Source: Shutterstock

In Warren Buffett’s 1992 letter to Berkshire Hathaway Inc. (NYSE:BRK.B) shareholders, Buffett touches upon a subject at odds with much of the investment industry:

“Most analysts feel they must choose between two approaches customarily thought to be in opposition: ‘value’ and ‘growth.’ Indeed, many investment professionals see any mixing of the two terms as a form of intellectual cross-dressing.

We view that as fuzzy thinking… In our opinion, the two approaches are joined at the hip: Growth is always a component in the calculation of value, constituting a variable whose importance can range from negligible to enormous and whose impact can be negative as well as positive.”

Many investors tend to categorize stocks into value and growth. However, the most successful investors view growth as simply one component of a company’s value as Mr. Buffett explains.

The future outlook for a company is an important aspect when you’re looking at buying a stock. And while value investors would argue that it’s the intrinsic value relative to the current trading price that matters the most, a more compelling investment thesis would be high growth potential at a cheap price.

Therefore, I used finbox.io’s stock screener to see if I could find high growth stocks trading below their intrinsic value.

Screening for Inexpensive Growth Stocks

The following are all the filters applied in this growth at a reasonable price stock screen:

- Upside as calculated from finbox.io’s fair value estimate > 0%

- Upside as calculated from consensus analyst price targets > 5%.

- Historical 5-year Revenue CAGR > 10%

- Projected 5-year Revenue CAGR > 10%

- EBITDA Margin > 0%

- Revenue > $1 billion

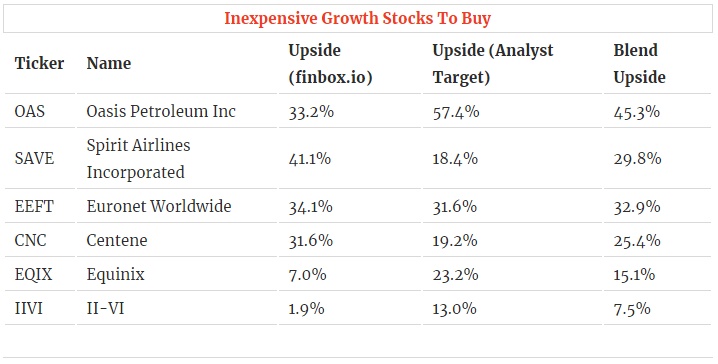

The six stocks that stood out from the screen above are presented below.

Inexpensive Growth Stocks to Buy Now: Oasis Petroleum (OAS)

Oasis Petroleum Inc. (NYSE:OAS) is an exploration and production company.

The company’s total revenue stands at $1,248 million as of fiscal year ending December 2017. This is 81.8% higher than the $687 million achieved in fiscal year December 2012 and represents a five-year compounded annual growth rate (CAGR) of 12.7%.

Source: finbox.io

Analysts forecast that Oasis Petroleum’s total revenue will reach $3,012 million by fiscal year 2022 representing a five-year CAGR of 19.3%.

Source: finbox.io

Shares of the company are down -38.8% over the last year while the stock last traded at $8.00 as of Tuesday, March 20th. Three separate valuation analyses imply that there is 34.7% upside relative to its current trading price. Wall Street’s price target of $12.43 per share implies even further upside.

It’s also worth noting that illustrious money manager T Boone Pickens currently owns 331,541 shares of OAS which represents 1.0% of his stock portfolio. T. Boone Pickens is a legend in the American energy industry and has been labeled anywhere from a ‘wildcatter’ to a corporate raider. He clearly expects outsized returns from his investment in OAS.

Inexpensive Growth Stocks to Buy Now: Spirit Airlines (SAVE)

Spirit Airlines Incorporated (NYSE:SAVE) is a low-fare airline operating in North America.

The airline’s total revenue stands at $2,648 million as of fiscal year ending December 2017. This is 100.8% higher than the $1,318 million achieved in fiscal year December 2012. In addition, Spirit’s revenue growth has been fairly stable ranging from 8.4% to 25.5% over the last five years.

Source: finbox.io

Going forward, Wall Street is forecasting that Spirit’s total revenue will reach $4,508 million by fiscal year 2022 representing a five-year CAGR of 11.2%.

Source: finbox.io

Shares of Spirit Airlines are down -13.0% over the last year and finbox.io’s fair value estimate of $62.66 per share calculated from six cash flow models imply 41.1% upside. The average price target from 15 Wall Street analysts of $52.47 per share similarly imply upside.

Inexpensive Growth Stocks to Buy Now: Euronet (EEFT)

Euronet Worldwide, Inc. (NASDAQ:EEFT) provides electronic payment services to financial institutions and retailers worldwide.

