Stocks to Sell in March: Big 5 Sporting Goods Corporation (BGFV)

When I think of stocks to sell, Big 5 Sporting Goods Corporation (NASDAQ:BGFV) comes immediately to mind. Unfortunately, BGFV suffers from two double whammies: a terribly poor retail environment for sports equipment, and rising outcry over gun violence.

My first point is obvious. A surefire way to fail in business is to open a sporting goods store. The more specific the endeavor — in this case, outdoors sports — the more likely you’ll fail. Consider that in the past few years, specialty retailers Golfsmith and Eastern Outfitters filed for bankruptcy. Additionally, big name stores like Sports Authority and Sport Chalet closed their operations.

As a forgotten side note, the upside to BGFV stock is extremely limited. Even worse, the company will have to deal with the stigma of selling guns and ammunition. That in and of itself wouldn’t be a significant problem if it weren’t for the fact that Big 5 sells boring guns at ridiculous premiums.

Whenever gun control fears spike, people buy out politically targeted firearms; namely, the maligned AR15 and Kalashnikov-style rifles. Unfortunately, Big 5 doesn’t sell these guns. Instead, they offer shotguns, bolt-action rifles among other firearms. Thus, they deal with the stigma without any of the “benefit.”

That’s bad news for BGFV stock, and I don’t think circumstances will improve.

Stocks to Sell in March: New York Times Co (NYT)

The bear case for New York Times Co (NYSE:NYT) is a tough pill to swallow for me. Last year, I stated that NYT stock will win big in the era of “fake news.” No matter what side of the political spectrum you belong, we can say that everyone loves drama. Despite the NYT obviously not liking President Trump, he ironically gave the Times a reason to exist.

Since I last wrote about NYT stock, shares have gone up a whopping 67%. On a year-to-date basis, the Times has, in my view, inexplicably gained nearly 34%. I was bullish on this iconic news organization, but I think enough’s enough. The rally has gone too far, too fast and it’s time for a pullback.

Supposedly, rising sales in digital advertising and digital-only subscriptions contributed heavily to NYT stock. I say big deal. Not only are we experiencing a media revolution in which mainstream outlets are falling behind, people simply don’t get their news from the news anymore. How else can you explain Alex Jones’ popularity?

We live in a world where conspiracy theorists are given a (generous) platform simply because they’re not mainstream. And while NYT benefits from Trump scandals, I think the American people have had enough.

NYT stock deserves to be up, but not by this much!

Stocks to Sell in March: Jack in the Box Inc. (JACK)

When I was growing up, eating a McDonald’s Corporation (NYSE:MCD) Big Mac was considered a rite of passage. Today, it’s rightfully considered child abuse. That’s why I was so shocked when I read our Will Ashworth’s latest piece on MCD. Mind you, I don’t care that he’s bullish on the company. Rather, I was floored when he gladly admitted to eating the stuff!

Joking aside, American public sentiment towards fast food is sharply declining. Most people are concerned about their health than ever before, particularly the younger generation. With several fast food companies having made strong gains in recent years, I think now is a great time to take profits. This goes double for smaller eateries like Jack in the Box Inc. (NASDAQ:JACK).

The McDonald’s eating Ashworth made strong points about MCD, noting their aggressive push into budget meals and food deliveries. You combine this with their overall image renovation, and you have an outperformer in a soon-to-be-declining industry. McDonald’s can afford to do this. I’m not so sure that JACK can pull it off.

While I appreciate Jack in the Box’s humorous commercials, the competition moving forward will be fierce. McDonald’s has the brand, the locations, and the resources. JACK has funny advertisements. Beyond that, its shares’ technical volatility concerns me.

JACK stock enjoyed a stellar run from 2016, but it’s time to take some profits off the table.

Stocks to Sell in March: Twitter Inc (TWTR)

Admittedly, I’m not the social media platform’s biggest fan. Therefore, it’s no surprise that I’ve been rather dim on Twitter Inc (NYSE:TWTR). While TWTR stock’s recent meteoric rise has been nothing short of stunning, I don’t like to chase momentum. I especially don’t like to chase investments that are not fundamentally sound.

Say what you want about the nearer-term trading opportunities for TWTR; its organizational structure is pure chaos. As my InvestorPlace colleague Dana Blankenhorn explained, COO Anthony Noto left the company to seek greener pastures. We all know that head executive Jack Dorsey is a part-timer. Blankenhorn writes that “Twitter has lost its adult supervision.” I do not disagree.

A breaking Reuters story, though, offers a contrasting take. TWTR is gaining both subscribers and ad revenues in Japan. The implication is that Twitter can duplicate the Japanese success in other markets.

To that, I say, good luck. Things are different in Japan. Facebook Inc (NASDAQ:FB) isn’t the undisputed, dominant social media platform. The Japanese prefer the Yahoo search engine over Alphabet Inc’s (NASDAQ:GOOG,NASDAQ:GOOGL) ubiquitous Google.

Even if Twitter manages to turn Japan into its own powerhouse asset, one country won’t solve its problems. Specifically, its subscriber growth is stagnating and until they figure that out, TWTR is just floating on empty speculation.

Stocks to Sell in March: Dillard’s, Inc. (DDS)

Business owners always fear market saturation, but in reality, saturation in and of itself isn’t a problem. Issues arise when the underlying industry cannot support the present number of competitors; that’s when market saturation rears its ugly head. I believe that head is turning quite aggressively against Dillard’s, Inc. (NYSE:DDS).

With e-commerce giants like Amazon.com, Inc. (NASDAQ:AMZN) tearing into market share, being a specialty department store was always going to be a challenge. What brick-and-mortars had to their advantage was the apparel industry: you don’t know if something is going to fit you until you try it. But because every other brick-and-mortar have rebranded their businesses, DDS looks ancient.

It lacks Nordstrom, Inc.’s (NYSE:JWN) pizzazz. More people recognize the Macy’s Inc(NYSE:M) brand than Dillard’s. Neither of the companies have investors aching to buy their respective shares. Unfortunately, the physical retail market is shrinking, and DDS is the odd man out.

But the most important point to consider is the technical argument. On a year-to-date basis, DDS stock is up nearly 36%. Does it, or any other specialty department store, deserve to be up this high so quickly? I seriously doubt it, which is why I placed DDS on this stocks to sell list.

Source: Investor Place

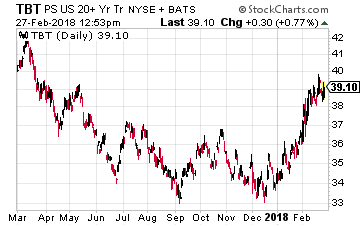

Then putting money into the ProShares UltraShort 20+Year Treasury ETF (NYSE: TBT) would make a lot of sense. This ETF uses futures and swaps to correspond to twice the inverse of the ICE U.S. Treasury 20+Year Bond Index. It is up 15% year-to-date thanks to the recent bond market scare, but is little changed over the past year.

Then putting money into the ProShares UltraShort 20+Year Treasury ETF (NYSE: TBT) would make a lot of sense. This ETF uses futures and swaps to correspond to twice the inverse of the ICE U.S. Treasury 20+Year Bond Index. It is up 15% year-to-date thanks to the recent bond market scare, but is little changed over the past year.