Still feeling the taxman’s sting from April? Then you probably need to consider getting some tax-free income.

Having an income stream the IRS can’t touch may sound like pie in the sky, but it’s a reality if you hold municipal bonds. That’s because the tax code provides an exclusion for these bonds, allowing most US investors to collect interest payments from them tax-free. And in many states, income from those bonds is exempt from state taxes, as well.

If you aren’t intrigued yet, then let me show you some numbers—and what they could mean to your portfolio.

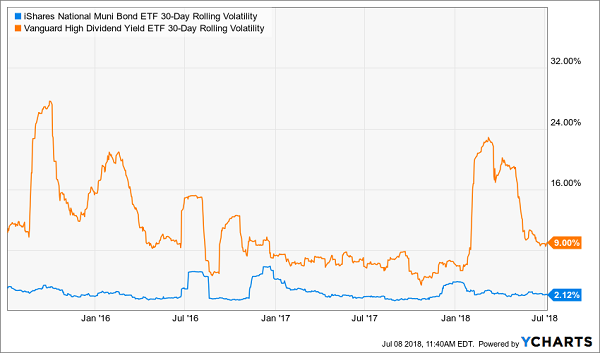

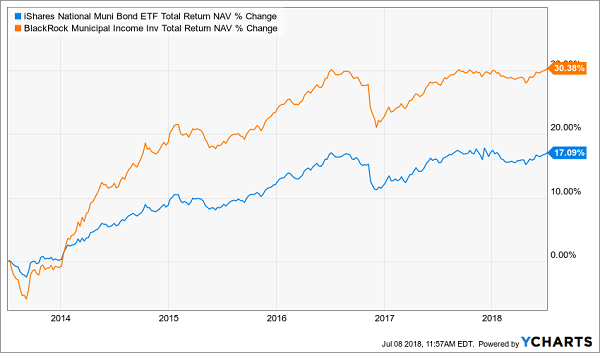

If you’re in the highest tax bracket (37%) and you get a 6%-yielding municipal-bond fund, that income is the exact same as a 9.5% dividend from stocks. And municipal bonds are nowhere near as volatile as high-yield stocks. Just compare the volatility of the iShares National Muni Bond ETF (MUB) and the Vanguard High Dividend Yield ETF (VYM):

A Smoother Ride Makes Withdrawals Easier

Not only does this lower volatility give you peace of mind, but it also makes withdrawing from your principal easier in cases of emergency.

There’s just one problem—MUB yields a paltry 2.4%!

But have no fear—I’m going to show you 3 closed-end funds (CEFs) that yield far more than that and are still tax-free. Before I get to them, though, let me tell you why you should choose these funds, and why now is the time to jump in.

Why Muni CEFs—and Why Now

One of the biggest benefits of closed-end funds is how inefficient they are. It sounds crazy, but CEFs cater to retail investors, who often just don’t know how far apart these funds’ market prices are from their their net asset values (NAVs), resulting in big discounts for a lot of CEFs.

In fact, the average CEF now trades at a 6.3% discount to its NAV—which is near the biggest average discount over the last year.

But some CEFs are more heavily discounted than others, while some actually trade at a premium—or for more than what their portfolios are worth. That risk of overpaying is why you can’t just choose any CEF.

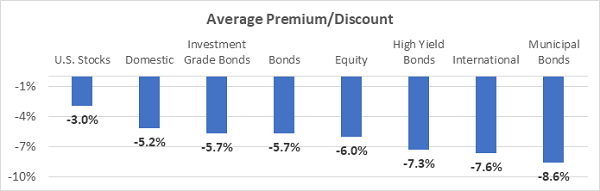

The most interesting trend in CEFs over the last few months has been the shrinking discount to NAV among equity funds and the growing discount among bond funds—but nowhere is the discount bigger than among municipal-bond funds. Take a look:

Big Discounts in Muni Funds Create Buying Opportunities

Source: CEF Insider

With the average discount among muni-bond CEFs at 8.6% (which is near double the 5.3% average discount of just a year ago, by the way), these funds offer us an incredible buying opportunity right now.

And while a few discounts in US-stock CEFs are still there, the recovering market that I predicted back in April means that the oversold equity funds I showed you back then aren’t so cheap anymore, so we need to get a bit creative.

