Yes, the markets are getting hammered like it’s 2008. But this isn’t because the world is coming to an end, or that the global economic system is about to fail.

This is about transition and risk.

The markets are undergoing a significant amount of transition as most central banks are relinquishing control over monetary policy and letting the markets sort it out. Add to that issue the fact that the Brexit mess is affecting one of the major global currencies.

There’s the fact that the U.S. economy continues to show signs of recovery — job growth is very strong, the participation rate is rising and wages are also increasing. Yet rising interest rates, the trade wars with Europe and China make that footing weaker.

For every bit a good news, there’s the shadow of bad news and the markets have never been a fan of uncertainty.

That’s why now is a great time to check out these nine A-rated safety stocks for a grossly oversold market. They’re highly rated in my Portfolio Grader, and with patience as the watchword now, these great stocks are selling at great prices.

Mr Cooper Group (COOP)

Mr Cooper Group (NASDAQ:COOP) may not be a household name — unless, of course you use it to start your household. It basically acquires companies that are focused on servicing, origination and transaction-based services for single family homes in the U.S. Its two biggest brands are Mr Cooper and Xome. It’s the leading non-bank mortgage servicer in the U.S.

This is one market that has been on both sides of the interest-rate roller coaster. When rates were high, home sales slowed, but when rates started to fall because of fears about the economy, that helped boost home sales and refinancings.

Its recent purchase of IBM’s (NYSE:IBM) Seterus mortgage servicing platform adds $24 billion of mortgages and 300,000 new customers to it rolls. It’s COOP’s second major purchase in 3 months.

Once this bumpy ride smooths, COOP will be well positioned.

Popular (BPOP)

Popular (NASDAQ:BPOP) is a holding company that operates financial institutions in the U.S., U.S. Virgin Islands and Puerto Rico. Its parent is Banco Popular de Puerto Rico, which was established in 1893.

Popular opened in the Bronx over 50 years ago and now has U.S. branches in New York, New Jersey and South Florida. Given the amount of Puerto Ricans that call the U.S. home, as well as other Latinos that are drawn by the bank’s roots in the Hispanic culture, BPOP offers a unique opportunity to take advantage of the demographic growth in this sector of the economy with an experienced, successful company.

Up 37% in the past year, and still delivering a 2.1% dividend yield, BPOP is doing very well in all this turmoil.

Medical Properties Trust (MPW)

Medical Properties Trust (NYSE:MPW) is the only medical real estate investment trust (REIT) that focuses solely on acute care facilities and hospitals where patients must be admitted by doctors.

Its goal is to blend the best of quality healthcare delivery and cost-effective management by maximizing operations management.

MPW started in 2003 and now sports a nearly $6 billion market cap. What’s more, it was up 17% in the past year, and that doesn’t include its generous 6.2% dividend.

It has recently moved into Europe with a big, multi-billion-dollar deal with a healthcare firm in Germany.

Qualys (QLYS)

Qualys (NASDAQ:QLYS) has done well in the past year, given the fact that it’s a tech stock.

But most of the credit goes to the fact that it’s a tech stock in the cybersecurity sector, and while that sector may have gotten a bit overpriced, it’s still something that is always in demand.

QLYS focuses on cloud security, which is one of the most in-demand aspects of cybersecurity since the growth in mobility and bandwidth demand have increased substantially. And the introduction of a new generation of data delivery — 5G — will make security even more important.

Also, with a market cap around $2.7 billion, QLYS is a tempting morsel for larger tech firms looking to expand their game in this space without having to build out from scratch.

Axon Enterprise (AAXN)

Axon Enterprise (NASDAQ:AAXN) is the new name for the TASER company, the folks that brought us the stun gun.

If you recall, a few years back there was an alarming number of fatalities linked to use of TASERs by law enforcement and others. Whether it was due to lack of training or abuse, the stain was largely put on the company.

But the name change as well as the company’s diversification into body-worn cameras for law enforcement has built a new line of products that have helped it diversify and regain its reputation as a reliable, non-lethal protection tool for professionals and citizens.

AAXN is up 71% in the past year and there is every reason to believe that kind of growth is achievable moving forward.

DSW (DSW)

DSW (NYSE:DSW), a big-box discount shoe retailer with more than 500 stores in the U.S., had great Q3 earnings and also raised its guidance for Q4. That happened at the beginning of December.