The company’s total revenue stands at $2,252 million as of fiscal year ending December 2017. This is 77.7% higher than the $1,268 million achieved in fiscal year December 2012 and represents a five-year CAGR of 12.2%. Euronet Worldwide’s revenue growth has also steadily ranged from 6.5% to 17.8% over the last five fiscal years.

Source: finbox.io

Analysts are estimating that Euronet Worldwide’s total revenue will reach $3,869 million by fiscal year 2022 representing a five-year CAGR of 11.4%.

Applying these assumptions to 8 valuation models imply nice upside for shareholders.

Source: finbox.io

Euronet Worldwide’s stock currently trades at $86.43 per share as of Tuesday, up only 2.8% over the last year. However, finbox.io’s intrinsic value estimate suggests that shares could increase 34.1% going forward.

Furthermore, Joel Greenblatt is a notable investor in the company. His fund currently holds a position worth $9.0 million. Greenblatt is best known for a very specific style of value investing termed: Magic Formula Investing. The company clearly has the fundamental characteristics that make it a perfect fit within his magic formula.

Inexpensive Growth Stocks to Buy Now: Centene (CNC)

Centene Corp (NYSE:CNC) is a multi-national healthcare enterprise that acts as an intermediary between government and private health insurance programs.

The company’s total revenue stands at $48.3 billion as of its latest fiscal year. This is nearly 5x higher than the $8.1 billion achieved five years prior.

Source: finbox.io

Going forward, analysts are forecasting that Centene’s total revenue will reach $87.9 billion by fiscal year 2022 representing a five-year CAGR of 12.7%.

Source: finbox.io

Shares of the company are trading 54.2% higher year over year. But the stock price could end up trading another 31.6% higher in 2018 based on Centene’s future cash flow projections.

It’s worth noting that highly followed portfolio manager David Tepper currently holds a position in Centene worth $76.5 million. Tepper, founder and portfolio manager at Appaloosa Management, is widely known for having inspired what’s been dubbed the Tepper Rally of 2010. Through his macro view of the financial markets, Tepper was able to predict not only the stock market rally but the catalysts behind it which ultimately proved to be the Fed’s stimulus. Whatever the catalyst, Tepper is likely expecting a sizable rally in Centene’s stock price.

Inexpensive Growth Stocks to Buy Now: Equinix (EQIX)

Equinix Inc (NASDAQ:EQIX) connects businesses to their customers, employees and partners via data centers.

The company’s top-line reached $4,368 million as of its latest fiscal year, up 131.5% from fiscal year December 2012. Over that time period, Equinix’s revenue growth has ranged from 11.5% to 32.5%.

Source: finbox.io

Wall Street analysts estimate that Equinix’s total revenue will continue to grow at an annual rate of 10.1% over the next five years.

Source: finbox.io

Equinix’s stock currently trades at $414.48 per share as of Tuesday, up 9.4% over the last year. On a fundamental basis, the company’s stock is trading at a 7.0% discount to finbox.io’s intrinsic value estimate. However, the average price target from 22 Wall Street analysts of $507.23 implies 23.2% upside.

Inexpensive Growth Stocks to Buy Now: II-VI (IIVI)

II-VI, Inc. (NASDAQ:IIVI) is an electronics component manufacturer.

The company’s total revenue reached $972 million as of fiscal year ending June 2017. This is 88.2% higher than the $516 million achieved in fiscal year June 2012. II-VI’s top-line growth has ranged from 6.7% to 24.0% over the last five fiscal years.

Source: finbox.io

Going forward, Wall Street forecasts that II-VI’s total revenue will reach $1,839 million by fiscal year 2022 representing a five-year CAGR of 13.6%.

Source: finbox.io

Shares of the company are up 23.0% over the last year. The stock last traded at $47.25 as of March 20th and 8 separate valuation analyses imply that the stock is trading near its fair value. However, the average price target from nine Wall Street analysts implies 13.0% upside.

Inexpensive Growth Stocks to Buy Now: A Summary

While investors tend to categorize stocks into value and growth, some of the most successful investors view growth as simply one component of a company’s value. The companies above have positioned themselves so that double-digit growth appears to be a reasonable assumption for the foreseeable future. More importantly, this growth actually looks attractive relative to their current trading levels. As such, value and growth investors may want to take a closer look at these names.

In conclusion, the table below ranks all six stocks by their blended upside.

Matt Hogan is a co-founder of finbox.io. His expertise is in investment decision making. Prior to finbox.io, Matt worked for an investment banking group providing fairness opinions in connection to stock acquisitions. He spent much of his time building valuation models to help clients determine an asset’s fair value. He believes that these same valuation models should be used by all investors before buying or selling a stock.

Source: Investor Place