Which is why muni-bond funds are the “it” thing to buy right now.

For one, with their unusually large discounts, muni funds are finding it easier to sustain their dividend payments, providing us with a safer income stream. Also, despite popular belief, municipal bonds do not go down during periods of rising interest rates.

In fact, this “rates up, muni bonds down” myth is a big driver of why muni-bond CEFs are so cheap now, again giving contrarians like us an opportunity to get tax-free income at a heavy discount.

Don’t believe me? Take a look at this chart from the mid-2000s, when the Federal Reserve increased interest rates by over 400%:

Interest Rates Rise—and so Do Muni Bonds

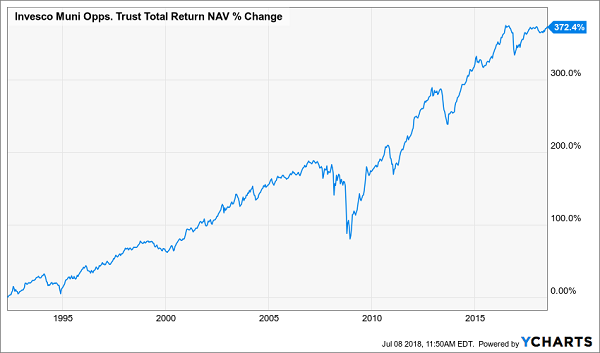

That blue line is the Invesco Municipal Opportunity Trust (VMO), the first pick I want to show you today. It’s a 5.7% yielder full of tax-free muni bonds that went up a full 17% during the last sustained rate-hike cycle.

And it’s unusually cheap now: its 10.8% discount to NAV is massive on its own, but it’s even more attractive when you consider that VMO’s discount has averaged just 2.3% in the last decade.

On top of that, VMO is managed by Invesco, one of the world’s biggest fund companies, with over $950 billion in assets under management (AUM). So you can count on this fund being reliable and secure.

Additionally, VMO has a long history. It’s been around since the early ’90s and has delivered consistently strong results since then—surviving the dot-com bubble bursting, the subprime mortgage crisis and all the drama in between:

A Steady Long-Term Performer

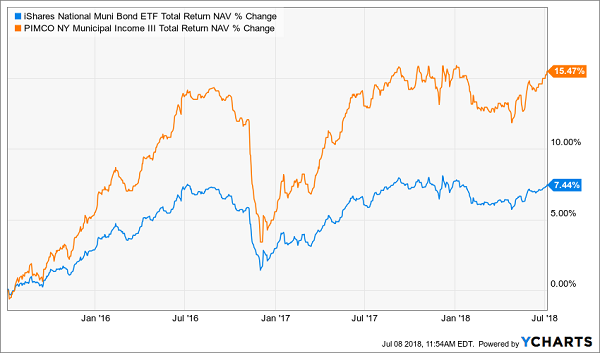

Which brings me to my second big yielder worth considering: the PIMCO NY Municipal Income III Fund (PYN), a 5.9% payer managed by one of the most respected names in the bond world: PIMCO, with $1.8 trillion in assets under management—more than the GDP of several small countries!

PIMCO built those assets through outperformance, which is why most of the company’s CEFs tend to trade at premiums to NAV.

PYN, however, is different. With a 2.6% discount to NAV, this fund is trading for less than the value of the assets in its portfolio—something it hasn’t done since 2009! And there’s no reason for it to trade so cheap, since PYN has doubled the return of its benchmark, MUB, since the Federal Reserve started raising interest rates in late 2015:

A Huge Overachiever

With such a track record, expect this one to trade at a premium to NAV soon. But there’s one other thing that makes PYN attractive: its size, or lack thereof.

Because PYN has just $51 million in AUM, it’s simply too small for a lot of large institutional investors—and that small size means that it’s incredibly inefficient, even by CEF standards. That’s why this fund typically has traded for a premium to NAV for most of the last decade, making its recent discount that much more appealing.

