Markets rallied for a fifth straight week Friday as a trifecta of good news was enjoyed by investors. President Trump announced a temporary reopening of the U.S. government after reaching a deal with Congress. Unless a final deal is reached before mid-February, another shutdown could ensue. But, traders are hopeful this is a sign that a permanent solution can be reached.

The WSJ reported the Fed may be close to halting its program of quantitative tightening. This could give markets the breathing room they need to regather for another rally. And, finally, positive news on the trade front is raising confidence that additional tariffs will be avoided in coming months.

We are in the heart of earnings season, and the last week of January will start off with a bang. Monday morning analysts will get right to work dissecting earnings from Caterpillar (CAT) and then interpreting releases from Whirlpool (WHR) and Celanese (CE) after the close. Caterpillar has been a bellwether in the recent trade dispute between the U.S and China, rising when there is good news and falling when tensions between the countries rise. Analysts will be looking for the real impacts of the trade dispute when Cat reports. Whirlpool has long been viewed as a measure of how the consumer is holding up. The company is expected to report $4.30 per share, with the main question being whether the company is seeing inflationary pressures from its suppliers.

The Dallas Fed Manufacturing Survey and the Chicago Fed National Activity Index will both be released Monday. The Chicago numbers could be particularly interesting as they pick up activity nationwide, and should give a better reading on how weak manufacturing has become. Last month’s reading came in at .22, and the current three month average is .12. The positive numbers indicate manufacturing is still growing above trend, even with the recent falloff reported by regional Fed Banks. Tuesday analysts will look through Redbook retail numbers, international trade numbers, and the Corelogic Case-Schiller Home Price Index (HPI). The HPI October numbers were relatively flat.

Apple (AAPL) will be the headliner Tuesday when the company reports earnings. Investors are anticipating an update on sales in China, and many analysts feel price cuts are coming in the newest iPhones. Pfizer (PFE), Verizon (VZ) and 3M (MMM) also report Tuesday. The hits keep coming Wednesday when Microsoft (MSFT), Facebook (FB), and Visa (V) all report. Facebook’s Mark Zuckerberg will likely comment on Facebook’s advertising practices after penning a piece for the WSJ addressing the issue on Friday.

Mortgage applications, impending home sales, and the ADP employment report are all released Wednesday morning. Also on the slate are GDP numbers. GDP is expected to come in at 3.4% for the quarter. Wednesday afternoon will also mark the close of a two day Federal Open Market Committee meeting, with any interest rate changes announced at 2 pm. Traders do not expect any move by the Fed, but will be watching the statement closely for any deviation in wording from the Feds last comments.

Thursday we’ll hear from Amazon (AMZN), Mastercard (MA) and General Electric (GE) as they report quarterly earnings. Investors will likely get an update on how the standup of the new Amazon headquarters is progressing. Friday will be all about big oil as both Exxon Mobil (XOM) and Chevron (CVX) report before the opening bell.

Jobless claims and the employment cost index will be released Thursday. And on the first day of February, consumer sentiment, employment situation numbers, and the PMI manufacturing index will all be released Friday. Non-farm payrolls are expected to come in at 312K and the unemployment rate is projected to be 3.9%.

[Editor’s note: This story was originally published in August 2018. It has since been updated and republished to reflect changes in stock price, although the writer’s opinions may have changed.]

The stock market is a mess right now. Ever since Facebook (NASDAQ:FB) dropped the ball, the whole tech sector has rolled over and markets have dropped. The broad market volatility, however, does not change the bull thesis on cheap stocks. In the group of stocks under $5, macro market movements can cause some noise in shares. But, the investment thesis on cheap stocks is predicated on huge moves higher in the long-term. Thus, near-term, macro-driven movements amount to nothing more than a sideshow.

From this perspective, now might be a good time to pile into some stocks under $5. These stocks are a high-risk bunch. But, they do have high-reward potential, too. Just look at the three stocks under $10 that I recommended buying in late March, including Pandora (NYSE:P).

All three stocks were considered high-risk losers at the time. But since then, P stock has risen nearly 80%.

With that in mind, here is a list of five cheap stocks, which I think have equally big upside potential over the next several months.

Source: Shutterstock

Pier 1 (PIR)

PIR Stock Price: 71 cents

Furniture retailer Pier 1 Imports (NYSE:PIR) has had a tough time getting its act together for several years.

