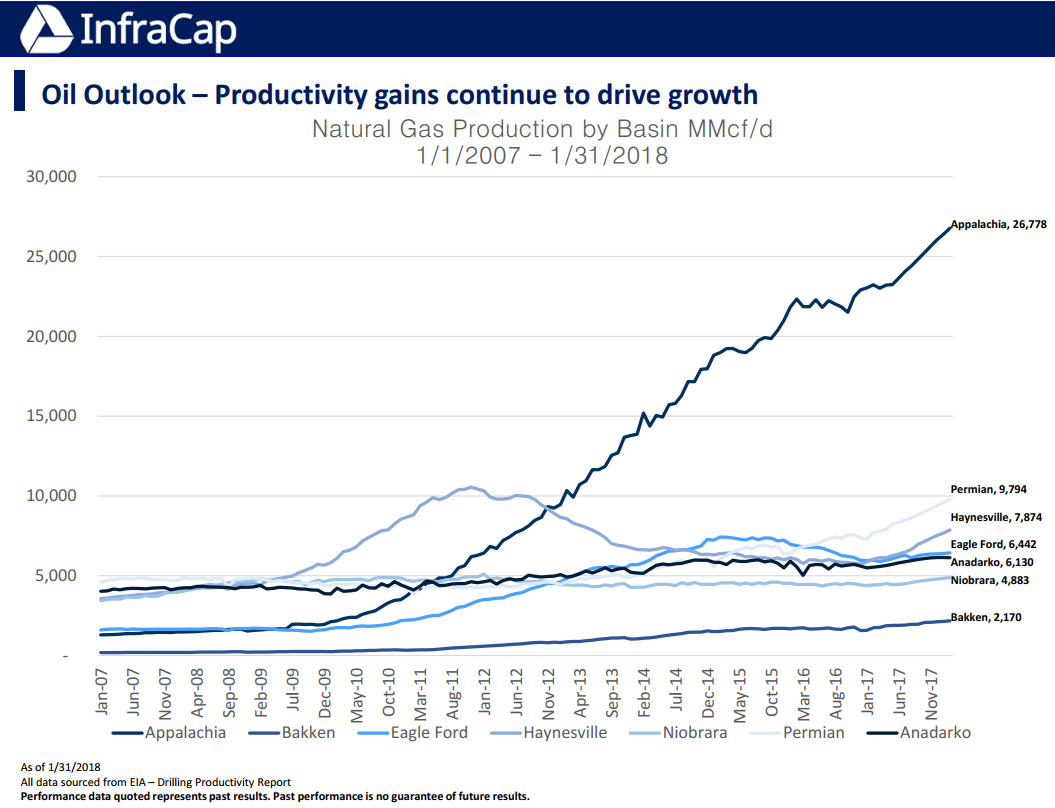

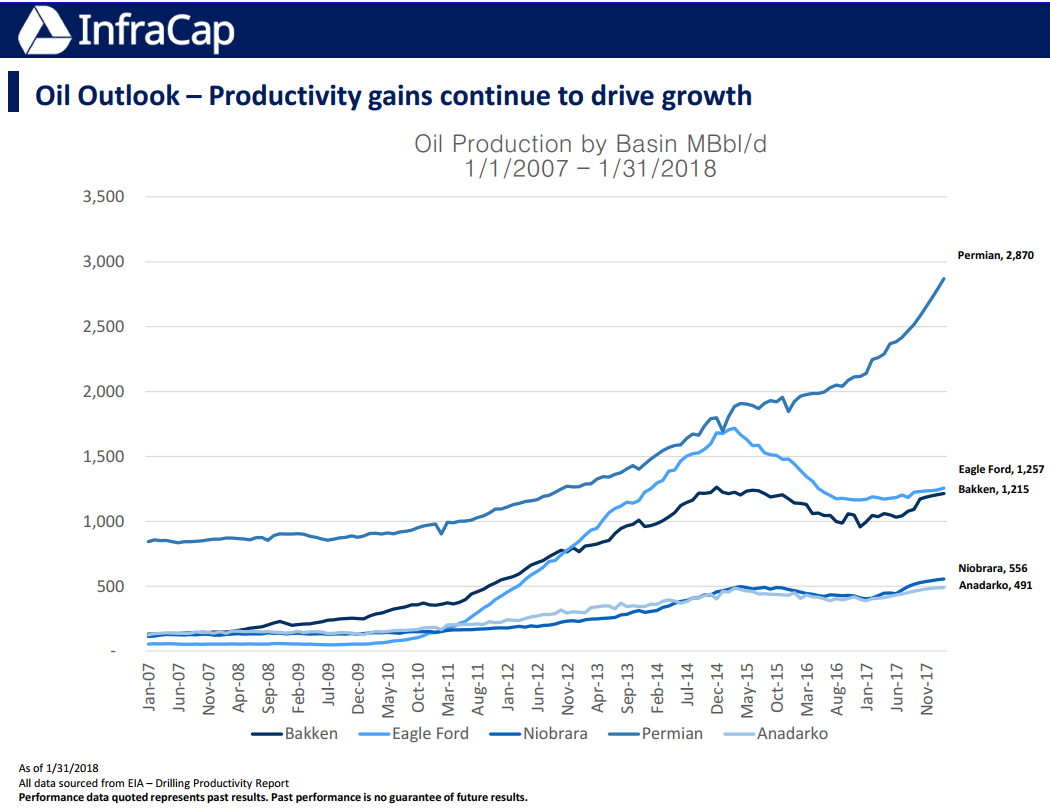

We discussed the fact that MLP market values are highly influenced by the swings in energy commodity prices, especially crude oil. At the same time, both crude oil and natural gas production in the U.S. continue to grow.

Crude oil production growth is decreasing the need for oil imports and the increase in natural gas is being absorbed by the shift to gas to produce electricity, new chemical plants being built in the U.S. and the recent launch and growth of LNG exports. These charts show the production growth. It is this growth that produces the revenue growth for midstream MLPs. It was noted that MLPs increased distributions by 1.5% for the 2018 first quarter, which puts the sector on path for 6% annual distribution growth.

Now to the topic I think most want to hear about, the AMZA dividends. Ed and Jay discussed how during the last year, they were getting large purchases of new shares just before the ex-dividend date. As a result, they would have to immediately pay out some of the new capital as dividends. This left less capital to invest in MLPs to support the future dividends on new and existing shares.

With MLP values declining in 2017 it became very difficult to support both the dividend rate and the NAV (share value). Despite the challenges, AMZA did outperform the AMZI in 2017. The new dividend rate of $0.11 per share and monthly payment are intended to both continue to pay a very attractive yield and allow the NAV to grow.

The new dividend rate gives AMZA a 15% yield. The distributions from MLPs owned by the fund account for the first 10% and the fund’s call selling program will bring in the other 5%. Jay expressed confidence the management team could produce 5% cash flow from option selling and still grow the NAV when MLP values move higher. Ed and Jay also noted that the 5% figure will stay the same as the NAV increases. This means that if AMZA moves up to $10 or $12 per share, they will be able to generate higher cash per share from the options program. This fact plus the distribution growth in the MLP sector gives the potential for future dividend growth from AMZA. Nothing was predicted, and much is dependent on MLP values.

Taxes on dividends were discussed. Since MLP distributions are classified as non-taxable return of capital, the two-thirds of the AMZA dividend from the MLP distributions will be ROC. The one-third from the options selling program will come through as qualified dividends. Ed noted that future dividends should end up close to the two-thirds/one-third tax characteristics with the new dividend program. About taxes, Ed noted that the new tax law and lower corporate income tax rate provides a higher relative benefit to MLP funds compared to individual MLP investments.

Source: Investors Alley