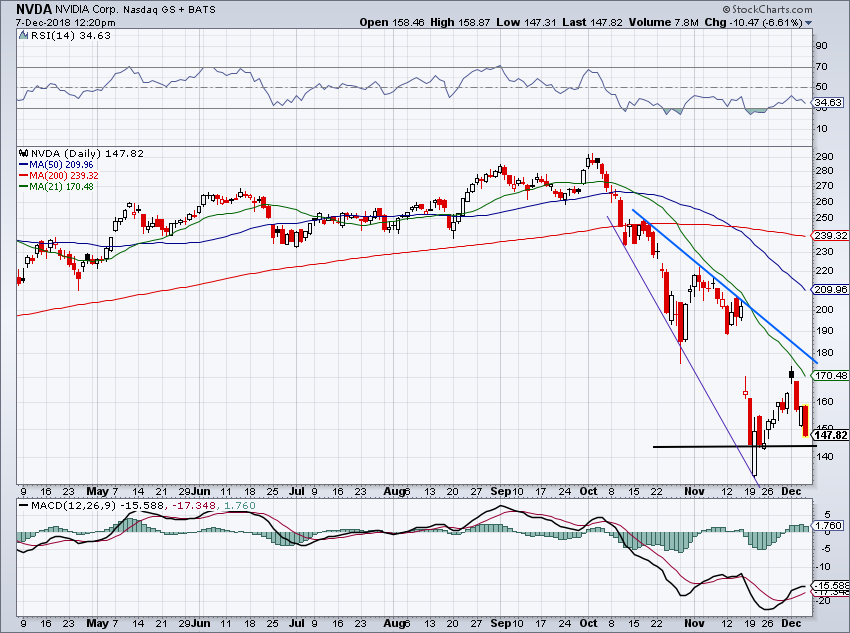

To build momentum from your income stocks going into the new year, consider buying into those REITs that should announce higher dividend rates in the first month of 2019. Each month I publish a list of those real estate investment trusts (REITs) that should announce higher dividend rates in the upcoming months. This knowledge can give you a jump on the rest of investing public, which will be surprised when the positive news is announced.

I maintain a database of about 130 REITs. With it I track current yields, dividend growth rates and when these companies usually announced new dividend rates. Most REITs announce a new dividend rate once a year, and then pay that rate for the next four quarters. Currently about 85 REITs in my database have recent and ongoing histories of dividend growth. Out of that group, higher dividend announcements will come from different REIT companies during almost every month of the year. With the potential of continued Fed interest rate hikes, the prospects of higher dividend payments coming in January will help to offset any share price disruptions resulting from announcements out of the Federal Reserve Board.

My list shows three companies that historically announce higher dividends in January and should do so again this year. Investors will start earning the higher payouts in the new year. But remember, you want to buy shares before the dividend announcement to get the benefit of a share price bump caused by the positive news event.

Here are three REITs expected to raise dividends that you might want to consider:

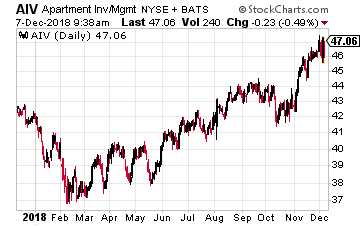

Apartment Investment and Management (NYSE: AIV) is a mid-cap sized REIT that owns and operates about 140 apartment communities.

Apartment Investment and Management (NYSE: AIV) is a mid-cap sized REIT that owns and operates about 140 apartment communities.

About 40% of the company’s properties are in coastal California, with the balance spread across major U.S. metropolitan areas.

Last year, AIV increased its dividend by 5.6%. Cash flow growth has been comparable in 2018, and I forecast an 5% to 6% dividend increase in January.

The new dividend rate announcement will come out in late January with a mid-February ex-dividend date and payment at the end of February.

AIV yields 3.3%.

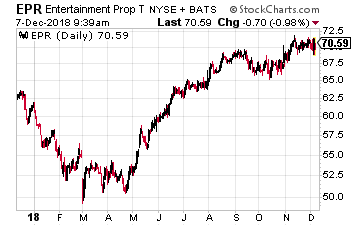

EPR Properties (NYSE: EPR) focuses its real estate investments in three different business sectors. Primary is the ownership and triple-net leasing of entertainment complexes and multiplex theaters. The second sector is the ownership of golf and ski recreation centers, also triple-net leased. The third sector is the construction, ownership and leasing of private and charter schools.

EPR Properties (NYSE: EPR) focuses its real estate investments in three different business sectors. Primary is the ownership and triple-net leasing of entertainment complexes and multiplex theaters. The second sector is the ownership of golf and ski recreation centers, also triple-net leased. The third sector is the construction, ownership and leasing of private and charter schools.

EPR pays monthly dividends and has grown the dividend rate by an average of 6.3% per year for the last five years.

In 2018 the company was active in both acquisitions and new developments.

The new dividend rate is announced in mid-January, with an end of January record date and mid-February payment. This stock is a long-term recommendation in my Dividend Hunter high-yield investing service.

EPR currently yields 6.2%.