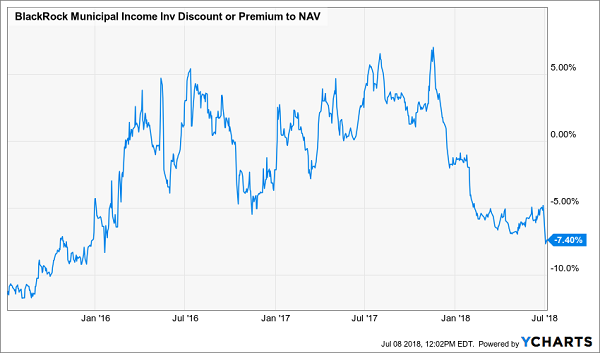

The last fund I want to show you is the BlackRock Municipal Income Investment Trust (BBF), which commands attention thanks to its 6.1% yield.

But that’s not the best thing about this fund. Like PYN, BBF is really small, with just $142.2 million in AUM, which is about a quarter of the size of most muni CEFs. And that small size results in mispricings that don’t reflect its stellar track record.

Another Big Winner

As you can see, the BlackRock Municipal Income Investment Trust has beaten the index for a very long time (this chart just covers five years, but since the fund’s inception in 2007, BBF has returned 79.3% versus MUB’s 50% over the same period).

I may be burying the lead here, though; the really nice thing about BBF is its manager: BlackRock, the largest investment firm in the world, with a staggering $6.3 trillion in assets under management. That means it has the connections to get the best municipal bonds as soon as they go IPO, the best minds and technology to analyze those municipal bonds and the best market position to trade those bonds most profitably.

Is this corporate heft priced in to BBF? Hardly. It’s trading at a massive 7.4% discount to NAV, after trading at a premium for most of the last three years:

BBF Suddenly Very Cheap

Should we expect this premium to NAV to come back? The short answer is yes. The discount only showed up—and steepened—in the last few months due to the market panic of the last few months.

But the market is getting more comfortable, which will likely result in BBF returning to its normal high price—giving those of us who buy today some tidy capital gains on top of that massive 6.1% income stream.

This CEF Doubled the Market and Pays 7.8% in Cash!

There’s no doubt that in a few months we’ll look back at the selloff in muni bonds and recognize it for the terrific buying opportunity it was. So don’t miss your chance to lock in the safe, tax-free payouts muni-bond funds offer now—while you can still get them cheap.

Here’s something else you should know: “munis” aren’t the only assets to be hit by the silly (and wrong) investor myth that rising rates are a bad-news story.

Another? High-yield real estate investment trusts (REITs).

And just as I showed you with VMO above, REITs also do great when rates head higher—contrary to what most folks believe.

Check out how the benchmark REIT ETF, the Vanguard REIT ETF (VNQ) did in the last sustained rising-rate period:

Rates Rise, REITs Surge

That makes now a terrific time to buy this unloved asset class, too. But just as we did with muni-bond funds, we’re going to take a pass on the popular REIT ETF and go with my top CEF pick in the sector.

Why?

For one, my No. 1 REIT CEF pick fund hands us an outsized 7.8% CASH dividend today. And talk about stable: it not only survived the financial crisis, it rebounded far more quickly than the market and has gone on to hand investors far bigger gains since.

An All-Star Management Team in Action

And keep in mind that this fund posted these incredible returns while investing in real estate: the very thing that caused the collapse in the first place!

Think about that for a moment.

This fund not only more than DOUBLED the market’s gain—even when you factor in the Great Recession and the subprime mortgage crisis—but its incredible management team did it while paying a rock-solid 7%+ dividend the whole time!

If this isn’t a fund worth paying a premium for, I don’t know what is. But thanks to the wacky mispricings in CEF land, this one’s trading at an absurd discount to NAV today.

Once the herd catches on to what it’s missing, this fund could easily blow into premium territory.

How do I know? Because it’s happened many times in the past—and when it does again, we’ll easily be sitting on an easy 20% gain, on top of this fund’s juicy 7.8% dividend payout.

Please don't make this huge dividend mistake... If you are currently investing in dividend stocks – or even if you think you MIGHT invest in any dividend stocks over the next several months – then please take a few minutes to read this urgent new report. Not only could it prevent you from making a huge mistake related to income investing, it could also help you earn 12% a year from here on out! Click here to get the full story right away.

Source: Contrarian Outlook