Peer Restoration Hardware (NYSE:RH) has seen its stock rise 30% over the past year thanks to a red-hot housing market and robust demand for home furnishings. PIR stock, however, has collapsed during that same stretch. These problems aren’t new. Over the past five years, this stock has lost more than 90% of its value.

Having said that, there is visibility for a turnaround in PIR stock in the near future.

At its core, Pier 1 has been killed by rising e-commerce threats creating huge pricing and traffic headwinds. Pier 1, which stands somewhat square in the middle of price and quality, doesn’t really have anything special about the business to protect against these headwinds. Consequently, sales and margins have dropped in a big way.

But, the company recently unveiled a three-year strategic plan to turn the business around. The plan includes a re-launch of the Pier 1 brand this fall and bigger investments into omni-channel commerce capabilities and marketing.

No one knows whether or not this plan will actually work. But, home furnishings is a market with enduring demand, so that helps. Plus, search interest related to the company is actually starting to grow on a year-over-year basis, illustrating that this plan is off to a good start.

Meanwhile, PIR stock is dirt cheap. This company used to have earnings power of $1 per share. Even half of that earnings power (50 cents) would be huge for a $2 stock. At 50 cents per share in earnings power, it wouldn’t be unreasonable to see this stock hit $8 (a market-average 16x multiple).

Source: Shutterstock

Groupon (GRPN)

GRPN Stock Price: $3.63

Much like Pier 1, savings-king Groupon (NASDAQ:GRPN) feels like one of those companies that were loved yesterday but will be forgotten tomorrow. But, I don’t think that’s true. I get that the savings and deals market is commoditized now. I also understand that Groupon really isn’t a household name for coupons like it used to be.

But, I’m a numbers a guy. And the numbers are pretty good here. The customer base is actually still growing (up more than 2% year-over-year last quarter). Thus, global popularity of the Groupon platform is only growing.

Meanwhile, margins are improving thanks to management’s focus on higher-margin businesses. Operating expenses are also being removed from the system, so the company’s overall profitability profile is dramatically improving.

Aside from the numbers, Groupon launched an aggressive 2018 advertising campaign with hyper-relevant Tiffany Haddish that scored just shy of 100 million views. I think this campaign will have a long-term positive effect on usage, which could drive the stock higher.

I’m not a huge fan of the mobile gaming sector. It’s a tough space plagued with competition and low margins. Plus, competition is only building thanks to social media apps becoming increasingly multi-purpose.

But, mobile gaming company Zynga (NASDAQ:ZNGA) seems to have found the key to success in the mobile gaming world.

Zynga used to be a mega-popular browser game company with tons of users. But then the company overreached by branching into games that had heavy overlap with the traditional video game market, like sports titles. They couldn’t compete in that market. Eventually, the over-extension sparked user churn, and ZNGA stock spiraled downward.

That forced Zynga to re-invent itself into something much more relevant and defensible. They did just that. Zynga has transitioned its business model from web-focused to mobile-first while narrowing its gaming title focus. This pivot has streamlined operations, re-invigorated top-line growth, cut costs and improved profitability.

Consequently, the numbers supporting Zynga are pretty good. Mobile revenue growth was up 9%in the third quarter. Mobile bookings growth hit 23% year-over-year. The company also reported a huge audience of 22 million mobile daily active users (+10%) and 87 million mobile monthly active users (+9%).

From where I sit, this pivot appears to be in its early stages. Mobile is a secular growth narrative, and ZNGA has developed a gaming portfolio that is focused and tailored to that growth narrative. Thus, so long as mobile engagement heads higher, Zynga’s numbers should get better. Better numbers will inevitably lead to a higher stock price.

There is no hiding the fact that the defense sector is hot right now.

President Donald Trump came into office, upped the ante on defense and military spending, and in response, the whole world is spending more on defense and military.

Defense contractors win when this happens. That is why mega-cap defense contractors like Lockheed Martin (NYSE:LMT) and Boeing (NYSE:BA) have been on fire for the past several quarters.

But one micro-cap defense contractor that has missed out on this rally is Arotech (NASDAQ:ARTX). Over the past several years, the financials at Arotech haven’t gained any ground. Five years ago, revenues were $88 million and operating profits were $3.5 billion. Last year, revenues were $98 million and operating profits were $2.9 million.