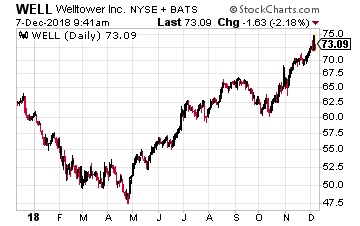

Welltower Inc (NYSE: WELL) is a large cap healthcare sector REIT. The company owns properties concentrated in markets in the United States, Canada and the United Kingdom.

Welltower Inc (NYSE: WELL) is a large cap healthcare sector REIT. The company owns properties concentrated in markets in the United States, Canada and the United Kingdom.

The portfolio is divided into three segments consisting of: Seniors housing, post-acute communities, and outpatient medical properties. Triple-net properties include independent living facilities, independent supportive living facilities, continuing care retirement communities, assisted living facilities, care homes with and without nursing, Alzheimer’s/dementia care facilities, long-term/post-acute care facilities and hospitals.

Outpatient medical properties include outpatient medical buildings. Welltower had increased its dividend every year since 2009 but did not change the rate at the beginning of 2017.

To get back on the dividend growth track, I expect a 2.0% to 2.5% increase to be announced in January.

The announcement will come out at the end of the month, with an early February record date and payment around February 20.

The stock yields 4.8%.

Pay Your Bills for LIFE with These Dividend Stocks

Get your hands on my most comprehensive, step-by-step dividend plan yet. In just a few minutes, you will have a 36-month road map that could generate $4,804 (or more!) per month for life. It's the perfect supplement to Social Security and works even if the stock market tanks. Over 6,500 retirement investors have already followed the recommendations I've laid out.

Click here for complete details to start your plan today.

Source: Investors Alley

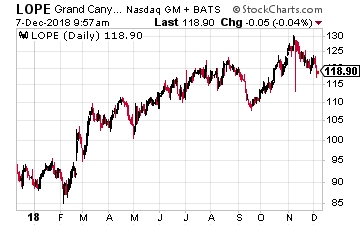

Grand Canyon Education (Nasdaq: LOPE)

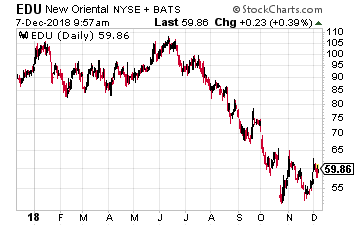

Grand Canyon Education (Nasdaq: LOPE) New Oriental Education & Technology Group (NYSE: EDU)

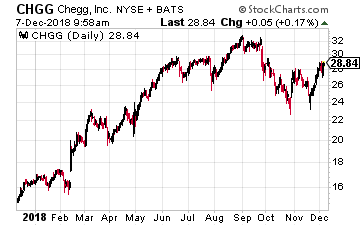

New Oriental Education & Technology Group (NYSE: EDU) Chegg, Inc. (Nasdaq: CHGG)

Chegg, Inc. (Nasdaq: CHGG)

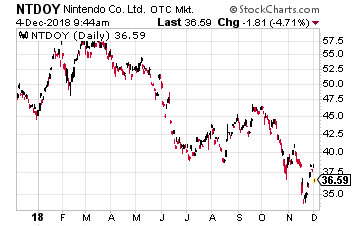

If you have children, you no doubt have heard of the Japanese gaming company Nintendo (OTC: NTDOY). It is doing well and recently announced its best quarterly results in eight years! It reported operating profits of ¥30.9 billion ($27.2 million) for the July to September quarter, up 30% on the same period a year earlier.

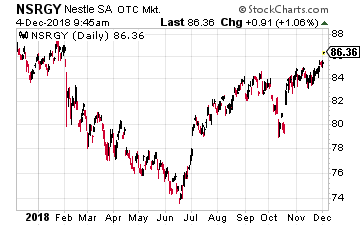

If you have children, you no doubt have heard of the Japanese gaming company Nintendo (OTC: NTDOY). It is doing well and recently announced its best quarterly results in eight years! It reported operating profits of ¥30.9 billion ($27.2 million) for the July to September quarter, up 30% on the same period a year earlier. For more conservative investors, there is the world’s largest food and beverage company, Switzerland’s Nestlé (OOTC: NSRGY), which was founded as a baby food manufacturer in the 1860s. Today, Nestlé’s four priority markets are coffee, bottled water, pet food and baby food.

For more conservative investors, there is the world’s largest food and beverage company, Switzerland’s Nestlé (OOTC: NSRGY), which was founded as a baby food manufacturer in the 1860s. Today, Nestlé’s four priority markets are coffee, bottled water, pet food and baby food. Nestlé said that the planned sale or spin-off would “sharpen its focus” on food, drinks and “nutritional health products”, led by its top brands including KitKat chocolate bars, Perrier bottled water and Purina pet food. The decision to abandon the skin health business I believe reduces still further the strategic case for Nestlé selling its 23% stake in the French cosmetics giant, L’Oreal (OTC: LRLCY).

Nestlé said that the planned sale or spin-off would “sharpen its focus” on food, drinks and “nutritional health products”, led by its top brands including KitKat chocolate bars, Perrier bottled water and Purina pet food. The decision to abandon the skin health business I believe reduces still further the strategic case for Nestlé selling its 23% stake in the French cosmetics giant, L’Oreal (OTC: LRLCY).