This is one of those brands that actually became stronger during the recession because that lost decade brought people in who weren’t regular customers previously.

There are two types of regular shoppers — the ones who go in like it’s a treasure hunt, looking for bargains on great shoes and the ones that like the fact that there’s a huge selection to choose from.

During slow economic times, everyone is looking for a deal and DSW is one of the beneficiaries. But now as times improve, it has added to its regular shoppers and instead of returning to premium stores, many shoppers choose to stick with DSW.

It’s why the stock is up 20% in the past year and still delivers a 3% dividend.

Evertec (EVTC)

Evertec (NYSE:EVTC) is the leading payment processing company in Latin America. It operates in 26 Latin American companies, including Mexico and the Caribbean.

Financial technology, or “fintech” is a huge force in the way financial institutions are transitioning from the old style of banking, to the new digital style. And this affects every aspect of the business, especially between the financial institutions and the businesses that they support.

And these digital standards are especially important in emerging markets, where a traditional financial infrastructure can be tough to come by.

EVTC is up over 100% in the past year and is still only trading at a P/E of 29. There is plenty of growth left in the tank.

Brinker International (EAT)

Brinker International (NYSE:EAT) owns the Chili’s Grill and Bar and Maggiano’s Little Italy chains. Most of the restaurants are company owned, although Chili’s does franchise some of its properties.

There has been a shift in tastes among customers and these large restaurant chains have begun appealing to new generations of potential diners. Healthier meals, different pricing structures, etc all have been implemented to keep the new breed of diners happy.

Some have had a tough time transitioning, but EAT has not been one of them. Up 15% in the last year, it also delivers a respectable 3.3% dividend.

Aerojet Rocketdyne Holdings (AJRD)

Aerojet Rocketdyne Holdings (NYSE:AJRD) is a second-tier aerospace and defense contractor. Basically, that means it usually is a subcontractor to the big defense names when it comes to building rockets, propulsion and guidance systems. It also has a long relationship with NASA and other aerospace organizations.

While there is a lot of talk about private aerospace firms entering into the market, the fact is, there is huge potential for the best companies. And given the amount of aerospace work that lies ahead, AJRD will be a major player.

With talk of near-space commercial travel as well as missions to Mars, AJRD will have plenty of work. And the fact that it has been around in various iterations since 1914 shows that it knows how to adapt and thrive.

This ‘Overlooked’ Sector Produced the Biggest Winners of the Last DecadeWall Street is oblivious to it, yet you can earn 2,537% profits from an overlooked "blue chip" sector. The same group of stocks that has produced some of the biggest winners of the last 10 years.

Investors have earned 618%, 834%, and up to 2,500% - performing better than Amazon, Netflix and Facebook.

Click here to get in on your own 2,537% windfall.

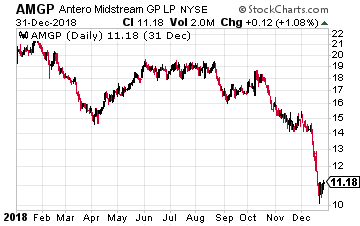

Antero Midstream GP LP (NYSE: AMGP) is an energy midstream services company in transition. The company came to market with a May 2017 IPO. The assets at that time were general partner incentive distribution rights (IDR) ownership interest in high growth, midstream MLP, Antero Midstream Partners (NYSE: AM). The MLP was sponsored and controlled by Marcellus natural gas producer Antero Resources (NYSE: AR).

Antero Midstream GP LP (NYSE: AMGP) is an energy midstream services company in transition. The company came to market with a May 2017 IPO. The assets at that time were general partner incentive distribution rights (IDR) ownership interest in high growth, midstream MLP, Antero Midstream Partners (NYSE: AM). The MLP was sponsored and controlled by Marcellus natural gas producer Antero Resources (NYSE: AR). Starwood Property Trust, Inc. (NYSE: STWD) is a finance REIT whose primary business is the origination of commercial property mortgages. As one of the largest players in the field, Starwood Property trust focuses on making large loans with specialized terms. This gives them a competitive advantage over banks and smaller commercial finance REITs.

Starwood Property Trust, Inc. (NYSE: STWD) is a finance REIT whose primary business is the origination of commercial property mortgages. As one of the largest players in the field, Starwood Property trust focuses on making large loans with specialized terms. This gives them a competitive advantage over banks and smaller commercial finance REITs.