In other words, profits haven’t risen in five years. When profits don’t go up, the stock tends not to go up. It is a simple relationship.

But, profits are stabilizing. When profits go from declining to stabilizing, they usually go to growth next.

And, when profits go up, stocks tend to go up.

As such, it looks like Arotech is finally joining the tide when it comes to big boosts in defense and military spending. This tide will inevitably lift Arotech’s earnings power substantially, and ARTX will rally as a result.

Source: Shutterstock

Blink Charging (BLNK)

BLNK Stock Price: $1.73

When it comes to cheap stocks, there are few as volatile as Blink Charging (NASDAQ:BLNK).

Over the past two years, BLNK stock has gone from $30 to $5, and popped from $5 to $15 … it now sits at a paltry $1.73. This volatility won’t give up any time soon. Thus, if you want to avoid volatility, I’d say avoid BLNK stock.

That being said, if this company’s secular growth narrative surrounding building a network of electric vehicle charging stations globally materializes within the next five years, this stock could be a 5-to-10 bagger.

It is a big risk. But, eventually, global infrastructure will need to match demand. At that point in time, there will be some huge contracts awarded to electric vehicle charging station companies.

Will Blink be one of them? Perhaps. Tough to tell. But if they do land some big contracts, this stock could have another huge pop in a short amount of time.

As of this writing, Luke Lango was long FB, PIR, GRPN and ARTX.

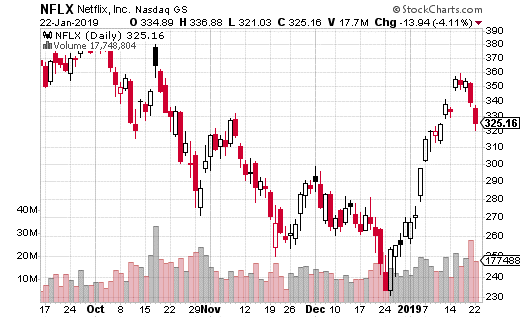

The FANG stocks can be quite polarizing for investors, and Netflix (NASDAQ: NFLX) is no exception. The streaming video giant (and the N in FANG) also may be the most volatile of the four. You can usually count on it for some action every few weeks or so.

Of course, NFLX just posted earnings so there was bound to be a lot of volatility associated with the event. But even before earnings, the stock had been plenty active. As you can see from the chart, there’s over a hundred point range in less than a month.

Last earnings period in 2018, NFLX beat earnings substantially. But, poor market conditions (and a high valuation) led to a steep decline in the share price. The drop ended and the reversal began right at the end of the year. Since that time, the stock has mostly gone straight up until just recently pulling back.

Along with momentum from the stock market recovery, NFLX headed higher in January due to higher viewership numbers. And then, the company announced it would be raising prices. Since NFLX appears to be a fairly inelastic good, most customers will continue their subscriptions after the price hike. That means a bigger bottom line for the company.

On the other hand, the recent earnings news wasn’t stellar. The results weren’t exactly disappointing, but they don’t blow away expectations either. And, the company’s high cash flow needs are a clear reason why raising subscription prices had to take place.

So what’s in store for NFLX next? Let’s take a look at the options action…

A well-capitalized trader just made an expensive bullish bet on NFLX that expires in April. The trader purchased the April 320-330 call spread (buying the 320 call and selling the 330 at the same time) for $5.40 with the stock price at $321.90. The trade was executed 2,680 times for a total cost of $1.4 million.

The cost of the trade, the $1.4 million in premium, is the max risk on the trade. The trade breaks even at $325.40, and can achieve max gain at $330 or above by April. The $4.60 in max gains translates to $1.2 million in profits, or 85% gains.

Now, it may seem like $1.4 million is a lot to spend to only make 85% – at least for a volatile stock like NFLX. However, keep in mind that the trade is already in the money. There’s $1.90 in intrinsic value already in the spread, so really the trader is only paying an extra $3.50 for the position. Moreover, being in the money substantially increases the probability of the trade’s success.

This is an expensive call spread on NFLX, but it has 3 months to expiration and is higher probability than most large call spreads you’ll see. If you are bullish on NFLX, this is a reasonable idea for a trade if you have a bit more money to spend on premiums.